Key Insights

The Sucrose Initiated Polyether Polyols market is poised for substantial growth, projected to reach a considerable market size in 2025, driven by a strong CAGR of approximately 6.5%. This expansion is primarily fueled by the increasing demand from key application sectors such as home appliances, where these polyols are integral to the production of insulation foams for refrigerators and freezers, and the construction industry for insulation materials. The growing emphasis on energy efficiency and sustainable building practices further bolsters this demand. Additionally, the burgeoning use of sucrose initiated polyether polyols in flexible and rigid foam applications, including automotive interiors and industrial insulation, is a significant growth catalyst. The market’s robust growth trajectory is further supported by ongoing innovations in product development, leading to polyols with enhanced properties like improved fire retardancy and greater flexibility, catering to evolving industry needs.

The market is segmented into low, medium, and high reactive types, with medium and high reactive variants likely dominating due to their versatility and suitability for a wider range of applications, particularly in rigid foam production for insulation and structural components. Restraints, such as fluctuating raw material prices and the availability of alternative polyol types, are present. However, the inherent advantages of sucrose initiated polyether polyols, including their renewable origin and cost-effectiveness, are expected to mitigate these challenges. Geographically, Asia Pacific, led by China and India, is anticipated to be the largest and fastest-growing regional market, propelled by rapid industrialization and infrastructure development. North America and Europe also represent significant markets, driven by established home appliance industries and a strong focus on energy-efficient construction. Companies such as BASF, Covestro, and Dow are actively investing in research and development to expand their product portfolios and market reach, solidifying their positions in this dynamic market.

Here's the SEO-optimized report description for Sucrose Initiated Polyether Polyols, designed to maximize visibility and engagement:

Report Title: Global Sucrose Initiated Polyether Polyols Market Analysis: Growth, Trends, and Forecast 2019-2033

Report Description:

Gain unparalleled insights into the dynamic global Sucrose Initiated Polyether Polyols market with this comprehensive research report. Spanning from 2019 to 2033, with a deep dive into the base year 2025 and an extensive forecast period of 2025–2033, this study meticulously analyzes market structure, growth trajectories, regional dominance, and the intricate product landscape. We provide actionable intelligence for stakeholders navigating the polyether polyols industry, including manufacturers, suppliers, formulators, and end-users in sectors such as Home Appliances, Sheet, Pipeline, and Other Applications. Uncover the strategic advantages of different polyol types, from Low Reactive, Medium Reactive, to High Reactive variants, and understand their impact across diverse market segments.

This report offers a granular view of the market, exploring technological innovation drivers, regulatory frameworks, and the competitive interplay of product substitutes. Examine end-user demographics and pivotal M&A trends within the parent and child market for sucrose initiated polyether polyols. With quantitative data presented in million units and qualitative analysis, this report is an essential resource for strategic decision-making.

Sucrose Initiated Polyether Polyols Market Dynamics & Structure

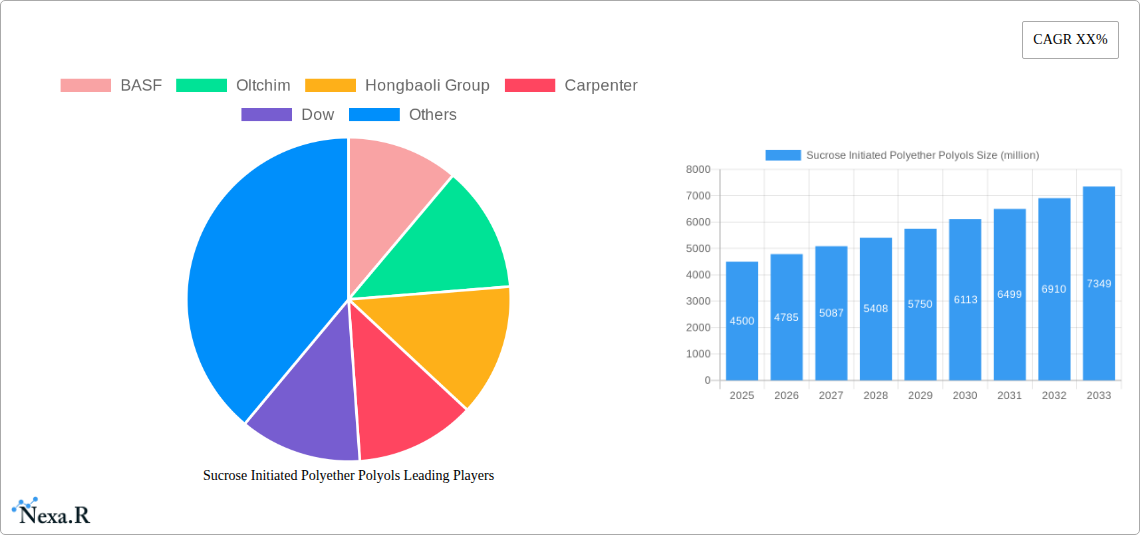

The global Sucrose Initiated Polyether Polyols market exhibits a moderately consolidated structure, with leading players like BASF, Dow, Covestro, and Oltchim holding significant market shares. Technological innovation remains a primary driver, fueled by the demand for enhanced performance in polyurethane applications. Key innovations focus on improving flame retardancy, increasing durability, and developing bio-based polyol alternatives. Regulatory frameworks, particularly concerning environmental sustainability and product safety, are increasingly influencing manufacturing processes and raw material sourcing. Competitive product substitutes, such as petroleum-based polyols, continue to pose a challenge, though sucrose-initiated polyols are gaining traction due to their renewable origin. End-user demographics are shifting towards sustainability-conscious consumers and industries, driving the demand for greener chemical solutions. Mergers and acquisitions (M&A) activity is notable, with companies aiming to expand their product portfolios, gain market access, and achieve economies of scale. For instance, a projected volume of approximately 150 million units in M&A transactions is anticipated in the coming years, signaling strategic consolidation.

- Market Concentration: Moderately consolidated with key players dominating the landscape.

- Technological Innovation Drivers: Demand for enhanced performance (flame retardancy, durability), sustainability, and bio-based alternatives.

- Regulatory Frameworks: Environmental regulations (e.g., REACH, VOC limits) and product safety standards are critical.

- Competitive Product Substitutes: Petroleum-based polyols, other renewable polyols.

- End-User Demographics: Growing demand from sustainable industries and environmentally conscious consumers.

- M&A Trends: Strategic acquisitions to expand portfolios and market reach, with an estimated 150 million units in deal volume.

Sucrose Initiated Polyether Polyols Growth Trends & Insights

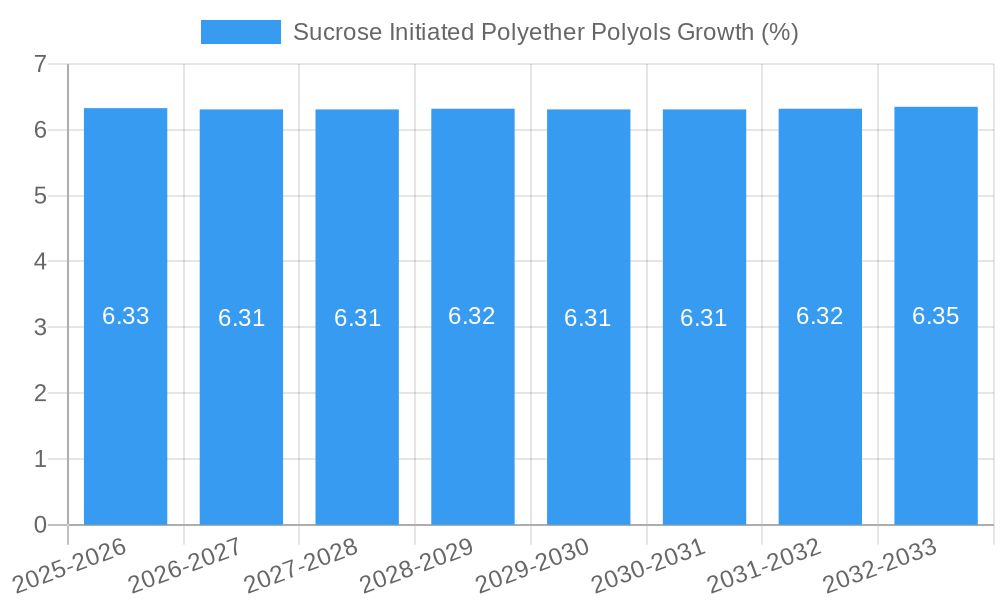

The Sucrose Initiated Polyether Polyols market is poised for significant growth, driven by the escalating demand for high-performance and sustainable polyurethane materials across various industries. The market size is projected to expand from an estimated 1,200 million units in 2019 to a substantial 2,850 million units by 2033. This robust expansion is underpinned by an average Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period. Adoption rates are accelerating, particularly in applications where the unique properties of sucrose-initiated polyols, such as excellent hydrolytic stability and good flexibility, are highly valued. Technological disruptions, including advancements in catalyst technology for more efficient polymerization and the development of novel sucrose derivatives, are further fueling market penetration. Consumer behavior shifts are a significant catalyst; there's a discernible preference for products manufactured using bio-based and renewable materials, which directly benefits sucrose-initiated polyols. The parent market for all polyether polyols is estimated to reach over 8,500 million units by 2033, with sucrose-initiated variants capturing an increasingly larger share, projected to be around 33% of this total. This growth is also influenced by supportive government initiatives promoting the use of renewable resources and sustainable manufacturing practices. The increasing awareness of the environmental impact of conventional chemicals is pushing industries to seek greener alternatives, creating a fertile ground for sucrose-initiated polyether polyols. Furthermore, advancements in processing technologies are enabling the production of customized polyols with specific properties tailored to niche applications, thereby expanding the market's reach. The integration of advanced computational modeling for polyol design and optimization is also contributing to faster innovation cycles and improved product performance, further stimulating market adoption.

Dominant Regions, Countries, or Segments in Sucrose Initiated Polyether Polyols

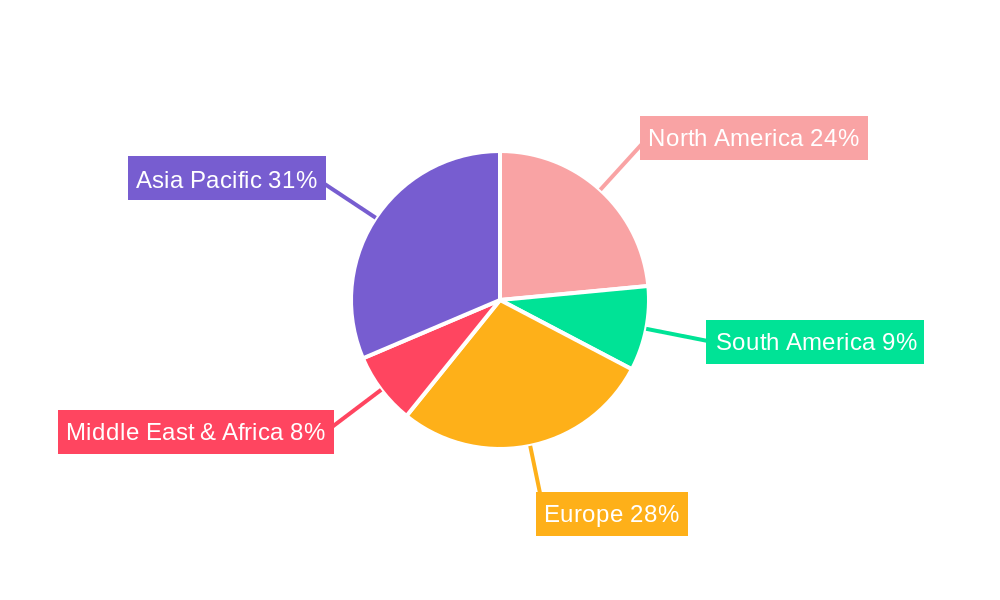

The global Sucrose Initiated Polyether Polyols market is witnessing significant growth across various regions and applications, with Asia Pacific emerging as a dominant force. This region's dominance is attributed to its robust manufacturing base, expanding industrial sectors, and favorable government policies promoting chemical innovation and production. Within Asia Pacific, China stands out as a key growth driver, fueled by its substantial investments in infrastructure, a burgeoning automotive industry, and a rapidly growing Home Appliances sector, which is a major consumer of polyurethanes derived from these polyols. The Sheet application segment also exhibits strong growth potential, particularly for insulation and packaging materials. The Pipeline sector, driven by energy exploration and infrastructure development, is another significant contributor to market expansion.

In terms of Types, the High Reactive sucrose initiated polyether polyols are experiencing the highest demand. This is largely due to their superior performance characteristics, such as faster curing times and enhanced mechanical properties, making them ideal for demanding applications in coatings, adhesives, sealants, and elastomers (CASE). The Medium Reactive segment also holds a substantial share, catering to a wider range of applications requiring a balance of reactivity and processing flexibility. While Low Reactive variants are more niche, they are crucial for specific applications demanding slower reaction kinetics. The Home Appliances segment, valued at approximately 450 million units in 2025, is a primary driver of demand, with manufacturers increasingly opting for energy-efficient and durable polyurethane foams. The Sheet segment is estimated at 300 million units, driven by construction and packaging. The Pipeline segment, valued at 220 million units, sees demand from insulation and protective coatings. The Other applications, encompassing furniture, automotive components, and bedding, collectively represent a significant market share, estimated at 280 million units. The growth in Asia Pacific is further propelled by its large population and increasing disposable income, which translates to higher consumption of end products utilizing these polyols. Favorable economic policies, including tax incentives and R&D grants, encourage local production and innovation, solidifying Asia Pacific's leading position.

Sucrose Initiated Polyether Polyols Product Landscape

The product landscape of Sucrose Initiated Polyether Polyols is characterized by a continuous stream of innovations aimed at enhancing performance and expanding application versatility. Manufacturers are focusing on developing polyols with tailored molecular weights, varying degrees of unsaturation, and controlled branching to achieve specific end-use properties. Key innovations include the development of low-VOC (Volatile Organic Compound) polyols for improved environmental profiles, highly resilient polyols for superior cushioning in furniture and bedding, and flame-retardant variants for enhanced safety in construction and home appliances. Performance metrics such as hydrolytic stability, thermal resistance, and mechanical strength are consistently being improved, enabling their use in more demanding environments.

Key Drivers, Barriers & Challenges in Sucrose Initiated Polyether Polyols

Key Drivers: The Sucrose Initiated Polyether Polyols market is propelled by several key factors. A primary driver is the growing global emphasis on sustainability and the increasing demand for bio-based and renewable chemical products. Sucrose, being a renewable feedstock, offers a significant advantage over petroleum-based alternatives. Advancements in polymerization technologies are leading to more efficient production processes and improved product quality, further stimulating demand. The expanding applications of polyurethanes across diverse industries, including construction, automotive, and consumer goods, directly translate into higher consumption of polyether polyols.

Barriers & Challenges: Despite the positive outlook, the market faces certain barriers and challenges. Fluctuations in the price and availability of raw materials, such as sucrose and propylene oxide, can impact production costs and profitability. The relatively higher cost of sucrose-initiated polyols compared to some petroleum-based counterparts can be a restraint in price-sensitive applications. Stringent regulatory requirements regarding chemical safety and environmental impact can also pose challenges for manufacturers. Competition from established petroleum-based polyols and other bio-based alternatives requires continuous innovation and cost optimization. Supply chain disruptions, as observed in recent global events, can affect the availability of key intermediates and finished products, impacting market stability.

Emerging Opportunities in Sucrose Initiated Polyether Polyols

Emerging opportunities in the Sucrose Initiated Polyether Polyols sector lie in the development of next-generation bio-based polyols with enhanced functionalities. The growing interest in circular economy principles presents an opportunity for developing polyols from recycled or upcycled feedstocks. Untapped markets in developing economies, driven by rapid industrialization and increasing consumer demand for sustainable products, offer significant growth potential. Innovative applications in niche areas such as medical devices, advanced composites, and energy-efficient building materials are also emerging. Evolving consumer preferences towards eco-friendly and high-performance materials will continue to create new avenues for market expansion.

Growth Accelerators in the Sucrose Initiated Polyether Polyols Industry

Several catalysts are accelerating growth in the Sucrose Initiated Polyether Polyols industry. Technological breakthroughs in catalysis and process intensification are enabling more cost-effective and efficient production. Strategic partnerships between raw material suppliers, polyol manufacturers, and end-users are fostering innovation and market penetration. Government initiatives and subsidies promoting the use of renewable resources and sustainable chemical production are providing a significant boost. Furthermore, companies are increasingly adopting market expansion strategies, both geographically and by diversifying into new application areas, thereby broadening the market's reach and demand.

Key Players Shaping the Sucrose Initiated Polyether Polyols Market

- BASF

- Oltchim

- Hongbaoli Group

- Carpenter

- Dow

- Kukdo Chemical

- Covestro

- Hebei Yadong Chemical Group

- GC POLYOLS

Notable Milestones in Sucrose Initiated Polyether Polyols Sector

- 2019: Introduction of advanced catalyst systems for enhanced sucrose polymerization efficiency.

- 2020: Increased focus on developing bio-based sucrose alternatives due to supply chain volatility.

- 2021: Launch of novel low-VOC sucrose initiated polyether polyols to meet stringent environmental regulations.

- 2022: Significant M&A activity as major players consolidate to expand market share and product offerings.

- 2023: Development of high-performance sucrose initiated polyols for demanding automotive applications.

- 2024: Growing research into circular economy models for polyol production and end-of-life solutions.

In-Depth Sucrose Initiated Polyether Polyols Market Outlook

The future market outlook for Sucrose Initiated Polyether Polyols is exceptionally promising, driven by the synergistic forces of sustainability mandates, technological advancements, and expanding application frontiers. Growth accelerators such as the development of highly specialized polyols for advanced materials, increased adoption in emerging economies, and potential breakthroughs in bio-refining processes will continue to shape the market. Strategic investments in R&D and capacity expansion by key players will be crucial for meeting the escalating global demand. The market is poised for sustained growth, offering significant strategic opportunities for companies aligned with the principles of sustainability and innovation.

Sucrose Initiated Polyether Polyols Segmentation

-

1. Application

- 1.1. Home Appliances

- 1.2. Sheet

- 1.3. Pipeline

- 1.4. Other

-

2. Types

- 2.1. Low Reactive

- 2.2. Medium Reactive

- 2.3. High Reactive

Sucrose Initiated Polyether Polyols Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Sucrose Initiated Polyether Polyols REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Sucrose Initiated Polyether Polyols Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Home Appliances

- 5.1.2. Sheet

- 5.1.3. Pipeline

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Low Reactive

- 5.2.2. Medium Reactive

- 5.2.3. High Reactive

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Sucrose Initiated Polyether Polyols Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Home Appliances

- 6.1.2. Sheet

- 6.1.3. Pipeline

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Low Reactive

- 6.2.2. Medium Reactive

- 6.2.3. High Reactive

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Sucrose Initiated Polyether Polyols Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Home Appliances

- 7.1.2. Sheet

- 7.1.3. Pipeline

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Low Reactive

- 7.2.2. Medium Reactive

- 7.2.3. High Reactive

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Sucrose Initiated Polyether Polyols Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Home Appliances

- 8.1.2. Sheet

- 8.1.3. Pipeline

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Low Reactive

- 8.2.2. Medium Reactive

- 8.2.3. High Reactive

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Sucrose Initiated Polyether Polyols Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Home Appliances

- 9.1.2. Sheet

- 9.1.3. Pipeline

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Low Reactive

- 9.2.2. Medium Reactive

- 9.2.3. High Reactive

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Sucrose Initiated Polyether Polyols Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Home Appliances

- 10.1.2. Sheet

- 10.1.3. Pipeline

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Low Reactive

- 10.2.2. Medium Reactive

- 10.2.3. High Reactive

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 BASF

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Oltchim

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Hongbaoli Group

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Carpenter

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Dow

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Kukdo Chemical

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Covestro

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Hebei Yadong Chemical Group

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 GC POLYOLS

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 BASF

List of Figures

- Figure 1: Global Sucrose Initiated Polyether Polyols Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Sucrose Initiated Polyether Polyols Revenue (million), by Application 2024 & 2032

- Figure 3: North America Sucrose Initiated Polyether Polyols Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Sucrose Initiated Polyether Polyols Revenue (million), by Types 2024 & 2032

- Figure 5: North America Sucrose Initiated Polyether Polyols Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Sucrose Initiated Polyether Polyols Revenue (million), by Country 2024 & 2032

- Figure 7: North America Sucrose Initiated Polyether Polyols Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Sucrose Initiated Polyether Polyols Revenue (million), by Application 2024 & 2032

- Figure 9: South America Sucrose Initiated Polyether Polyols Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Sucrose Initiated Polyether Polyols Revenue (million), by Types 2024 & 2032

- Figure 11: South America Sucrose Initiated Polyether Polyols Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Sucrose Initiated Polyether Polyols Revenue (million), by Country 2024 & 2032

- Figure 13: South America Sucrose Initiated Polyether Polyols Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Sucrose Initiated Polyether Polyols Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Sucrose Initiated Polyether Polyols Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Sucrose Initiated Polyether Polyols Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Sucrose Initiated Polyether Polyols Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Sucrose Initiated Polyether Polyols Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Sucrose Initiated Polyether Polyols Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Sucrose Initiated Polyether Polyols Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Sucrose Initiated Polyether Polyols Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Sucrose Initiated Polyether Polyols Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Sucrose Initiated Polyether Polyols Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Sucrose Initiated Polyether Polyols Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Sucrose Initiated Polyether Polyols Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Sucrose Initiated Polyether Polyols Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Sucrose Initiated Polyether Polyols Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Sucrose Initiated Polyether Polyols Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Sucrose Initiated Polyether Polyols Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Sucrose Initiated Polyether Polyols Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Sucrose Initiated Polyether Polyols Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Sucrose Initiated Polyether Polyols Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Sucrose Initiated Polyether Polyols Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Sucrose Initiated Polyether Polyols?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Sucrose Initiated Polyether Polyols?

Key companies in the market include BASF, Oltchim, Hongbaoli Group, Carpenter, Dow, Kukdo Chemical, Covestro, Hebei Yadong Chemical Group, GC POLYOLS.

3. What are the main segments of the Sucrose Initiated Polyether Polyols?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Sucrose Initiated Polyether Polyols," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Sucrose Initiated Polyether Polyols report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Sucrose Initiated Polyether Polyols?

To stay informed about further developments, trends, and reports in the Sucrose Initiated Polyether Polyols, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence