Key Insights

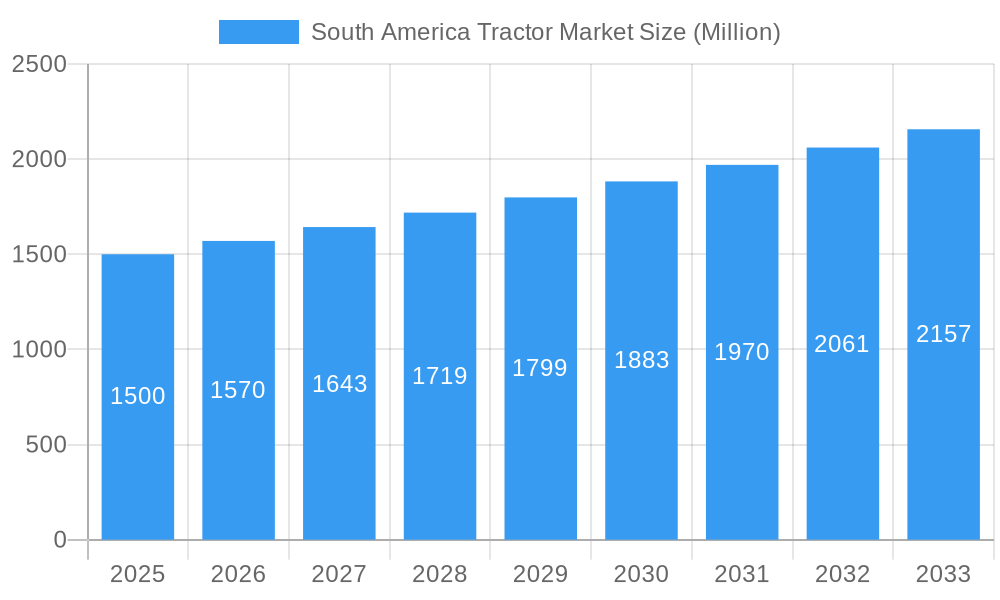

The South American tractor market, valued at approximately $XX million in 2025, is projected to experience steady growth, driven by a Compound Annual Growth Rate (CAGR) of 4.50% from 2025 to 2033. This expansion is fueled by several key factors. Firstly, the increasing demand for efficient agricultural practices across Brazil and Argentina, the largest markets within the region, is a major catalyst. Modernization of farming techniques, coupled with government initiatives promoting agricultural development, are contributing significantly to tractor adoption. Secondly, the rising acreage under cultivation for key crops like soybeans and sugarcane necessitates robust and efficient machinery, boosting the demand for higher horsepower tractors. The expanding livestock sector also fuels demand, particularly for orchard and row-crop tractors. However, the market faces certain challenges. Economic fluctuations in the region can impact investment in agricultural equipment. Moreover, fluctuating commodity prices and competition from used tractor imports could present constraints on market growth. Segmentation reveals a preference for tractors in the 81-130 HP range, reflecting a balance between affordability and sufficient power for diverse applications. Key players such as ZETOR TRACTORS a s, AGCO Corporation, and Mahindra & Mahindra Ltd. are strategically focusing on product innovation and localized distribution networks to capitalize on this expanding market.

South America Tractor Market Market Size (In Billion)

The forecast period (2025-2033) anticipates a continuous upward trajectory for the South American tractor market, though the pace might fluctuate slightly year-to-year due to macroeconomic factors. Brazil and Argentina, benefiting from relatively fertile land and supportive government policies, will likely remain the dominant markets within South America. Further growth is expected as farmers adopt more advanced technologies to enhance productivity and efficiency. The shift toward higher-horsepower tractors will continue, driven by the increasing scale of agricultural operations and the demand for specialized equipment for diverse crops and terrains. Companies are expected to respond by offering a wider array of models to cater to the varied needs of different farm sizes and agricultural practices across the region. The market is likely to witness increased competition, leading to innovative financing options and after-sales services to attract customers and secure market share.

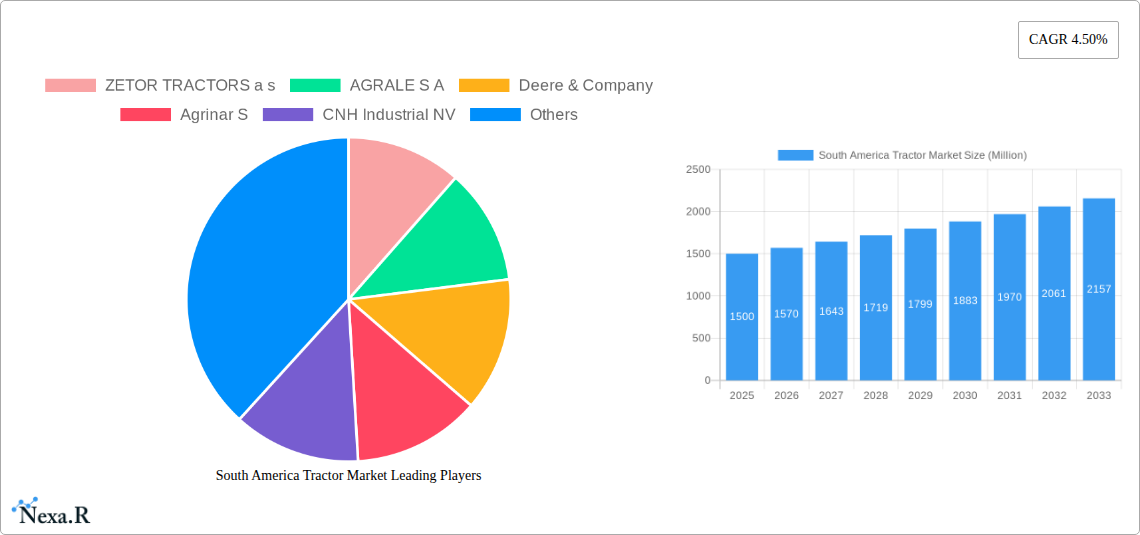

South America Tractor Market Company Market Share

South America Tractor Market: A Comprehensive Analysis (2019-2033)

This in-depth report provides a comprehensive analysis of the South America Tractor Market, covering market dynamics, growth trends, dominant segments, key players, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The report uses Million units as the unit of measurement for market size.

Keywords: South America Tractor Market, Tractor Market, Agricultural Machinery, Farm Equipment, Orchard Tractors, Row-Crop Tractors, ZETOR TRACTORS, AGRALE S.A, Deere & Company, Agrinar S, CNH Industrial, CLAAS, Kubota, Mahindra & Mahindra, AGCO, Below 80 HP Tractors, 81 HP to 130 HP Tractors, Above 130 HP Tractors, Market Size, Market Share, Market Growth, Market Forecast, Industry Analysis, Competitive Landscape

South America Tractor Market Dynamics & Structure

This section analyzes the South America tractor market's competitive landscape, technological advancements, and regulatory influences, shaping its current structure and future trajectory. The market is characterized by a moderate level of concentration, with a few major players holding significant market share. However, smaller regional players also contribute substantially to the overall market volume.

- Market Concentration: The top 5 players account for approximately xx% of the total market share in 2025.

- Technological Innovation: Precision agriculture technologies, such as GPS-guided tractors and automated systems, are driving innovation and efficiency gains. However, high initial investment costs and limited access to technology in certain regions represent barriers to wider adoption.

- Regulatory Framework: Government policies promoting agricultural modernization and rural development significantly impact market growth. Subsidies and financing schemes for tractor purchases influence market demand.

- Competitive Substitutes: The primary substitutes include used tractors and animal-powered farming, particularly in smaller farms. However, the increasing efficiency and productivity of modern tractors are driving substitution away from these alternatives.

- End-User Demographics: The market comprises a mix of large-scale commercial farms and smallholder farmers. The needs and preferences of these two groups influence tractor types and features in demand.

- M&A Trends: The tractor manufacturing landscape has witnessed xx M&A deals in the last five years, primarily focused on expanding market reach and technological capabilities.

South America Tractor Market Growth Trends & Insights

The South America Tractor Market has demonstrated robust expansion, experiencing a significant compound annual growth rate (CAGR) during the historical period (2019-2024). The market size reached approximately **[Insert Specific Value] Million units in 2024**. This upward trajectory is primarily fueled by the escalating demand for agricultural output, coupled with proactive government initiatives aimed at enhancing agricultural productivity across the region. Looking ahead, the market is poised for continued growth, projected to expand at a CAGR of **[Insert Specific Value]%** during the forecast period (2025-2033), with an anticipated market size of **[Insert Specific Value] Million units by 2033**. Key growth catalysts include the rising global demand for food and agricultural products, the increasing embrace of modern and sustainable farming methodologies, and substantial improvements in rural infrastructure. While technological disruptions such as precision farming and the emergence of autonomous tractors are gradually gaining traction, their adoption rates remain comparatively lower than in developed markets. Nonetheless, evolving consumer preferences towards more efficient and technologically advanced tractor solutions are actively shaping product development strategies and market segmentation within South America.

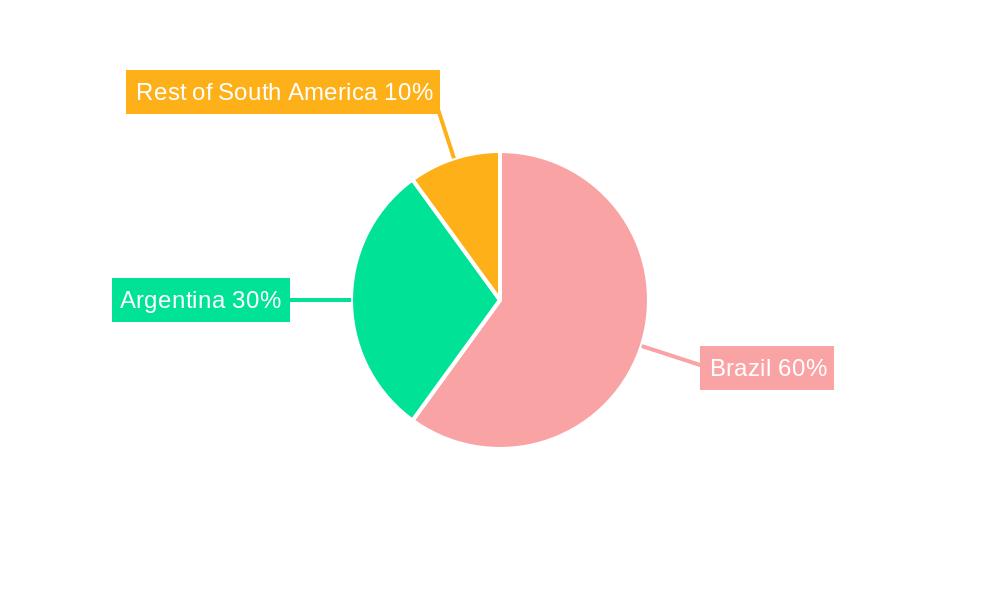

Dominant Regions, Countries, or Segments in South America Tractor Market

Brazil holds the largest market share within South America for tractors, accounting for approximately xx% of total sales in 2025. This dominance stems from its vast agricultural land, robust agricultural sector, and government support for agricultural mechanization. Argentina and Colombia also constitute significant markets.

- Horsepower: The 81 HP to 130 HP segment holds the largest market share, driven by the prevalence of medium-sized farms.

- Type: Row-crop tractors dominate the market due to the region's large-scale crop production.

- Key Drivers: Government incentives for farm mechanization, expanding agricultural land under cultivation, and favorable economic conditions in certain periods contribute to the market's growth in dominant regions.

South America Tractor Market Product Landscape

The South America tractor market exhibits a diverse product landscape encompassing various horsepower ranges, tractor types tailored to specific agricultural needs (orchard, row-crop, etc.), and technological features. Recent innovations focus on improving fuel efficiency, enhancing operator comfort, and integrating precision agriculture technologies like GPS-guided steering and automated functionalities. These advancements aim to boost productivity and reduce operational costs. Key selling propositions include enhanced durability, adaptability to varied terrains, and affordability for diverse farming operations.

Key Drivers, Barriers & Challenges in South America Tractor Market

Key Drivers: The expansion of agricultural land and intensification of farming practices, coupled with robust government support for farm modernization and mechanization, are powerful drivers. Additionally, rising disposable incomes among certain farming segments and a growing awareness of the economic and operational benefits derived from agricultural mechanization are further propelling market growth.

Challenges: Significant hurdles include the high initial capital expenditure required for purchasing tractors, which can be particularly prohibitive for smallholder farmers. Limited access to affordable credit and flexible financing options exacerbates this challenge. Furthermore, persistent infrastructural limitations in various rural areas, including inadequate road networks and power supply, can impede efficient tractor operation and maintenance. Fluctuations in global agricultural commodity prices and prevailing economic instability within individual countries can also create demand volatility. Moreover, the imposition of import tariffs and restrictive trade policies in certain South American nations can impact tractor pricing and overall market accessibility.

Emerging Opportunities in South America Tractor Market

Untapped potential lies in expanding tractor sales to smallholder farmers through affordable financing schemes and tailored product offerings. The integration of precision agriculture technologies presents a significant opportunity for growth, as does catering to the demand for specialized tractors for specific crops and farming conditions.

Growth Accelerators in the South America Tractor Market Industry

Continuous technological innovation in tractor design, focusing on enhanced fuel efficiency, improved operational capabilities, and the integration of automation features, will be a critical growth accelerator. The forging of strategic alliances and partnerships between leading tractor manufacturers and agricultural input suppliers presents a significant opportunity to develop integrated solutions and unlock new value propositions for farmers. Government-led initiatives that actively promote agricultural modernization, invest in vital infrastructure development, and offer subsidies or incentives for technology adoption will substantially amplify market potential. Furthermore, the strategic expansion into untapped regional markets within South America, alongside the exploration of lucrative export opportunities, will play a pivotal role in driving overall industry expansion.

Key Players Shaping the South America Tractor Market Market

Notable Milestones in South America Tractor Market Sector

- 2023 Q4: A leading manufacturer introduced a new line of compact tractors specifically designed for small-scale farmers and specialized crops, addressing a key market segment.

- 2023 Q2: Several countries in the region implemented new agricultural policies offering tax incentives for the purchase of advanced agricultural machinery, including modern tractors.

- 2022 Q3: Deere & Company launched a new series of high-horsepower tractors optimized for South American soil conditions and farming practices, enhancing productivity for larger agricultural operations.

- 2021 Q4: AGRALE S.A. announced a strategic partnership with a prominent local financing company to significantly expand access to tailored credit solutions for smallholder farmers, easing the financial burden of mechanization.

- 2020 Q1: CNH Industrial made substantial investments in upgrading its manufacturing facilities in Brazil, boosting production capacity and efficiency to meet the growing regional demand for tractors.

In-Depth South America Tractor Market Market Outlook

The South America tractor market is characterized by a highly promising growth outlook, propelled by sustained agricultural expansion, the accelerating adoption of contemporary and sustainable farming techniques, and committed government support for rural development and agricultural modernization. Strategic opportunities abound for market players that prioritize innovation, develop cost-effective and accessible solutions, and tailor their product offerings to the diverse and evolving needs of South American farmers. The coming years are expected to witness a significant surge in technological advancements, including the increased integration of precision agriculture systems and the gradual introduction of autonomous tractor technologies, promising to revolutionize farming practices. To fully unlock future growth potential, it will be imperative for market stakeholders to focus on enhancing market access for smallholder farmers through innovative financing and support programs, alongside continued investment in and development of essential rural infrastructure across the continent.

South America Tractor Market Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

South America Tractor Market Segmentation By Geography

-

1. South America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Peru

- 1.6. Venezuela

- 1.7. Ecuador

- 1.8. Bolivia

- 1.9. Paraguay

- 1.10. Uruguay

South America Tractor Market Regional Market Share

Geographic Coverage of South America Tractor Market

South America Tractor Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. South America

- 6. South America Tractor Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 ZETOR TRACTORS a s

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 AGRALE S A

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Deere & Company

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Agrinar S

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 CNH Industrial NV

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 CLAAS KGaA mbH

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Kubota Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Mahindra & Mahindra Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AGCO Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 ZETOR TRACTORS a s

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South America Tractor Market Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: South America Tractor Market Share (%) by Company 2025

List of Tables

- Table 1: South America Tractor Market Revenue undefined Forecast, by Production Analysis 2020 & 2033

- Table 2: South America Tractor Market Revenue undefined Forecast, by Consumption Analysis 2020 & 2033

- Table 3: South America Tractor Market Revenue undefined Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: South America Tractor Market Revenue undefined Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: South America Tractor Market Revenue undefined Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: South America Tractor Market Revenue undefined Forecast, by Region 2020 & 2033

- Table 7: South America Tractor Market Revenue undefined Forecast, by Production Analysis 2020 & 2033

- Table 8: South America Tractor Market Revenue undefined Forecast, by Consumption Analysis 2020 & 2033

- Table 9: South America Tractor Market Revenue undefined Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: South America Tractor Market Revenue undefined Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: South America Tractor Market Revenue undefined Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: South America Tractor Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil South America Tractor Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina South America Tractor Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Chile South America Tractor Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Colombia South America Tractor Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 17: Peru South America Tractor Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Venezuela South America Tractor Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 19: Ecuador South America Tractor Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Bolivia South America Tractor Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: Paraguay South America Tractor Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Uruguay South America Tractor Market Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Tractor Market?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the South America Tractor Market?

Key companies in the market include ZETOR TRACTORS a s, AGRALE S A, Deere & Company, Agrinar S, CNH Industrial NV, CLAAS KGaA mbH, Kubota Corporation, Mahindra & Mahindra Ltd, AGCO Corporation.

3. What are the main segments of the South America Tractor Market?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Low Availability of Skilled Labor; Technological Advancements.

6. What are the notable trends driving market growth?

Increasing Cost of Farm Labor Driving the Market.

7. Are there any restraints impacting market growth?

Increasing Farm Expenditure; Security Concerns in Modern Farming Machinery.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Tractor Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Tractor Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Tractor Market?

To stay informed about further developments, trends, and reports in the South America Tractor Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence