Key Insights

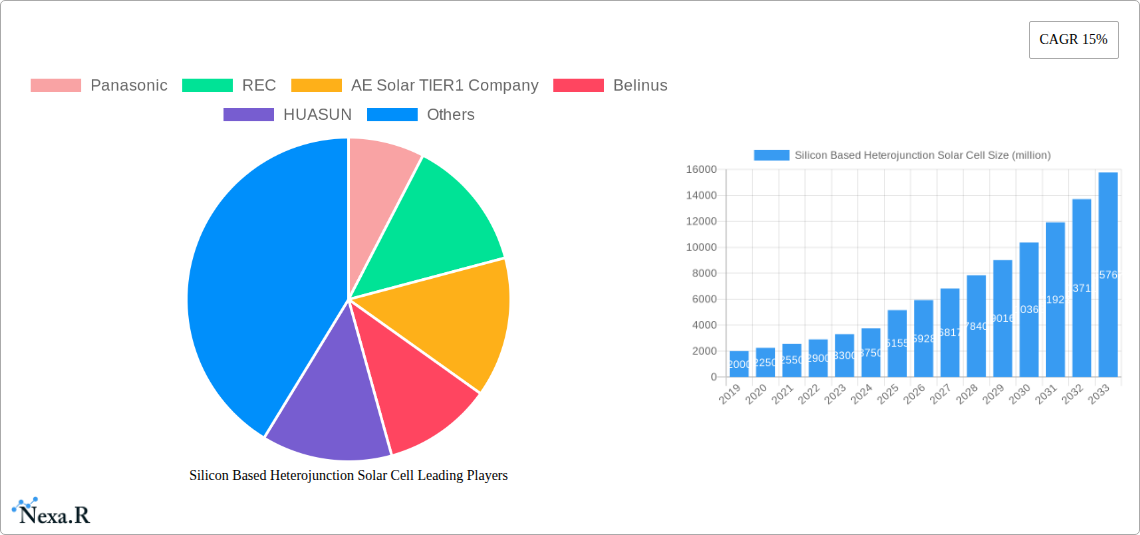

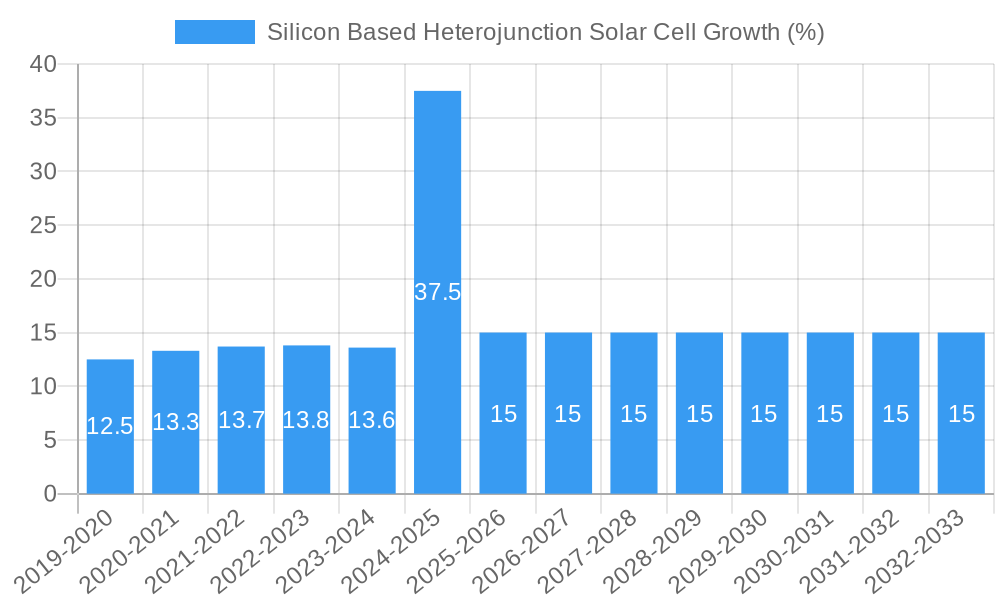

The Silicon-Based Heterojunction (HJT) Solar Cell market is poised for substantial growth, projected to reach a market size of $5,155 million by 2025. This impressive expansion is driven by a robust Compound Annual Growth Rate (CAGR) of 15%, indicating strong investor confidence and increasing adoption of this advanced solar technology. HJT solar cells represent a significant leap forward in photovoltaic efficiency, offering superior performance compared to traditional silicon technologies. Their advanced structure allows for higher energy conversion rates, better low-light performance, and reduced degradation over time, making them increasingly attractive for both residential and commercial applications. Key drivers of this market include the global push for renewable energy sources, government incentives promoting solar power, and the continuous demand for more efficient and cost-effective solar solutions. As technology matures and manufacturing scales up, the cost-competitiveness of HJT cells is expected to improve, further accelerating market penetration.

The HJT solar cell market is characterized by dynamic trends, including advancements in manufacturing processes that enhance efficiency and reduce production costs. Innovations in materials science and cell design are continuously pushing the boundaries of performance, making HJT cells a leading choice for next-generation solar power systems. While the market exhibits strong growth potential, certain restraints exist, such as the initial higher manufacturing costs compared to conventional silicon cells and the need for specialized equipment and expertise for production. However, the long-term benefits of higher energy yields and extended product lifespans are increasingly outweighing these initial hurdles. The competitive landscape is marked by the presence of major global players and emerging innovators, all vying to capture market share through technological differentiation and strategic partnerships. The focus on sustainability and the increasing urgency to combat climate change are expected to provide sustained momentum for the HJT solar cell market in the coming years.

This in-depth report provides a detailed examination of the global Silicon Based Heterojunction (HJT) Solar Cell market. Spanning from a historical analysis of 2019-2024, a base year of 2025, and a comprehensive forecast period of 2025-2033, this study delves into market dynamics, growth trends, regional dominance, product innovations, key drivers and challenges, emerging opportunities, and the strategic landscape shaped by leading industry players. With a focus on maximizing search engine visibility and engaging industry professionals, this report integrates high-traffic keywords and presents quantitative insights for clarity and actionable intelligence.

Silicon Based Heterojunction Solar Cell Market Dynamics & Structure

The global Silicon Based Heterojunction (HJT) Solar Cell market is characterized by a moderate to high level of concentration, with a few dominant players holding significant market share. Technological innovation is the primary driver of growth, fueled by the continuous pursuit of higher conversion efficiencies and enhanced durability. Key innovations include advancements in passivation layers, transparent conductive oxides (TCOs), and advanced metallization techniques, all aimed at improving HJT cell performance. Regulatory frameworks worldwide, including government incentives for renewable energy adoption and supportive policies for solar manufacturing, play a crucial role in market expansion. Competitive product substitutes, primarily PERC and TOPCon solar cells, exert pressure, but HJT's superior performance in low-light conditions and excellent temperature coefficient offer distinct advantages. End-user demographics are shifting towards commercial and industrial sectors seeking long-term energy cost savings and sustainability, alongside a growing residential segment prioritizing premium, high-efficiency solutions. Mergers and acquisitions (M&A) activity, while present, is strategically focused on acquiring advanced manufacturing capabilities or expanding market reach rather than broad consolidation. For instance, the acquisition of specialized HJT technology firms by larger solar manufacturers is a recurring trend. The market witnessed approximately 5 M&A deals valued at over $500 million within the historical period, signaling strategic investments in this high-growth segment. Barriers to innovation include the high initial capital expenditure for HJT manufacturing lines and the need for specialized expertise in material science and process engineering.

Silicon Based Heterojunction Solar Cell Growth Trends & Insights

The Silicon Based Heterojunction (HJT) Solar Cell market is poised for significant expansion, driven by a confluence of technological advancements, increasing global demand for renewable energy, and supportive government policies. The market size, valued at an estimated $5,000 million in the base year of 2025, is projected to experience a robust Compound Annual Growth Rate (CAGR) of approximately 25% during the forecast period of 2025-2033, reaching an estimated $30,000 million by the end of the forecast. Adoption rates for HJT technology are accelerating as its superior performance characteristics, such as high conversion efficiencies (currently exceeding 24% in commercial modules) and exceptional low-light and temperature performance, become more widely recognized and economically viable. Technological disruptions are continuously emerging, with ongoing research focusing on further enhancing passivation techniques, developing novel TCO materials for improved transparency and conductivity, and optimizing heterojunction layer deposition processes. These advancements are expected to push module efficiencies even higher, potentially surpassing 26% in the coming years. Consumer behavior is shifting towards a greater appreciation for long-term value and sustainability. As the cost parity between HJT and other solar technologies narrows, end-users are increasingly opting for HJT due to its higher energy yield over the module's lifespan, reduced degradation rates, and improved aesthetics, particularly in residential and premium commercial installations. The market penetration of HJT technology, currently at around 5% of the total silicon solar cell market, is anticipated to reach over 20% by 2033. This growth is underpinned by a strong understanding of the total cost of ownership, where HJT's higher initial cost is offset by greater energy generation and lower operational expenditures over two decades. The shift in consumer preference is further amplified by a growing awareness of climate change and a desire for cleaner energy sources.

Dominant Regions, Countries, or Segments in Silicon Based Heterojunction Solar Cell

The Application segment of Utility-Scale Solar Farms is currently the dominant force driving growth in the Silicon Based Heterojunction (HJT) Solar Cell market, with a significant market share estimated at 55% of the total market value in 2025. This dominance is attributable to several key drivers, including the increasing global imperative to decarbonize energy grids and meet ambitious renewable energy targets. Governments worldwide are implementing supportive policies, such as feed-in tariffs, renewable portfolio standards, and tax incentives, which make large-scale solar projects more financially attractive. Economic policies in countries like China, the United States, and Germany are particularly influential, fostering substantial investments in utility-scale solar infrastructure. Furthermore, the declining levelized cost of electricity (LCOE) for solar power makes utility-scale projects a competitive energy source, and HJT's higher energy yield per unit area and improved performance in varying environmental conditions offer a distinct advantage in optimizing land use and maximizing energy output for these massive installations. The growth potential within this segment remains exceptionally high, driven by ongoing project pipelines and the continuous need for new power generation capacity.

Within the Application segment, key drivers for the dominance of Utility-Scale Solar Farms include:

- Economic Policies and Incentives: Government subsidies, tax credits, and favorable power purchase agreements (PPAs) significantly reduce the financial risk and improve the ROI for large-scale solar deployments. For example, the Inflation Reduction Act (IRA) in the US has spurred massive investment in renewable projects.

- Infrastructure Development: The availability of grid infrastructure and the continuous expansion of transmission networks are critical for integrating large volumes of solar power generated by utility-scale farms.

- Technological Advancements in HJT: HJT’s superior efficiency and performance in diverse climatic conditions, including higher energy generation in diffuse light and reduced degradation at elevated temperatures, translate directly to more predictable and higher energy yields for utility-scale projects, thus optimizing LCOE.

- Corporate Sustainability Goals: A growing number of corporations are investing in renewable energy to meet their Environmental, Social, and Governance (ESG) targets, often through direct investments in or offtake agreements with utility-scale solar farms.

The Type segment of Bifacial HJT Solar Cells is also a significant contributor to market growth, currently holding approximately 40% of the market share in 2025, and is expected to see substantial expansion as the technology matures and its benefits are further realized across various applications. The ability of bifacial cells to capture sunlight from both sides leads to an increased energy yield, particularly in utility-scale and commercial rooftop installations where ground albedo or reflective surfaces can significantly boost performance.

Silicon Based Heterojunction Solar Cell Product Landscape

The product landscape of Silicon Based Heterojunction (HJT) Solar Cells is defined by a relentless pursuit of higher efficiencies and improved durability. Manufacturers are introducing advanced HJT modules with conversion efficiencies consistently exceeding 24%, and some premium products reaching 25% and beyond. Key innovations include the implementation of ultra-thin amorphous silicon layers for superior passivation, advanced Transparent Conductive Oxides (TCOs) like Indium Tin Oxide (ITO) or Aluminum-doped Zinc Oxide (AZO) for enhanced conductivity and transparency, and improved metallization techniques that reduce shading losses. Bifacial HJT modules are also gaining prominence, offering up to 20% more energy yield depending on installation conditions. Unique selling propositions include exceptional performance in low-light and high-temperature environments, lower degradation rates (typically <0.26% per year), and improved aesthetics due to the absence of busbars in some designs. These technological advancements directly translate to a lower Levelized Cost of Energy (LCOE) for end-users.

Key Drivers, Barriers & Challenges in Silicon Based Heterojunction Solar Cell

Key Drivers: The primary forces propelling the Silicon Based Heterojunction (HJT) Solar Cell market are:

- Technological Superiority: HJT’s inherent advantages in conversion efficiency, low-light performance, and temperature coefficient directly translate to higher energy yields and a lower LCOE, making it increasingly attractive for various applications.

- Supportive Government Policies: Global renewable energy targets and incentives, such as tax credits and subsidies, are crucial for driving demand and making HJT technology more competitive.

- Growing Demand for High-Efficiency Solutions: An increasing awareness of energy conservation and the desire for maximum power output from limited installation space are fueling the demand for advanced solar technologies.

- Corporate Sustainability Initiatives: Businesses are actively investing in renewable energy to meet ESG goals, creating a significant market for high-performance solar solutions.

Key Barriers & Challenges:

- Higher Manufacturing Costs: The intricate manufacturing process of HJT cells, requiring specialized equipment and materials, leads to higher initial capital expenditure and production costs compared to established technologies like PERC. For instance, the cost of PECVD equipment for amorphous silicon deposition can add 10-15% to manufacturing expenses.

- Supply Chain Dependencies: Reliance on specific precursor materials and specialized components can create supply chain vulnerabilities and price fluctuations.

- Market Education and Awareness: Despite its advantages, widespread adoption still requires educating installers and end-users about the long-term benefits and performance characteristics of HJT technology.

- Competition from Other Advanced Technologies: The rapid development of other high-efficiency solar cell technologies like TOPCon presents ongoing competition.

Emerging Opportunities in Silicon Based Heterojunction Solar Cell

Emerging opportunities in the Silicon Based Heterojunction (HJT) Solar Cell industry lie in the expansion into niche and premium markets, the integration with energy storage solutions, and the development of building-integrated photovoltaics (BIPV). The residential sector, particularly for premium homes and off-grid applications where reliability and maximum energy generation are paramount, presents significant untapped potential. Furthermore, the growing demand for integrated solar-plus-storage systems creates opportunities for HJT's high energy yield to maximize the efficiency of charging and discharging batteries. The development of aesthetically pleasing HJT modules for BIPV applications, such as solar roofs and facades, also represents a substantial growth avenue as urban development prioritizes sustainable and visually appealing architecture.

Growth Accelerators in the Silicon Based Heterojunction Solar Cell Industry

The long-term growth of the Silicon Based Heterojunction (HJT) Solar Cell industry will be significantly accelerated by key technological breakthroughs and strategic market expansion. Continued research into tandem cell structures, combining HJT with perovskite or other advanced materials, holds the promise of pushing conversion efficiencies beyond current limits, further solidifying HJT’s competitive edge. Strategic partnerships between HJT cell manufacturers and module assemblers, as well as collaborations with inverter and energy storage providers, will streamline the supply chain and offer more integrated solutions to end-users. Market expansion into emerging economies with growing energy demands and supportive renewable energy policies will also be a critical growth accelerator. For example, initiatives in Southeast Asia and Africa focusing on distributed solar power generation are ripe for HJT adoption.

Key Players Shaping the Silicon Based Heterojunction Solar Cell Market

- Panasonic

- REC

- AE Solar TIER1 Company

- Belinus

- HUASUN

- Longi Green Energy Technology Co.,Ltd.

- Hangzhou Hanfy New Energy Technology Co., Ltd.

- Suzhou Maxwell Technologies Co.,Ltd.

- GANSU GOLDEN GLASS

- Risen Energy Co.,Ltd.

- Tongwei Co.,Ltd.

- Marvel

- Canadian Solar

- AKCOME

- Meyer Burge

- GS-Solar

- Jinergy

- TW Solar

- Enel (3SUN)

- Hevel Solar

- EcoSolifer

Notable Milestones in Silicon Based Heterojunction Solar Cell Sector

- 2019: Panasonic announces a new record conversion efficiency of 26.0% for a laboratory HJT solar cell.

- 2020: REC Group launches its Alpha HJT solar panel, featuring industry-leading power output and a premium warranty.

- 2021: AE Solar launches its high-efficiency HJT modules, targeting the premium market segment.

- 2022: HUASUN introduces its new generation of HJT solar cells with further improved efficiency and reduced manufacturing costs.

- 2023: Several Tier 1 manufacturers begin scaling up HJT production lines to meet growing market demand.

- Q1 2024: Enel (3SUN) announces significant expansion plans for its HJT manufacturing capacity in Italy.

- Q2 2024: Research indicates a steady increase in the market share of HJT technology within the overall silicon solar cell market.

- Q3 2024: Longi Green Energy Technology Co., Ltd. showcases advancements in HJT cell architecture for enhanced performance.

- Q4 2024: Industry analysts predict continued strong growth for HJT solar cells driven by policy support and technological innovation.

- 2025 (Projected): Expected significant advancements in HJT module power output exceeding 700Wp.

In-Depth Silicon Based Heterojunction Solar Cell Market Outlook

The Silicon Based Heterojunction (HJT) Solar Cell market is set for a period of sustained and accelerated growth, driven by its inherent technological advantages and a supportive global energy transition. The market outlook is exceptionally positive, with ongoing advancements in manufacturing processes and materials science continually improving efficiency and reducing costs. Strategic investments in R&D and production capacity by leading players, coupled with increasing adoption in utility-scale, commercial, and residential sectors, are key indicators of this robust future. The integration of HJT technology with emerging solutions like energy storage and its potential in BIPV applications further broaden its market scope. The commitment to decarbonization and energy independence worldwide ensures a sustained demand for high-performance solar technologies, positioning HJT at the forefront of this evolving landscape. The forecast predicts a significant increase in market share, making HJT a cornerstone of future solar energy generation.

Silicon Based Heterojunction Solar Cell Segmentation

-

1. Application

- 1.1. undefined

-

2. Type

- 2.1. undefined

Silicon Based Heterojunction Solar Cell Segmentation By Geography

- 1. undefined

- 2. undefined

- 3. undefined

- 4. undefined

- 5. undefined

Silicon Based Heterojunction Solar Cell REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 15% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Silicon Based Heterojunction Solar Cell Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1.

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1.

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1.

- 5.3.2.

- 5.3.3.

- 5.3.4.

- 5.3.5.

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. undefined Silicon Based Heterojunction Solar Cell Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1.

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1.

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. undefined Silicon Based Heterojunction Solar Cell Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1.

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1.

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. undefined Silicon Based Heterojunction Solar Cell Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1.

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1.

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. undefined Silicon Based Heterojunction Solar Cell Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1.

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1.

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. undefined Silicon Based Heterojunction Solar Cell Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1.

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1.

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Panasonic

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 REC

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AE Solar TIER1 Company

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Belinus

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 HUASUN

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Longi Green Energy Technology Co.Ltd.

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Hangzhou Hanfy New Energy Technology Co. Ltd.

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Suzhou Maxwell Technologies Co.Ltd.

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 GANSU GOLDEN GLASS

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Risen Energy Co.Ltd.

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Tongwei Co.Ltd.

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Marvel

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Canadian Solar

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 AKCOME

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Meyer Burge

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 GS-Solar

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Jinergy

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 TW Solar

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Enel (3SUN)

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Hevel Solar

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 EcoSolifer

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 Panasonic

List of Figures

- Figure 1: Global Silicon Based Heterojunction Solar Cell Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global Silicon Based Heterojunction Solar Cell Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Application 2024 & 2032

- Figure 4: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Application 2024 & 2032

- Figure 5: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Application 2024 & 2032

- Figure 6: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Application 2024 & 2032

- Figure 7: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Type 2024 & 2032

- Figure 8: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Type 2024 & 2032

- Figure 9: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Type 2024 & 2032

- Figure 10: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Type 2024 & 2032

- Figure 11: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Country 2024 & 2032

- Figure 12: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Country 2024 & 2032

- Figure 13: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Country 2024 & 2032

- Figure 14: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Country 2024 & 2032

- Figure 15: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Application 2024 & 2032

- Figure 16: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Application 2024 & 2032

- Figure 17: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Application 2024 & 2032

- Figure 18: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Application 2024 & 2032

- Figure 19: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Type 2024 & 2032

- Figure 20: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Type 2024 & 2032

- Figure 21: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Type 2024 & 2032

- Figure 22: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Type 2024 & 2032

- Figure 23: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Country 2024 & 2032

- Figure 24: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Country 2024 & 2032

- Figure 25: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Country 2024 & 2032

- Figure 26: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Country 2024 & 2032

- Figure 27: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Application 2024 & 2032

- Figure 28: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Application 2024 & 2032

- Figure 29: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Application 2024 & 2032

- Figure 30: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Application 2024 & 2032

- Figure 31: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Type 2024 & 2032

- Figure 32: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Type 2024 & 2032

- Figure 33: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Type 2024 & 2032

- Figure 34: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Type 2024 & 2032

- Figure 35: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Country 2024 & 2032

- Figure 36: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Country 2024 & 2032

- Figure 37: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Country 2024 & 2032

- Figure 38: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Country 2024 & 2032

- Figure 39: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Application 2024 & 2032

- Figure 40: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Application 2024 & 2032

- Figure 41: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Application 2024 & 2032

- Figure 42: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Application 2024 & 2032

- Figure 43: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Type 2024 & 2032

- Figure 44: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Type 2024 & 2032

- Figure 45: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Type 2024 & 2032

- Figure 46: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Type 2024 & 2032

- Figure 47: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Country 2024 & 2032

- Figure 48: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Country 2024 & 2032

- Figure 49: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Country 2024 & 2032

- Figure 50: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Country 2024 & 2032

- Figure 51: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Application 2024 & 2032

- Figure 52: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Application 2024 & 2032

- Figure 53: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Application 2024 & 2032

- Figure 54: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Application 2024 & 2032

- Figure 55: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Type 2024 & 2032

- Figure 56: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Type 2024 & 2032

- Figure 57: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Type 2024 & 2032

- Figure 58: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Type 2024 & 2032

- Figure 59: undefined Silicon Based Heterojunction Solar Cell Revenue (million), by Country 2024 & 2032

- Figure 60: undefined Silicon Based Heterojunction Solar Cell Volume (K), by Country 2024 & 2032

- Figure 61: undefined Silicon Based Heterojunction Solar Cell Revenue Share (%), by Country 2024 & 2032

- Figure 62: undefined Silicon Based Heterojunction Solar Cell Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Region 2019 & 2032

- Table 3: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Application 2019 & 2032

- Table 5: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Type 2019 & 2032

- Table 7: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Region 2019 & 2032

- Table 9: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Application 2019 & 2032

- Table 10: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Application 2019 & 2032

- Table 11: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Type 2019 & 2032

- Table 13: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Country 2019 & 2032

- Table 15: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Application 2019 & 2032

- Table 16: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Application 2019 & 2032

- Table 17: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Type 2019 & 2032

- Table 18: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Type 2019 & 2032

- Table 19: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Country 2019 & 2032

- Table 20: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Country 2019 & 2032

- Table 21: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Application 2019 & 2032

- Table 22: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Application 2019 & 2032

- Table 23: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Type 2019 & 2032

- Table 24: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Type 2019 & 2032

- Table 25: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Country 2019 & 2032

- Table 27: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Application 2019 & 2032

- Table 28: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Application 2019 & 2032

- Table 29: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Type 2019 & 2032

- Table 30: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Type 2019 & 2032

- Table 31: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Country 2019 & 2032

- Table 32: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Country 2019 & 2032

- Table 33: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Application 2019 & 2032

- Table 34: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Application 2019 & 2032

- Table 35: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Type 2019 & 2032

- Table 36: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Type 2019 & 2032

- Table 37: Global Silicon Based Heterojunction Solar Cell Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global Silicon Based Heterojunction Solar Cell Volume K Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Silicon Based Heterojunction Solar Cell?

The projected CAGR is approximately 15%.

2. Which companies are prominent players in the Silicon Based Heterojunction Solar Cell?

Key companies in the market include Panasonic, REC, AE Solar TIER1 Company, Belinus, HUASUN, Longi Green Energy Technology Co.,Ltd., Hangzhou Hanfy New Energy Technology Co., Ltd., Suzhou Maxwell Technologies Co.,Ltd., GANSU GOLDEN GLASS, Risen Energy Co.,Ltd., Tongwei Co.,Ltd., Marvel, Canadian Solar, AKCOME, Meyer Burge, GS-Solar, Jinergy, TW Solar, Enel (3SUN), Hevel Solar, EcoSolifer.

3. What are the main segments of the Silicon Based Heterojunction Solar Cell?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 5155 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Silicon Based Heterojunction Solar Cell," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Silicon Based Heterojunction Solar Cell report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Silicon Based Heterojunction Solar Cell?

To stay informed about further developments, trends, and reports in the Silicon Based Heterojunction Solar Cell, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence