Key Insights into South Korea Mobile Payment Industry

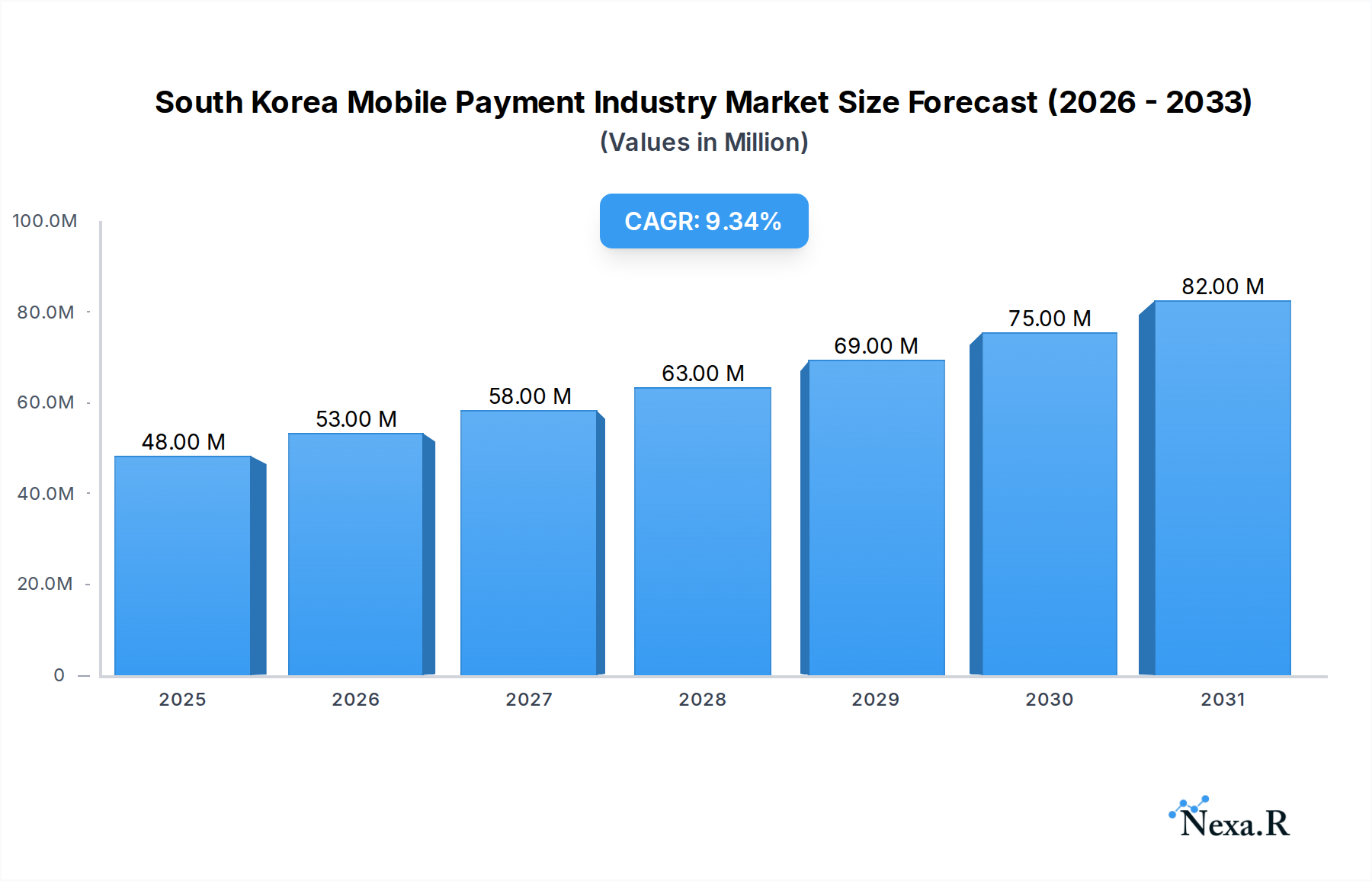

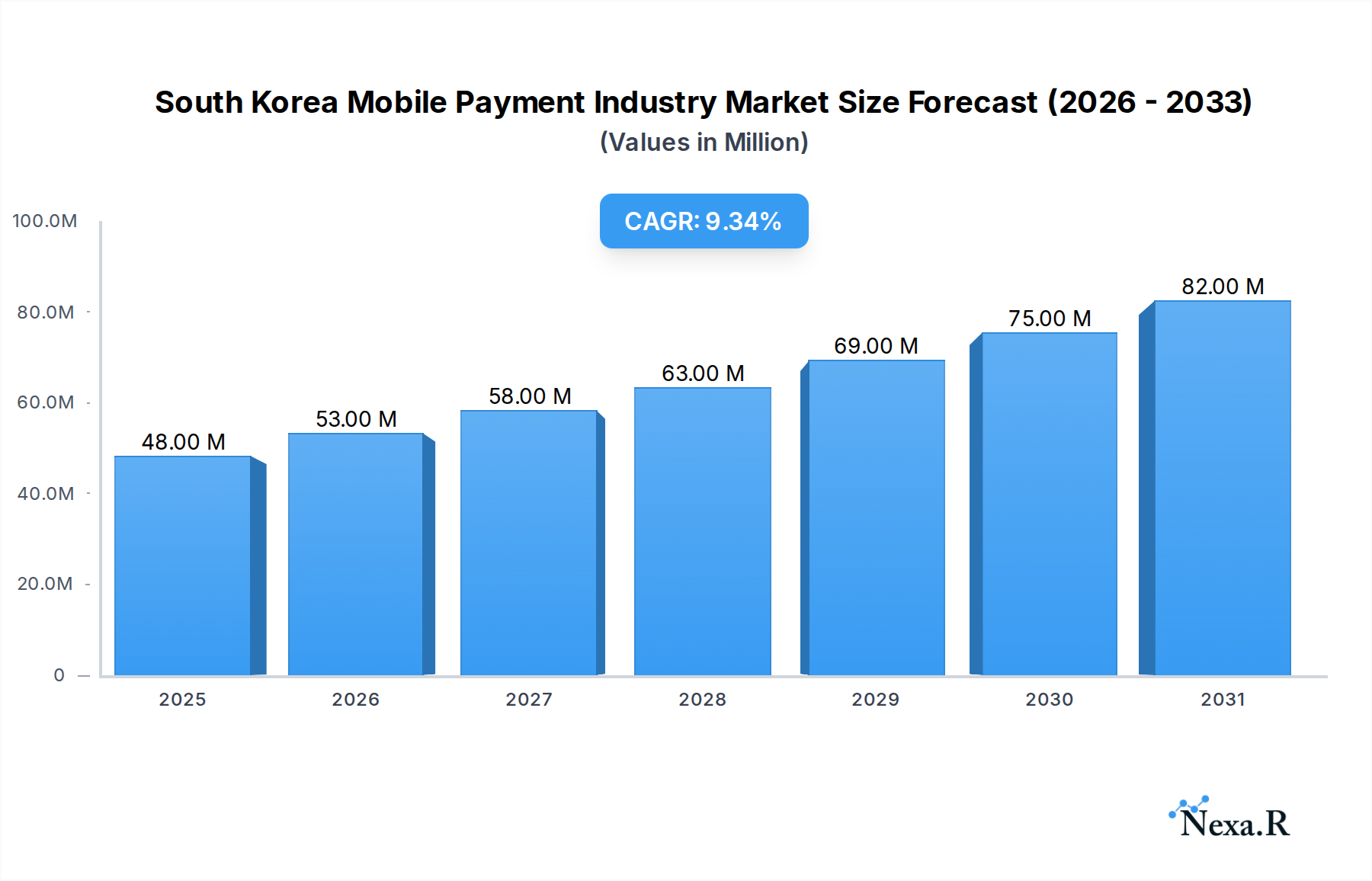

The South Korea Mobile Payment Industry is experiencing robust expansion, driven by widespread smartphone adoption, advanced digital infrastructure, and a highly tech-savvy population. As of the latest reporting period, the market is valued at USD 40.67 Million, demonstrating significant potential for future growth. Analysts project a robust Compound Annual Growth Rate (CAGR) of 9.13% from 2026 to 2034, which is anticipated to propel the market valuation to approximately USD 97.57 Million by 2034. This growth trajectory is underpinned by several key demand drivers, primarily the increasing adoption of mobile devices and the surging demand and inclination towards e-commerce and online shopping. The proliferation of smartphones and high internet penetration rates have created a fertile ground for mobile payment solutions, integrating them seamlessly into daily consumer transactions. Furthermore, the burgeoning e-commerce sector acts as a powerful catalyst, driving transaction volumes and fostering innovation in payment methods.

South Korea Mobile Payment Industry Market Size (In Million)

Macroeconomic tailwinds, such as sustained economic growth and government initiatives promoting digital transformation, further support the market's expansion. The continuous evolution of payment technologies, including advancements in QR code payments, Near Field Communication (NFC), and mobile applications, contributes significantly to consumer convenience and security, thereby accelerating adoption. However, the market faces challenges, prominently the growing cyber threats in the region, which necessitate continuous investment in robust security infrastructure and consumer trust-building measures. Despite these challenges, the overarching trend points towards a future where the E-commerce Industry is expected to drive the growth of the market, with mobile payments becoming an indispensable component of the broader digital commerce ecosystem. The competitive landscape is dynamic, characterized by fierce innovation among established players and emerging fintech companies, all vying for market share in this lucrative sector. The South Korea Mobile Payment Industry is poised for sustained growth, underpinned by technological advancements and evolving consumer preferences.

South Korea Mobile Payment Industry Company Market Share

Dominance of Remote Payments in South Korea Mobile Payment Industry

Within the South Korea Mobile Payment Industry, the remote payment segment is anticipated to hold the dominant market share by revenue, a trend largely fueled by the exponential growth of e-commerce and the increasing sophistication of mobile banking and shopping applications. Remote payment transactions, which include online purchases made via mobile devices, in-app payments, and direct mobile billing, far outpace traditional in-store Proximity Payment Market transactions in overall value and volume. This dominance is intrinsically linked to South Korea's high internet penetration and advanced digital infrastructure, which facilitates seamless online shopping experiences. Consumers in South Korea extensively utilize their smartphones not just for communication but as primary tools for online retail, content consumption, and financial management.

Key players like Kakao Pay, Naver Pay, and Coupang's proprietary payment systems have heavily invested in robust remote payment infrastructures, offering a multitude of services from simple click-to-pay options to complex installment plans, all accessible via mobile devices. The convenience of executing transactions from any location, without the physical presence of a card or cash, resonates strongly with the modern Korean lifestyle. The increasing penetration of the Digital Wallet Market, where users store multiple payment methods, loyalty cards, and even digital IDs, further solidifies the position of remote payments. These digital wallets are primarily utilized for online and in-app transactions, contributing significantly to the Remote Payment Market segment's growth.

The widespread adoption of dedicated Mobile App Payment Market solutions, offered by various financial institutions, e-commerce platforms, and telecommunication companies, has also been a critical factor. These apps often integrate personalized promotions, loyalty programs, and streamlined checkout processes, enhancing the user experience and encouraging repeat usage. While the Proximity Payment Market, encompassing technologies like Near Field Communication Market (NFC) and QR Code Payment Market, continues to grow, its revenue share is comparatively smaller than remote payments. The COVID-19 pandemic further accelerated the shift towards online transactions, consolidating the leadership position of the remote payment segment. This trend is expected to continue, with ongoing innovations in security, user experience, and integration with emerging technologies ensuring sustained growth for remote payments in the South Korea Mobile Payment Industry.

Key Drivers and Constraints Shaping South Korea Mobile Payment Industry

Several intrinsic factors are propelling the growth of the South Korea Mobile Payment Industry, while certain challenges necessitate strategic mitigation. A primary driver is the Increasing Adoption of Mobile Devices. South Korea boasts one of the highest smartphone penetration rates globally, with nearly 95% of its population owning a smartphone. This ubiquitous access to mobile technology forms the foundational ecosystem for the expansion of mobile payment services. The high usage frequency of these devices for daily activities, from communication to content consumption, naturally extends to financial transactions, making mobile payments an intuitive and convenient choice for consumers. The continuous advancements in smartphone technology, offering enhanced security features and user interfaces, further encourage greater adoption of these payment methods.

Another significant catalyst is The Growing Demand and Inclination Towards E-commerce and Online Shopping. South Korea's e-commerce sector is a global powerhouse, consistently ranking among the top markets worldwide. This robust Online Retail Market creates an immense demand for seamless and secure digital payment solutions. Mobile payments are the preferred transaction method for a vast majority of online purchases due to their speed and convenience. The integration of payment gateways directly into e-commerce platforms and shopping applications has streamlined the checkout process, directly boosting transaction volumes for the E-commerce Payment Market. The trend indicates that the E-commerce Industry is expected to drive the growth of the market, reinforcing the symbiotic relationship between online retail and mobile payments.

Conversely, a prominent constraint on the South Korea Mobile Payment Industry is the Growing Cyber Threats in the region. As mobile payment systems become more sophisticated and integrated into various aspects of daily life, they simultaneously become attractive targets for cybercriminals. Data breaches, phishing scams, malware attacks, and identity theft pose significant risks, undermining consumer trust and potentially leading to substantial financial losses. Service providers and financial institutions must invest heavily in advanced cybersecurity measures, including multi-factor authentication, tokenization, and real-time fraud detection systems. Regulatory bodies also play a crucial role in establishing stringent security standards and frameworks to protect consumer data and ensure the integrity of the mobile payment ecosystem, thereby mitigating the impact of these persistent cyber threats.

Pricing Dynamics and Margin Pressures in South Korea Mobile Payment Industry

The pricing dynamics within the South Korea Mobile Payment Industry are highly competitive, characterized by intense pressure on transaction fees and an evolving margin structure across the value chain. Average Selling Price (ASP) for mobile payment services is primarily represented by merchant discount rates (MDRs) or interchange fees charged per transaction, as well as subscription fees for value-added services. These fees vary significantly based on merchant size, transaction volume, and the type of payment service utilized (e.g., credit card-linked, bank transfer, or digital wallet). Major players often engage in aggressive pricing strategies, sometimes offering zero or minimal transaction fees to small and medium-sized enterprises (SMEs) to gain market share, particularly for QR Code Payment Market services, which can have lower infrastructure costs compared to NFC-based transactions.

Margin structures for mobile payment providers are influenced by several key cost levers, including technology infrastructure investment, marketing and customer acquisition costs, regulatory compliance expenditures, and robust cybersecurity measures. Building and maintaining secure, scalable platforms for high transaction volumes requires substantial capital outlays. Furthermore, the battle for consumer adoption and merchant onboarding necessitates significant marketing spend and incentive programs. The competitive intensity from dominant players like Kakao Pay, Samsung Pay, and Naver Pay, who benefit from extensive user bases and integrated ecosystems, creates downward pressure on margins for smaller or newer entrants. These giants can leverage their existing user data and platform synergies to offer more competitive pricing or bundle payment services with other offerings.

Commodity cycles, while not directly impacting software-based payment services, can indirectly affect consumer spending patterns and merchant revenues, thereby influencing transaction volumes and the overall profitability of payment providers. For instance, economic downturns might reduce discretionary spending, impacting merchant sales and subsequently the revenue streams of mobile payment platforms. The regulatory environment also plays a role, with initiatives like ZeroPay aiming to reduce merchant fees, further impacting the pricing power of commercial payment providers. This environment compels companies to constantly innovate, seek operational efficiencies, and diversify revenue streams beyond transaction processing to maintain healthy margins within the highly dynamic South Korea Mobile Payment Industry.

Regulatory and Policy Landscape Shaping South Korea Mobile Payment Industry

The South Korea Mobile Payment Industry operates under a sophisticated and evolving regulatory framework designed to foster innovation while ensuring financial stability, consumer protection, and data security. The primary regulatory bodies include the Financial Services Commission (FSC) and the Bank of Korea (BOK). The FSC is responsible for supervising the overall financial industry, including licensing and oversight of electronic financial transaction service providers. The BOK, as the central bank, oversees the payment and settlement systems, ensuring their safety and efficiency. Key legislation such as the Electronic Financial Transactions Act (EFTA) governs the rights and responsibilities of parties involved in electronic financial transactions, setting standards for security, data protection, and dispute resolution.

Recent policy changes have aimed at promoting open competition and enhancing user convenience. The introduction of Open Banking in South Korea has significantly impacted the Fintech Market, allowing third-party fintech companies to access customer bank account information (with consent) to offer innovative financial services, including aggregated payment solutions and personal financial management tools. This has intensified competition among traditional banks and fintech disruptors, driving down costs and improving service quality within the South Korea Mobile Payment Industry. Additionally, the government has supported initiatives like ZeroPay, a QR-code-based mobile payment system aimed at reducing transaction fees for small businesses. While ZeroPay's market penetration has been somewhat challenging against established commercial players, it reflects a policy objective to create a more equitable payment ecosystem.

Data privacy regulations, particularly the Personal Information Protection Act (PIPA), are critically important, imposing strict requirements on how personal data, including payment information, is collected, processed, stored, and shared. Compliance with these stringent data protection laws requires significant investment from mobile payment providers to safeguard user information and prevent cyber threats. Any breach of these regulations can result in severe penalties and reputational damage. Future policy developments are expected to focus on further integrating emerging technologies like blockchain for secure transactions, regulating digital assets, and harmonizing national payment systems with international standards to facilitate cross-border mobile payments. These regulatory and policy landscapes are continuously shaping the competitive dynamics and operational requirements for all participants in the South Korea Mobile Payment Industry.

Competitive Ecosystem of South Korea Mobile Payment Industry

The South Korea Mobile Payment Industry is characterized by an intensely competitive landscape, dominated by a few large technology and financial conglomerates that leverage their extensive user bases and comprehensive digital ecosystems. Innovation and strategic partnerships are crucial for maintaining and expanding market share.

- Kakao Pay: As an affiliate of the popular KakaoTalk messaging app, Kakao Pay benefits from an immense captive user base. It offers a broad spectrum of financial services, including payments, remittances, asset management, and insurance, aiming to be a comprehensive digital financial platform.

- Samsung Pay: Integrated into Samsung smartphones, Samsung Pay offers both NFC and Magnetic Secure Transmission (MST) capabilities, giving it broad acceptance at traditional card terminals. It focuses on seamless, secure in-store and online payments and integrates with various loyalty programs.

- Toss: Operated by Viva Republica, Toss is a rapidly growing fintech platform that started with easy money transfers and has expanded into a full suite of financial services, including credit scores, insurance, and investment products, appealing particularly to younger demographics.

- PayCo: Backed by NHN Entertainment, PayCo offers online and offline payment services, focusing on integration with various e-commerce platforms and gaming services. It strives for user convenience and a diversified service portfolio.

- SK Group: Through its subsidiary SK Planet, SK Group operates Syrup Pay, a mobile wallet service. SK Group leverages its telecommunications infrastructure and extensive retail network to integrate payment solutions across its diverse business ventures.

- L Pay: As a part of the Lotte Group, L Pay is deeply integrated into Lotte's vast retail empire, including department stores, supermarkets, and online malls. It primarily serves to enhance the shopping experience for Lotte customers with loyalty programs and exclusive offers.

- ZeroPay Pvt. Ltd.: A government-backed initiative, ZeroPay aims to reduce transaction fees for small businesses through its QR code payment system. It collaborates with various banks and fintech companies to expand its network and promote a cashless society.

- Coupang: As the largest e-commerce platform in South Korea, Coupang operates its own robust payment system for seamless checkout experiences within its ecosystem. Its payment solution is a critical component of its end-to-end customer journey.

- SSG.com Corp: The online retail arm of Shinsegae Group, SSG.com offers its own integrated payment solutions, enhancing convenience for shoppers across its online and offline retail channels, including department stores and hypermarkets.

- Naver Pay: Affiliated with the dominant search engine Naver, Naver Pay leverages a massive user base and integrates payments across Naver's extensive services, including online shopping, content subscriptions, and booking services, making it a powerful player in the

Fintech Market. - Others: This category includes smaller fintech startups, international payment service providers entering the market, and specialized payment solutions catering to niche segments, all contributing to the dynamic and evolving landscape of the South Korea Mobile Payment Industry.

Recent Developments & Milestones in South Korea Mobile Payment Industry

The South Korea Mobile Payment Industry has witnessed several pivotal developments in recent years, reflecting continuous innovation, strategic collaborations, and global expansion efforts by key players:

- February 2024: The TWQR mobile payment service was officially launched in South Korea. This significant development marks a collaboration between Taiwanese organizations and the South Korean financial services company BC Card Co. The service rapidly expanded its reach, becoming available at 35,000 merchants across the East Asian country, aiming to enhance convenience for Taiwanese tourists and local users by leveraging QR code technology for seamless transactions.

- April 2023: Kakao Pay, the online payment service division of South Korean messaging and internet giant Kakao, made a strategic move into the global financial markets. The company declared its acquisition of a 19.9% stake in Siebert Financial, a brokerage firm based in New York. This transaction involved an investment of USD 17 million, signifying Kakao Pay's ambitions to expand its financial services footprint beyond domestic borders and tap into international brokerage capabilities.

These developments highlight a trend towards internationalization and the diversification of mobile payment offerings, reinforcing South Korea's position as a leader in digital commerce and fintech innovation.

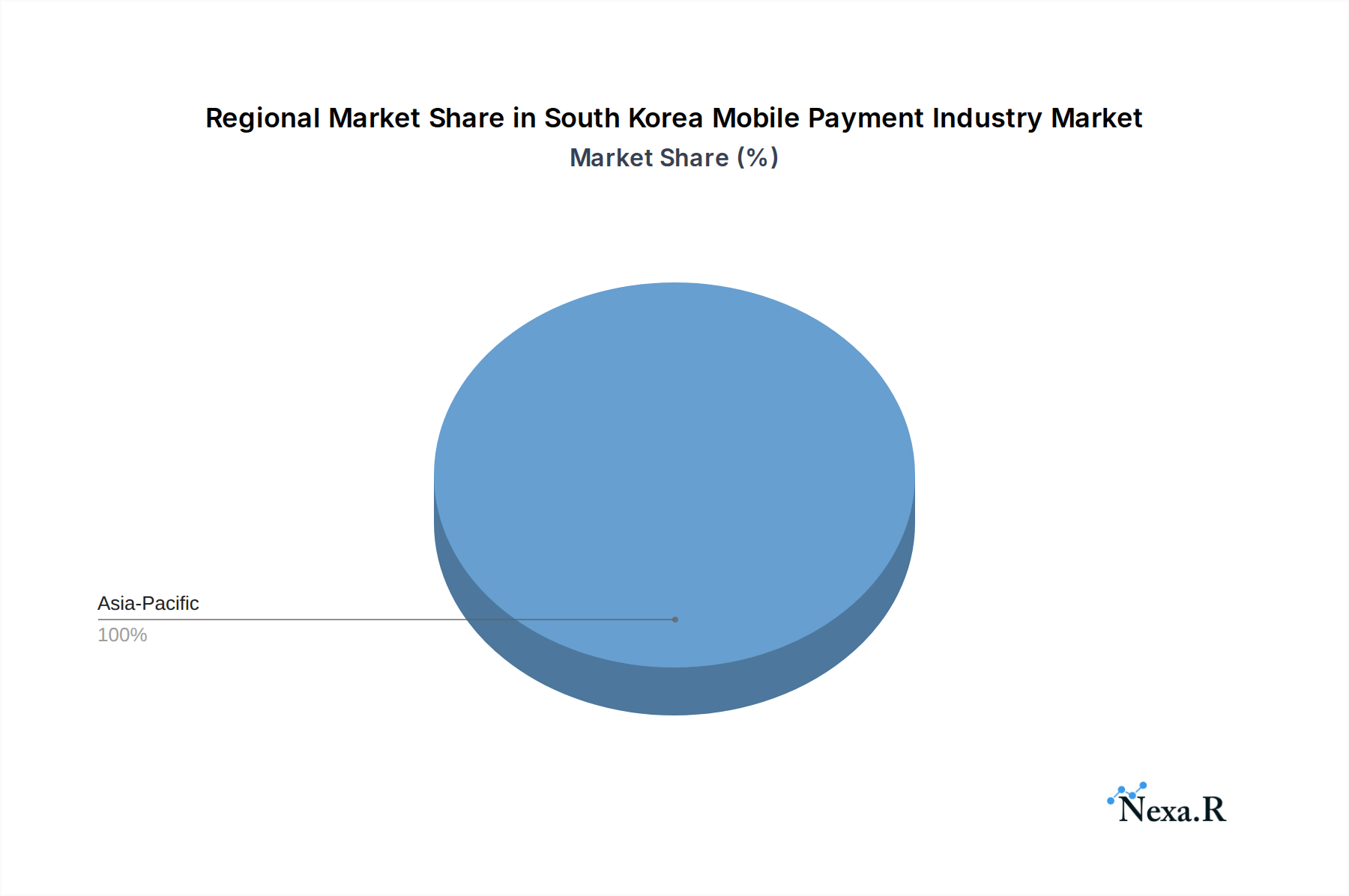

Internal Geographical Dynamics Driving South Korea Mobile Payment Industry

Given the specificity of this report to the South Korea Mobile Payment Industry, a direct comparison of four distinct national or supra-national regions is not applicable. Instead, this section will analyze key internal geographical and demographic differentiators within South Korea that influence mobile payment adoption and growth. While specific regional CAGRs or absolute revenue shares for sub-national areas are not uniformly available in the provided data, a qualitative assessment reveals distinct patterns across the nation.

Seoul Metropolitan Area (Seoul, Incheon, Gyeonggi Province): This densely populated megalopolis serves as the undeniable epicenter of the South Korea Mobile Payment Industry. Characterized by high concentrations of tech-savvy early adopters, a robust digital infrastructure, and a significant presence of corporate headquarters, fintech startups, and major retail hubs, this region exhibits the highest penetration and transaction volumes for mobile payments. Innovation often originates here, with new services and technologies, including Near Field Communication Market advancements and advanced Mobile App Payment Market features, first gaining traction before expanding nationwide. The primary demand driver is convenience and the pervasive digital lifestyle.

Busan-Ulsan-Gyeongnam (Southeast Economic Zone): As a major industrial and port region, this area represents a significant economic cluster outside the capital. Mobile payment adoption here is strong, driven by a combination of a large working population, expanding urban centers, and increasing integration of digital payments into daily commercial activities. The

E-commerce Payment Marketsees robust growth here, supported by logistics and manufacturing bases. The primary demand driver is a growing urban population embracing digital solutions for efficiency.Daejeon-Sejong-Chungcheong Region (Central & Innovation Hub): This region is emerging as a critical hub for government administration, research, and development. With the presence of government offices in Sejong and numerous research institutions in Daejeon, there's a strong emphasis on digital services and smart city initiatives. Mobile payment adoption is driven by governmental support for digital transformation and a highly educated populace. The primary demand driver is government-led digitalization and a technically proficient population.

Jeolla and Gyeongsang Provinces (Rural and Secondary Urban Areas): These regions, encompassing a mix of secondary cities and more rural landscapes, typically show a slower but steady growth in mobile payment adoption. While major urban centers within these provinces will mirror trends seen in larger cities, broader adoption in less-dense areas is often driven by the increasing necessity for cashless transactions, especially for essential services, and the expansion of coverage by national payment providers. The primary demand driver here is increasing accessibility to digital infrastructure and the convenience of mobile payments gradually replacing cash in daily transactions, particularly for the

Online Retail Marketin smaller communities.

South Korea Mobile Payment Industry Segmentation

-

1. Mode

- 1.1. Proximity Payment

- 1.2. Remote Payment

-

2. Payment Type

- 2.1. B2B

- 2.2. B2C

- 2.3. B2G

-

3. Technology

- 3.1. Near Field Communication (NFC)

- 3.2. QR Code Payment

- 3.3. Mobile Web Payment

- 3.4. Direct Mobile Billing

- 3.5. Mobile Apps

- 3.6. Wireless Application Protocol (WAP)

- 3.7. Others

-

4. Industry Vertical

- 4.1. Media & Entertainment

- 4.2. Retail & E-commerce

- 4.3. BFSI

- 4.4. Automotive

- 4.5. Medical & Healthcare

- 4.6. Transportation

- 4.7. Consumer Electronics

- 4.8. Others

South Korea Mobile Payment Industry Segmentation By Geography

- 1. South Korea

South Korea Mobile Payment Industry Regional Market Share

Geographic Coverage of South Korea Mobile Payment Industry

South Korea Mobile Payment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Mode

- 5.1.1. Proximity Payment

- 5.1.2. Remote Payment

- 5.2. Market Analysis, Insights and Forecast - by Payment Type

- 5.2.1. B2B

- 5.2.2. B2C

- 5.2.3. B2G

- 5.3. Market Analysis, Insights and Forecast - by Technology

- 5.3.1. Near Field Communication (NFC)

- 5.3.2. QR Code Payment

- 5.3.3. Mobile Web Payment

- 5.3.4. Direct Mobile Billing

- 5.3.5. Mobile Apps

- 5.3.6. Wireless Application Protocol (WAP)

- 5.3.7. Others

- 5.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 5.4.1. Media & Entertainment

- 5.4.2. Retail & E-commerce

- 5.4.3. BFSI

- 5.4.4. Automotive

- 5.4.5. Medical & Healthcare

- 5.4.6. Transportation

- 5.4.7. Consumer Electronics

- 5.4.8. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. South Korea

- 5.1. Market Analysis, Insights and Forecast - by Mode

- 6. South Korea Mobile Payment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Mode

- 6.1.1. Proximity Payment

- 6.1.2. Remote Payment

- 6.2. Market Analysis, Insights and Forecast - by Payment Type

- 6.2.1. B2B

- 6.2.2. B2C

- 6.2.3. B2G

- 6.3. Market Analysis, Insights and Forecast - by Technology

- 6.3.1. Near Field Communication (NFC)

- 6.3.2. QR Code Payment

- 6.3.3. Mobile Web Payment

- 6.3.4. Direct Mobile Billing

- 6.3.5. Mobile Apps

- 6.3.6. Wireless Application Protocol (WAP)

- 6.3.7. Others

- 6.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 6.4.1. Media & Entertainment

- 6.4.2. Retail & E-commerce

- 6.4.3. BFSI

- 6.4.4. Automotive

- 6.4.5. Medical & Healthcare

- 6.4.6. Transportation

- 6.4.7. Consumer Electronics

- 6.4.8. Others

- 6.1. Market Analysis, Insights and Forecast - by Mode

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Kakao Pay

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Samsung Pay

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Toss

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 PayCo

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 SK Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 L Pay

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 ZeroPay Pvt. Ltd.

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Coupang

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 SSG.com Corp

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Naver Pay

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Others

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Kakao Pay

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South Korea Mobile Payment Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: South Korea Mobile Payment Industry Share (%) by Company 2025

List of Tables

- Table 1: South Korea Mobile Payment Industry Revenue Million Forecast, by Mode 2020 & 2033

- Table 2: South Korea Mobile Payment Industry Revenue Million Forecast, by Payment Type 2020 & 2033

- Table 3: South Korea Mobile Payment Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 4: South Korea Mobile Payment Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 5: South Korea Mobile Payment Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: South Korea Mobile Payment Industry Revenue Million Forecast, by Mode 2020 & 2033

- Table 7: South Korea Mobile Payment Industry Revenue Million Forecast, by Payment Type 2020 & 2033

- Table 8: South Korea Mobile Payment Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 9: South Korea Mobile Payment Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 10: South Korea Mobile Payment Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South Korea Mobile Payment Industry?

The projected CAGR is approximately 9.13%.

2. Which companies are prominent players in the South Korea Mobile Payment Industry?

Key companies in the market include Kakao Pay, Samsung Pay, Toss, PayCo, SK Group, L Pay, ZeroPay Pvt. Ltd., Coupang, SSG.com Corp, Naver Pay, Others.

3. What are the main segments of the South Korea Mobile Payment Industry?

The market segments include Mode, Payment Type, Technology, Industry Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 40.67 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Mobile Devices; The Growing Demand and Inclination Towards E-commerce and Online Shopping.

6. What are the notable trends driving market growth?

E-commerce Industry is expected to drive the growth of the market.

7. Are there any restraints impacting market growth?

Growing Cyber Threats in the region.

8. Can you provide examples of recent developments in the market?

Frebruary 2024 - TWQR mobile payment service launched in South Korea. The mobile payment service, available at 35,000 merchants in the East Asian country, is a collaboration between the two Taiwanese organizations and the South Korean financial services company BC Card Co, per the statement.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South Korea Mobile Payment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South Korea Mobile Payment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South Korea Mobile Payment Industry?

To stay informed about further developments, trends, and reports in the South Korea Mobile Payment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence