Key Insights

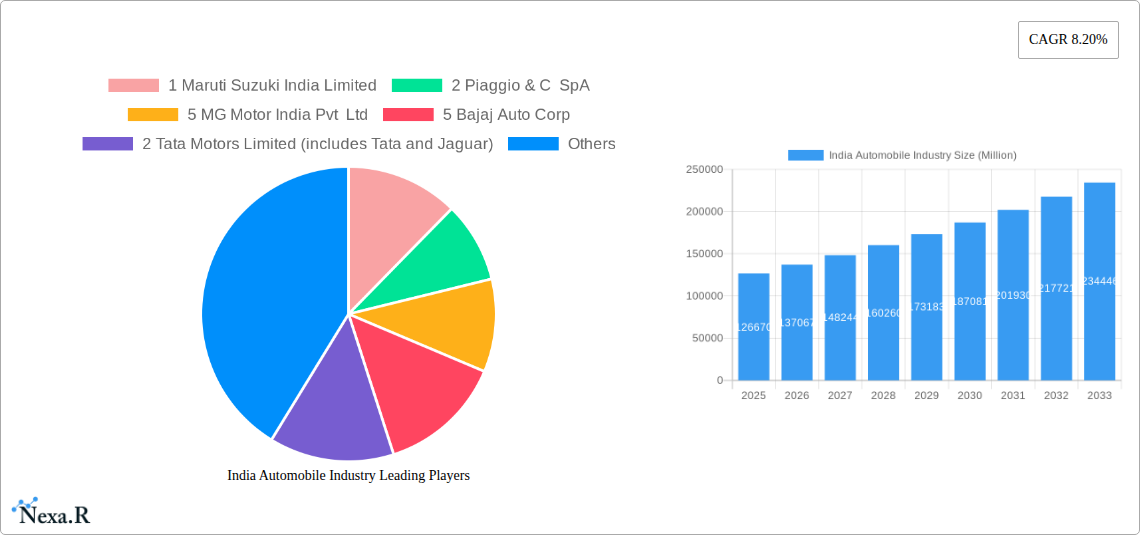

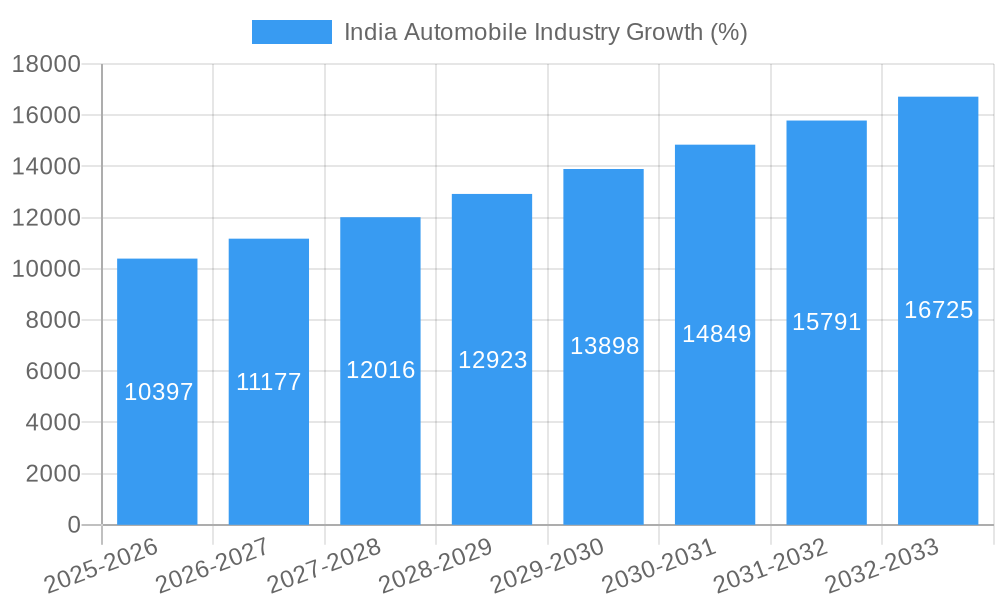

The Indian automobile industry, valued at $126.67 billion in 2025, is projected to experience robust growth, with a compound annual growth rate (CAGR) of 8.20% from 2025 to 2033. This expansion is driven by several factors, including rising disposable incomes, increasing urbanization, and a burgeoning middle class with a growing preference for personal vehicles. Government initiatives promoting electric vehicles (EVs) and infrastructure development further contribute to this positive outlook. However, challenges remain, including the volatility of fuel prices, stringent emission norms, and supply chain disruptions. The market is segmented by vehicle type (two-wheelers, passenger cars, commercial vehicles, three-wheelers), fuel type (diesel, petrol/gasoline, CNG and LPG, electric, others), and region (North, South, East, and West India). The dominance of two-wheelers is expected to continue, though passenger cars and commercial vehicles will see significant growth, fueled by increasing demand for SUVs and improved road infrastructure. The shift towards electric vehicles will be a defining trend, although the penetration rate will depend on factors like charging infrastructure availability and battery technology advancements. Competition is fierce, with major players like Maruti Suzuki, Tata Motors, Bajaj Auto, and Hero MotoCorp vying for market share alongside international brands like Hyundai, Honda, and Volkswagen. The industry will need to strategically manage these factors to sustain its growth trajectory.

The competitive landscape is characterized by both established domestic players and international automotive giants. Maruti Suzuki, a dominant player in the passenger car segment, faces competition from Tata Motors, Hyundai, and others. In the two-wheeler segment, Bajaj Auto and Hero MotoCorp hold substantial market share, but face challenges from emerging electric two-wheeler companies. The commercial vehicle segment is characterized by companies like Tata Motors and Mahindra & Mahindra, who are adapting to changing fuel preferences and technological advancements. The growth of the EV segment will significantly impact the competitive dynamics, attracting new entrants and triggering strategic alliances and acquisitions. The success of individual players will depend on their ability to innovate, adapt to changing consumer preferences, and manage supply chain complexities. Growth in specific regions, such as South India's expanding urban centers, will present significant opportunities for companies to target their marketing and distribution strategies accordingly.

India Automobile Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Indian automobile industry, encompassing market dynamics, growth trends, key players, and future outlook. With a focus on the period 2019-2033, including a base year of 2025 and a forecast period of 2025-2033, this report is essential for industry professionals, investors, and policymakers seeking to understand and capitalize on opportunities within this rapidly evolving sector. The report segments the market by vehicle type (two-wheelers, passenger cars, commercial vehicles, three-wheelers), fuel type (diesel, petrol/gasoline, CNG & LPG, electric, others), and region (North, South, East, West India).

India Automobile Industry Market Dynamics & Structure

The Indian automobile market, valued at xx million units in 2024, exhibits a complex interplay of factors shaping its structure and growth. Market concentration is moderate, with a few major players dominating specific segments (e.g., Maruti Suzuki in passenger cars, Hero MotoCorp in two-wheelers). Technological innovation, driven by government mandates for fuel efficiency and emission reduction, is a key driver, alongside evolving consumer preferences towards safety features and advanced technologies. The regulatory framework, including emission standards and safety regulations, significantly influences industry practices. Competitive product substitutes, such as public transportation and ride-sharing services, exert pressure on certain market segments. The end-user demographics, characterized by a growing middle class and increasing urbanization, fuel demand for personal vehicles. M&A activity has been moderate in recent years, with xx deals recorded in 2024, primarily focused on strategic partnerships and technology acquisitions.

- Market Concentration: Moderate, with significant players dominating specific segments.

- Technological Innovation: Driven by emission standards and consumer demand for advanced features.

- Regulatory Framework: Influential in shaping industry practices and product development.

- Competitive Substitutes: Public transport and ride-sharing present challenges to certain segments.

- End-User Demographics: Growing middle class and urbanization boost vehicle demand.

- M&A Trends: Moderate activity, focusing on strategic partnerships and technology acquisitions.

India Automobile Industry Growth Trends & Insights

The Indian automobile industry has experienced significant growth over the historical period (2019-2024), driven by factors such as increasing disposable incomes, infrastructure development, and government initiatives to promote vehicle ownership. The market size witnessed a compound annual growth rate (CAGR) of xx% during this period. Technological disruptions, particularly the rise of electric vehicles (EVs), are reshaping the industry landscape, though adoption rates remain relatively low compared to petrol and diesel vehicles. Consumer behavior is evolving, with increased preference for safety, fuel efficiency, and connected car features. The forecast period (2025-2033) anticipates continued growth, albeit at a potentially slower pace compared to the historical period, due to factors such as economic fluctuations and increasing competition. Market penetration of EVs is projected to increase significantly, reaching xx% by 2033.

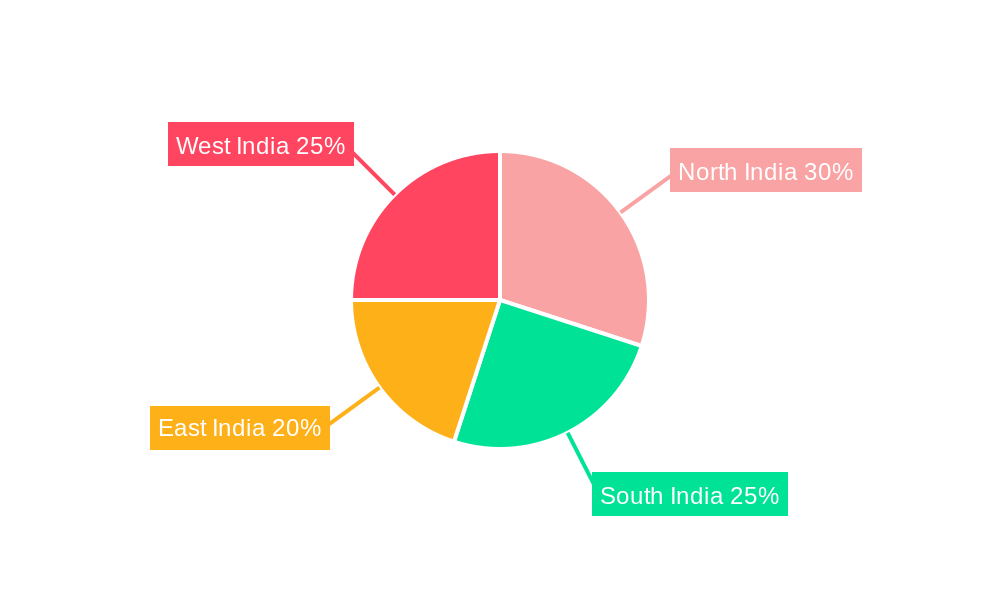

Dominant Regions, Countries, or Segments in India Automobile Industry

The Indian automobile market exhibits regional variations in its growth and dominance patterns. Two-wheelers constitute the largest segment by vehicle type, driven by affordability and suitability for diverse terrains. Passenger cars are the second largest segment with strong growth in urban areas. The North and West regions generally exhibit higher demand for vehicles compared to the East and South, reflecting factors like higher population density and economic activity. Petrol and diesel fuel types currently dominate, though the electric vehicle segment is rapidly gaining traction, fueled by government incentives and environmental concerns.

- Key Drivers:

- Economic growth: Rising disposable incomes and improved infrastructure.

- Government policies: Incentives for vehicle ownership and manufacturing.

- Urbanization: Increased demand for personal mobility in urban centers.

- Technological advancements: Fuel efficiency improvements and introduction of EVs.

- Dominant Segments: Two-wheelers and passenger cars are the largest by volume, with the petrol/gasoline segment leading in fuel type. North and West India represent the strongest regional markets.

India Automobile Industry Product Landscape

The Indian automobile market is characterized by a diverse range of vehicles catering to different consumer needs and price points. Product innovation focuses on improving fuel efficiency, safety features, and connectivity. The introduction of EVs and hybrid vehicles marks a significant technological advancement, and manufacturers are actively investing in research and development to improve battery technology and charging infrastructure. Unique selling propositions encompass fuel efficiency, style, safety technologies, and affordability, depending on the segment.

Key Drivers, Barriers & Challenges in India Automobile Industry

Key Drivers: Increasing disposable incomes, improving infrastructure, favorable government policies (e.g., production-linked incentive schemes), and technological advancements are driving the market.

Key Challenges & Restraints: Supply chain disruptions (semiconductor shortages, raw material costs), stringent emission norms, intense competition, and fluctuating fuel prices pose significant challenges. The impact of these challenges can lead to production delays and increased vehicle prices, affecting market growth.

Emerging Opportunities in India Automobile Industry

Untapped markets exist in rural areas, which offer potential for growth with accessible and affordable vehicles. There’s also potential in the burgeoning EV segment, including the development of charging infrastructure and battery technology. Evolving consumer preferences towards connected cars and autonomous driving features present further opportunities for technological innovation and market expansion.

Growth Accelerators in the India Automobile Industry Industry

Technological breakthroughs in EV batteries, autonomous driving, and connectivity will be crucial growth catalysts. Strategic partnerships between domestic and international players, particularly in the EV sector, will drive market growth. Expanding market access to rural areas and attracting foreign investment will accelerate future growth.

Key Players Shaping the India Automobile Industry Market

- Maruti Suzuki India Limited

- Piaggio & C SpA

- MG Motor India Pvt Ltd

- Bajaj Auto Corp

- Tata Motors Limited

- Hero Moto Corp

- Atul Auto Limited

- Mercedes-Benz India Pvt Ltd

- Honda Motorcycle & Scooter India Pvt Ltd

- Terra Motors India Corp

- Renault Group

- TVS Motor Company

- Volkswagen India

- Kinetic Green Energy & Power Solutions Lt

- Mahindra & Mahindra Limited

- Suzuki Motorcycle India Private Limited

- Royal Enfield

- Scooters India Ltd

- Honda Cars India Ltd

- Lohia Auto Industries

- Hyundai Motor India Ltd

- BMW AG

- BYD Company Ltd

Notable Milestones in India Automobile Industry Sector

- January 2024: Maruti Suzuki announces plans for a new Gujarat manufacturing facility with an annual capacity of 1 million vehicles, representing a USD 4.2 billion investment.

- February 2024: TVS Mobility secures a 32% investment from Mitsubishi Corporation, totaling USD 40 million, in its new subsidiary, TVS VMS.

In-Depth India Automobile Industry Market Outlook

The Indian automobile industry is poised for continued growth, driven by technological advancements, strategic partnerships, and expanding market access. The increasing adoption of EVs, coupled with supportive government policies, will shape the future market landscape. Strategic investments in infrastructure and technological innovation will be crucial to unlocking the industry's full potential and meeting the growing demand for sustainable and efficient transportation solutions. Opportunities abound for both domestic and international players looking to establish a strong foothold in this dynamic market.

India Automobile Industry Segmentation

-

1. Vehicle Type

- 1.1. Two-wheelers

- 1.2. Passenger Cars

- 1.3. Commercial Vehicles

- 1.4. Three-wheelers

-

2. Fuel Type

- 2.1. Diesel

- 2.2. Petrol/Gasoline

- 2.3. CNG and LPG

- 2.4. Electric

- 2.5. Others

India Automobile Industry Segmentation By Geography

- 1. India

India Automobile Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.20% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 The Growing Economy

- 3.2.2 Coupled with Rising Disposal Incomes and Urbanization

- 3.2.3 Fuels Demand for the Market

- 3.3. Market Restrains

- 3.3.1 Various Regulatory Changes

- 3.3.2 Safety Standards

- 3.3.3 and Taxation Policies by the Government may Hamper the Market

- 3.4. Market Trends

- 3.4.1. The Two-Wheelers Segment to Register Fastest Growth over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India Automobile Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Two-wheelers

- 5.1.2. Passenger Cars

- 5.1.3. Commercial Vehicles

- 5.1.4. Three-wheelers

- 5.2. Market Analysis, Insights and Forecast - by Fuel Type

- 5.2.1. Diesel

- 5.2.2. Petrol/Gasoline

- 5.2.3. CNG and LPG

- 5.2.4. Electric

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. North India India Automobile Industry Analysis, Insights and Forecast, 2019-2031

- 7. South India India Automobile Industry Analysis, Insights and Forecast, 2019-2031

- 8. East India India Automobile Industry Analysis, Insights and Forecast, 2019-2031

- 9. West India India Automobile Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 1 Maruti Suzuki India Limited

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 2 Piaggio & C SpA

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 5 MG Motor India Pvt Ltd

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 5 Bajaj Auto Corp

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 2 Tata Motors Limited (includes Tata and Jaguar)

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 2 Hero Moto Corp

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 4 Atul Auto Limited

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 11 Mercedes-Benz India Pvt Ltd

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 3 Honda Motorcycle & Scooter India Pvt Ltd

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 5 Terra Motors India Corp

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 7 Renault Group (Includes Nissan and Renault)

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 Two-wheelers

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.13 1 TVS Motor Company

- 10.2.13.1. Overview

- 10.2.13.2. Products

- 10.2.13.3. SWOT Analysis

- 10.2.13.4. Recent Developments

- 10.2.13.5. Financials (Based on Availability)

- 10.2.14 Three-wheelers

- 10.2.14.1. Overview

- 10.2.14.2. Products

- 10.2.14.3. SWOT Analysis

- 10.2.14.4. Recent Developments

- 10.2.14.5. Financials (Based on Availability)

- 10.2.15 6 Volkswagen India

- 10.2.15.1. Overview

- 10.2.15.2. Products

- 10.2.15.3. SWOT Analysis

- 10.2.15.4. Recent Developments

- 10.2.15.5. Financials (Based on Availability)

- 10.2.16 6 Kinetic Green Energy & Power Solutions Lt

- 10.2.16.1. Overview

- 10.2.16.2. Products

- 10.2.16.3. SWOT Analysis

- 10.2.16.4. Recent Developments

- 10.2.16.5. Financials (Based on Availability)

- 10.2.17 Passenger Cars and Commercial Vehicles

- 10.2.17.1. Overview

- 10.2.17.2. Products

- 10.2.17.3. SWOT Analysis

- 10.2.17.4. Recent Developments

- 10.2.17.5. Financials (Based on Availability)

- 10.2.18 4 Mahindra & Mahindra Limited

- 10.2.18.1. Overview

- 10.2.18.2. Products

- 10.2.18.3. SWOT Analysis

- 10.2.18.4. Recent Developments

- 10.2.18.5. Financials (Based on Availability)

- 10.2.19 6 Suzuki Motorcycle India Private Limited

- 10.2.19.1. Overview

- 10.2.19.2. Products

- 10.2.19.3. SWOT Analysis

- 10.2.19.4. Recent Developments

- 10.2.19.5. Financials (Based on Availability)

- 10.2.20 4 Royal Enfield

- 10.2.20.1. Overview

- 10.2.20.2. Products

- 10.2.20.3. SWOT Analysis

- 10.2.20.4. Recent Developments

- 10.2.20.5. Financials (Based on Availability)

- 10.2.21 3 Scooters India Ltd

- 10.2.21.1. Overview

- 10.2.21.2. Products

- 10.2.21.3. SWOT Analysis

- 10.2.21.4. Recent Developments

- 10.2.21.5. Financials (Based on Availability)

- 10.2.22 8 Honda Cars India Ltd

- 10.2.22.1. Overview

- 10.2.22.2. Products

- 10.2.22.3. SWOT Analysis

- 10.2.22.4. Recent Developments

- 10.2.22.5. Financials (Based on Availability)

- 10.2.23 1 Lohia Auto Industries

- 10.2.23.1. Overview

- 10.2.23.2. Products

- 10.2.23.3. SWOT Analysis

- 10.2.23.4. Recent Developments

- 10.2.23.5. Financials (Based on Availability)

- 10.2.24 3 Hyundai Motor India Ltd

- 10.2.24.1. Overview

- 10.2.24.2. Products

- 10.2.24.3. SWOT Analysis

- 10.2.24.4. Recent Developments

- 10.2.24.5. Financials (Based on Availability)

- 10.2.25 10 BMW AG (includes BMW and MINI)

- 10.2.25.1. Overview

- 10.2.25.2. Products

- 10.2.25.3. SWOT Analysis

- 10.2.25.4. Recent Developments

- 10.2.25.5. Financials (Based on Availability)

- 10.2.26 9 BYD Company Ltd

- 10.2.26.1. Overview

- 10.2.26.2. Products

- 10.2.26.3. SWOT Analysis

- 10.2.26.4. Recent Developments

- 10.2.26.5. Financials (Based on Availability)

- 10.2.1 1 Maruti Suzuki India Limited

List of Figures

- Figure 1: India Automobile Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India Automobile Industry Share (%) by Company 2024

List of Tables

- Table 1: India Automobile Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India Automobile Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 3: India Automobile Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 4: India Automobile Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: India Automobile Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: North India India Automobile Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: South India India Automobile Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: East India India Automobile Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: West India India Automobile Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: India Automobile Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 11: India Automobile Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 12: India Automobile Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Automobile Industry?

The projected CAGR is approximately 8.20%.

2. Which companies are prominent players in the India Automobile Industry?

Key companies in the market include 1 Maruti Suzuki India Limited, 2 Piaggio & C SpA, 5 MG Motor India Pvt Ltd, 5 Bajaj Auto Corp, 2 Tata Motors Limited (includes Tata and Jaguar), 2 Hero Moto Corp, 4 Atul Auto Limited, 11 Mercedes-Benz India Pvt Ltd, 3 Honda Motorcycle & Scooter India Pvt Ltd, 5 Terra Motors India Corp, 7 Renault Group (Includes Nissan and Renault), Two-wheelers, 1 TVS Motor Company, Three-wheelers, 6 Volkswagen India, 6 Kinetic Green Energy & Power Solutions Lt, Passenger Cars and Commercial Vehicles, 4 Mahindra & Mahindra Limited, 6 Suzuki Motorcycle India Private Limited, 4 Royal Enfield, 3 Scooters India Ltd, 8 Honda Cars India Ltd, 1 Lohia Auto Industries, 3 Hyundai Motor India Ltd, 10 BMW AG (includes BMW and MINI), 9 BYD Company Ltd.

3. What are the main segments of the India Automobile Industry?

The market segments include Vehicle Type, Fuel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 126.67 Million as of 2022.

5. What are some drivers contributing to market growth?

The Growing Economy. Coupled with Rising Disposal Incomes and Urbanization. Fuels Demand for the Market.

6. What are the notable trends driving market growth?

The Two-Wheelers Segment to Register Fastest Growth over the Forecast Period.

7. Are there any restraints impacting market growth?

Various Regulatory Changes. Safety Standards. and Taxation Policies by the Government may Hamper the Market.

8. Can you provide examples of recent developments in the market?

January 2024: Maruti Suzuki India intended to build a car production facility in Gujarat, India, capable of manufacturing 1 million vehicles annually, with an estimated investment of around INR 35,000 crore (USD 4.2 billion). This move is expected to bolster the Indian automobile industry significantly.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Automobile Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Automobile Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Automobile Industry?

To stay informed about further developments, trends, and reports in the India Automobile Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence