Key Insights

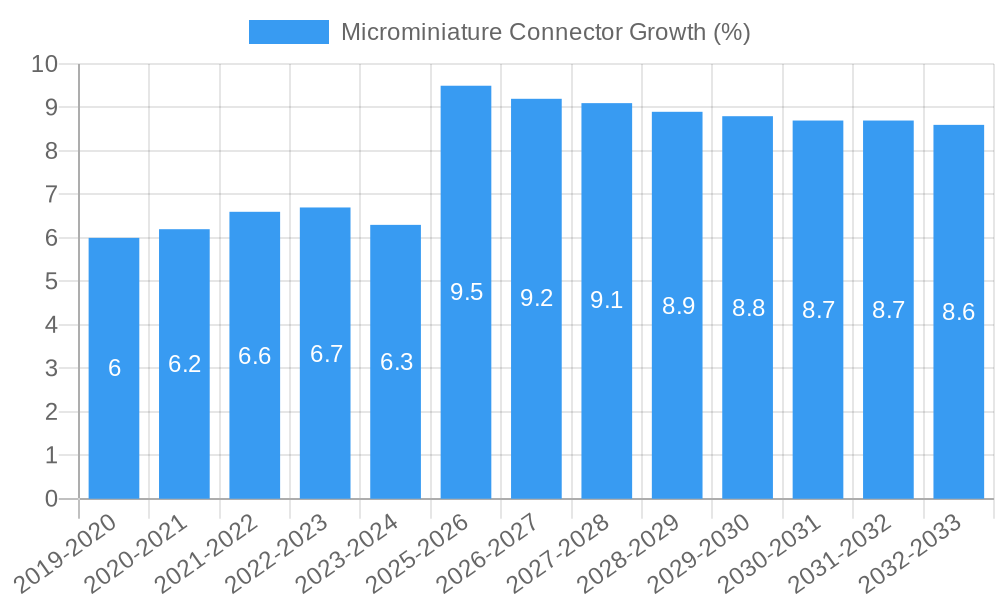

The global microminiature connector market is poised for significant expansion, driven by an estimated market size of USD 3,500 million in 2025, with a projected Compound Annual Growth Rate (CAGR) of 9.5% through 2033. This robust growth is primarily fueled by the escalating demand for miniaturization across a multitude of burgeoning industries. The relentless pursuit of smaller, lighter, and more powerful electronic devices in sectors like consumer electronics, portable medical equipment, and advanced communication systems necessitates the adoption of these compact yet high-performance connectors. Furthermore, the increasing integration of sophisticated electronic components in automotive applications, particularly in electric vehicles and advanced driver-assistance systems (ADAS), alongside the critical requirements for lightweight and reliable solutions in the aerospace and defense sectors, are powerful catalysts for market expansion. Innovations in connector technology, focusing on enhanced signal integrity, improved durability, and higher density configurations, are continuously pushing the boundaries of what is achievable, further stimulating market adoption.

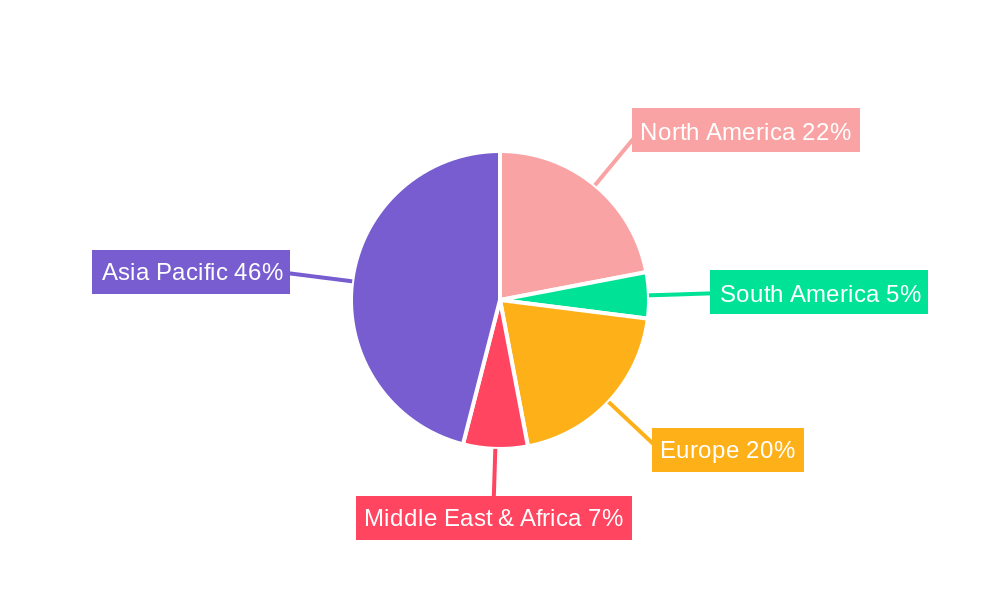

Key market restraints, such as the intricate manufacturing processes and the inherent cost associated with producing such precise components, could pose challenges to widespread adoption. However, the overwhelming benefits in terms of space saving, weight reduction, and performance optimization offered by microminiature connectors are expected to outweigh these limitations. The market is segmented by application, with Electronics expected to dominate due to its pervasive use in countless devices, followed by Automotive and Aerospace. By type, Wire to Board connectors are anticipated to hold a significant share, reflecting their widespread application in connecting internal circuitry. Geographically, the Asia Pacific region, led by China and India, is projected to be the fastest-growing market, owing to its substantial manufacturing base and rapidly expanding electronics and automotive industries. North America and Europe are also expected to maintain strong growth trajectories due to their advanced technological ecosystems and high demand for innovative solutions.

Microminiature Connector Market: Global Industry Analysis, Size, Share, Growth, Trends, and Forecast to 2033

This comprehensive report delivers an in-depth analysis of the global microminiature connector market, offering critical insights into its structure, dynamics, growth trajectories, and future outlook. Designed for industry professionals, procurement managers, R&D specialists, and strategic planners, this report leverages high-traffic keywords such as "tiny connectors," "high-density connectors," "miniature interconnects," "electronic components," and "aerospace connectors" to maximize search engine visibility. We delve into parent and child market segments, providing a nuanced understanding of market segmentation and cross-over opportunities. All quantitative values are presented in million units for clarity and industry relevance.

Microminiature Connector Market Dynamics & Structure

The microminiature connector market is characterized by a moderate to high level of concentration, with a few key players holding significant market share. Technological innovation remains a primary driver, fueled by the relentless demand for miniaturization across diverse electronic applications. Advancements in materials science, manufacturing processes, and design engineering enable connectors with higher pin densities, improved signal integrity, and enhanced durability in smaller form factors. Regulatory frameworks, particularly those pertaining to safety standards and environmental compliance (e.g., RoHS, REACH), are crucial in shaping product development and market entry. Competitive product substitutes, such as advanced soldering techniques or alternative interconnect technologies, pose a constant challenge, though microminiature connectors often offer superior flexibility, serviceability, and performance. End-user demographics are increasingly skewed towards industries prioritizing space-saving solutions, including consumer electronics, medical devices, and defense systems. Mergers and acquisitions (M&A) trends are prevalent, with larger companies acquiring smaller, specialized firms to broaden their product portfolios and technological capabilities. For instance, the acquisition of innovative design firms by established connector manufacturers has been a recurring strategy to gain a competitive edge.

- Market Concentration: Moderate to High, dominated by established players with specialized expertise.

- Technological Innovation Drivers: Miniaturization, high-density interconnects, signal integrity, ruggedization.

- Regulatory Frameworks: RoHS, REACH, industry-specific safety certifications.

- Competitive Product Substitutes: Advanced soldering, chip-level integration, specialized flexible circuits.

- End-User Demographics: Consumer electronics, automotive, aerospace, medical devices, industrial automation, telecommunications.

- M&A Trends: Strategic acquisitions for technology integration and market expansion.

Microminiature Connector Growth Trends & Insights

The microminiature connector market is projected to witness robust growth driven by escalating demand for sophisticated and compact electronic devices across various sectors. The market size has experienced a steady upward trajectory throughout the historical period (2019-2024), with an estimated market size of USD 4,200 million in 2024. This expansion is underpinned by increasing adoption rates in smartphones, wearable technology, advanced medical implants, and compact automotive electronic control units (ECUs). The compound annual growth rate (CAGR) is anticipated to remain strong, reaching approximately 7.5% during the forecast period of 2025–2033. Technological disruptions, such as the development of ultra-fine pitch connectors and novel dielectric materials, are continuously pushing the boundaries of miniaturization and performance. Consumer behavior shifts towards portable, powerful, and feature-rich electronic devices directly influence the demand for smaller, more efficient interconnect solutions. The market penetration of these connectors is expected to deepen as manufacturers strive to integrate more functionality into increasingly smaller product footprints. For example, the evolution of 5G infrastructure and the proliferation of the Internet of Things (IoT) devices are significant catalysts, requiring high-performance connectors capable of handling increased data speeds and power in confined spaces. The base year of 2025 is estimated to see a market size of USD 4,550 million, paving the way for sustained expansion.

- Market Size Evolution: From an estimated USD 4,550 million in the base year 2025, the market is on a trajectory of significant expansion.

- Adoption Rates: High in consumer electronics, automotive, and aerospace, with increasing penetration in medical and industrial IoT.

- Technological Disruptions: Advancements in materials, manufacturing, and design enabling higher density and better performance.

- Consumer Behavior Shifts: Demand for portable, powerful, and feature-rich devices driving miniaturization.

- Market Penetration: Deepening as product designs increasingly prioritize space efficiency.

- CAGR (Forecast Period 2025-2033): Approximately 7.5%.

- Historical Market Size (2024): Estimated at USD 4,200 million.

Dominant Regions, Countries, or Segments in Microminiature Connector

The Electronics application segment, encompassing consumer electronics, telecommunications, and computing, is a dominant force driving the growth of the microminiature connector market. This segment's dominance is attributable to the insatiable global demand for portable and advanced electronic devices, where space constraints are paramount. North America, particularly the United States, stands out as a leading country due to its strong presence of major electronics manufacturers, extensive R&D investments, and a high adoption rate of cutting-edge technologies. The region's robust aerospace and defense industries also contribute significantly to the demand for high-reliability microminiature connectors. Furthermore, the automotive sector, with its increasing integration of electronic components for advanced driver-assistance systems (ADAS), infotainment, and powertrain management, represents a rapidly growing market. Countries like Germany, Japan, and South Korea, renowned for their automotive manufacturing prowess, are key contributors to this segment's growth. The "Wire to Board" type segment is currently the largest, facilitating essential connections in countless electronic products. However, the "Board to Board" segment is experiencing accelerated growth, driven by the need for modularity and stacked architectures in complex electronic assemblies.

- Dominant Application Segment: Electronics (Consumer Electronics, Telecommunications, Computing) – Accounted for an estimated 40% of the market share in 2025.

- Key Drivers: Proliferation of smartphones, tablets, wearable devices, and data centers.

- Growth Potential: Continual innovation in product design and increasing demand for high-speed data transmission.

- Leading Country: United States – Driven by a strong R&D ecosystem and significant presence of tech giants.

- Market Share Contribution: Estimated at 25% of the global market in 2025.

- Key Industries: Consumer electronics, aerospace, defense, medical devices.

- Dominant Connector Type: Wire to Board – Essential for connecting external components to printed circuit boards, estimated to hold 45% of the market in 2025.

- Fastest Growing Segment: Board to Board – Driven by modular designs and advanced electronic packaging, with a projected CAGR of 8.2% from 2025-2033.

- Key Applications: Smart devices, high-performance computing, medical equipment.

Microminiature Connector Product Landscape

The microminiature connector product landscape is characterized by continuous innovation in miniaturization, enhanced performance, and specialized functionalities. Manufacturers are developing ultra-small form factor connectors with exceptionally high pin densities, enabling the integration of more electrical connections within confined spaces. This includes advancements in surface-mount technology (SMT) connectors, push-pull self-locking mechanisms for rugged environments, and modular designs for flexible configurations. Performance metrics such as increased data transfer speeds, improved signal integrity, higher current carrying capacity, and enhanced resistance to vibration and shock are key differentiators. Unique selling propositions often lie in the ability to withstand extreme temperatures, harsh chemicals, or high-pressure environments, making them ideal for specialized applications. Technological advancements include the integration of advanced materials like high-performance thermoplastics and specialized metal alloys to improve durability and electrical properties.

Key Drivers, Barriers & Challenges in Microminiature Connector

Key Drivers:

- Miniaturization Trend: The relentless demand for smaller, lighter, and more portable electronic devices across all sectors is the primary driver.

- Technological Advancements: Continuous innovation in materials, manufacturing processes, and design enables higher density and performance.

- Growth in Key End-Use Industries: Rapid expansion in consumer electronics, automotive (EVs, ADAS), aerospace, and medical devices fuels demand.

- 5G Deployment and IoT Expansion: These technologies require high-density, high-performance interconnects for increased data speeds and connectivity.

Key Barriers & Challenges:

- Manufacturing Complexity and Cost: Producing microminiature connectors requires highly precise and specialized manufacturing techniques, leading to higher production costs.

- Supply Chain Volatility: Sourcing specialized raw materials and components can be subject to global supply chain disruptions and price fluctuations.

- Stringent Quality and Reliability Standards: Applications in aerospace, medical, and automotive demand exceptionally high levels of reliability and performance, posing development and testing challenges.

- Competition from Alternative Solutions: While often superior, microminiature connectors face competition from direct soldering or other integrated circuit solutions in some applications.

- Skilled Labor Shortages: The specialized nature of manufacturing and design requires a skilled workforce, which can be a limiting factor.

Emerging Opportunities in Microminiature Connector

Emerging opportunities in the microminiature connector market are abundant, driven by new technological frontiers and evolving consumer needs. The expansion of augmented reality (AR) and virtual reality (VR) devices presents a significant avenue for growth, requiring compact and high-bandwidth connectors. The burgeoning medical technology sector, particularly in implantable devices, wearable health monitors, and advanced diagnostic equipment, offers substantial potential for specialized, biocompatible microminiature connectors. Furthermore, the increasing adoption of electric vehicles (EVs) and autonomous driving systems necessitates robust and miniaturized power and data connectors for their complex electronic architectures. The growing demand for sophisticated industrial automation and robotics also opens doors for high-reliability connectors capable of withstanding harsh environments.

Growth Accelerators in the Microminiature Connector Industry

The microminiature connector industry's long-term growth is being significantly accelerated by key factors. Technological breakthroughs in materials science, leading to enhanced dielectric properties and thermal management, allow for connectors that can handle higher power densities in smaller footprints. Strategic partnerships between connector manufacturers and semiconductor companies are crucial, fostering the development of integrated interconnect solutions. Market expansion strategies, including targeting nascent industries and geographical regions with rapidly growing electronics sectors, are also vital. The increasing focus on sustainability is driving the development of eco-friendly connector solutions, which can also serve as a growth accelerator by meeting regulatory demands and consumer preferences. The ongoing miniaturization trend across nearly all electronic devices ensures a sustained demand for these critical components.

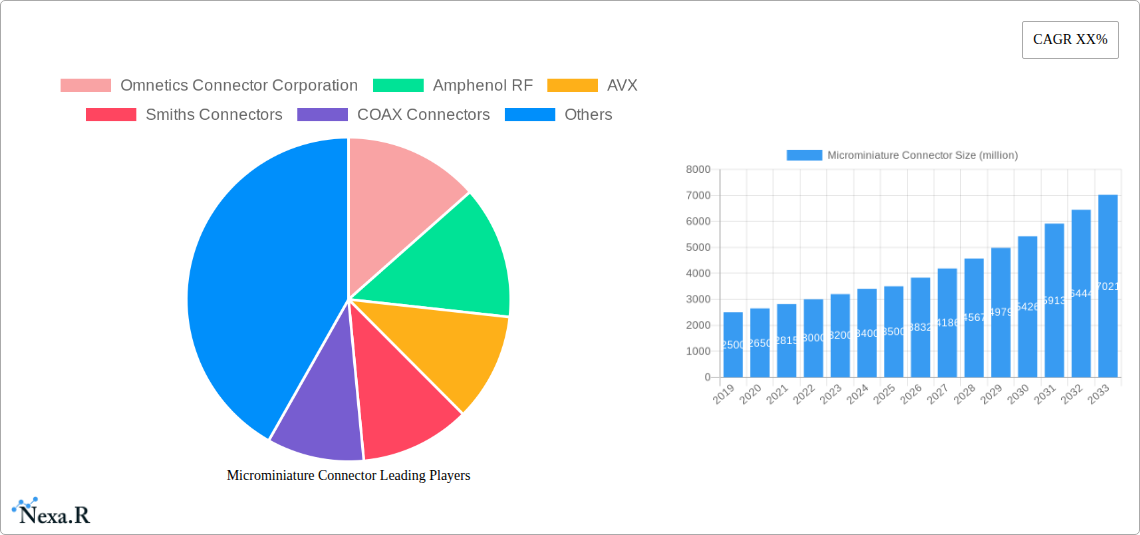

Key Players Shaping the Microminiature Connector Market

- Omnetics Connector Corporation

- Amphenol RF

- AVX

- Smiths Connectors

- COAX Connectors

- Molex

- TTI, Inc.

Notable Milestones in Microminiature Connector Sector

- 2019: Introduction of new high-density D-sub connectors with enhanced shielding by a leading manufacturer.

- 2020: Launch of ultra-miniature board-to-board connectors designed for wearable electronics.

- 2021: Major acquisition of a specialized microminiature connector design firm by a global interconnect solutions provider.

- 2022: Development of ruggedized microminiature connectors for harsh environment applications in aerospace and defense.

- 2023: Release of new series of high-speed microminiature connectors supporting 5G infrastructure requirements.

- 2024: Advancements in overmolding techniques for improved environmental sealing and strain relief in microminiature connectors.

In-Depth Microminiature Connector Market Outlook

The outlook for the microminiature connector market remains exceptionally strong, fueled by ongoing technological evolution and pervasive demand across critical industries. Growth accelerators like advancements in materials science and collaborative efforts between connector and semiconductor firms will continue to drive innovation and market expansion. The increasing adoption of 5G technology, the Internet of Things (IoT), and the burgeoning electric vehicle market are creating sustained demand for high-performance, miniaturized interconnects. Strategic opportunities lie in further developing connectors for emerging applications such as advanced AR/VR systems, implantable medical devices, and next-generation aerospace and defense platforms. The market is poised for continued growth, offering significant potential for stakeholders who can adapt to evolving technological landscapes and meet the stringent requirements of a miniaturized future.

Microminiature Connector Segmentation

-

1. Application

- 1.1. Electronics

- 1.2. Automotive

- 1.3. Aerospace

- 1.4. Others

-

2. Types

- 2.1. Wire to Board

- 2.2. Board to Board

- 2.3. Others

Microminiature Connector Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Microminiature Connector REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Microminiature Connector Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Electronics

- 5.1.2. Automotive

- 5.1.3. Aerospace

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Wire to Board

- 5.2.2. Board to Board

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Microminiature Connector Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Electronics

- 6.1.2. Automotive

- 6.1.3. Aerospace

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Wire to Board

- 6.2.2. Board to Board

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Microminiature Connector Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Electronics

- 7.1.2. Automotive

- 7.1.3. Aerospace

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Wire to Board

- 7.2.2. Board to Board

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Microminiature Connector Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Electronics

- 8.1.2. Automotive

- 8.1.3. Aerospace

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Wire to Board

- 8.2.2. Board to Board

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Microminiature Connector Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Electronics

- 9.1.2. Automotive

- 9.1.3. Aerospace

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Wire to Board

- 9.2.2. Board to Board

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Microminiature Connector Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Electronics

- 10.1.2. Automotive

- 10.1.3. Aerospace

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Wire to Board

- 10.2.2. Board to Board

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Omnetics Connector Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Amphenol RF

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AVX

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Smiths Connectors

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 COAX Connectors

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Molex

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 TTI

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Inc.

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Omnetics Connector Corporation

List of Figures

- Figure 1: Global Microminiature Connector Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Microminiature Connector Revenue (million), by Application 2024 & 2032

- Figure 3: North America Microminiature Connector Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Microminiature Connector Revenue (million), by Types 2024 & 2032

- Figure 5: North America Microminiature Connector Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Microminiature Connector Revenue (million), by Country 2024 & 2032

- Figure 7: North America Microminiature Connector Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Microminiature Connector Revenue (million), by Application 2024 & 2032

- Figure 9: South America Microminiature Connector Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Microminiature Connector Revenue (million), by Types 2024 & 2032

- Figure 11: South America Microminiature Connector Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Microminiature Connector Revenue (million), by Country 2024 & 2032

- Figure 13: South America Microminiature Connector Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Microminiature Connector Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Microminiature Connector Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Microminiature Connector Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Microminiature Connector Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Microminiature Connector Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Microminiature Connector Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Microminiature Connector Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Microminiature Connector Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Microminiature Connector Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Microminiature Connector Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Microminiature Connector Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Microminiature Connector Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Microminiature Connector Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Microminiature Connector Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Microminiature Connector Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Microminiature Connector Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Microminiature Connector Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Microminiature Connector Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Microminiature Connector Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Microminiature Connector Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Microminiature Connector Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Microminiature Connector Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Microminiature Connector Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Microminiature Connector Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Microminiature Connector Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Microminiature Connector Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Microminiature Connector Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Microminiature Connector Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Microminiature Connector Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Microminiature Connector Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Microminiature Connector Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Microminiature Connector Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Microminiature Connector Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Microminiature Connector Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Microminiature Connector Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Microminiature Connector Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Microminiature Connector Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Microminiature Connector Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Microminiature Connector?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Microminiature Connector?

Key companies in the market include Omnetics Connector Corporation, Amphenol RF, AVX, Smiths Connectors, COAX Connectors, Molex, TTI, Inc..

3. What are the main segments of the Microminiature Connector?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Microminiature Connector," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Microminiature Connector report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Microminiature Connector?

To stay informed about further developments, trends, and reports in the Microminiature Connector, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence