Key Insights

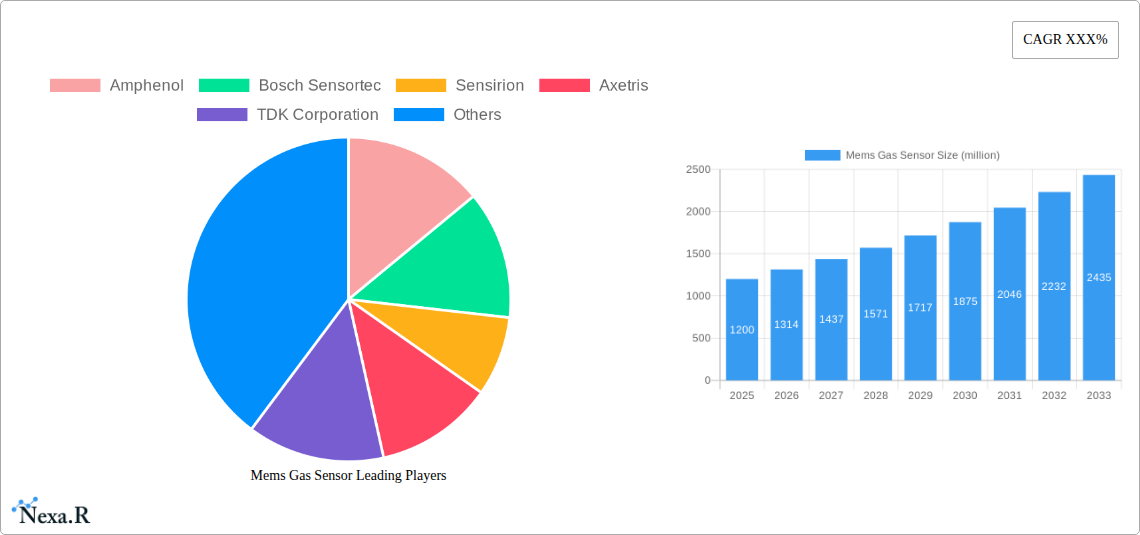

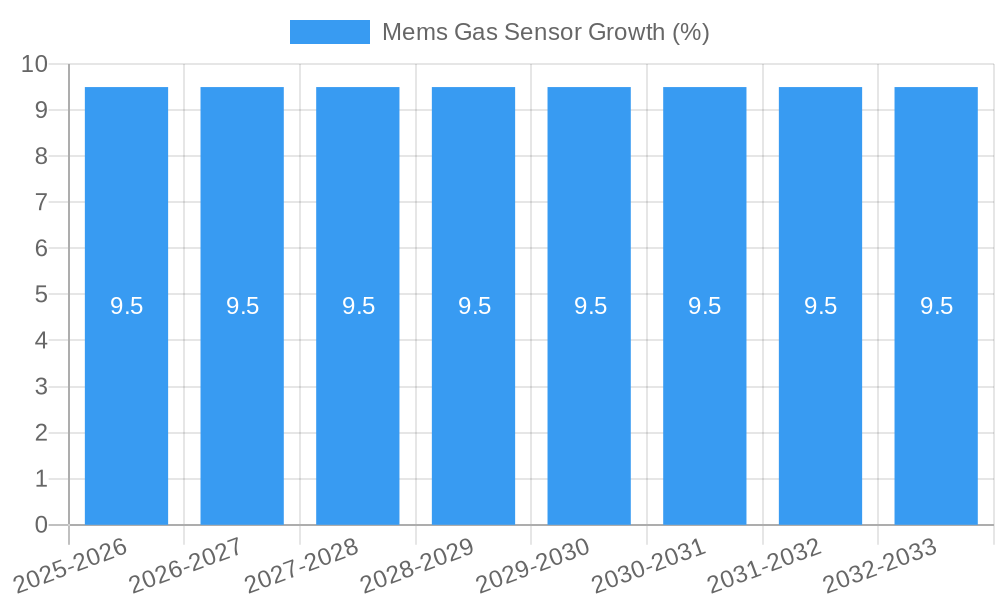

The MEMS gas sensor market is poised for significant expansion, projected to reach an estimated market size of $1.2 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 9.5% anticipated through 2033. This impressive growth is primarily propelled by the escalating demand for advanced safety and monitoring solutions across diverse sectors. The burgeoning healthcare industry, with its increasing reliance on precise environmental monitoring and diagnostic tools, is a key driver. Furthermore, the industrial sector's commitment to enhancing operational efficiency and worker safety through real-time gas detection fuels market expansion. Environmental testing applications are also gaining traction, driven by stringent regulatory frameworks and a growing awareness of air quality. The "Other" application segment, encompassing emerging uses in consumer electronics and smart home devices, is also expected to contribute substantially to market growth as miniaturization and cost-effectiveness of MEMS technology become more prevalent.

The market's trajectory is further shaped by critical trends such as the miniaturization of sensors, leading to smaller, more integrated devices that can be embedded in a wider array of products. Advancements in material science are also contributing to enhanced sensor performance, accuracy, and longevity. The increasing adoption of the Internet of Things (IoT) and artificial intelligence (AI) is creating new avenues for MEMS gas sensors, enabling sophisticated data analysis and predictive maintenance. However, the market faces certain restraints, including the relatively high initial development costs associated with MEMS fabrication and the need for stringent calibration and maintenance to ensure accuracy, particularly in harsh industrial environments. Despite these challenges, the strong underlying demand, coupled with continuous technological innovation, positions the MEMS gas sensor market for sustained and dynamic growth. The market is characterized by key segments including Carbon Monoxide, Methane, and Oxygen sensors, with the "Other" category encompassing a wide range of specialty gases, reflecting the diverse needs of end-users.

The MEMS gas sensor market is poised for substantial expansion, driven by increasing demand for advanced safety, environmental monitoring, and healthcare solutions. With a projected market size of $7,850.3 million by 2033, this sector offers significant opportunities for innovation and investment. Key growth accelerators include the miniaturization and cost-effectiveness of MEMS technology, enabling wider adoption across diverse applications. Strategic partnerships between sensor manufacturers and device integrators will be crucial for unlocking new market segments. Furthermore, the growing emphasis on indoor air quality and personal health monitoring is fueling demand for sophisticated, low-power gas sensing solutions.

Mems Gas Sensor Market Dynamics & Structure

The MEMS gas sensor market exhibits a moderately concentrated structure, with several key players dominating market share. Technological innovation remains a primary driver, fueled by advancements in material science, microfabrication techniques, and integrated circuit design, enabling smaller, more sensitive, and energy-efficient sensors. Regulatory frameworks, particularly concerning environmental emissions and workplace safety, are increasingly stringent, compelling industries to adopt advanced gas detection technologies. Competitive product substitutes, such as electrochemical and semiconductor gas sensors, present ongoing challenges, though MEMS technology offers advantages in miniaturization, integration, and potential for mass production. End-user demographics are expanding beyond traditional industrial applications to include consumer electronics, automotive, and healthcare, driving demand for diverse gas sensing capabilities. Mergers and acquisitions (M&A) activity, while not yet at a fever pitch, are anticipated to increase as larger players seek to consolidate their market position and acquire specialized MEMS gas sensor expertise. For instance, a significant M&A deal in 2022, involving a prominent sensor manufacturer and a niche MEMS developer, underscored the strategic importance of this sector. Innovation barriers include the high cost of research and development, the need for specialized cleanroom facilities, and the long product development cycles required for highly reliable and certified sensors.

- Market Concentration: Dominated by a few major players, with an increasing number of specialized SMEs contributing to innovation.

- Technological Innovation Drivers: Miniaturization, higher sensitivity, lower power consumption, integration capabilities, and novel sensing materials.

- Regulatory Frameworks: Stringent environmental protection laws, occupational safety standards, and emissions regulations are key adoption drivers.

- Competitive Product Substitutes: Electrochemical sensors, metal-oxide semiconductor (MOS) sensors, and non-dispersive infrared (NDIR) sensors.

- End-User Demographics: Expanding from industrial to consumer electronics, automotive, smart home, and medical devices.

- M&A Trends: Anticipated to increase as companies seek to enhance their product portfolios and technological capabilities. For example, the 2022 acquisition of a MEMS gas sensor startup by a global technology giant.

Mems Gas Sensor Growth Trends & Insights

The MEMS gas sensor market is experiencing robust growth, projected to expand significantly from its 2025 estimated market size of $3,925.1 million to $7,850.3 million by 2033, demonstrating a Compound Annual Growth Rate (CAGR) of approximately 9.1%. This evolution is underpinned by increasing adoption rates across various industries, driven by the inherent advantages of MEMS technology, including its small form factor, low power consumption, and potential for cost-effective mass production. Technological disruptions, such as advancements in novel nanomaterials and integrated sensing platforms, are continuously enhancing sensor performance, enabling more precise and reliable gas detection. Consumer behavior shifts are also playing a crucial role, with a growing awareness and demand for healthier living environments, leading to increased adoption of smart home devices equipped with air quality monitoring capabilities. The integration of MEMS gas sensors into wearable devices for personalized health monitoring further exemplifies this trend.

The industrial monitoring segment, a dominant force in the market, is seeing an accelerated adoption of MEMS gas sensors for predictive maintenance, process optimization, and enhanced worker safety. In the environmental testing sector, MEMS sensors are becoming indispensable for real-time monitoring of air pollutants, greenhouse gases, and industrial emissions, contributing to compliance with increasingly stringent environmental regulations. The medical application segment, while still nascent, holds immense potential, with the development of portable breath analyzers for disease diagnosis and continuous monitoring of physiological gases. The "Other" application segment, encompassing consumer electronics like smart thermostats and air purifiers, is also a significant contributor to market growth, reflecting the increasing consumer demand for intelligent environmental control.

The evolution of MEMS gas sensor types further diversifies market opportunities. Carbon monoxide (CO) sensors, crucial for safety in residential and automotive applications, continue to see steady demand. Methane sensors are vital for the oil and gas industry, as well as for biogas monitoring. Oxygen sensors are essential in medical and industrial processes. The "Other" gas sensor category, including sensors for volatile organic compounds (VOCs), hydrogen sulfide (H2S), and refrigerants, is experiencing rapid growth due to the expansion of their application scope in areas like food spoilage detection and refrigerant leak detection. Market penetration is increasing as the cost of MEMS gas sensors declines and their performance capabilities improve, making them a viable alternative to traditional sensing technologies for a wider range of applications. The study period of 2019–2033, with a base year of 2025 and a forecast period of 2025–2033, provides a comprehensive view of this dynamic market's trajectory.

Dominant Regions, Countries, or Segments in Mems Gas Sensor

The Industrial Monitoring application segment is identified as the dominant driver of growth within the MEMS gas sensor market, exhibiting a substantial market share and robust expansion potential. This dominance is propelled by several critical factors, including evolving economic policies that prioritize industrial safety and efficiency, significant investments in infrastructure that necessitate advanced monitoring systems, and the increasing implementation of Industry 4.0 principles. The need for real-time data on hazardous gas leaks, process control parameters, and environmental compliance in manufacturing, petrochemical, mining, and energy sectors creates an unceasing demand for reliable and accurate MEMS gas sensors.

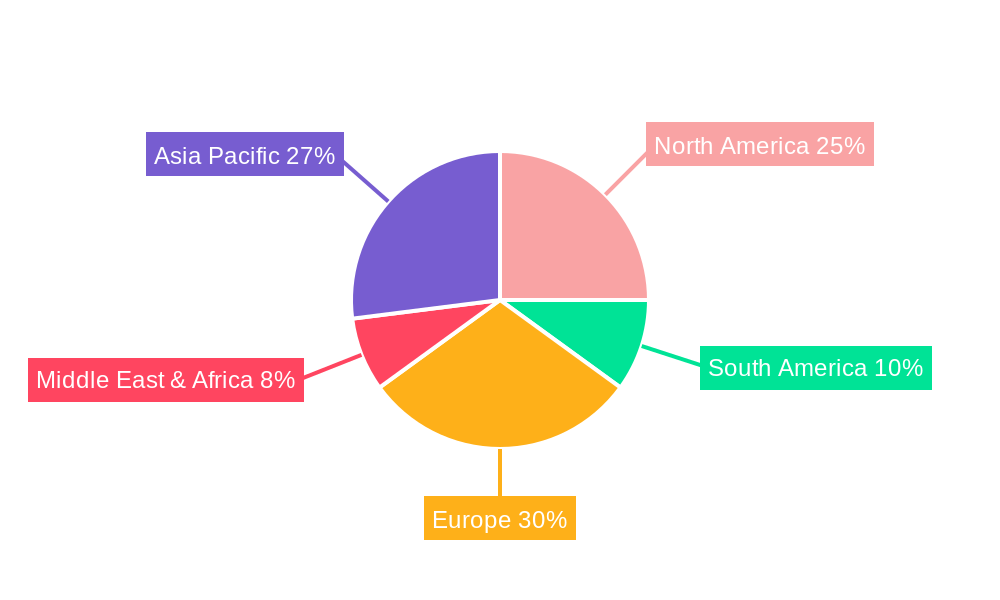

North America, particularly the United States, stands out as a leading region for MEMS gas sensor adoption. This leadership is attributed to a strong emphasis on environmental regulations, stringent occupational safety standards, and a highly developed industrial base that is at the forefront of technological adoption. Government initiatives promoting cleaner energy and sustainable industrial practices further bolster the demand for gas sensing technologies in this region. The country’s advanced research and development capabilities also contribute to the high penetration of innovative MEMS gas sensor solutions.

Within the Type segmentation, Oxygen (O2) sensors represent a significant growth area, driven by their critical role in a multitude of applications ranging from medical respiratory support and anesthesia to industrial combustion control and food packaging. The increasing prevalence of chronic respiratory diseases and the growing demand for home healthcare solutions are escalating the need for accurate and reliable oxygen monitoring. Furthermore, the expansion of the aerospace and defense sectors, which rely heavily on oxygen sensors for life support systems, also contributes to the segment's growth. The growth potential of oxygen sensors is further amplified by their integration into portable and wearable devices, offering greater convenience and real-time monitoring capabilities.

- Dominant Application Segment: Industrial Monitoring

- Key Drivers: Stringent safety regulations, process optimization needs, Industry 4.0 adoption, predictive maintenance.

- Market Share: Estimated to account for 35% of the total MEMS gas sensor market in 2025.

- Growth Potential: High, driven by continuous technological advancements and evolving industrial needs.

- Leading Region: North America

- Key Drivers: Strong regulatory frameworks, advanced industrial base, government support for sustainability, R&D investment.

- Market Share: Estimated to hold 30% of the global MEMS gas sensor market in 2025.

- Growth Potential: Sustained growth due to ongoing technological integration and policy support.

- Dominant Sensor Type: Oxygen (O2)

- Key Drivers: Medical applications (respiratory, anesthesia), industrial processes (combustion control), food packaging, aerospace.

- Market Share: Estimated to represent 25% of the total MEMS gas sensor market by type in 2025.

- Growth Potential: Significant, fueled by healthcare trends and expanding industrial uses.

Mems Gas Sensor Product Landscape

The MEMS gas sensor product landscape is characterized by rapid innovation in miniaturization, sensitivity, and selectivity. Companies are developing compact, low-power sensors capable of detecting a wide range of gases with enhanced accuracy. Product innovations focus on integrating multiple sensing elements onto a single chip, enabling multi-gas detection and reducing overall system costs. Applications are diversifying from traditional industrial safety to smart homes, wearables, and medical diagnostics, with new product launches frequently featuring improved response times and extended operational lifespans. Technological advancements include the use of novel nanomaterials like graphene and metal-organic frameworks (MOFs) to enhance gas molecule interaction and sensor performance.

Key Drivers, Barriers & Challenges in Mems Gas Sensor

Key Drivers: The MEMS gas sensor market is propelled by a confluence of critical drivers. Technological advancements in microfabrication and material science are enabling smaller, more sensitive, and energy-efficient sensors. Growing global concerns about environmental pollution and air quality are creating significant demand for accurate monitoring solutions. Stringent government regulations for industrial safety and emissions control mandate the adoption of advanced gas detection technologies. The expansion of the Internet of Things (IoT) ecosystem and the rise of smart devices are creating new application avenues, from smart homes to wearables, for integrated gas sensing capabilities.

Barriers & Challenges: Despite its growth potential, the MEMS gas sensor market faces several significant challenges. High research and development costs, coupled with the need for specialized manufacturing facilities, create substantial entry barriers for new players. Ensuring long-term sensor stability and reliability in diverse environmental conditions, such as extreme temperatures and humidity, remains a technical hurdle. Supply chain disruptions, particularly for specialized raw materials and components, can impact production volumes and lead times. Furthermore, competition from established non-MEMS sensing technologies, such as electrochemical sensors, presents a continuous challenge, especially in price-sensitive applications. Regulatory hurdles in achieving certification for medical and safety-critical applications also pose a significant constraint. The estimated cost of a critical component shortage in 2023 alone was $500 million in lost revenue for sensor manufacturers.

Emerging Opportunities in Mems Gas Sensor

Emerging opportunities in the MEMS gas sensor market are abundant, driven by evolving consumer needs and technological frontiers. The burgeoning market for personal health monitoring presents a significant avenue, with MEMS sensors poised for integration into wearable devices for non-invasive disease diagnosis and continuous health tracking, such as breath analysis for detecting early signs of illness. The expanding smart agriculture sector offers opportunities for soil gas monitoring and optimized crop management. Furthermore, the increasing adoption of electric vehicles (EVs) and the need for battery safety monitoring are opening new application domains for specialized gas sensors. Untapped markets in developing economies, where industrialization is rapidly progressing, also present substantial growth potential for affordable and reliable gas sensing solutions. The development of AI-powered sensor fusion techniques, combining data from multiple MEMS sensors to provide more comprehensive environmental insights, is another exciting area for innovation.

Growth Accelerators in the Mems Gas Sensor Industry

The long-term growth of the MEMS gas sensor industry is significantly accelerated by several key catalysts. Technological breakthroughs in novel sensing materials and advanced microfluidic designs are continuously improving sensor performance, enabling higher accuracy, faster response times, and lower detection limits. Strategic partnerships between MEMS manufacturers and original equipment manufacturers (OEMs) are crucial for integrating sensors into a wider array of end products and accelerating market penetration. The increasing focus on sustainability and environmental protection by governments and corporations worldwide is a powerful market expansion strategy, driving demand for emission monitoring and pollution control solutions. The development of sophisticated data analytics platforms that leverage the vast amounts of data generated by MEMS gas sensors will further enhance their value proposition and drive adoption.

Key Players Shaping the Mems Gas Sensor Market

- Amphenol

- Bosch Sensortec

- Sensirion

- Axetris

- TDK Corporation

- Figaro Engineering

- Omron

- ES Systems

- Siargo

- Renesas

- First Sensor

- Flusso

- Winsen Electronics Technology

- Hanwei Electronics Group

- Micro-nano Sensing Technology

- ACEINNA

Notable Milestones in Mems Gas Sensor Sector

- 2021: Introduction of highly integrated, multi-gas MEMS sensor modules for consumer electronics.

- 2022: Significant advancement in MEMS sensor miniaturization, enabling integration into wearable health trackers.

- 2022: Development of novel MOF-based MEMS sensors with significantly enhanced selectivity for specific gases.

- 2023: Launch of robust MEMS gas sensors designed for extreme industrial environments, expanding their application scope.

- 2023: Increased venture capital funding for startups developing innovative MEMS gas sensing solutions for the medical sector.

- 2024: Release of MEMS sensors with integrated AI capabilities for predictive analytics in environmental monitoring.

In-Depth Mems Gas Sensor Market Outlook

- 2021: Introduction of highly integrated, multi-gas MEMS sensor modules for consumer electronics.

- 2022: Significant advancement in MEMS sensor miniaturization, enabling integration into wearable health trackers.

- 2022: Development of novel MOF-based MEMS sensors with significantly enhanced selectivity for specific gases.

- 2023: Launch of robust MEMS gas sensors designed for extreme industrial environments, expanding their application scope.

- 2023: Increased venture capital funding for startups developing innovative MEMS gas sensing solutions for the medical sector.

- 2024: Release of MEMS sensors with integrated AI capabilities for predictive analytics in environmental monitoring.

In-Depth Mems Gas Sensor Market Outlook

The MEMS gas sensor market is on a trajectory of sustained and accelerated growth, projected to reach $7,850.3 million by 2033. Growth accelerators such as miniaturization, enhanced sensitivity, and reduced power consumption are driving wider adoption. Strategic partnerships between sensor developers and device manufacturers are crucial for unlocking new application areas, particularly in the booming IoT and wearable technology markets. The increasing global emphasis on health, safety, and environmental sustainability will continue to be a significant driver. Technological breakthroughs in materials science and microfabrication promise even more advanced and cost-effective sensing solutions. Future growth will be significantly influenced by the successful integration of MEMS gas sensors into advanced diagnostic tools, smart infrastructure, and next-generation automotive systems, presenting substantial opportunities for innovation and market expansion.

Mems Gas Sensor Segmentation

-

1. Application

- 1.1. Medical

- 1.2. Industrial Monitoring

- 1.3. Environmental Testing

- 1.4. Other

-

2. Type

- 2.1. Carbon Monoxide

- 2.2. Methane

- 2.3. Oxygen

- 2.4. Other

Mems Gas Sensor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Mems Gas Sensor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XXX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Mems Gas Sensor Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Medical

- 5.1.2. Industrial Monitoring

- 5.1.3. Environmental Testing

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Carbon Monoxide

- 5.2.2. Methane

- 5.2.3. Oxygen

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Mems Gas Sensor Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Medical

- 6.1.2. Industrial Monitoring

- 6.1.3. Environmental Testing

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Carbon Monoxide

- 6.2.2. Methane

- 6.2.3. Oxygen

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Mems Gas Sensor Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Medical

- 7.1.2. Industrial Monitoring

- 7.1.3. Environmental Testing

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Carbon Monoxide

- 7.2.2. Methane

- 7.2.3. Oxygen

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Mems Gas Sensor Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Medical

- 8.1.2. Industrial Monitoring

- 8.1.3. Environmental Testing

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Carbon Monoxide

- 8.2.2. Methane

- 8.2.3. Oxygen

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Mems Gas Sensor Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Medical

- 9.1.2. Industrial Monitoring

- 9.1.3. Environmental Testing

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Carbon Monoxide

- 9.2.2. Methane

- 9.2.3. Oxygen

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Mems Gas Sensor Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Medical

- 10.1.2. Industrial Monitoring

- 10.1.3. Environmental Testing

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Carbon Monoxide

- 10.2.2. Methane

- 10.2.3. Oxygen

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Amphenol

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Bosch Sensortec

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sensirion

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Axetris

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 TDK Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Figaro Engineering

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Omron

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ES Systems

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Siargo

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Renesas

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 First Sensor

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Flusso

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Winsen Electronics Technology

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Hanwei Electronics Group

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Micro-nano Sensing Technology

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 ACEINNA

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Amphenol

List of Figures

- Figure 1: Global Mems Gas Sensor Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global Mems Gas Sensor Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: North America Mems Gas Sensor Revenue (million), by Application 2024 & 2032

- Figure 4: North America Mems Gas Sensor Volume (K), by Application 2024 & 2032

- Figure 5: North America Mems Gas Sensor Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Mems Gas Sensor Volume Share (%), by Application 2024 & 2032

- Figure 7: North America Mems Gas Sensor Revenue (million), by Type 2024 & 2032

- Figure 8: North America Mems Gas Sensor Volume (K), by Type 2024 & 2032

- Figure 9: North America Mems Gas Sensor Revenue Share (%), by Type 2024 & 2032

- Figure 10: North America Mems Gas Sensor Volume Share (%), by Type 2024 & 2032

- Figure 11: North America Mems Gas Sensor Revenue (million), by Country 2024 & 2032

- Figure 12: North America Mems Gas Sensor Volume (K), by Country 2024 & 2032

- Figure 13: North America Mems Gas Sensor Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America Mems Gas Sensor Volume Share (%), by Country 2024 & 2032

- Figure 15: South America Mems Gas Sensor Revenue (million), by Application 2024 & 2032

- Figure 16: South America Mems Gas Sensor Volume (K), by Application 2024 & 2032

- Figure 17: South America Mems Gas Sensor Revenue Share (%), by Application 2024 & 2032

- Figure 18: South America Mems Gas Sensor Volume Share (%), by Application 2024 & 2032

- Figure 19: South America Mems Gas Sensor Revenue (million), by Type 2024 & 2032

- Figure 20: South America Mems Gas Sensor Volume (K), by Type 2024 & 2032

- Figure 21: South America Mems Gas Sensor Revenue Share (%), by Type 2024 & 2032

- Figure 22: South America Mems Gas Sensor Volume Share (%), by Type 2024 & 2032

- Figure 23: South America Mems Gas Sensor Revenue (million), by Country 2024 & 2032

- Figure 24: South America Mems Gas Sensor Volume (K), by Country 2024 & 2032

- Figure 25: South America Mems Gas Sensor Revenue Share (%), by Country 2024 & 2032

- Figure 26: South America Mems Gas Sensor Volume Share (%), by Country 2024 & 2032

- Figure 27: Europe Mems Gas Sensor Revenue (million), by Application 2024 & 2032

- Figure 28: Europe Mems Gas Sensor Volume (K), by Application 2024 & 2032

- Figure 29: Europe Mems Gas Sensor Revenue Share (%), by Application 2024 & 2032

- Figure 30: Europe Mems Gas Sensor Volume Share (%), by Application 2024 & 2032

- Figure 31: Europe Mems Gas Sensor Revenue (million), by Type 2024 & 2032

- Figure 32: Europe Mems Gas Sensor Volume (K), by Type 2024 & 2032

- Figure 33: Europe Mems Gas Sensor Revenue Share (%), by Type 2024 & 2032

- Figure 34: Europe Mems Gas Sensor Volume Share (%), by Type 2024 & 2032

- Figure 35: Europe Mems Gas Sensor Revenue (million), by Country 2024 & 2032

- Figure 36: Europe Mems Gas Sensor Volume (K), by Country 2024 & 2032

- Figure 37: Europe Mems Gas Sensor Revenue Share (%), by Country 2024 & 2032

- Figure 38: Europe Mems Gas Sensor Volume Share (%), by Country 2024 & 2032

- Figure 39: Middle East & Africa Mems Gas Sensor Revenue (million), by Application 2024 & 2032

- Figure 40: Middle East & Africa Mems Gas Sensor Volume (K), by Application 2024 & 2032

- Figure 41: Middle East & Africa Mems Gas Sensor Revenue Share (%), by Application 2024 & 2032

- Figure 42: Middle East & Africa Mems Gas Sensor Volume Share (%), by Application 2024 & 2032

- Figure 43: Middle East & Africa Mems Gas Sensor Revenue (million), by Type 2024 & 2032

- Figure 44: Middle East & Africa Mems Gas Sensor Volume (K), by Type 2024 & 2032

- Figure 45: Middle East & Africa Mems Gas Sensor Revenue Share (%), by Type 2024 & 2032

- Figure 46: Middle East & Africa Mems Gas Sensor Volume Share (%), by Type 2024 & 2032

- Figure 47: Middle East & Africa Mems Gas Sensor Revenue (million), by Country 2024 & 2032

- Figure 48: Middle East & Africa Mems Gas Sensor Volume (K), by Country 2024 & 2032

- Figure 49: Middle East & Africa Mems Gas Sensor Revenue Share (%), by Country 2024 & 2032

- Figure 50: Middle East & Africa Mems Gas Sensor Volume Share (%), by Country 2024 & 2032

- Figure 51: Asia Pacific Mems Gas Sensor Revenue (million), by Application 2024 & 2032

- Figure 52: Asia Pacific Mems Gas Sensor Volume (K), by Application 2024 & 2032

- Figure 53: Asia Pacific Mems Gas Sensor Revenue Share (%), by Application 2024 & 2032

- Figure 54: Asia Pacific Mems Gas Sensor Volume Share (%), by Application 2024 & 2032

- Figure 55: Asia Pacific Mems Gas Sensor Revenue (million), by Type 2024 & 2032

- Figure 56: Asia Pacific Mems Gas Sensor Volume (K), by Type 2024 & 2032

- Figure 57: Asia Pacific Mems Gas Sensor Revenue Share (%), by Type 2024 & 2032

- Figure 58: Asia Pacific Mems Gas Sensor Volume Share (%), by Type 2024 & 2032

- Figure 59: Asia Pacific Mems Gas Sensor Revenue (million), by Country 2024 & 2032

- Figure 60: Asia Pacific Mems Gas Sensor Volume (K), by Country 2024 & 2032

- Figure 61: Asia Pacific Mems Gas Sensor Revenue Share (%), by Country 2024 & 2032

- Figure 62: Asia Pacific Mems Gas Sensor Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Mems Gas Sensor Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Mems Gas Sensor Volume K Forecast, by Region 2019 & 2032

- Table 3: Global Mems Gas Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Mems Gas Sensor Volume K Forecast, by Application 2019 & 2032

- Table 5: Global Mems Gas Sensor Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Mems Gas Sensor Volume K Forecast, by Type 2019 & 2032

- Table 7: Global Mems Gas Sensor Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global Mems Gas Sensor Volume K Forecast, by Region 2019 & 2032

- Table 9: Global Mems Gas Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 10: Global Mems Gas Sensor Volume K Forecast, by Application 2019 & 2032

- Table 11: Global Mems Gas Sensor Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Mems Gas Sensor Volume K Forecast, by Type 2019 & 2032

- Table 13: Global Mems Gas Sensor Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global Mems Gas Sensor Volume K Forecast, by Country 2019 & 2032

- Table 15: United States Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: United States Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 17: Canada Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 18: Canada Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 19: Mexico Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 20: Mexico Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 21: Global Mems Gas Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 22: Global Mems Gas Sensor Volume K Forecast, by Application 2019 & 2032

- Table 23: Global Mems Gas Sensor Revenue million Forecast, by Type 2019 & 2032

- Table 24: Global Mems Gas Sensor Volume K Forecast, by Type 2019 & 2032

- Table 25: Global Mems Gas Sensor Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global Mems Gas Sensor Volume K Forecast, by Country 2019 & 2032

- Table 27: Brazil Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Brazil Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 29: Argentina Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 30: Argentina Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 31: Rest of South America Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 32: Rest of South America Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 33: Global Mems Gas Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 34: Global Mems Gas Sensor Volume K Forecast, by Application 2019 & 2032

- Table 35: Global Mems Gas Sensor Revenue million Forecast, by Type 2019 & 2032

- Table 36: Global Mems Gas Sensor Volume K Forecast, by Type 2019 & 2032

- Table 37: Global Mems Gas Sensor Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global Mems Gas Sensor Volume K Forecast, by Country 2019 & 2032

- Table 39: United Kingdom Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 40: United Kingdom Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 41: Germany Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: Germany Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 43: France Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: France Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 45: Italy Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Italy Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 47: Spain Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 48: Spain Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 49: Russia Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 50: Russia Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 51: Benelux Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 52: Benelux Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 53: Nordics Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 54: Nordics Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 55: Rest of Europe Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 56: Rest of Europe Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 57: Global Mems Gas Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 58: Global Mems Gas Sensor Volume K Forecast, by Application 2019 & 2032

- Table 59: Global Mems Gas Sensor Revenue million Forecast, by Type 2019 & 2032

- Table 60: Global Mems Gas Sensor Volume K Forecast, by Type 2019 & 2032

- Table 61: Global Mems Gas Sensor Revenue million Forecast, by Country 2019 & 2032

- Table 62: Global Mems Gas Sensor Volume K Forecast, by Country 2019 & 2032

- Table 63: Turkey Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 64: Turkey Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 65: Israel Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 66: Israel Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 67: GCC Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 68: GCC Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 69: North Africa Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 70: North Africa Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 71: South Africa Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 72: South Africa Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 73: Rest of Middle East & Africa Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 74: Rest of Middle East & Africa Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 75: Global Mems Gas Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 76: Global Mems Gas Sensor Volume K Forecast, by Application 2019 & 2032

- Table 77: Global Mems Gas Sensor Revenue million Forecast, by Type 2019 & 2032

- Table 78: Global Mems Gas Sensor Volume K Forecast, by Type 2019 & 2032

- Table 79: Global Mems Gas Sensor Revenue million Forecast, by Country 2019 & 2032

- Table 80: Global Mems Gas Sensor Volume K Forecast, by Country 2019 & 2032

- Table 81: China Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 82: China Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 83: India Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 84: India Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 85: Japan Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 86: Japan Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 87: South Korea Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 88: South Korea Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 89: ASEAN Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 90: ASEAN Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 91: Oceania Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 92: Oceania Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

- Table 93: Rest of Asia Pacific Mems Gas Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 94: Rest of Asia Pacific Mems Gas Sensor Volume (K) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mems Gas Sensor?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Mems Gas Sensor?

Key companies in the market include Amphenol, Bosch Sensortec, Sensirion, Axetris, TDK Corporation, Figaro Engineering, Omron, ES Systems, Siargo, Renesas, First Sensor, Flusso, Winsen Electronics Technology, Hanwei Electronics Group, Micro-nano Sensing Technology, ACEINNA.

3. What are the main segments of the Mems Gas Sensor?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mems Gas Sensor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mems Gas Sensor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mems Gas Sensor?

To stay informed about further developments, trends, and reports in the Mems Gas Sensor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence