Key Insights

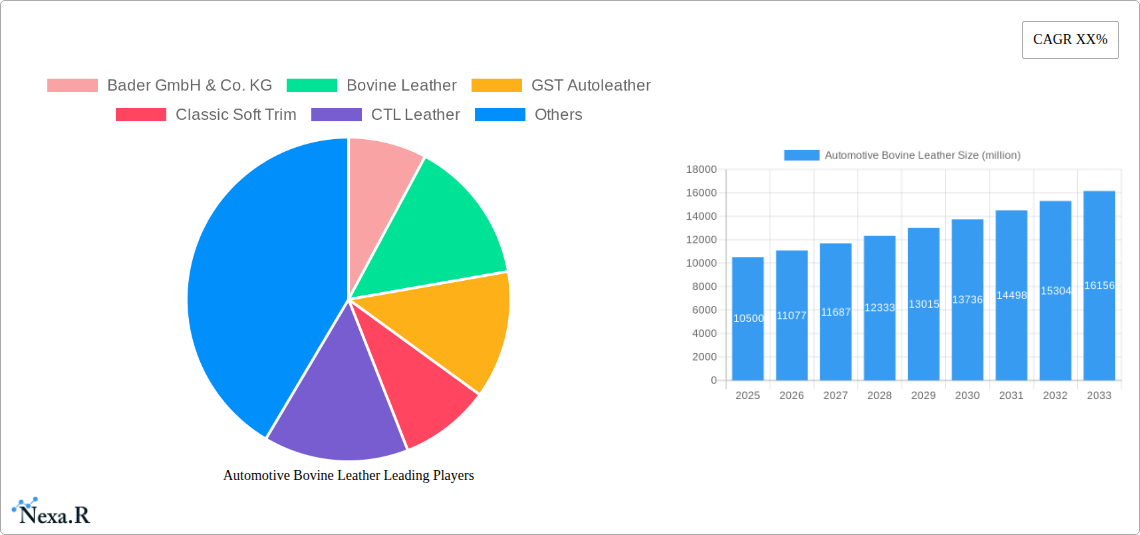

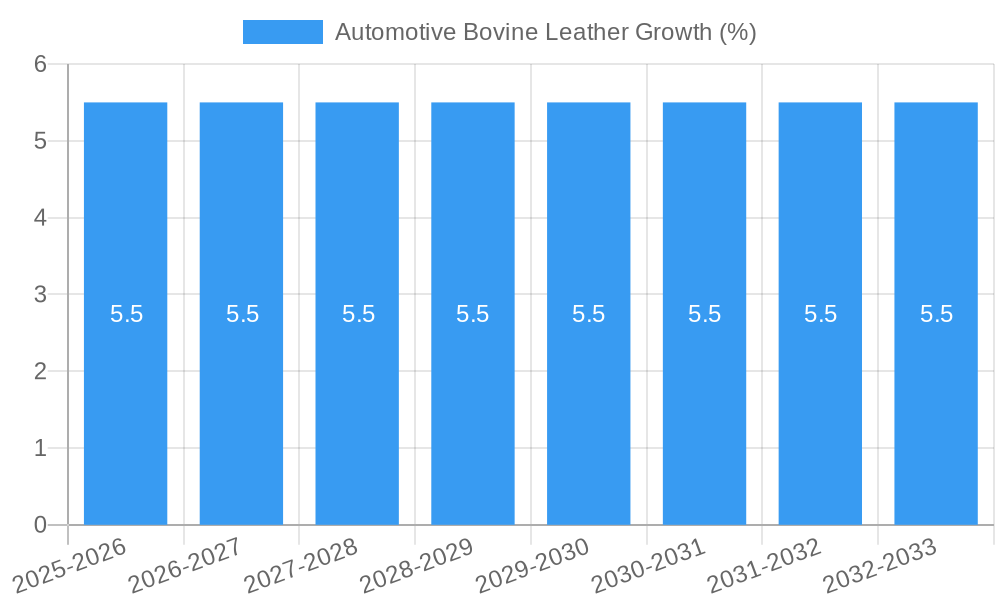

The global automotive bovine leather market is poised for robust expansion, projected to reach an estimated market size of approximately USD 10,500 million by 2025, with a Compound Annual Growth Rate (CAGR) of around 5.5% expected through 2033. This growth is primarily fueled by the increasing demand for premium interiors in passenger vehicles and the rising production of commercial vehicles that increasingly opt for durable and aesthetically pleasing leather upholstery. The inherent qualities of bovine leather, such as its durability, comfort, and luxurious appeal, continue to make it a preferred material for automotive applications, especially in the mid-to-high end segments. The market is witnessing a significant trend towards sustainable and ethically sourced leather, with manufacturers investing in greener tanning processes and circular economy initiatives to cater to environmentally conscious consumers and stringent regulations. Innovations in leather treatments and finishes are also contributing to its appeal, offering enhanced scratch resistance, UV protection, and ease of maintenance, thereby extending the lifespan and aesthetic integrity of automotive interiors.

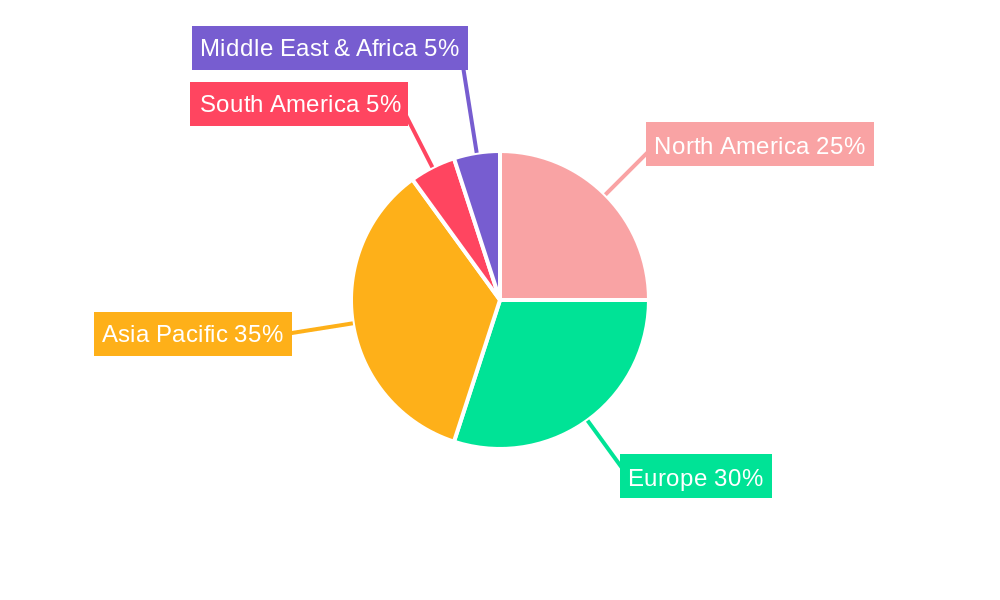

The market's trajectory is further supported by evolving consumer preferences for personalized and sophisticated vehicle interiors. This has led to a surge in demand for custom upholstery, seat covers, and dashboard trims, where bovine leather plays a pivotal role. Geographically, Asia Pacific, particularly China and India, is emerging as a key growth engine due to the rapid expansion of its automotive manufacturing sector and a burgeoning middle class with a taste for premium vehicles. North America and Europe remain significant markets, driven by established automotive industries and a strong emphasis on vehicle quality and luxury. While the widespread adoption of electric vehicles (EVs) might introduce new material considerations, the inherent demand for comfort and luxury in automotive cabins suggests a continued, albeit potentially evolving, role for bovine leather. Challenges such as the fluctuating raw material prices and competition from synthetic alternatives necessitate continuous innovation and strategic sourcing to maintain market dominance. However, the enduring appeal and established infrastructure supporting bovine leather production are expected to ensure its sustained relevance in the automotive sector.

Here is a compelling, SEO-optimized report description for Automotive Bovine Leather, integrating high-traffic keywords and market structure as requested.

Automotive Bovine Leather Market Dynamics & Structure

The global Automotive Bovine Leather market exhibits a moderate to high concentration, with key players like Bader GmbH & Co. KG, GST Autoleather, Classic Soft Trim, CTL Leather, Eagle Ottawa (Lear Corporation), and Gruppo Mastrotto dominating the supply chain. Technological innovation is a significant driver, particularly in developing advanced treatments for durability, aesthetics, and sustainability, addressing increasing demand for premium interiors. Regulatory frameworks, such as emissions standards and material safety regulations, indirectly influence the adoption of leather alternatives and sustainable leather processing. Competitive product substitutes, including high-quality synthetics and advanced textiles, present a constant challenge, necessitating continuous product development and differentiation in the automotive leather sector. End-user demographics, especially the growing affluent class in emerging economies and the demand for luxury features in passenger vehicles, are shaping market preferences. Mergers and acquisitions (M&A) are observed as companies seek to expand their geographical reach, enhance their product portfolios, and secure raw material supply.

- Market Concentration: Moderately consolidated with dominant global suppliers.

- Technological Innovation: Focus on enhanced durability, comfort, and sustainable processing.

- Regulatory Influence: Indirect impact via emissions, safety, and material sourcing standards.

- Competitive Substitutes: Advanced synthetics and high-performance textiles.

- End-User Demographics: Driven by luxury demand in passenger vehicles and emerging market growth.

- M&A Trends: Strategic acquisitions to expand market share and capabilities.

Automotive Bovine Leather Growth Trends & Insights

The global Automotive Bovine Leather market is poised for robust growth, projected to reach a value of $xx.x billion by 2033, expanding from an estimated $xx.x billion in 2025. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of xx.x% during the forecast period of 2025–2033. The increasing production of passenger vehicles, coupled with a rising consumer preference for premium and luxurious automotive interiors, is a primary catalyst. Technological advancements in leather processing, such as advanced tanning techniques and the development of more sustainable and eco-friendly materials, are enhancing the appeal and applicability of bovine leather in automotive segments. Furthermore, the shift towards SUVs and premium car models, where leather upholstery is a sought-after feature, directly contributes to market expansion. Consumer behavior is evolving, with a greater emphasis on perceived quality, comfort, and the tactile experience that only natural leather can provide. The adoption rates of bovine leather in both traditional and new automotive applications are expected to climb as manufacturers continue to integrate these materials to elevate their vehicle offerings. The historical period from 2019 to 2024 saw steady growth, with the market valued at $xx.x billion in 2024, setting a strong foundation for future expansion. The base year of 2025 is critical for establishing current market benchmarks and projecting future trajectories with precision.

Dominant Regions, Countries, or Segments in Automotive Bovine Leather

The Passenger Vehicles segment is the undeniable dominant force within the global Automotive Bovine Leather market, accounting for an estimated xx% of the total market value in 2025. This dominance is driven by several interconnected factors, including the sheer volume of passenger car production worldwide and the inherent consumer demand for luxury, comfort, and durability in these vehicles. The Upholstery/Seat Covers application within this segment commands the largest share, estimated at xx% of the bovine leather market in 2025, as it is the most visible and tactile component of a vehicle's interior. North America, particularly the United States, and Europe, led by Germany, remain the leading regional markets. This is attributed to established automotive manufacturing hubs, a high concentration of premium vehicle manufacturers, and affluent consumer bases with a strong preference for high-quality leather interiors. The economic policies in these regions, supportive of the automotive industry and luxury goods, further bolster demand. Infrastructure supporting advanced manufacturing and a well-established supply chain for automotive leather processing also contribute to their leadership. The growth potential in emerging economies, especially in Asia-Pacific, is substantial, with countries like China and India showing increasing adoption rates due to rising disposable incomes and a growing middle class aspiring to premium automotive experiences. While Heavy Commercial Vehicles and Light Commercial Vehicles represent niche markets, their demand for durable and high-performance leather for specific applications like driver seats and interior trim is also contributing to the overall market growth, albeit at a slower pace than passenger vehicles. The forecast period 2025–2033 is expected to see sustained leadership from the passenger vehicle segment, with continued innovation in sustainable leather solutions to meet evolving consumer and regulatory demands.

- Dominant Segment: Passenger Vehicles (estimated xx% market share in 2025).

- Leading Application: Upholstery/Seat Covers (estimated xx% of bovine leather market in 2025).

- Key Regions: North America and Europe, driven by manufacturing and consumer preference.

- Emerging Markets: Asia-Pacific showing significant growth potential.

- Growth Drivers: High vehicle production volumes, luxury demand, and evolving consumer preferences.

Automotive Bovine Leather Product Landscape

The Automotive Bovine Leather product landscape is characterized by continuous innovation aimed at enhancing aesthetics, durability, and sustainability. Manufacturers are developing advanced leather finishes that offer superior scratch resistance, UV protection, and stain repellency, crucial for automotive applications. Innovations include the development of low-VOC (Volatile Organic Compound) tanning processes and the use of natural dyes, aligning with increasing environmental consciousness among consumers and stricter regulations. Furthermore, advancements in laser perforation and stitching technologies allow for more intricate designs and improved breathability in seat covers and steering wheels. The performance metrics focus on tensile strength, abrasion resistance, and colorfastness, ensuring longevity and a premium feel throughout the vehicle's lifespan. Unique selling propositions lie in the natural feel, breathability, and premium look that bovine leather offers, differentiating it from synthetic alternatives.

Key Drivers, Barriers & Challenges in Automotive Bovine Leather

The Key Drivers propelling the Automotive Bovine Leather market forward are primarily the escalating demand for premium and luxury vehicles, where leather interiors are a significant differentiator. Technological advancements in tanning and finishing processes, leading to more durable, comfortable, and aesthetically pleasing leather, also act as strong drivers. Growing consumer awareness regarding the natural, breathable, and sustainable aspects of genuine leather, when processed responsibly, further fuels demand. Economic growth in emerging markets translates to increased purchasing power and a greater desire for higher-value automotive features.

Key Barriers and Challenges include the fluctuating prices of raw hides, which can impact profitability and lead to increased material costs. The rising availability and improving quality of high-performance synthetic leather alternatives pose a significant competitive threat. Stringent environmental regulations concerning tanning chemicals and wastewater disposal necessitate substantial investment in sustainable processing technologies. Supply chain disruptions, as witnessed in recent global events, can affect the availability of raw materials and finished products. Additionally, ethical concerns and increasing demand for vegan alternatives present a growing challenge for the traditional leather industry. The overall market value is estimated to be impacted by these factors, potentially moderating growth to xx% in specific sub-segments.

Emerging Opportunities in Automotive Bovine Leather

Emerging opportunities within the Automotive Bovine Leather sector lie in the development of bio-based and recycled leather alternatives, catering to the burgeoning demand for sustainable automotive materials. The integration of smart technologies, such as embedded sensors for climate control or haptic feedback, within leather upholstery presents a novel avenue for innovation. Furthermore, expanding into the aftermarket for classic and vintage car restoration offers a niche but high-value market. The increasing focus on interior personalization allows for greater customization of leather finishes, colors, and textures, appealing to individual consumer preferences. The automotive industry's push towards electric vehicles (EVs) also presents an opportunity to develop specialized bovine leather that is lighter and more energy-efficient for EV interiors.

Growth Accelerators in the Automotive Bovine Leather Industry

Several catalysts are accelerating long-term growth in the Automotive Bovine Leather industry. Technological breakthroughs in chrome-free tanning and water-saving dyeing processes are significantly enhancing the sustainability profile of bovine leather, addressing environmental concerns and attracting eco-conscious automakers and consumers. Strategic partnerships between leather suppliers and automotive OEMs (Original Equipment Manufacturers) are crucial for co-developing innovative interior solutions and ensuring seamless integration of leather materials. Market expansion strategies, focusing on emerging economies with rapidly growing automotive sectors, will unlock new demand centers. The continuous drive towards higher vehicle segmentation, with an emphasis on luxury and comfort, directly translates to increased utilization of premium bovine leather.

Key Players Shaping the Automotive Bovine Leather Market

- Bader GmbH & Co. KG

- GST Autoleather

- Classic Soft Trim

- CTL Leather

- Eagle Ottawa (Lear Corporation)

- Gruppo Mastrotto

Notable Milestones in Automotive Bovine Leather Sector

- 2019: Increased focus on sustainable tanning methods and reduced chemical usage by leading manufacturers.

- 2020: Emergence of advanced finishing techniques for enhanced durability and stain resistance in automotive leather.

- 2021: Growing adoption of low-VOC leather options to meet stringent emission standards.

- 2022: Strategic partnerships formed to develop innovative and lightweight leather solutions for electric vehicles.

- 2023: Significant investments in research and development for bio-based leather alternatives.

- 2024: Expansion of production capacities in emerging automotive markets to meet growing demand.

In-Depth Automotive Bovine Leather Market Outlook

The future of the Automotive Bovine Leather market is exceptionally promising, driven by a convergence of consumer desire for luxury and advancements in sustainable material science. Growth accelerators such as eco-friendly processing technologies and strategic collaborations between leather producers and automotive manufacturers are poised to redefine the industry landscape. The market is expected to witness continued expansion, driven by the increasing production of premium passenger vehicles and the growing demand for personalized interior designs. Strategic opportunities abound in the development of lightweight, durable, and aesthetically superior bovine leather that aligns with the evolving needs of the automotive sector, particularly in the burgeoning electric vehicle segment.

Automotive Bovine Leather Segmentation

-

1. Application

- 1.1. Passenger Vehicles

- 1.2. Heavy Commercial Vehicles

- 1.3. Light Commercial Vehicles

-

2. Types

- 2.1. Upholstery/Seat Covers

- 2.2. Doors

- 2.3. Dashboard and Headliners

- 2.4. Steering Wheel

- 2.5. Floor Mats/Carpets

- 2.6. Others

Automotive Bovine Leather Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Bovine Leather REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Bovine Leather Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Vehicles

- 5.1.2. Heavy Commercial Vehicles

- 5.1.3. Light Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Upholstery/Seat Covers

- 5.2.2. Doors

- 5.2.3. Dashboard and Headliners

- 5.2.4. Steering Wheel

- 5.2.5. Floor Mats/Carpets

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Bovine Leather Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Vehicles

- 6.1.2. Heavy Commercial Vehicles

- 6.1.3. Light Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Upholstery/Seat Covers

- 6.2.2. Doors

- 6.2.3. Dashboard and Headliners

- 6.2.4. Steering Wheel

- 6.2.5. Floor Mats/Carpets

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Bovine Leather Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Vehicles

- 7.1.2. Heavy Commercial Vehicles

- 7.1.3. Light Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Upholstery/Seat Covers

- 7.2.2. Doors

- 7.2.3. Dashboard and Headliners

- 7.2.4. Steering Wheel

- 7.2.5. Floor Mats/Carpets

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Bovine Leather Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Vehicles

- 8.1.2. Heavy Commercial Vehicles

- 8.1.3. Light Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Upholstery/Seat Covers

- 8.2.2. Doors

- 8.2.3. Dashboard and Headliners

- 8.2.4. Steering Wheel

- 8.2.5. Floor Mats/Carpets

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Bovine Leather Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Vehicles

- 9.1.2. Heavy Commercial Vehicles

- 9.1.3. Light Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Upholstery/Seat Covers

- 9.2.2. Doors

- 9.2.3. Dashboard and Headliners

- 9.2.4. Steering Wheel

- 9.2.5. Floor Mats/Carpets

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Bovine Leather Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Vehicles

- 10.1.2. Heavy Commercial Vehicles

- 10.1.3. Light Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Upholstery/Seat Covers

- 10.2.2. Doors

- 10.2.3. Dashboard and Headliners

- 10.2.4. Steering Wheel

- 10.2.5. Floor Mats/Carpets

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Bader GmbH & Co. KG

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Bovine Leather

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 GST Autoleather

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Classic Soft Trim

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 CTL Leather

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Eagle Ottawa (Lear Corporation)

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Gruppo Mastrotto

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.1 Bader GmbH & Co. KG

List of Figures

- Figure 1: Global Automotive Bovine Leather Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Automotive Bovine Leather Revenue (million), by Application 2024 & 2032

- Figure 3: North America Automotive Bovine Leather Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Automotive Bovine Leather Revenue (million), by Types 2024 & 2032

- Figure 5: North America Automotive Bovine Leather Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Automotive Bovine Leather Revenue (million), by Country 2024 & 2032

- Figure 7: North America Automotive Bovine Leather Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Automotive Bovine Leather Revenue (million), by Application 2024 & 2032

- Figure 9: South America Automotive Bovine Leather Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Automotive Bovine Leather Revenue (million), by Types 2024 & 2032

- Figure 11: South America Automotive Bovine Leather Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Automotive Bovine Leather Revenue (million), by Country 2024 & 2032

- Figure 13: South America Automotive Bovine Leather Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Automotive Bovine Leather Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Automotive Bovine Leather Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Automotive Bovine Leather Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Automotive Bovine Leather Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Automotive Bovine Leather Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Automotive Bovine Leather Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Automotive Bovine Leather Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Automotive Bovine Leather Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Automotive Bovine Leather Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Automotive Bovine Leather Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Automotive Bovine Leather Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Automotive Bovine Leather Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Automotive Bovine Leather Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Automotive Bovine Leather Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Automotive Bovine Leather Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Automotive Bovine Leather Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Automotive Bovine Leather Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Automotive Bovine Leather Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Automotive Bovine Leather Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Automotive Bovine Leather Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Automotive Bovine Leather Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Automotive Bovine Leather Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Automotive Bovine Leather Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Automotive Bovine Leather Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Automotive Bovine Leather Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Automotive Bovine Leather Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Automotive Bovine Leather Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Automotive Bovine Leather Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Automotive Bovine Leather Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Automotive Bovine Leather Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Automotive Bovine Leather Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Automotive Bovine Leather Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Automotive Bovine Leather Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Automotive Bovine Leather Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Automotive Bovine Leather Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Automotive Bovine Leather Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Automotive Bovine Leather Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Automotive Bovine Leather Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Bovine Leather?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Automotive Bovine Leather?

Key companies in the market include Bader GmbH & Co. KG, Bovine Leather, GST Autoleather, Classic Soft Trim, CTL Leather, Eagle Ottawa (Lear Corporation), Gruppo Mastrotto.

3. What are the main segments of the Automotive Bovine Leather?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Bovine Leather," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Bovine Leather report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Bovine Leather?

To stay informed about further developments, trends, and reports in the Automotive Bovine Leather, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence