Key Insights

The Latin American mobile payments market is poised for significant expansion, driven by rising smartphone adoption, increased internet connectivity, and a thriving fintech ecosystem. Projecting a Compound Annual Growth Rate (CAGR) of 10.13%, the market is estimated to reach 787.74 billion by 2025. This growth is bolstered by widespread adoption of innovative payment solutions such as Brazil's Pix and similar regional platforms, alongside the increasing penetration of underbanked populations and a clear preference for digital transactions. Leading players, including Mercado Pago and Nubank, are actively shaping the market by offering localized, user-friendly mobile payment experiences. While proximity payments remain prevalent, remote payment solutions are experiencing rapid growth, signaling a strong shift towards e-commerce and digital services. Brazil and Mexico are leading the market, supported by their substantial populations and robust digital infrastructure. However, significant growth opportunities are present across the broader Latin American region, particularly with the expansion of digital financial inclusion programs.

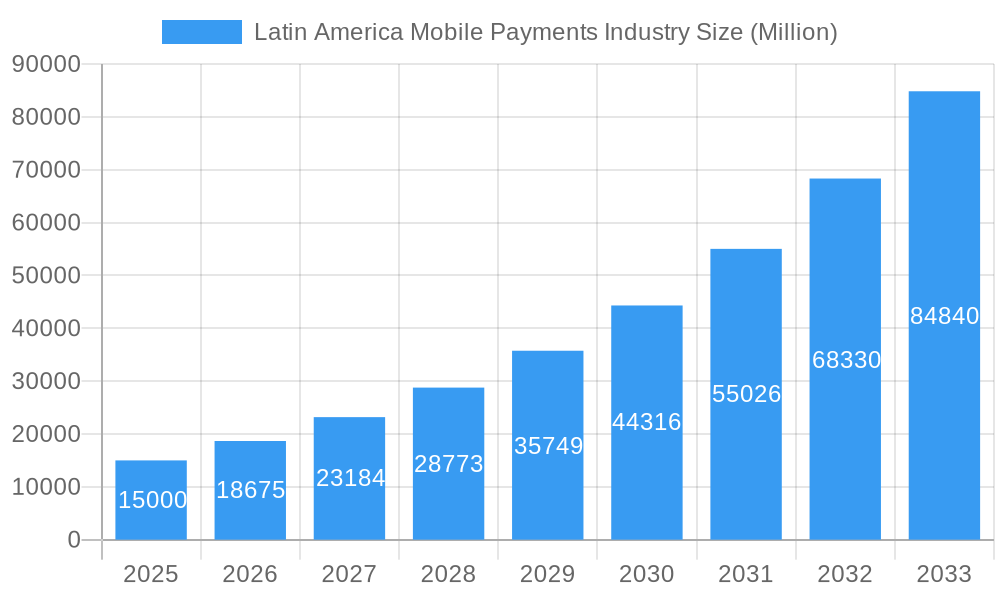

Latin America Mobile Payments Industry Market Size (In Billion)

Looking towards 2033, the market is expected to sustain its growth trajectory, propelled by government-led digital financial inclusion initiatives, the escalating adoption of mobile wallets, and the integration of mobile payments into comprehensive financial services. Key challenges include bridging digital literacy gaps, strengthening cybersecurity measures, and adapting to evolving regulatory frameworks. The competitive arena is characterized by continuous innovation from established players and the emergence of new entrants targeting niche markets. Ultimately, a strong emphasis on user experience, robust security, and pervasive financial inclusion will define the future of mobile payments in Latin America.

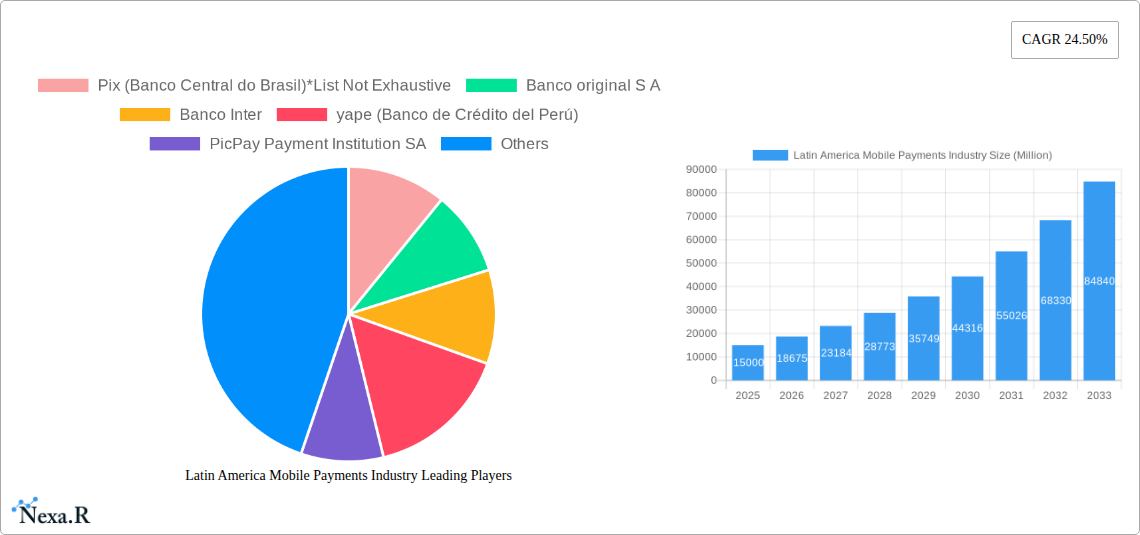

Latin America Mobile Payments Industry Company Market Share

Latin America Mobile Payments Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the dynamic Latin America mobile payments industry, covering the period 2019-2033. With a focus on key markets like Brazil and Mexico, and segments including proximity and remote payments, this report is essential for industry professionals, investors, and strategic planners. The report leverages extensive data analysis to provide valuable insights into market size, growth trends, competitive landscape, and future opportunities. The base year for this report is 2025, with estimates for 2025 and a forecast extending to 2033. The historical period covered is 2019-2024. Market values are presented in millions of units.

Latin America Mobile Payments Industry Market Dynamics & Structure

This section analyzes the market structure of the Latin American mobile payments industry, examining market concentration, technological innovation, regulatory frameworks, competitive substitutes, end-user demographics, and merger & acquisition (M&A) activity.

The Latin American mobile payments market is characterized by a dynamic interplay of established players and emerging fintechs. Market concentration is moderate, with a few dominant players and many smaller, specialized firms. Technological innovation is a key driver, fueled by advancements in mobile technology, biometrics, and AI. Regulatory frameworks vary across countries, impacting market penetration and adoption rates. The competitive landscape includes traditional financial institutions and a surge of fintech companies offering innovative solutions. The end-user demographic is shifting towards younger, digitally savvy populations, driving the growth of mobile payments. M&A activity has been significant, with larger players consolidating their market positions through strategic acquisitions.

- Market Concentration: Moderate, with a few dominant players and numerous smaller firms.

- Technological Innovation: Strong driver, including advancements in mobile technology, biometrics, and AI.

- Regulatory Frameworks: Vary significantly across countries, creating varying degrees of market openness.

- Competitive Landscape: Intense competition between established banks and emerging fintech companies.

- End-User Demographics: Increasingly younger and tech-savvy populations, driving adoption.

- M&A Activity: Significant volume, resulting in market consolidation. xx M&A deals in the past 5 years. xx% increase in deal volume year-on-year in 2024.

Latin America Mobile Payments Industry Growth Trends & Insights

This section details the evolution of the Latin American mobile payments market, analyzing market size, adoption rates, technological disruptions, and shifts in consumer behavior. Quantitative metrics like Compound Annual Growth Rate (CAGR) and market penetration are used to provide deeper insight.

The Latin American mobile payments market has experienced substantial growth in recent years, driven by increasing smartphone penetration, expanding internet access, and a growing preference for digital transactions. The market size has expanded significantly, with a CAGR of xx% during the historical period (2019-2024). The adoption of mobile payments is accelerating across diverse demographics, especially among younger consumers. Technological advancements, including improved mobile infrastructure and the rise of super-apps, continue to fuel market expansion. Changes in consumer behavior, such as an increasing preference for cashless transactions and the growing adoption of e-commerce, are driving the shift toward mobile payments. The forecast period (2025-2033) projects continued strong growth, with the market reaching xx million units by 2033.

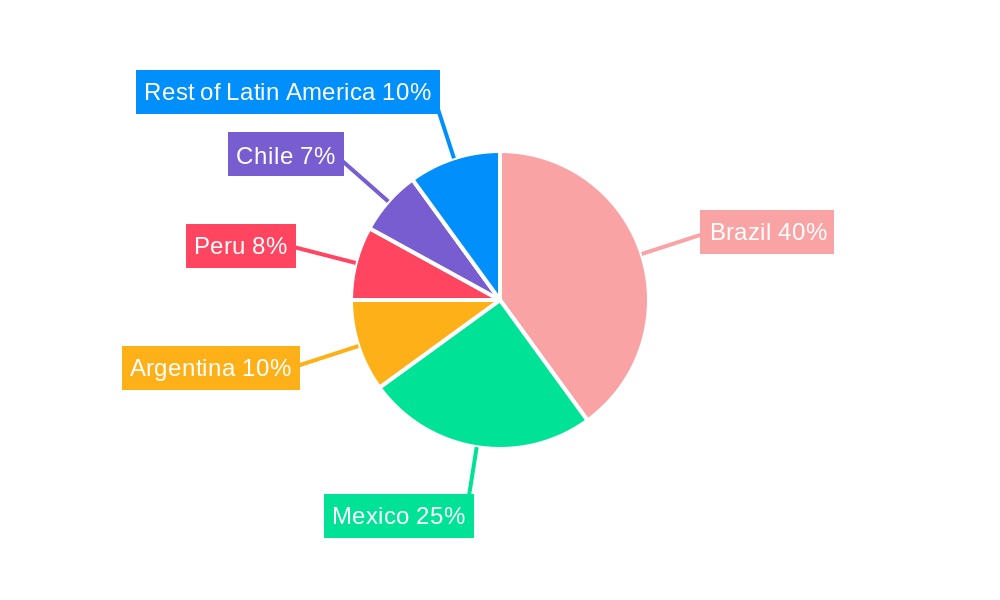

Dominant Regions, Countries, or Segments in Latin America Mobile Payments Industry

This section identifies the leading regions, countries, and segments within the Latin American mobile payments market. It analyzes dominance factors, including market share and growth potential, using detailed analysis to highlight key drivers such as economic policies and infrastructure development.

Brazil and Mexico are the dominant markets for mobile payments in Latin America, accounting for xx% and xx% of the regional market, respectively. Brazil's dominance is attributed to a combination of factors, including a large and growing population of smartphone users, a supportive regulatory environment, and a robust fintech ecosystem. Mexico's market is driven by rising digital adoption, improving infrastructure, and increasing e-commerce activity. The proximity payment type holds a xx% market share, driven by the high adoption of QR code-based payments. Remote payments account for xx% of the market, propelled by increased e-commerce and peer-to-peer (P2P) transactions.

- Brazil: Large smartphone user base, supportive regulations, and vibrant fintech ecosystem.

- Mexico: Rising digital adoption, improving infrastructure, and increased e-commerce activity.

- Proximity Payments: High adoption of QR code payments, driving market share.

- Remote Payments: Growth fueled by e-commerce and P2P transactions.

Latin America Mobile Payments Industry Product Landscape

This section provides an overview of the product innovations, applications, and performance metrics within the Latin American mobile payments landscape. It highlights unique selling propositions and key technological advancements.

The Latin American mobile payments landscape showcases a diverse range of products and services, from simple peer-to-peer (P2P) apps to sophisticated integrated payment platforms. Innovation is evident in the use of biometrics for enhanced security, AI-driven fraud detection systems, and the integration of mobile wallets with other financial services. These products are tailored to address specific regional needs, including support for various local currencies and functionalities catering to diverse consumer needs. Key performance metrics focus on transaction volume, processing speed, security, and customer satisfaction.

Key Drivers, Barriers & Challenges in Latin America Mobile Payments Industry

This section outlines the factors propelling the market's growth and the challenges hindering its expansion. Quantitative impacts are provided where available.

Key Drivers:

- Growing smartphone and internet penetration.

- Increasing adoption of e-commerce and digital services.

- Expanding fintech ecosystem with innovative solutions.

- Government initiatives promoting financial inclusion.

Challenges:

- Regulatory inconsistencies across countries.

- Concerns regarding data security and privacy.

- Limited financial literacy in certain segments.

- Infrastructure limitations in some areas, limiting access to mobile payment services.

Emerging Opportunities in Latin America Mobile Payments Industry

This section highlights emerging trends and opportunities within the Latin America mobile payments sector.

- Expanding into underserved rural markets.

- Developing innovative mobile payment solutions for micro, small, and medium-sized enterprises (MSMEs).

- Integrating mobile payments with other financial services, such as micro-loans and insurance.

- Leveraging blockchain technology for enhanced security and transparency.

Growth Accelerators in the Latin America Mobile Payments Industry

This section discusses the long-term growth catalysts within the Latin American mobile payments industry.

Continued advancements in mobile technology, coupled with strategic partnerships between fintech companies and traditional financial institutions, will accelerate growth. The increasing adoption of open banking APIs is expected to foster innovation and competition. Expansion into underserved markets and the development of tailored solutions for specific consumer segments will further fuel market expansion. Government initiatives promoting financial inclusion will also play a crucial role in driving long-term growth.

Key Players Shaping the Latin America Mobile Payments Industry Market

- Pix (Banco Central do Brasil)

- Banco original S A

- Banco Inter

- yape (Banco de Crédito del Perú)

- PicPay Payment Institution SA

- MercadoLibre S R L (Mercado Pago)

- RapiPay Fintech Pvt Ltd

- Pagbank(PAGSEGURO INTERNET S/A )

- Ame Digital

- Next Digital

- Nubank

- uala

Notable Milestones in Latin America Mobile Payments Industry Sector

- June 2022: Apple Pay Later launched, offering installment payments.

- June 2022: Elo and BV Financeira launched a payment solution integrating a prepaid card with abastece-aí's digital wallet.

In-Depth Latin America Mobile Payments Industry Market Outlook

The Latin American mobile payments market presents significant future potential, driven by several key factors. Continued growth in smartphone penetration and internet access, coupled with increasing consumer preference for digital transactions, will fuel market expansion. Innovation in mobile payment technologies, such as biometric authentication and AI-powered fraud detection, will further enhance the sector's attractiveness. Strategic partnerships between fintech companies and traditional banks will strengthen the ecosystem and drive further adoption. Opportunities abound for companies that can tailor their offerings to specific regional needs and consumer preferences, particularly in underserved markets.

Latin America Mobile Payments Industry Segmentation

-

1. Payme

- 1.1. Proximity

- 1.2. Remote

Latin America Mobile Payments Industry Segmentation By Geography

-

1. Latin America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Mexico

- 1.6. Peru

- 1.7. Venezuela

- 1.8. Ecuador

- 1.9. Bolivia

- 1.10. Paraguay

Latin America Mobile Payments Industry Regional Market Share

Geographic Coverage of Latin America Mobile Payments Industry

Latin America Mobile Payments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Payme

- 5.1.1. Proximity

- 5.1.2. Remote

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Payme

- 6. Latin America Mobile Payments Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Payme

- 6.1.1. Proximity

- 6.1.2. Remote

- 6.1. Market Analysis, Insights and Forecast - by Payme

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Pix (Banco Central do Brasil)*List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Banco original S A

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Banco Inter

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 yape (Banco de Crédito del Perú)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 PicPay Payment Institution SA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 MercadoLibre S R L (Mercado Pago)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 RapiPay Fintech Pvt Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Pagbank(PAGSEGURO INTERNET S/A )

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Ame Digital

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Next Digital

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Nubank

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 uala

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Pix (Banco Central do Brasil)*List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Latin America Mobile Payments Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Latin America Mobile Payments Industry Share (%) by Company 2025

List of Tables

- Table 1: Latin America Mobile Payments Industry Revenue billion Forecast, by Payme 2020 & 2033

- Table 2: Latin America Mobile Payments Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Latin America Mobile Payments Industry Revenue billion Forecast, by Payme 2020 & 2033

- Table 4: Latin America Mobile Payments Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Brazil Latin America Mobile Payments Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Argentina Latin America Mobile Payments Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Chile Latin America Mobile Payments Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Colombia Latin America Mobile Payments Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Latin America Mobile Payments Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Peru Latin America Mobile Payments Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Venezuela Latin America Mobile Payments Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Ecuador Latin America Mobile Payments Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Bolivia Latin America Mobile Payments Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Paraguay Latin America Mobile Payments Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America Mobile Payments Industry?

The projected CAGR is approximately 10.13%.

2. Which companies are prominent players in the Latin America Mobile Payments Industry?

Key companies in the market include Pix (Banco Central do Brasil)*List Not Exhaustive, Banco original S A, Banco Inter, yape (Banco de Crédito del Perú), PicPay Payment Institution SA, MercadoLibre S R L (Mercado Pago), RapiPay Fintech Pvt Ltd, Pagbank(PAGSEGURO INTERNET S/A ), Ame Digital, Next Digital, Nubank, uala.

3. What are the main segments of the Latin America Mobile Payments Industry?

The market segments include Payme.

4. Can you provide details about the market size?

The market size is estimated to be USD 787.74 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing number of smartphone users; Increasing internet penetration and growing E-commerce & M-commerce market.

6. What are the notable trends driving market growth?

NFC (Near-field communication) will Hold Major Market Share.

7. Are there any restraints impacting market growth?

High Initial Cost Involved.

8. Can you provide examples of recent developments in the market?

June 2022 - Apple pay announced an update to its Apple Pay solutions: Apple Pay Later, which will allow users to pay in installments for their purchases-divided into four equal payments, over six weeks, without late fees or interest. The launch aims to increase focus on the payments industry.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America Mobile Payments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America Mobile Payments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America Mobile Payments Industry?

To stay informed about further developments, trends, and reports in the Latin America Mobile Payments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence