Key Insights

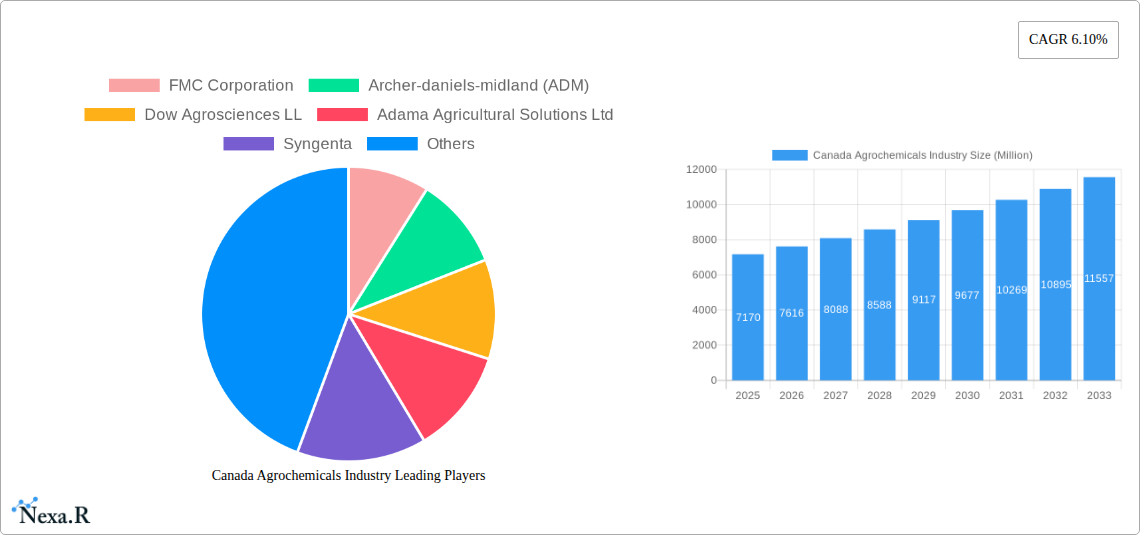

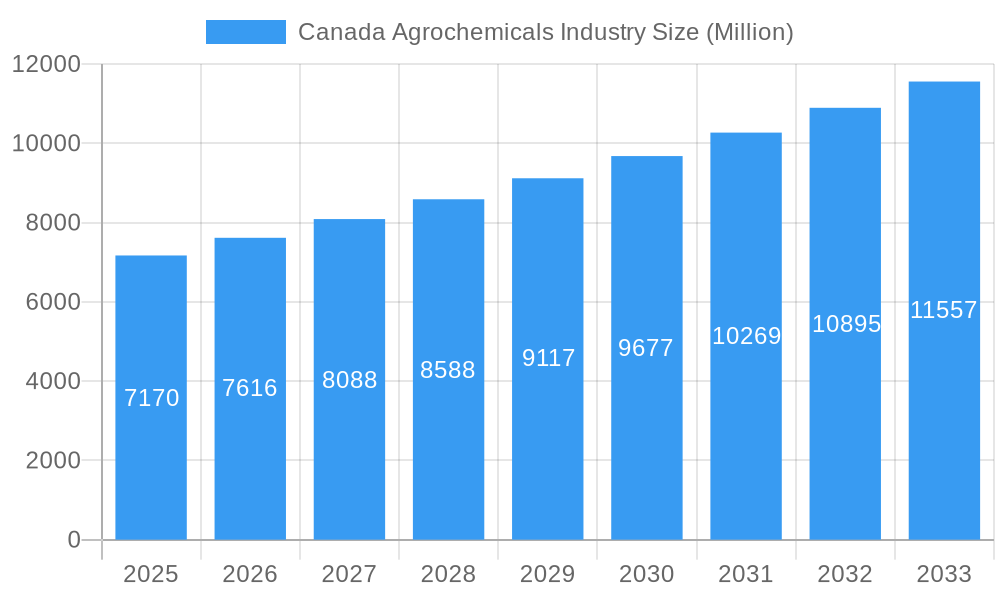

The Canadian agrochemicals market, valued at $7.17 billion in 2025, is projected to experience robust growth, driven by increasing agricultural production to meet rising food demands and a growing focus on improving crop yields through enhanced pest and disease management. The market's Compound Annual Growth Rate (CAGR) of 6.10% from 2019 to 2024 indicates a steady upward trajectory, expected to continue through 2033. Key drivers include government initiatives promoting sustainable agricultural practices, technological advancements in pesticide and fertilizer formulations (leading to increased efficacy and reduced environmental impact), and the growing adoption of precision agriculture techniques. Market segmentation reveals significant contributions from fertilizers, followed by pesticides, adjuvants, and plant growth regulators. Application-wise, grains and cereals, pulses and oilseeds, and fruits and vegetables constitute major segments, with the turf and ornamental grass sector showing potential for future growth. While challenges exist, such as stringent environmental regulations and potential supply chain disruptions, the overall market outlook remains positive, fueled by Canada's strong agricultural sector and the global demand for food security.

Canada Agrochemicals Industry Market Size (In Billion)

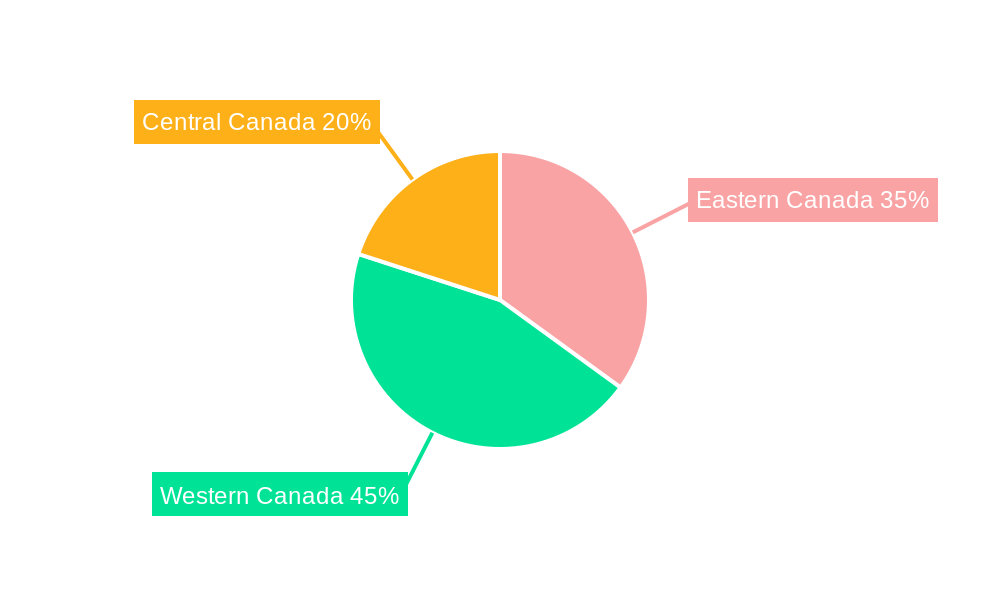

The competitive landscape is marked by the presence of both multinational giants like FMC Corporation, Syngenta, and BASF, and regional players. These companies are actively engaged in research and development to bring innovative and sustainable agrochemical solutions to the Canadian market. Regional variations within Canada, influenced by climatic conditions and agricultural practices, are observed across Eastern, Western, and Central Canada. The market's future growth will depend on factors such as climate change adaptation strategies, the development of resistant crop varieties, and the evolving consumer preferences toward sustainably produced food. Further research focusing on specific segments and regional dynamics will provide a more nuanced understanding of market opportunities and challenges. A thorough understanding of these factors is crucial for stakeholders to make informed strategic decisions for future growth and expansion in the Canadian agrochemical market.

Canada Agrochemicals Industry Company Market Share

Canada Agrochemicals Industry: Market Report 2019-2033

This comprehensive report provides a detailed analysis of the Canada agrochemicals market, covering the period 2019-2033. It delves into market dynamics, growth trends, key players, and future opportunities within the Canadian agricultural landscape. This in-depth study is crucial for businesses, investors, and policymakers seeking to understand and navigate this dynamic sector. The report utilizes a robust methodology incorporating both qualitative and quantitative data, delivering actionable insights for strategic decision-making.

Canada Agrochemicals Industry Market Dynamics & Structure

The Canadian agrochemicals market, valued at xx Million in 2024, is characterized by moderate concentration, with a few multinational corporations holding significant market share. Technological innovation, particularly in precision agriculture and sustainable solutions, is a major driver, alongside stringent regulatory frameworks focused on environmental protection and human health. The market witnesses continuous evolution through mergers and acquisitions (M&A) activities. Competitive pressures arise from both established players and the emergence of bio-based alternatives.

- Market Concentration: The top five players account for approximately xx% of the market share in 2024.

- Technological Innovation: Focus on developing targeted, low-impact formulations and digital agriculture technologies is increasing.

- Regulatory Landscape: Strict regulations surrounding pesticide registration and usage are shaping product development and market access.

- Competitive Landscape: The market is characterized by intense competition among established players and the emergence of new entrants offering sustainable alternatives.

- M&A Activity: The number of M&A deals in the Canadian agrochemicals market averaged xx per year during 2019-2024.

- End-User Demographics: The market is driven primarily by large-scale commercial farms, with a growing segment of smaller, specialized operations adopting sustainable practices.

Canada Agrochemicals Industry Growth Trends & Insights

The Canadian agrochemicals market exhibits a steady growth trajectory, driven by factors such as increasing crop production, government support for agricultural modernization, and rising demand for higher crop yields. The market experienced a CAGR of xx% during 2019-2024 and is projected to grow at a CAGR of xx% from 2025 to 2033, reaching xx Million by 2033. This growth is being propelled by technological advancements, including the adoption of precision agriculture techniques, and changing consumer preferences toward sustainably produced food. Market penetration of newer technologies is steadily increasing, particularly in areas with higher adoption rates of technology amongst farmers.

Dominant Regions, Countries, or Segments in Canada Agrochemicals Industry

The Prairie Provinces (Alberta, Saskatchewan, Manitoba) represent the dominant region for agrochemicals due to their extensive arable land and significant grain and oilseed production. Within the product segments, pesticides and fertilizers constitute the largest portions of the market, driven by high demand from the Grains and Cereals, and Pulses and Oilseeds application segments.

- Key Drivers: Favorable climatic conditions, government agricultural subsidies, and the concentration of large-scale farming operations in the Prairie Provinces significantly drive growth within this region.

- Market Share: The Prairie Provinces hold approximately xx% of the total Canadian agrochemicals market share.

- Growth Potential: Continued investment in agricultural infrastructure and technological advancements in this region point to significant future growth.

Canada Agrochemicals Industry Product Landscape

The Canadian agrochemicals market offers a diverse range of products, including fertilizers (nitrogen, phosphorus, potassium), pesticides (herbicides, insecticides, fungicides), adjuvants, and plant growth regulators. Innovation focuses on developing targeted formulations with improved efficacy, reduced environmental impact, and enhanced safety for human health. New product introductions are frequently accompanied by detailed application instructions and support for optimal results. Key features include water solubility, ease of application, and cost-effectiveness.

Key Drivers, Barriers & Challenges in Canada Agrochemicals Industry

Key Drivers:

- Growing demand for food and feed crops.

- Increasing adoption of precision agriculture technologies.

- Government initiatives promoting sustainable agriculture practices.

Challenges:

- Stringent environmental regulations.

- Price volatility of raw materials.

- Potential resistance development in pests and diseases. Supply chain disruptions due to logistical challenges and geopolitical factors impacted the market by approximately xx% in 2022, leading to price increases.

Emerging Opportunities in Canada Agrochemicals Industry

- Growing demand for biopesticides and biofertilizers.

- Increasing focus on precision agriculture and data-driven solutions.

- Opportunities in niche markets, such as organic farming and specialty crops.

Growth Accelerators in the Canada Agrochemicals Industry

Technological advancements, strategic partnerships between agrochemical companies and agricultural technology providers, and expansion into new markets such as organic farming are key catalysts for long-term growth in the Canadian agrochemicals industry. Government support for research and development, coupled with increased farmer adoption of sustainable agricultural practices, will further accelerate market expansion.

Key Players Shaping the Canada Agrochemicals Industry Market

Notable Milestones in Canada Agrochemicals Industry Sector

- September 2022: Gowan Canada and ISK BioSciences launched 'Insight 339SC', a new group 14 herbicide.

- July 2022: Pivot Bio expanded into Canada, focusing on sustainable nitrogen solutions.

- May 2022: Protein Industries Canada announced a USD 19 million project for new micronutrient fertilizer commercialization.

In-Depth Canada Agrochemicals Industry Market Outlook

The Canadian agrochemicals market is poised for sustained growth, driven by technological innovation, increasing demand for sustainable agricultural practices, and government support for the agricultural sector. Strategic partnerships, focused product development, and market expansion strategies will be crucial for success in this dynamic market. The long-term outlook is positive, with considerable potential for expansion in various segments and regions.

Canada Agrochemicals Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Canada Agrochemicals Industry Segmentation By Geography

- 1. Canada

Canada Agrochemicals Industry Regional Market Share

Geographic Coverage of Canada Agrochemicals Industry

Canada Agrochemicals Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.10% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Decreasing Per Capita Arable Land; Increased Demand for Food

- 3.3. Market Restrains

- 3.3.1. High Initial Investments; Requirement of Precision Agriculture

- 3.4. Market Trends

- 3.4.1. Need for Improving Productivity by Limiting the Crop Damage

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Agrochemicals Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 FMC Corporation

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Archer-daniels-midland (ADM)

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Dow Agrosciences LL

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Adama Agricultural Solutions Ltd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Syngenta

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 UPL Limited

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Corteva Agriscience

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Bayer CropScience AG

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Nufarm Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 BASF SE

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 FMC Corporation

List of Figures

- Figure 1: Canada Agrochemicals Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Canada Agrochemicals Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: Canada Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Canada Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Canada Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Canada Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Canada Agrochemicals Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Canada Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: Canada Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Canada Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Canada Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Canada Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Canada Agrochemicals Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Agrochemicals Industry?

The projected CAGR is approximately 6.10%.

2. Which companies are prominent players in the Canada Agrochemicals Industry?

Key companies in the market include FMC Corporation, Archer-daniels-midland (ADM), Dow Agrosciences LL, Adama Agricultural Solutions Ltd, Syngenta, UPL Limited, Corteva Agriscience, Bayer CropScience AG, Nufarm Ltd, BASF SE.

3. What are the main segments of the Canada Agrochemicals Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.17 Million as of 2022.

5. What are some drivers contributing to market growth?

Decreasing Per Capita Arable Land; Increased Demand for Food.

6. What are the notable trends driving market growth?

Need for Improving Productivity by Limiting the Crop Damage.

7. Are there any restraints impacting market growth?

High Initial Investments; Requirement of Precision Agriculture.

8. Can you provide examples of recent developments in the market?

September 2022: Gowan Canada and ISK BioSciences launched 'Insight 339SC', a new group 14 herbicide for pre-seed burnoff applications in wheat, corn, and soybean. Insight 339SC provides rapid and effective pre-seed burndown of important broadleaf weeds like kochia, redroot pigweed, common lamb's quarters, and wild buckwheat.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Agrochemicals Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Agrochemicals Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Agrochemicals Industry?

To stay informed about further developments, trends, and reports in the Canada Agrochemicals Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence