Key Insights

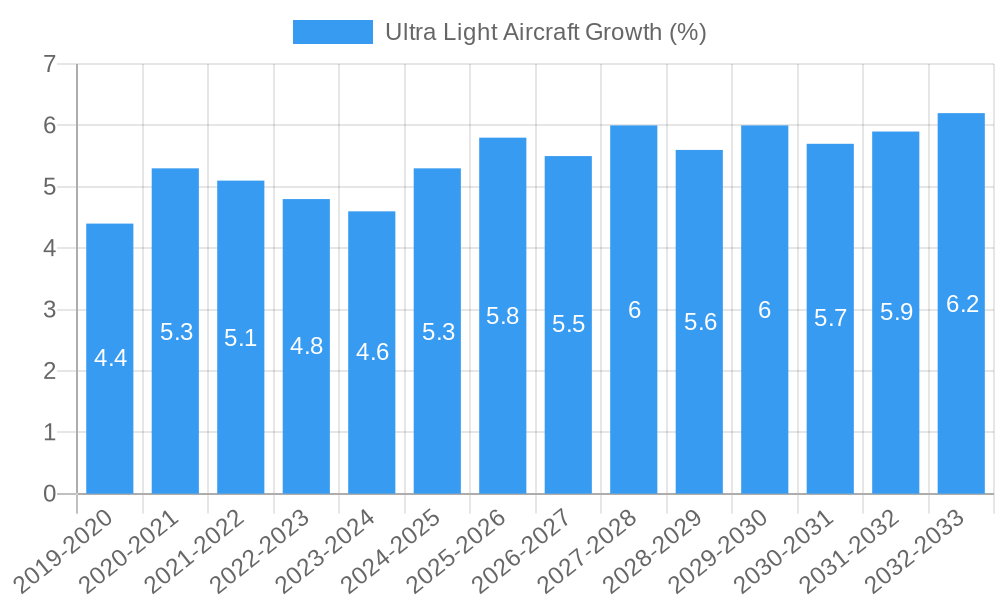

The global Ultra Light Aircraft market is experiencing robust growth, poised for significant expansion driven by increasing demand for recreational flying, pilot training, and niche aviation applications. With an estimated market size of approximately $550 million in 2025, the sector is projected to witness a Compound Annual Growth Rate (CAGR) of around 6.5% through 2033. This upward trajectory is primarily fueled by the growing accessibility of light sport aircraft (LSAs) and the persistent appeal of personal aviation for hobbyists and enthusiasts. Advancements in material science and engine technology are contributing to the development of lighter, more efficient, and cost-effective ultra-light aircraft, further broadening their market appeal. Additionally, the increasing need for cost-effective aerial surveillance, agricultural monitoring, and light cargo delivery in remote regions also presents a substantial growth opportunity. The market is characterized by a diverse range of players, from established manufacturers to nimble kit aircraft suppliers, catering to a spectrum of consumer needs and budget considerations.

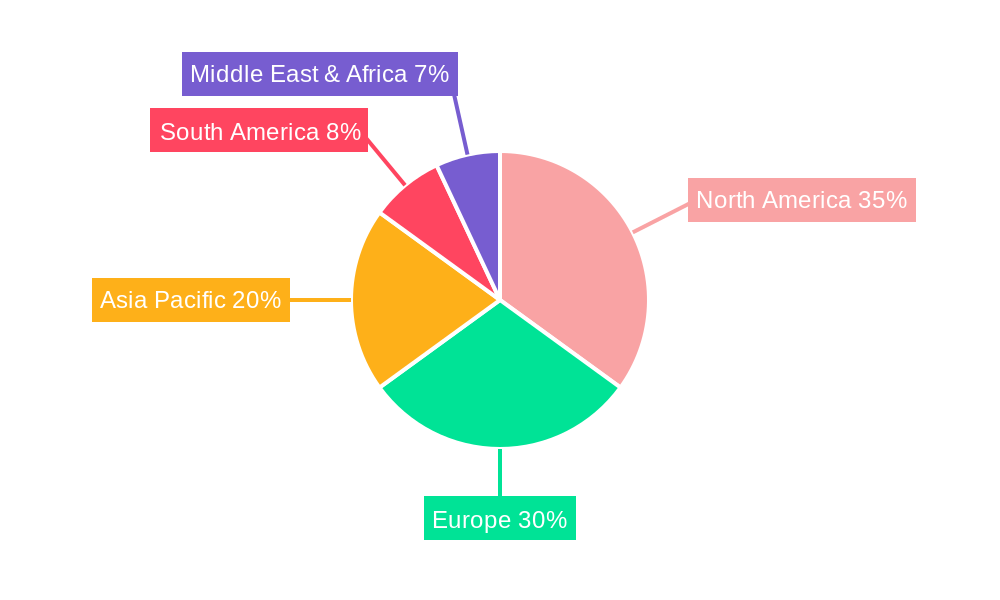

The market segmentation reveals a dynamic landscape with both commercial and personal applications contributing to its expansion. While personal recreational flying remains a cornerstone, the increasing adoption of ultra-light aircraft for specialized commercial operations, such as aerial photography, training schools, and localized delivery services, is a notable trend. Within the type segmentation, both rotary-wing and fixed-wing ultra-light aircraft hold significant market share, with fixed-wing models dominating due to their broader utility and established infrastructure. Geographically, North America and Europe currently lead the market, owing to well-established aviation cultures and supportive regulatory frameworks for light aircraft. However, the Asia Pacific region, particularly China and India, is anticipated to emerge as a high-growth market in the coming years, driven by rising disposable incomes and a burgeoning interest in aviation. Key restraints include stringent regulatory hurdles in certain regions and the inherent safety concerns associated with light aircraft, although continuous technological improvements are actively mitigating these challenges.

This comprehensive report, "Ultra Light Aircraft Market: Global Analysis & Forecast 2019-2033," offers an in-depth exploration of the dynamic ultra-light aircraft sector. Covering the historical period from 2019 to 2024 and projecting growth through 2033, with a base and estimated year of 2025, this study is an essential resource for industry professionals seeking to understand market trends, identify growth opportunities, and formulate strategic decisions. With a focus on both commercial ultra light aircraft and personal ultra light aircraft, and dissecting the market by rotary wing ultra light aircraft and fixed wing ultra light aircraft, this report provides unparalleled insights into a rapidly evolving industry.

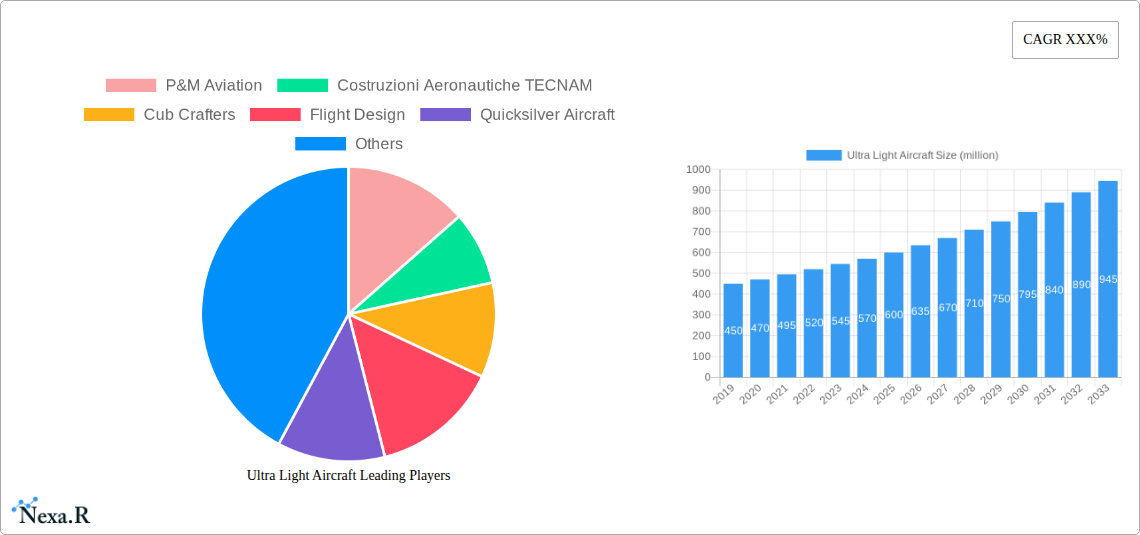

The market landscape is analyzed with a keen eye on key players like P&M Aviation, Costruzioni Aeronautiche TECNAM, Cub Crafters, Flight Design, Quicksilver Aircraft, Jabiru Aircraft, American Legend Aircraft, Aeropro, Gulfstream, Belite Enterprises, Learjet, Cessna, Pilatus Aircraft, Cirrus Aircraft, The Airplane Factory, CGS Aviation, Ekolot, Progressive Aerodyne, FANTASY AIR, Kitfox Aircraft, and Tecnam. We meticulously detail the ultra light aircraft market size and project its future trajectory, integrating high-traffic keywords such as light aircraft market, ultralight aircraft for sale, experimental aircraft market, and light sport aircraft market to maximize SEO visibility. Understand the impact of new ultra light aircraft technologies and the evolving ultra light aircraft regulations.

Ultra Light Aircraft Market Dynamics & Structure

The global ultra light aircraft market exhibits a moderate concentration, with a few key manufacturers holding significant market share while a robust ecosystem of smaller companies and kit manufacturers cater to niche demands. Technological innovation serves as a primary driver, fueled by advancements in lightweight materials, engine efficiency, and avionics, enabling enhanced performance and accessibility. Regulatory frameworks, particularly those for light sport aircraft (LSA) and experimental aircraft categories, play a crucial role in shaping market entry and product development. Competitive product substitutes, including advanced drones and advanced recreational vehicles, are emerging, although the unique appeal of manned flight continues to sustain demand. End-user demographics are diversifying, encompassing recreational pilots, flight training schools, and increasingly, commercial applications for aerial surveying and surveillance. Mergers and acquisitions (M&A) activity is moderate, primarily focused on consolidating niche technologies or expanding product portfolios. The market share of leading companies is approximately 35% among the top five players, with an estimated 50 M&A deals impacting the market within the historical period. Innovation barriers include high research and development costs and the complex certification processes in some regions.

Ultra Light Aircraft Growth Trends & Insights

The ultra light aircraft market is poised for significant expansion, driven by a confluence of factors that are redefining personal and commercial aviation. The projected market size in 2025 is valued at USD 3,100 million, with a robust Compound Annual Growth Rate (CAGR) of 7.2% anticipated from 2025 to 2033. This upward trajectory is underpinned by increasing adoption rates among recreational pilots seeking an accessible entry into aviation, as well as a growing interest in light sport aircraft sales for private ownership and pilot training. Technological disruptions, such as the integration of electric and hybrid propulsion systems, are not only enhancing sustainability but also reducing operational costs, thereby broadening the appeal of ultra light aircraft. Consumer behavior shifts are also playing a pivotal role; a growing desire for experiential travel and unique recreational activities is translating into increased demand for personal aviation solutions. Furthermore, the burgeoning experimental aircraft market is fostering a culture of innovation and customization, attracting a new generation of aviators. Market penetration is expected to increase by 15% over the forecast period, indicating a broader acceptance and integration of ultra light aircraft into various lifestyle and professional applications. The overall market value is projected to reach USD 5,200 million by 2033.

Dominant Regions, Countries, or Segments in Ultra Light Aircraft

The fixed wing ultra light aircraft segment is unequivocally dominating the global market, accounting for an estimated 85% of market share in 2025, driven by its versatility and established manufacturing base. Within this, the personal application segment commands the largest share, representing approximately 60% of the total market value, fueled by recreational flying and private ownership trends. North America, particularly the United States, stands as the leading region, contributing over 40% to the global market revenue. Key drivers behind this dominance include favorable economic policies that support aviation, a well-established aviation infrastructure including numerous airfields, and a strong culture of recreational flying. The presence of major manufacturers like Cub Crafters and American Legend Aircraft in the region further solidifies its position. The growth potential in this segment is substantial, supported by increasing disposable incomes and a persistent interest in private aviation. Furthermore, the demand for ultralight aircraft for sale in the personal segment continues to be robust, with an expected annual growth rate of 6.8% for fixed-wing aircraft in personal applications. While rotary wing ultra light aircraft are experiencing niche growth, particularly in specialized commercial applications, the sheer volume and widespread appeal of fixed-wing designs ensure their continued market leadership. The overall market value for fixed-wing ultra light aircraft in personal applications is projected to reach USD 3,120 million by 2033.

Ultra Light Aircraft Product Landscape

The ultra light aircraft product landscape is characterized by continuous innovation aimed at enhancing performance, safety, and accessibility. Manufacturers are increasingly focusing on the development of aircraft with improved fuel efficiency, quieter operations, and advanced avionics suites, making them more appealing to a broader customer base. Unique selling propositions often lie in the ease of operation, lower acquisition costs compared to traditional aircraft, and the ability to fly under specific ultralight or light sport aircraft regulations. Technological advancements include the adoption of composite materials for lighter airframes, more powerful and efficient engine options, and integrated digital flight displays. Applications range from recreational flying and pilot training to specialized commercial uses such as aerial photography, pipeline inspection, and agricultural surveillance. The performance metrics, such as speed, range, and payload capacity, are steadily improving, pushing the boundaries of what is possible within the ultralight category.

Key Drivers, Barriers & Challenges in Ultra Light Aircraft

Key Drivers:

- Technological Advancements: Innovations in lightweight materials, efficient engines, and advanced avionics are enhancing performance and reducing costs.

- Growing Recreational Aviation Demand: Increasing disposable incomes and a desire for unique leisure activities are fueling demand for personal ultra light aircraft.

- Lower Acquisition and Operating Costs: Compared to traditional aircraft, ultra light and light sport aircraft offer a more affordable entry into aviation.

- Favorable Regulatory Frameworks: Regulations for LSA and experimental aircraft categories often provide a less stringent path to market and operation.

Barriers & Challenges:

- Supply Chain Disruptions: Volatility in the availability of raw materials and components can impact production timelines and costs. For example, a 10% increase in raw material costs could lead to a 3% rise in aircraft prices.

- Stringent Certification and Regulatory Hurdles: While some regulations are favorable, others, particularly in new markets, can be complex and costly to navigate.

- Public Perception and Safety Concerns: Perceived safety risks associated with lighter aircraft can deter potential buyers and impact insurance rates.

- Limited Range and Payload Capacity: These inherent limitations can restrict the usability of ultra light aircraft for certain commercial or long-distance applications.

- Competition from Drones and Unmanned Aerial Vehicles (UAVs): These technologies are increasingly encroaching on some of the commercial applications previously explored by manned ultra light aircraft.

Emerging Opportunities in Ultra Light Aircraft

Emerging opportunities in the ultra light aircraft sector are diverse and promising. The development of electric and hybrid-powered ultra light aircraft presents a significant avenue for growth, catering to the increasing demand for sustainable aviation solutions and reducing operational noise pollution. Untapped markets in developing economies with growing middle classes and a nascent interest in aviation offer substantial expansion potential. Innovative applications for autonomous or semi-autonomous ultra light aircraft in cargo delivery and surveillance are also gaining traction. Furthermore, evolving consumer preferences towards personalized experiences are driving demand for highly customizable aircraft and specialized flight training programs. The kit aircraft market continues to be a fertile ground for innovation and hobbyist engagement.

Growth Accelerators in the Ultra Light Aircraft Industry

Several catalysts are accelerating long-term growth in the ultra light aircraft industry. Technological breakthroughs in battery technology are paving the way for practical and cost-effective electric propulsion systems, significantly expanding the operational envelope and environmental appeal of these aircraft. Strategic partnerships between established aerospace companies and innovative start-ups are fostering the rapid development and commercialization of new technologies. Furthermore, market expansion strategies, including targeted marketing campaigns to attract younger demographics and educational initiatives to demystify aviation, are crucial in broadening the customer base. The increasing integration of advanced simulation technologies for pilot training also reduces barriers to entry and enhances skill development, further stimulating demand.

Key Players Shaping the Ultra Light Aircraft Market

- P&M Aviation

- Costruzioni Aeronautiche TECNAM

- Cub Crafters

- Flight Design

- Quicksilver Aircraft

- Jabiru Aircraft

- American Legend Aircraft

- Aeropro

- Gulfstream

- Belite Enterprises

- Learjet

- Cessna

- Pilatus Aircraft

- Cirrus Aircraft

- The Airplane Factory

- CGS Aviation

- Ekolot

- Progressive Aerodyne

- FANTASY AIR

- Kitfox Aircraft

- Tecnam

Notable Milestones in Ultra Light Aircraft Sector

- 2019: Introduction of advanced composite materials in several new ultralight models, leading to improved performance and durability.

- 2020: Increased regulatory clarity for Light Sport Aircraft (LSA) in several key international markets, fostering new product development.

- 2021: Significant advancements in electric propulsion prototypes for ultralight aircraft, signaling a shift towards sustainable aviation.

- 2022: Rise in demand for homebuilt and kit aircraft, driven by an increased interest in hands-on aviation projects during the pandemic.

- 2023: Emergence of new manufacturers focusing on specialized applications like aerial surveillance and agricultural surveying using ultralight platforms.

- 2024: Expansion of flight simulation technology integration into ultralight pilot training, enhancing accessibility and safety.

In-Depth Ultra Light Aircraft Market Outlook

- 2019: Introduction of advanced composite materials in several new ultralight models, leading to improved performance and durability.

- 2020: Increased regulatory clarity for Light Sport Aircraft (LSA) in several key international markets, fostering new product development.

- 2021: Significant advancements in electric propulsion prototypes for ultralight aircraft, signaling a shift towards sustainable aviation.

- 2022: Rise in demand for homebuilt and kit aircraft, driven by an increased interest in hands-on aviation projects during the pandemic.

- 2023: Emergence of new manufacturers focusing on specialized applications like aerial surveillance and agricultural surveying using ultralight platforms.

- 2024: Expansion of flight simulation technology integration into ultralight pilot training, enhancing accessibility and safety.

In-Depth Ultra Light Aircraft Market Outlook

The future of the ultra light aircraft market is exceptionally bright, characterized by sustained growth driven by technological innovation, evolving consumer preferences, and strategic market expansion. The ongoing development of electric and hybrid propulsion systems will unlock new operational possibilities and environmental benefits, significantly broadening the appeal of these aircraft for both personal and commercial use. The increasing adoption of advanced avionics and safety features will further enhance their attractiveness and address any lingering safety concerns. The market is poised to witness a significant uptick in demand from emerging economies and a continued expansion within established markets, fueled by a growing interest in experiential activities and affordable personal aviation. Strategic partnerships and investments in research and development will be critical in capitalizing on these growth accelerators, ensuring a dynamic and prosperous future for the ultra light aircraft industry. The projected market value of USD 5,200 million by 2033 underscores the substantial opportunity ahead.

Ultra Light Aircraft Segmentation

-

1. Application

- 1.1. Commercial

- 1.2. Personal

-

2. Type

- 2.1. Rotary Wing

- 2.2. Fixed Wing

Ultra Light Aircraft Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ultra Light Aircraft REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XXX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ultra Light Aircraft Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial

- 5.1.2. Personal

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Rotary Wing

- 5.2.2. Fixed Wing

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Ultra Light Aircraft Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial

- 6.1.2. Personal

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Rotary Wing

- 6.2.2. Fixed Wing

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Ultra Light Aircraft Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial

- 7.1.2. Personal

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Rotary Wing

- 7.2.2. Fixed Wing

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ultra Light Aircraft Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial

- 8.1.2. Personal

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Rotary Wing

- 8.2.2. Fixed Wing

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Ultra Light Aircraft Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial

- 9.1.2. Personal

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Rotary Wing

- 9.2.2. Fixed Wing

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Ultra Light Aircraft Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial

- 10.1.2. Personal

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Rotary Wing

- 10.2.2. Fixed Wing

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 P&M Aviation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Costruzioni Aeronautiche TECNAM

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Cub Crafters

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Flight Design

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Quicksilver Aircraft

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Jabiru Aircraft

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 American Legend Aircraft

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Aeropro

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Gulfstream

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Belite Enterprises

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Learjet

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Cessna

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Pilatus Aircraft

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Cirrus Aircraft

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 The Airplane Factory

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 CGS Aviation

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Ekolot

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Progressive Aerodyne

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 FANTASY AIR

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Kitfox Aircraft

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Tecnam

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 P&M Aviation

List of Figures

- Figure 1: Global Ultra Light Aircraft Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Ultra Light Aircraft Revenue (million), by Application 2024 & 2032

- Figure 3: North America Ultra Light Aircraft Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Ultra Light Aircraft Revenue (million), by Type 2024 & 2032

- Figure 5: North America Ultra Light Aircraft Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Ultra Light Aircraft Revenue (million), by Country 2024 & 2032

- Figure 7: North America Ultra Light Aircraft Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Ultra Light Aircraft Revenue (million), by Application 2024 & 2032

- Figure 9: South America Ultra Light Aircraft Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Ultra Light Aircraft Revenue (million), by Type 2024 & 2032

- Figure 11: South America Ultra Light Aircraft Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Ultra Light Aircraft Revenue (million), by Country 2024 & 2032

- Figure 13: South America Ultra Light Aircraft Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Ultra Light Aircraft Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Ultra Light Aircraft Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Ultra Light Aircraft Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Ultra Light Aircraft Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Ultra Light Aircraft Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Ultra Light Aircraft Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Ultra Light Aircraft Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Ultra Light Aircraft Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Ultra Light Aircraft Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Ultra Light Aircraft Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Ultra Light Aircraft Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Ultra Light Aircraft Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Ultra Light Aircraft Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Ultra Light Aircraft Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Ultra Light Aircraft Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Ultra Light Aircraft Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Ultra Light Aircraft Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Ultra Light Aircraft Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Ultra Light Aircraft Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Ultra Light Aircraft Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Ultra Light Aircraft Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Ultra Light Aircraft Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Ultra Light Aircraft Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Ultra Light Aircraft Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Ultra Light Aircraft Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Ultra Light Aircraft Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Ultra Light Aircraft Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Ultra Light Aircraft Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Ultra Light Aircraft Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Ultra Light Aircraft Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Ultra Light Aircraft Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Ultra Light Aircraft Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Ultra Light Aircraft Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Ultra Light Aircraft Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Ultra Light Aircraft Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Ultra Light Aircraft Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Ultra Light Aircraft Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Ultra Light Aircraft Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ultra Light Aircraft?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Ultra Light Aircraft?

Key companies in the market include P&M Aviation, Costruzioni Aeronautiche TECNAM, Cub Crafters, Flight Design, Quicksilver Aircraft, Jabiru Aircraft, American Legend Aircraft, Aeropro, Gulfstream, Belite Enterprises, Learjet, Cessna, Pilatus Aircraft, Cirrus Aircraft, The Airplane Factory, CGS Aviation, Ekolot, Progressive Aerodyne, FANTASY AIR, Kitfox Aircraft, Tecnam.

3. What are the main segments of the Ultra Light Aircraft?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ultra Light Aircraft," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ultra Light Aircraft report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ultra Light Aircraft?

To stay informed about further developments, trends, and reports in the Ultra Light Aircraft, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence