Key Insights

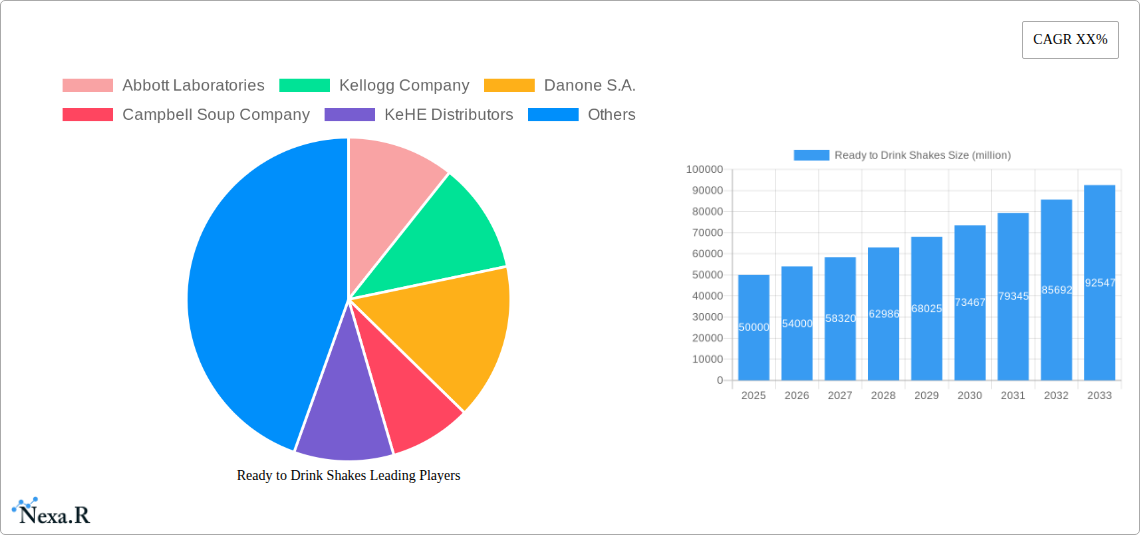

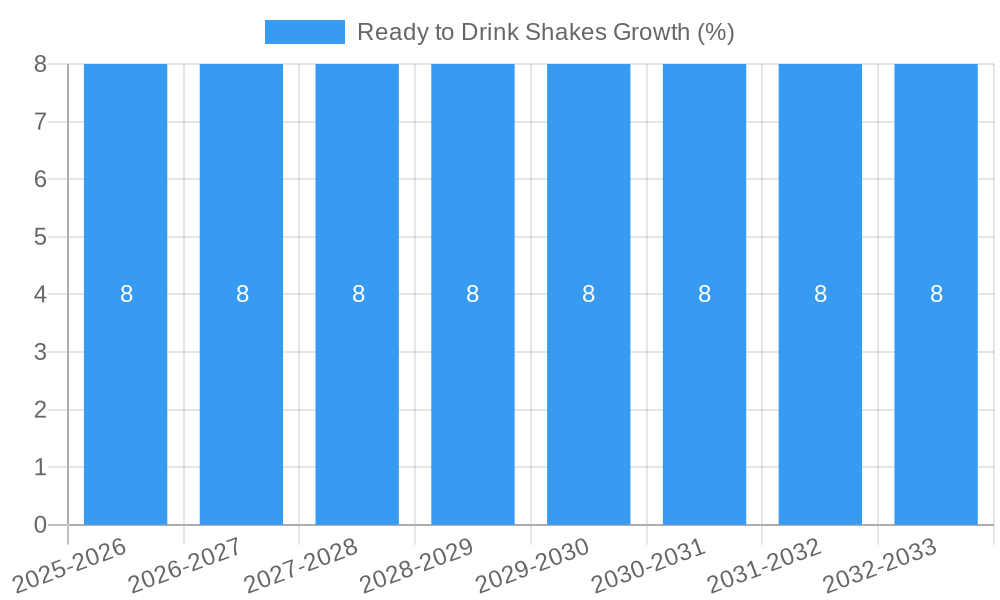

The Ready-to-Drink (RTD) Shakes market is poised for significant expansion, projected to reach approximately $50,000 million by 2025. This robust growth is fueled by a confluence of evolving consumer lifestyles, increasing health consciousness, and the demand for convenient, nutritious beverage options. The market is anticipated to experience a Compound Annual Growth Rate (CAGR) of around 8% between 2025 and 2033, underscoring its strong upward trajectory. Key drivers include the rising preference for on-the-go consumption, the growing awareness of protein and nutrient fortification, and the continuous innovation in product formulations and flavors. Consumers are increasingly seeking RTD shakes as convenient meal replacements, post-workout recovery drinks, and healthy snack alternatives, thus broadening the market appeal across diverse demographics.

The market's segmentation by application reveals a dominance of Supermarkets and Hypermarkets, which currently hold the largest share due to wider product availability and consumer purchasing habits. However, Convenience Stores and the Online channel are experiencing rapid growth, reflecting the shift towards immediate accessibility and e-commerce adoption. In terms of product types, Bottles Shakes lead the market, offering a premium and convenient format, followed by Cans Shakes and Tetra Packs Shakes, which cater to different price points and sustainability preferences. Geographically, North America and Europe currently represent the largest markets, driven by established distribution networks and high consumer spending power. Asia Pacific, however, is emerging as a high-growth region, propelled by a burgeoning middle class, increasing disposable incomes, and a growing adoption of Western dietary habits. Emerging economies within South America and the Middle East & Africa also present substantial untapped potential.

This comprehensive report delves into the dynamic Ready to Drink (RTD) Shakes market, providing in-depth insights and actionable intelligence for industry stakeholders. Spanning the historical period of 2019-2024, a base year of 2025, and a robust forecast period extending to 2033, this analysis leverages current market data and expert estimations to chart the future trajectory of this rapidly evolving sector. We explore the intricate market dynamics, growth trends, regional dominance, product innovations, and the pivotal players shaping the global RTD Shakes landscape.

Ready to Drink Shakes Market Dynamics & Structure

The Ready to Drink (RTD) Shakes market exhibits a moderately concentrated structure, with key players like Abbott Laboratories, Nestle S.A., PepsiCo, Inc., and Danone S.A. holding significant market shares. Technological innovation is primarily driven by advancements in formulation, shelf-life extension, and the development of specialized nutritional profiles, catering to health-conscious consumers and those with specific dietary needs. Regulatory frameworks, focusing on food safety standards, labeling requirements, and nutritional claims, play a crucial role in shaping product development and market access. Competitive product substitutes include traditional milk-based beverages, juices, and protein bars, each vying for consumer attention and market share. End-user demographics are increasingly skewed towards younger, urban populations seeking convenient, on-the-go nutrition solutions. Mergers and acquisitions (M&A) trends are evident as larger corporations seek to expand their portfolios and market reach, acquiring innovative startups and niche brands.

- Market Concentration: Moderate, with a few dominant global players and a growing number of specialized brands.

- Technological Innovation Drivers: Improved shelf-life technologies, advanced nutritional fortification, and sustainable packaging solutions.

- Regulatory Frameworks: Strict adherence to food safety regulations, evolving nutritional labeling laws, and consumer protection guidelines.

- Competitive Product Substitutes: Traditional dairy beverages, plant-based milk alternatives, fresh juices, and ready-to-eat meal replacements.

- End-User Demographics: Growing demand from Millennials and Gen Z, urban dwellers, fitness enthusiasts, and individuals with busy lifestyles.

- M&A Trends: Strategic acquisitions by major beverage and food conglomerates to diversify product offerings and enhance market presence. Estimated M&A deal volume: 25-35 deals annually.

Ready to Drink Shakes Growth Trends & Insights

The Ready to Drink (RTD) Shakes market is poised for significant expansion, driven by a confluence of factors including burgeoning health and wellness awareness, an increasingly mobile consumer base, and continuous product innovation. The global market size, estimated at $20,500 million in 2025, is projected to witness a robust Compound Annual Growth Rate (CAGR) of 7.8% from 2025 to 2033, reaching an estimated $36,500 million by the end of the forecast period. This impressive growth is underpinned by shifting consumer preferences towards convenient, nutritionally balanced beverages that fit seamlessly into busy lifestyles. The adoption rates for RTD shakes are escalating, particularly among younger demographics who are more receptive to functional foods and beverages. Technological disruptions are playing a pivotal role, with advancements in ingredient sourcing, processing techniques that retain maximum nutritional value, and the development of personalized nutrition shakes catering to specific dietary requirements such as low-carb, high-protein, or vegan formulations.

Consumer behavior shifts are profoundly impacting market dynamics. There's a discernible trend towards prioritizing convenience without compromising on health benefits. This has fueled the demand for RTD shakes as a viable alternative to traditional meals or snacks. Furthermore, the rising popularity of fitness and an increased focus on preventative healthcare have created a strong demand for protein-rich and nutrient-fortified RTD shakes. The market penetration of RTD shakes is still considerable in developed economies and is showing promising growth in emerging markets as disposable incomes rise and urbanization accelerates. The convenience factor, combined with the perceived health benefits, is driving consumers to incorporate RTD shakes into their daily routines, whether for post-workout recovery, meal replacement, or a quick nutritional boost. The industry is also witnessing a surge in demand for plant-based and organic RTD shakes, reflecting broader consumer trends towards sustainability and natural ingredients. The market penetration is expected to reach approximately 65% by 2033 in key developed markets, while emerging markets are projected to see penetration rates climb from 15% to 35% within the same timeframe.

Dominant Regions, Countries, or Segments in Ready to Drink Shakes

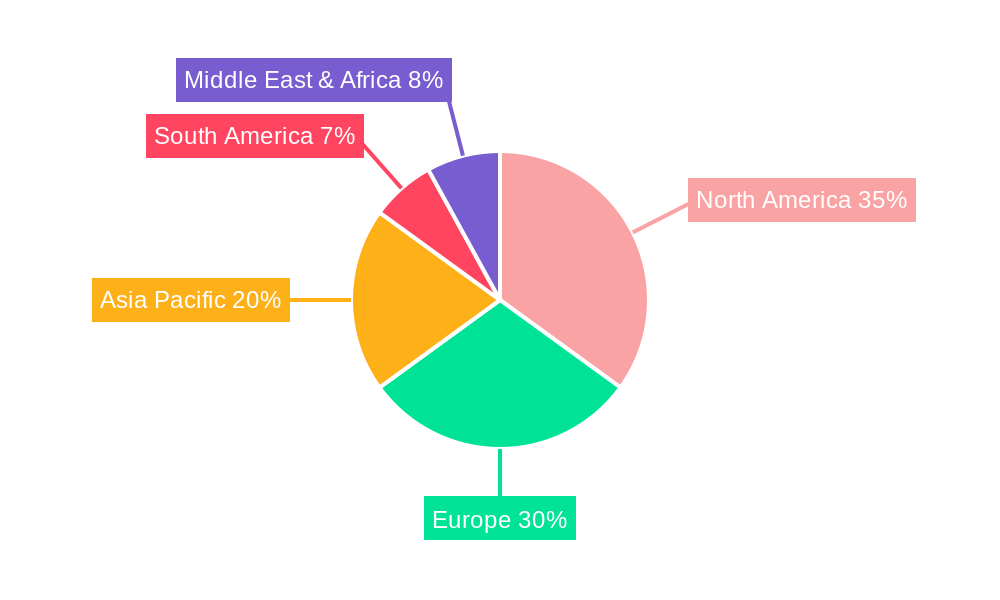

North America currently stands as the dominant region in the Ready to Drink (RTD) Shakes market, propelled by high consumer spending power, widespread adoption of health and wellness trends, and a well-established retail infrastructure that supports the distribution of RTD products. The United States, in particular, is a powerhouse, driven by its large population, significant investment in sports nutrition, and a strong culture of convenience-seeking consumers. The market share for North America in the RTD shakes sector is estimated at 35% of the global market in 2025. Key drivers of this dominance include robust economic policies that support consumer goods industries, advanced logistical networks, and high per capita income, enabling consumers to readily invest in premium nutritional beverages.

Among the application segments, Supermarkets and Hypermarkets represent the largest distribution channel, accounting for approximately 45% of RTD Shake sales in 2025. This dominance is attributed to their extensive product variety, prime locations, and the convenience they offer to a broad consumer base. Consumers often purchase RTD shakes alongside other grocery items, making these one-stop shopping destinations highly effective. Online sales represent the fastest-growing segment, projected to expand at a CAGR of 12% from 2025 to 2033, driven by the convenience of home delivery, wider product availability, and competitive pricing. Online channels are expected to capture a market share of 25% by 2033.

In terms of product types, Bottles Shakes hold the largest market share, estimated at 50% in 2025, due to their portability, resealability, and perceived premium appeal. Tetra Packs Shakes are also gaining traction due to their sustainability and long shelf life, projected to capture 25% of the market share by 2033. Cans Shakes offer a convenient and often more affordable option, particularly for single-serving consumption. Key growth potential within this segment lies in the innovation of sustainable packaging and the development of single-serve, eco-friendly options. The demand for RTD shakes in Asia-Pacific is also experiencing rapid growth, fueled by rising disposable incomes and increasing health consciousness, presenting significant future expansion opportunities.

Ready to Drink Shakes Product Landscape

The Ready to Drink (RTD) Shakes product landscape is characterized by a constant stream of innovation aimed at meeting diverse consumer needs. Product developments are increasingly focusing on functional benefits beyond basic nutrition, such as cognitive enhancement, immune support, and digestive health. Advanced formulations often incorporate plant-based protein sources, natural sweeteners, and superfoods like chia seeds, flaxseeds, and adaptogens. The performance metrics are evaluated based on nutritional content, taste profiles, shelf stability, and packaging sustainability. Unique selling propositions frequently revolve around specific dietary alignments (e.g., keto-friendly, gluten-free), ethical sourcing, and reduced environmental impact. Technological advancements are enabling the creation of microencapsulated nutrients for improved bioavailability and the development of customizable shake formulations through online platforms.

Key Drivers, Barriers & Challenges in Ready to Drink Shakes

The Ready to Drink (RTD) Shakes market is propelled by several key drivers. The escalating global demand for convenient and healthy nutrition is paramount. An increasingly health-conscious population, particularly among Millennials and Gen Z, actively seeks convenient ways to maintain a balanced diet amidst busy schedules. Technological advancements in food processing and ingredient innovation are enabling the development of more palatable, nutritious, and shelf-stable RTD shakes. Furthermore, the growing popularity of fitness and active lifestyles drives demand for protein-rich and recovery-focused shakes. Economic factors such as rising disposable incomes in emerging markets also contribute significantly.

However, the market faces several barriers and challenges. Supply chain disruptions, exacerbated by global events, can impact the availability and cost of raw materials. Regulatory hurdles, including evolving labeling requirements and stringent food safety standards across different regions, pose a significant challenge for manufacturers. Intense competitive pressure from established beverage giants and an influx of new entrants necessitates continuous innovation and aggressive marketing strategies. The perceived high cost of some specialized RTD shakes can also be a barrier for price-sensitive consumers. Furthermore, consumer skepticism regarding the "naturalness" and processing of some RTD products, coupled with the need for effective public health messaging about their nutritional value, remain ongoing challenges.

Emerging Opportunities in Ready to Drink Shakes

Emerging opportunities in the Ready to Drink (RTD) Shakes sector are abundant, driven by evolving consumer preferences and technological advancements. There's a significant untapped market in personalized nutrition, where consumers can customize their RTD shakes based on individual dietary needs, health goals, and taste preferences through online platforms. The development of RTD shakes catering to specific medical conditions or dietary restrictions, such as those for individuals with diabetes or lactose intolerance, presents a substantial growth avenue. Furthermore, the increasing focus on sustainability offers opportunities for brands to innovate with eco-friendly packaging solutions, biodegradable materials, and ethically sourced ingredients, resonating with environmentally conscious consumers. The expansion into developing economies, where awareness and disposable incomes are rising, also represents a considerable opportunity for market penetration.

Growth Accelerators in the Ready to Drink Shakes Industry

Several catalysts are accelerating growth in the Ready to Drink (RTD) Shakes industry. Technological breakthroughs in areas like advanced ingredient processing for enhanced nutrient absorption and the development of novel, natural flavors are continuously improving product appeal and efficacy. Strategic partnerships between RTD shake manufacturers and fitness influencers, gyms, and health food retailers are crucial for increasing brand visibility and reaching target demographics effectively. Market expansion strategies, including entry into underserved geographical regions and the development of product lines tailored to local tastes and nutritional needs, are also significant growth accelerators. The increasing focus on a circular economy and sustainable practices in packaging and production is further boosting consumer confidence and driving demand.

Key Players Shaping the Ready to Drink Shakes Market

- Abbott Laboratories

- Kellogg Company

- Danone S.A.

- Campbell Soup Company

- KeHE Distributors, LLC

- Huel GmbH

- The Coca Cola Company

- PepsiCo, Inc.

- Nestle S.A.

- Hormel Foods Corporation

Notable Milestones in Ready to Drink Shakes Sector

- 2019: Launch of Huel's new "Complete Nutrition" RTD shakes, focusing on plant-based ingredients and sustainability.

- 2020: PepsiCo acquires Rockstar Energy, expanding its beverage portfolio with a focus on energy and functional drinks, including RTD shakes.

- 2021: Danone launches a range of plant-based RTD shakes under its Alpro brand, catering to the growing vegan market.

- 2022: Nestle S.A. introduces a new line of Boost RTD nutritional shakes with added vitamins and minerals targeting elderly consumers.

- 2023: Kellogg Company acquires the remaining stake in Multi-X, a major Mexican food company, bolstering its presence in the Latin American RTD market.

- 2024: The Coca-Cola Company announces plans to expand its Fairlife RTD protein shake offerings into new international markets.

In-Depth Ready to Drink Shakes Market Outlook

- 2019: Launch of Huel's new "Complete Nutrition" RTD shakes, focusing on plant-based ingredients and sustainability.

- 2020: PepsiCo acquires Rockstar Energy, expanding its beverage portfolio with a focus on energy and functional drinks, including RTD shakes.

- 2021: Danone launches a range of plant-based RTD shakes under its Alpro brand, catering to the growing vegan market.

- 2022: Nestle S.A. introduces a new line of Boost RTD nutritional shakes with added vitamins and minerals targeting elderly consumers.

- 2023: Kellogg Company acquires the remaining stake in Multi-X, a major Mexican food company, bolstering its presence in the Latin American RTD market.

- 2024: The Coca-Cola Company announces plans to expand its Fairlife RTD protein shake offerings into new international markets.

In-Depth Ready to Drink Shakes Market Outlook

The future outlook for the Ready to Drink (RTD) Shakes market is exceptionally positive, driven by sustained consumer demand for convenient, healthy, and functional beverages. Growth accelerators, including ongoing technological innovation in product formulation and sustainable packaging, are expected to fuel market expansion. Strategic partnerships and market expansion into emerging economies will further broaden consumer access and adoption. The increasing consumer preference for plant-based and natural ingredients, coupled with a growing awareness of personalized nutrition, presents significant opportunities for differentiated product development. The market is projected to not only grow in volume but also in value, as consumers are increasingly willing to invest in premium, health-enhancing RTD shakes.

Ready to Drink Shakes Segmentation

-

1. Application

- 1.1. Supermarkets and Hypermarkets

- 1.2. Convenience Stores

- 1.3. Online

-

2. Types

- 2.1. Bottles Shakes

- 2.2. Cans Shakes

- 2.3. Tetra Packs Shakes

Ready to Drink Shakes Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ready to Drink Shakes REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ready to Drink Shakes Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Supermarkets and Hypermarkets

- 5.1.2. Convenience Stores

- 5.1.3. Online

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Bottles Shakes

- 5.2.2. Cans Shakes

- 5.2.3. Tetra Packs Shakes

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Ready to Drink Shakes Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Supermarkets and Hypermarkets

- 6.1.2. Convenience Stores

- 6.1.3. Online

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Bottles Shakes

- 6.2.2. Cans Shakes

- 6.2.3. Tetra Packs Shakes

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Ready to Drink Shakes Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Supermarkets and Hypermarkets

- 7.1.2. Convenience Stores

- 7.1.3. Online

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Bottles Shakes

- 7.2.2. Cans Shakes

- 7.2.3. Tetra Packs Shakes

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ready to Drink Shakes Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Supermarkets and Hypermarkets

- 8.1.2. Convenience Stores

- 8.1.3. Online

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Bottles Shakes

- 8.2.2. Cans Shakes

- 8.2.3. Tetra Packs Shakes

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Ready to Drink Shakes Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Supermarkets and Hypermarkets

- 9.1.2. Convenience Stores

- 9.1.3. Online

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Bottles Shakes

- 9.2.2. Cans Shakes

- 9.2.3. Tetra Packs Shakes

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Ready to Drink Shakes Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Supermarkets and Hypermarkets

- 10.1.2. Convenience Stores

- 10.1.3. Online

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Bottles Shakes

- 10.2.2. Cans Shakes

- 10.2.3. Tetra Packs Shakes

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Abbott Laboratories

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Kellogg Company

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Danone S.A.

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Campbell Soup Company

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 KeHE Distributors

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 LLC

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Huel GmbH

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 The Coca Cola Company

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 PepsiCo

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Inc.

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Nestle S.A.

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Hormel Foods Corporation

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Abbott Laboratories

List of Figures

- Figure 1: Global Ready to Drink Shakes Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Ready to Drink Shakes Revenue (million), by Application 2024 & 2032

- Figure 3: North America Ready to Drink Shakes Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Ready to Drink Shakes Revenue (million), by Types 2024 & 2032

- Figure 5: North America Ready to Drink Shakes Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Ready to Drink Shakes Revenue (million), by Country 2024 & 2032

- Figure 7: North America Ready to Drink Shakes Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Ready to Drink Shakes Revenue (million), by Application 2024 & 2032

- Figure 9: South America Ready to Drink Shakes Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Ready to Drink Shakes Revenue (million), by Types 2024 & 2032

- Figure 11: South America Ready to Drink Shakes Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Ready to Drink Shakes Revenue (million), by Country 2024 & 2032

- Figure 13: South America Ready to Drink Shakes Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Ready to Drink Shakes Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Ready to Drink Shakes Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Ready to Drink Shakes Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Ready to Drink Shakes Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Ready to Drink Shakes Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Ready to Drink Shakes Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Ready to Drink Shakes Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Ready to Drink Shakes Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Ready to Drink Shakes Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Ready to Drink Shakes Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Ready to Drink Shakes Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Ready to Drink Shakes Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Ready to Drink Shakes Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Ready to Drink Shakes Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Ready to Drink Shakes Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Ready to Drink Shakes Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Ready to Drink Shakes Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Ready to Drink Shakes Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Ready to Drink Shakes Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Ready to Drink Shakes Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Ready to Drink Shakes Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Ready to Drink Shakes Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Ready to Drink Shakes Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Ready to Drink Shakes Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Ready to Drink Shakes Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Ready to Drink Shakes Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Ready to Drink Shakes Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Ready to Drink Shakes Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Ready to Drink Shakes Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Ready to Drink Shakes Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Ready to Drink Shakes Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Ready to Drink Shakes Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Ready to Drink Shakes Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Ready to Drink Shakes Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Ready to Drink Shakes Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Ready to Drink Shakes Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Ready to Drink Shakes Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Ready to Drink Shakes Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ready to Drink Shakes?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Ready to Drink Shakes?

Key companies in the market include Abbott Laboratories, Kellogg Company, Danone S.A., Campbell Soup Company, KeHE Distributors, LLC, Huel GmbH, The Coca Cola Company, PepsiCo, Inc., Nestle S.A., Hormel Foods Corporation.

3. What are the main segments of the Ready to Drink Shakes?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ready to Drink Shakes," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ready to Drink Shakes report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ready to Drink Shakes?

To stay informed about further developments, trends, and reports in the Ready to Drink Shakes, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence