Key Insights

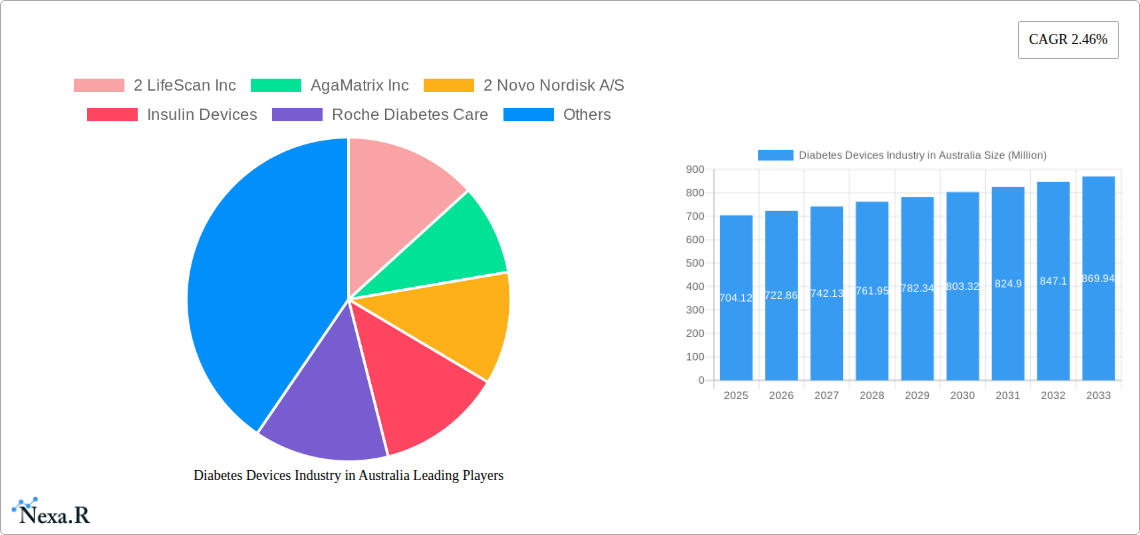

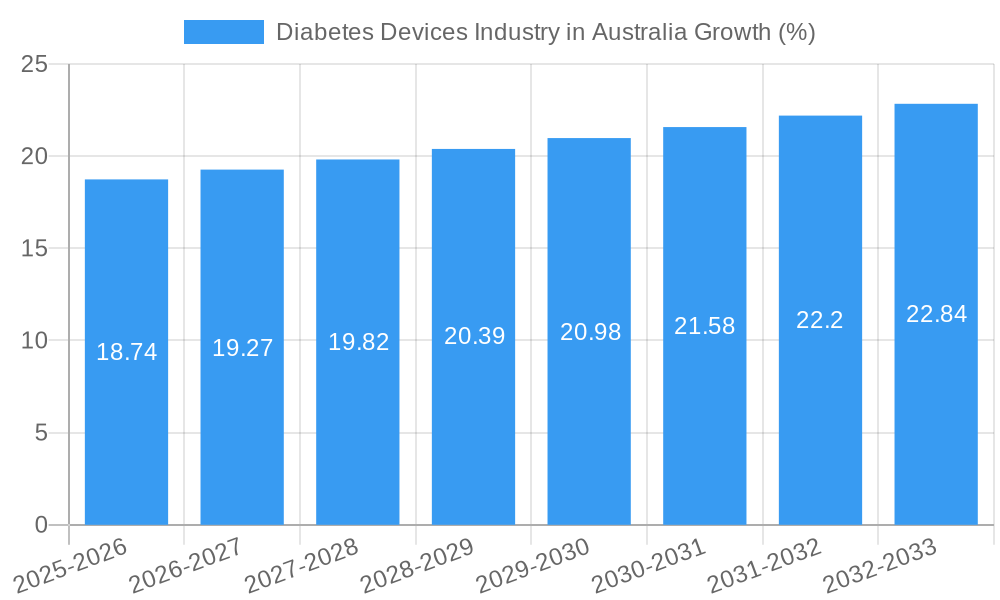

The Australian diabetes devices market, valued at $704.12 million in 2025, is projected to experience steady growth, driven by increasing prevalence of diabetes, advancements in continuous glucose monitoring (CGM) technology, and rising demand for insulin delivery systems. The market's Compound Annual Growth Rate (CAGR) of 2.46% from 2025 to 2033 indicates a consistent expansion, albeit at a moderate pace. Key growth drivers include an aging population, increasing urbanization leading to sedentary lifestyles and higher rates of obesity, and improved access to healthcare. The segment of continuous glucose monitoring (CGM) devices is anticipated to be a major growth area, fueled by the accuracy and convenience offered by these systems, reducing the burden of frequent finger-prick testing. While the market is characterized by strong competition from established players like Medtronic, Abbott Diabetes Care, and Dexcom, new entrants are expected to introduce innovative devices, fostering further growth and market diversification. However, high costs associated with advanced devices like CGMs, coupled with the need for consistent insulin supply and related management practices, may pose a restraint. The market is segmented into management devices (insulin pumps, syringes, pens, jet injectors) and monitoring devices (self-monitoring blood glucose, lancets, CGM). The continued expansion of telehealth and remote patient monitoring services should also contribute to market expansion by facilitating improved management and monitoring of diabetes.

The dominance of major players like Medtronic and Abbott in the Australian diabetes devices market suggests a consolidated landscape. However, smaller companies specializing in niche areas like innovative insulin delivery systems are likely to play a pivotal role in market innovation and diversification. Future growth hinges on several factors, including government initiatives to improve diabetes care access, successful integration of advanced technologies into mainstream care, and the affordability of diabetes management solutions. Further research into long-term complications of diabetes and advancements in preventing or slowing disease progression will also directly affect the market's trajectory. Successful development and market penetration of closed-loop insulin delivery systems represent a significant potential for future market expansion.

Diabetes Devices Industry in Australia: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Australian diabetes devices market, covering market dynamics, growth trends, regional segmentation, product landscape, key players, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. This report is essential for industry professionals, investors, and stakeholders seeking to understand this dynamic market.

Keywords: Australian Diabetes Devices Market, Diabetes Management Devices Australia, Continuous Glucose Monitoring (CGM) Australia, Insulin Pumps Australia, Self-Monitoring Blood Glucose (SMBG) Australia, Diabetes Care Australia, Diabetes Technology Australia, Insulin Delivery Devices Australia, Diabetes Market Size Australia, Diabetes Devices Market Growth Australia

Diabetes Devices Industry in Australia Market Dynamics & Structure

The Australian diabetes devices market is characterized by a moderate level of concentration, with several multinational corporations holding significant market share. Technological innovation, particularly in continuous glucose monitoring (CGM) and insulin delivery systems, is a key driver. Regulatory frameworks, such as the recent expansion of CGM prescription access, significantly impact market access and growth. The market faces competition from alternative therapies and management strategies. End-user demographics, driven by the increasing prevalence of diabetes, fuel market expansion. M&A activity, while not exceptionally high in recent years, reflects strategic positioning and consolidation amongst key players.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2025.

- Technological Innovation: Continuous glucose monitoring (CGM) and advanced insulin delivery systems are major drivers.

- Regulatory Framework: Recent changes expanding CGM prescription access are boosting market growth.

- Competitive Substitutes: Lifestyle changes, dietary management, and alternative therapies pose some competitive pressure.

- End-User Demographics: Increasing prevalence of diabetes, particularly type 2, fuels market growth.

- M&A Activity: xx major M&A deals recorded between 2019 and 2024, indicating strategic consolidation.

Diabetes Devices Industry in Australia Growth Trends & Insights

The Australian diabetes devices market experienced robust growth during the historical period (2019-2024), with a Compound Annual Growth Rate (CAGR) of xx%. This growth is projected to continue throughout the forecast period (2025-2033), driven by factors including rising diabetes prevalence, technological advancements in device accuracy and user-friendliness, increasing awareness of disease management, and supportive government initiatives. Market penetration of CGM devices is expected to increase significantly, from xx% in 2025 to xx% by 2033, reflecting the government's recent policy changes expanding access. Consumer behavior shifts toward technologically advanced, user-friendly devices are further propelling market expansion. The adoption of connected health platforms further improves patient compliance and treatment efficacy. Market size is expected to reach xx Million units by 2033.

Dominant Regions, Countries, or Segments in Diabetes Devices Industry in Australia

The Australian diabetes devices market demonstrates relatively even distribution across regions, reflecting the national prevalence of diabetes. However, urban centers with higher population densities and better access to healthcare infrastructure generally show higher adoption rates. Within the product segments, continuous glucose monitoring (CGM) devices are experiencing the fastest growth, driven by improved accuracy, ease of use, and expanded access. The self-monitoring blood glucose (SMBG) segment remains substantial, offering a more affordable alternative, especially for individuals with less severe conditions.

- Key Growth Drivers:

- Increasing prevalence of diabetes across all regions.

- Improved access to healthcare and specialist diabetes care.

- Government initiatives promoting early diagnosis and improved diabetes management.

- Rising healthcare expenditure.

- Dominant Segments:

- Continuous Glucose Monitoring (CGM): Fastest-growing segment due to improved technology and access.

- Self-Monitoring Blood Glucose (SMBG): Significant market share due to affordability and widespread use.

Diabetes Devices Industry in Australia Product Landscape

The Australian diabetes devices market offers a diverse range of products, including insulin pumps (with integrated CGM capabilities), various insulin delivery systems (pens, syringes, cartridges), and both traditional and advanced continuous glucose monitoring (CGM) devices. Product innovation focuses on improving accuracy, ease of use, integration with smartphone apps, and data connectivity for remote monitoring and better clinical decision-making. Many devices now include features like personalized insulin dosing recommendations, alerts for high or low glucose levels, and data-driven insights for both patients and clinicians.

Key Drivers, Barriers & Challenges in Diabetes Devices Industry in Australia

Key Drivers:

- Increasing prevalence of diabetes.

- Technological advancements leading to improved accuracy and user-friendliness.

- Government initiatives promoting early detection and improved diabetes management.

- Growing acceptance and adoption of digital health technologies.

Key Barriers & Challenges:

- High cost of advanced devices, limiting accessibility for some patients.

- Regulatory complexities and reimbursement processes for new technologies.

- Competition from alternative therapies and lifestyle modifications.

- Potential supply chain disruptions affecting device availability. A projected xx% decrease in supply chain efficiency in 2026 could impact market growth negatively by xx%.

Emerging Opportunities in Diabetes Devices Industry in Australia

- Expansion of telehealth and remote patient monitoring using connected devices.

- Growth in artificial intelligence (AI)-powered diabetes management solutions.

- Development of personalized medicine approaches tailored to individual patient needs.

- Focus on improving patient education and adherence through innovative digital tools.

Growth Accelerators in the Diabetes Devices Industry in Australia Industry

Technological breakthroughs in areas such as miniaturization, improved sensor accuracy, and seamless data integration are key drivers of long-term growth. Strategic partnerships between device manufacturers, pharmaceutical companies, and healthcare providers are vital in ensuring widespread adoption and effective integration into clinical workflows. Market expansion strategies targeting underserved populations and improved accessibility will also play a crucial role.

Key Players Shaping the Diabetes Devices Industry in Australia Market

- LifeScan Inc

- AgaMatrix Inc

- Novo Nordisk A/S

- Insulin Devices

- Roche Diabetes Care

- Eli Lilly

- Abbott Diabetes Care

- Medtronic

- Dexcom Inc

- Sanofi Aventis

- Insulet Corporation

- ARKRAY Inc

- Ypsomed Holding AG

- Ascensia Diabetes Care

Notable Milestones in Diabetes Devices Industry in Australia Sector

- November 2023: The Australian government expanded access to CGM prescriptions, allowing GPs, diabetes educators, and other healthcare professionals to prescribe these devices. This is expected to significantly boost CGM adoption.

- November 2022: Eli Lilly launched the Tempo Personalized Diabetes Management Platform, offering a connected solution for managing type 1 and 2 diabetes with integrated insulin delivery and data analysis. This innovative platform is expected to improve treatment outcomes and patient adherence.

In-Depth Diabetes Devices Industry in Australia Market Outlook

The Australian diabetes devices market presents significant growth potential driven by continued technological innovation, increasing diabetes prevalence, and supportive government policies. Strategic opportunities lie in developing and commercializing advanced CGM devices, integrating AI-driven analytics for personalized treatment, and expanding access to these technologies in underserved areas. The market is poised for continued expansion throughout the forecast period, driven by a combination of these factors and further advancements in diabetes management technologies.

Diabetes Devices Industry in Australia Segmentation

-

1. Management Devices

- 1.1. Insulin Pump

- 1.2. Insulin Syringes

- 1.3. cartridges in reusable pens

- 1.4. disposable pens

- 1.5. jet injectors

-

2. Monitoring Devices

- 2.1. Self-monitoring Blood Glucose

- 2.2. Continuous Glucose Monitoring

- 2.3. lancets

Diabetes Devices Industry in Australia Segmentation By Geography

- 1. Australia

Diabetes Devices Industry in Australia REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.46% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies

- 3.3. Market Restrains

- 3.3.1 ; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures

- 3.3.2 Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products

- 3.4. Market Trends

- 3.4.1. Increasing Diabetes Prevalence

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Diabetes Devices Industry in Australia Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Management Devices

- 5.1.1. Insulin Pump

- 5.1.2. Insulin Syringes

- 5.1.3. cartridges in reusable pens

- 5.1.4. disposable pens

- 5.1.5. jet injectors

- 5.2. Market Analysis, Insights and Forecast - by Monitoring Devices

- 5.2.1. Self-monitoring Blood Glucose

- 5.2.2. Continuous Glucose Monitoring

- 5.2.3. lancets

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Management Devices

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 2 LifeScan Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 AgaMatrix Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 2 Novo Nordisk A/S

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Insulin Devices

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Roche Diabetes Care

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Eli Lilly

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 LifeScan Inc

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Abbott Diabetes Care

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Medtronic

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 1 Dexcom Inc

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Dexcom Inc

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Continuous Glucose Monitoring Devices

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 1 Abbott Diabetes Care

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Sanofi Aventis

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 2 Medtronic PLC

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.16 Insulet Corporation

- 6.2.16.1. Overview

- 6.2.16.2. Products

- 6.2.16.3. SWOT Analysis

- 6.2.16.4. Recent Developments

- 6.2.16.5. Financials (Based on Availability)

- 6.2.17 ARKRAY Inc

- 6.2.17.1. Overview

- 6.2.17.2. Products

- 6.2.17.3. SWOT Analysis

- 6.2.17.4. Recent Developments

- 6.2.17.5. Financials (Based on Availability)

- 6.2.18 1 Insulet Corporation

- 6.2.18.1. Overview

- 6.2.18.2. Products

- 6.2.18.3. SWOT Analysis

- 6.2.18.4. Recent Developments

- 6.2.18.5. Financials (Based on Availability)

- 6.2.19 Self-monitoring Blood Glucose Devices

- 6.2.19.1. Overview

- 6.2.19.2. Products

- 6.2.19.3. SWOT Analysis

- 6.2.19.4. Recent Developments

- 6.2.19.5. Financials (Based on Availability)

- 6.2.20 Novo Nordisk A/S

- 6.2.20.1. Overview

- 6.2.20.2. Products

- 6.2.20.3. SWOT Analysis

- 6.2.20.4. Recent Developments

- 6.2.20.5. Financials (Based on Availability)

- 6.2.21 Ypsomed Holding AG

- 6.2.21.1. Overview

- 6.2.21.2. Products

- 6.2.21.3. SWOT Analysis

- 6.2.21.4. Recent Developments

- 6.2.21.5. Financials (Based on Availability)

- 6.2.22 Ascensia Diabetes Care

- 6.2.22.1. Overview

- 6.2.22.2. Products

- 6.2.22.3. SWOT Analysis

- 6.2.22.4. Recent Developments

- 6.2.22.5. Financials (Based on Availability)

- 6.2.1 2 LifeScan Inc

List of Figures

- Figure 1: Diabetes Devices Industry in Australia Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Diabetes Devices Industry in Australia Share (%) by Company 2024

List of Tables

- Table 1: Diabetes Devices Industry in Australia Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Diabetes Devices Industry in Australia Revenue Million Forecast, by Management Devices 2019 & 2032

- Table 4: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Management Devices 2019 & 2032

- Table 5: Diabetes Devices Industry in Australia Revenue Million Forecast, by Monitoring Devices 2019 & 2032

- Table 6: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Monitoring Devices 2019 & 2032

- Table 7: Diabetes Devices Industry in Australia Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Region 2019 & 2032

- Table 9: Diabetes Devices Industry in Australia Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Country 2019 & 2032

- Table 11: Diabetes Devices Industry in Australia Revenue Million Forecast, by Management Devices 2019 & 2032

- Table 12: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Management Devices 2019 & 2032

- Table 13: Diabetes Devices Industry in Australia Revenue Million Forecast, by Monitoring Devices 2019 & 2032

- Table 14: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Monitoring Devices 2019 & 2032

- Table 15: Diabetes Devices Industry in Australia Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diabetes Devices Industry in Australia?

The projected CAGR is approximately 2.46%.

2. Which companies are prominent players in the Diabetes Devices Industry in Australia?

Key companies in the market include 2 LifeScan Inc, AgaMatrix Inc, 2 Novo Nordisk A/S, Insulin Devices, Roche Diabetes Care, Eli Lilly, LifeScan Inc, Abbott Diabetes Care, Medtronic, 1 Dexcom Inc, Dexcom Inc, Continuous Glucose Monitoring Devices, 1 Abbott Diabetes Care, Sanofi Aventis, 2 Medtronic PLC, Insulet Corporation, ARKRAY Inc, 1 Insulet Corporation, Self-monitoring Blood Glucose Devices, Novo Nordisk A/S, Ypsomed Holding AG, Ascensia Diabetes Care.

3. What are the main segments of the Diabetes Devices Industry in Australia?

The market segments include Management Devices, Monitoring Devices.

4. Can you provide details about the market size?

The market size is estimated to be USD 704.12 Million as of 2022.

5. What are some drivers contributing to market growth?

; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies.

6. What are the notable trends driving market growth?

Increasing Diabetes Prevalence.

7. Are there any restraints impacting market growth?

; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures. Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products.

8. Can you provide examples of recent developments in the market?

November 2023: The Australian government has granted approval for individuals to obtain prescriptions for continuous glucose monitoring (CGM) devices from various healthcare professionals, including General Practitioners (GPs), diabetes educators, diabetes clinics, Registered Nurses (RNs), and specialists.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Diabetes Devices Industry in Australia," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Diabetes Devices Industry in Australia report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Diabetes Devices Industry in Australia?

To stay informed about further developments, trends, and reports in the Diabetes Devices Industry in Australia, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence