Key Insights

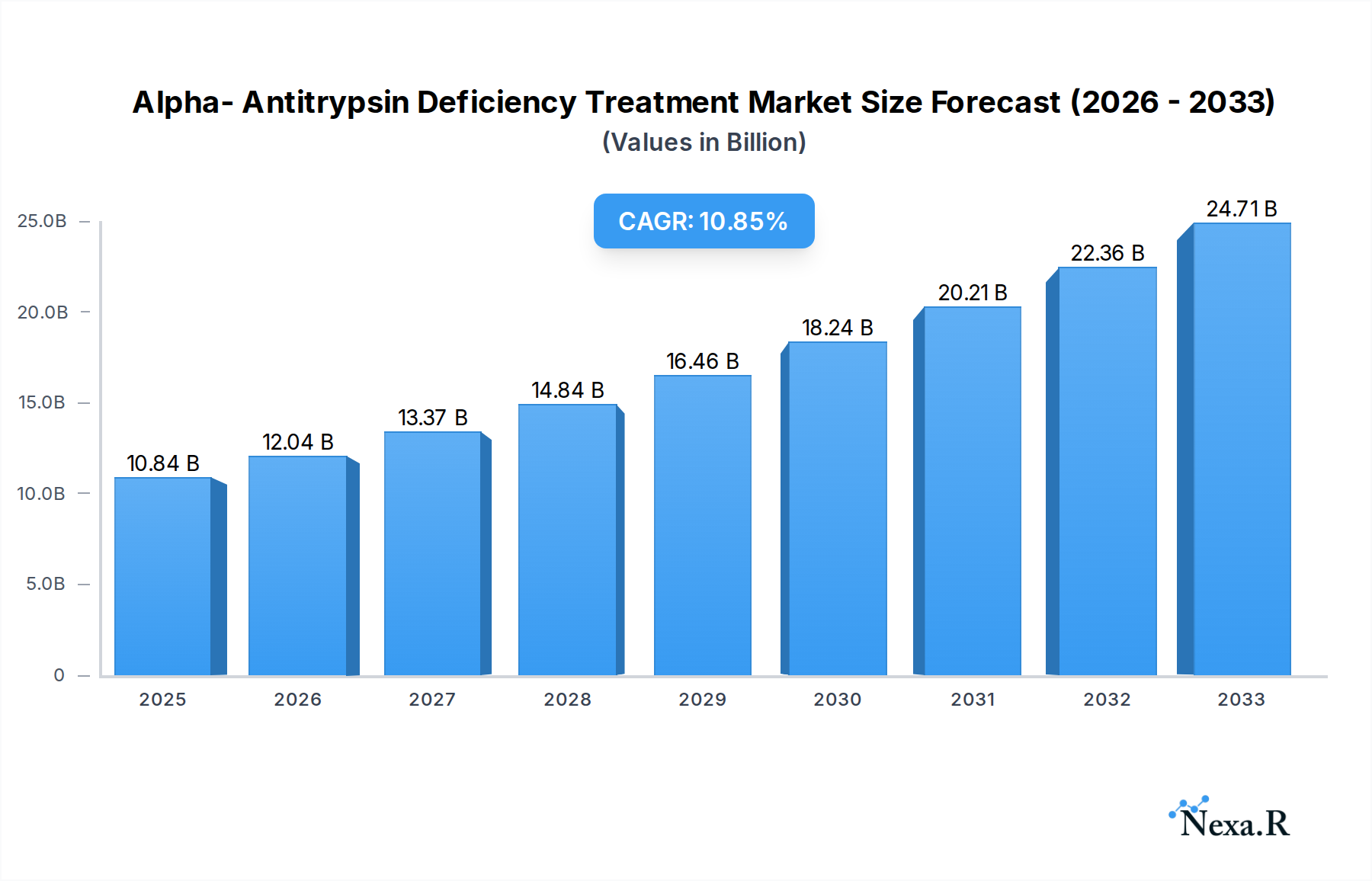

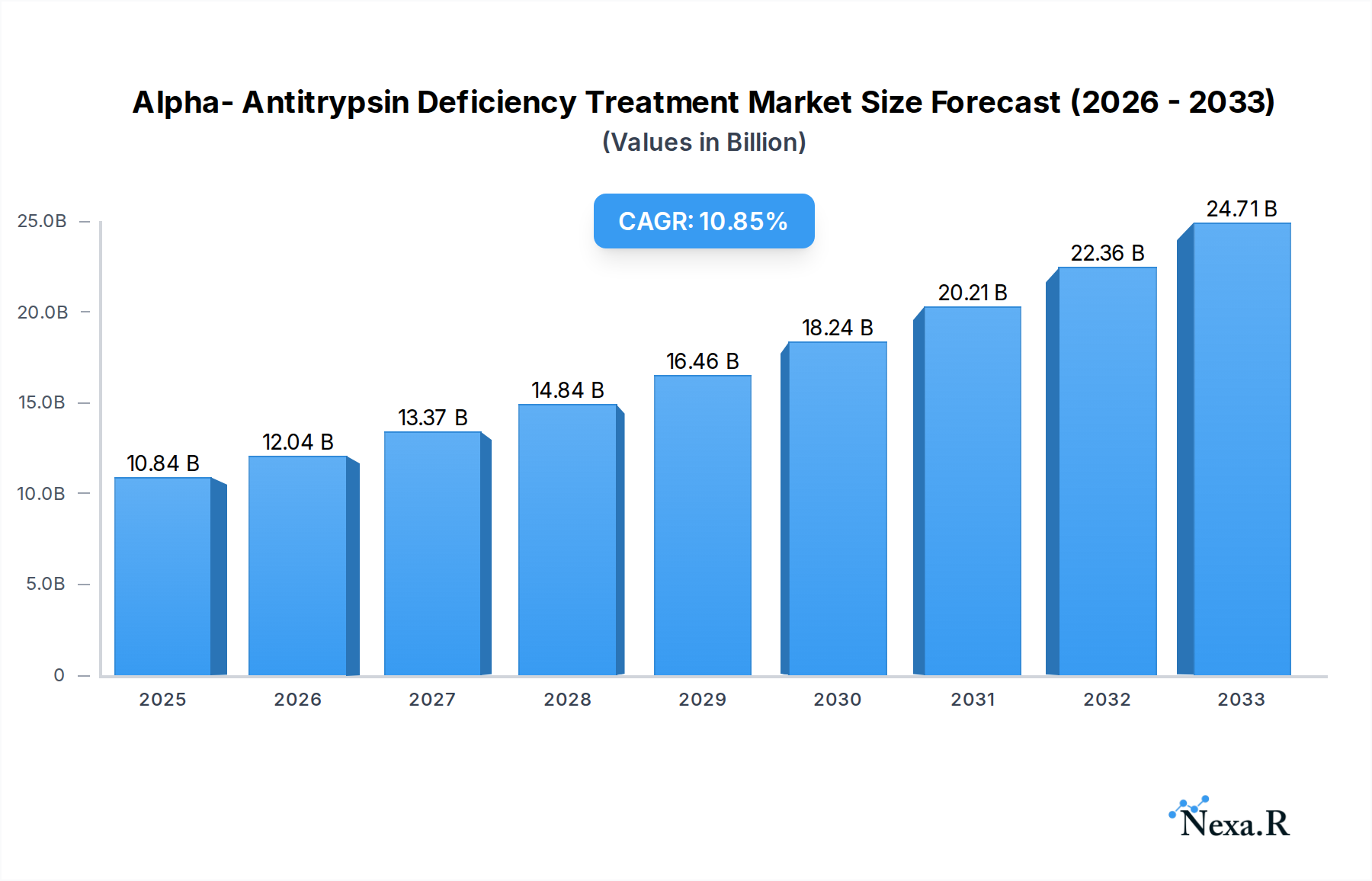

The Alpha-Antitrypsin Deficiency (AATD) treatment market is poised for significant expansion, projected to reach $10.84 billion in 2025 with a robust Compound Annual Growth Rate (CAGR) of 11.02% through 2033. This impressive growth is primarily fueled by an increased understanding of AATD, leading to enhanced diagnosis rates and a growing demand for effective therapeutic interventions. The market's expansion is critically driven by advancements in gene therapy and protein replacement therapies, which offer novel approaches to address the underlying genetic defect and its resulting organ damage, particularly in the lungs and liver. Furthermore, a rising prevalence of respiratory and liver diseases associated with AATD, coupled with a growing awareness among healthcare professionals and patients, are contributing factors to this upward trajectory. The integration of innovative treatment modalities and a focus on personalized medicine are expected to further propel market growth, creating new opportunities for pharmaceutical and biotechnology companies.

Alpha- Antitrypsin Deficiency Treatment Market Size (In Billion)

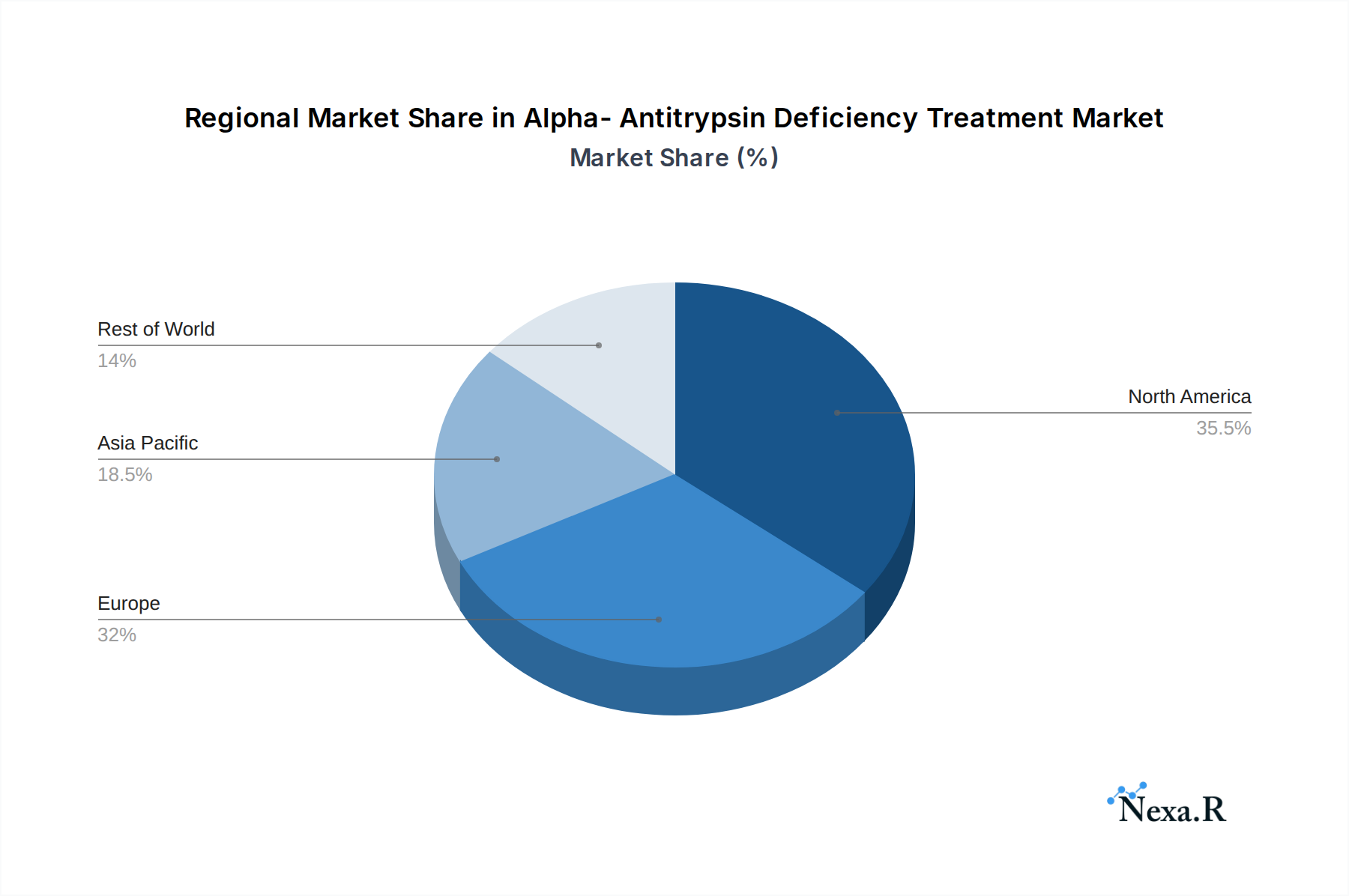

The AATD treatment landscape is segmented by diverse applications, including clinics and hospitals, catering to a broad spectrum of patient needs. Key treatment types such as CT-2009, POL-6014, ARO-AAT, and ALNAAT-02 represent the evolving therapeutic pipeline, with ongoing research and development promising more targeted and efficient treatments. Despite the promising outlook, certain restraints may influence market dynamics, including the high cost of advanced therapies and the complex regulatory pathways for novel gene and cell therapies. However, these challenges are being actively addressed through strategic partnerships and continued investment in research. North America and Europe currently dominate the market, driven by advanced healthcare infrastructures and higher patient awareness. Yet, the Asia Pacific region is anticipated to exhibit substantial growth due to increasing healthcare spending, a burgeoning patient population, and expanding diagnostic capabilities, signifying a global shift in treatment accessibility and adoption.

Alpha- Antitrypsin Deficiency Treatment Company Market Share

Alpha-Antitrypsin Deficiency Treatment Market: Comprehensive Growth Analysis and Future Outlook (2019–2033)

This report offers an in-depth analysis of the global Alpha-Antitrypsin Deficiency (AATD) treatment market, projecting robust growth and identifying key drivers, challenges, and opportunities. Leveraging extensive market intelligence, we provide a detailed roadmap for stakeholders navigating this evolving therapeutic landscape. The study encompasses a comprehensive market valuation from 2019 to 2033, with a base year of 2025 and a detailed forecast period from 2025 to 2033. We analyze parent and child market segments to provide a holistic view, incorporating high-traffic keywords for maximum SEO visibility.

Alpha- Antitrypsin Deficiency Treatment Market Dynamics & Structure

The Alpha-Antitrypsin Deficiency treatment market is characterized by dynamic evolution driven by advancements in genetic therapies and a growing understanding of the disease's underlying mechanisms. Market concentration is shifting as novel gene therapy and gene editing companies emerge, challenging established players in protein replacement therapies. Technological innovation is a primary driver, with significant investments in RNA interference (RNAi), CRISPR-based gene editing, and adeno-associated virus (AAV) gene therapy platforms. Regulatory frameworks are adapting to accommodate these novel therapeutic modalities, with regulatory bodies actively working to streamline approval processes for orphan diseases like AATD. Competitive product substitutes include traditional protein augmentation therapies, but the focus is increasingly on curative or disease-modifying treatments. End-user demographics comprise individuals diagnosed with AATD, with a growing emphasis on early diagnosis and proactive treatment. Mergers and acquisitions (M&A) trends are significant, indicating consolidation and strategic partnerships to leverage complementary technologies and expand market reach. For instance, the number of M&A deals in this segment has shown a XX% increase year-over-year during the historical period. Barriers to innovation include the high cost of research and development, long clinical trial durations, and the need for robust safety and efficacy data for novel gene therapies.

- Market Concentration Shifts: Rise of biotech startups with gene therapy platforms challenging established protein augmentation companies.

- Technological Innovation Drivers: Gene editing (CRISPR), RNAi, and AAV gene therapy platforms are at the forefront.

- Regulatory Landscape Evolution: Streamlining approval pathways for rare genetic diseases.

- Competitive Landscape: Emerging gene therapies vs. existing protein augmentation.

- End-User Focus: Early diagnosis and long-term disease management.

- M&A Activity: Strategic alliances and acquisitions to gain access to novel technologies.

Alpha- Antitrypsin Deficiency Treatment Growth Trends & Insights

The Alpha-Antitrypsin Deficiency treatment market is poised for substantial growth, driven by an increasing prevalence of diagnosed cases, heightened awareness, and a robust pipeline of innovative therapies. The global market size, valued at approximately $2.8 billion in 2023, is projected to reach $9.5 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 12.8% during the forecast period (2025–2033). This expansion is fueled by significant advancements in gene therapy and gene editing technologies, which offer the potential for disease modification and, in some cases, a functional cure. The adoption rates of these novel treatments are expected to accelerate as clinical data solidifies and regulatory approvals become more widespread. Technological disruptions, particularly in the realm of personalized medicine and in vivo gene editing, are poised to revolutionize AATD management. These advancements promise to address the root cause of the deficiency, offering more durable and potentially curative solutions compared to existing protein augmentation therapies. Consumer behavior is shifting towards seeking proactive, long-term treatment options, with a greater willingness to embrace innovative therapies that offer a higher quality of life. The increasing understanding of AATD's impact on both lung and liver health also broadens the patient population eligible for treatment. Furthermore, government initiatives and patient advocacy groups are playing a crucial role in driving awareness and facilitating access to advanced therapies. The market penetration of gene-based therapies is still in its nascent stages but is expected to climb significantly as more products gain approval and demonstrate long-term efficacy and safety. Investment in R&D for AATD treatments has surged, with venture capital funding and pharmaceutical company commitments reaching an estimated $1.2 billion in 2024. This influx of capital is critical for accelerating clinical trials and bringing promising therapies to market. The development of more sophisticated diagnostic tools also contributes to an increased diagnosis rate, thereby expanding the addressable market. The shift from symptomatic management to disease-modifying therapies will be a defining trend, creating a significant demand for therapies that can permanently correct the underlying genetic defect.

Dominant Regions, Countries, or Segments in Alpha- Antitrypsin Deficiency Treatment

North America is currently the dominant region in the Alpha-Antitrypsin Deficiency treatment market, driven by a strong healthcare infrastructure, high patient awareness, significant R&D investments, and favorable reimbursement policies for advanced therapies. The United States, in particular, represents a substantial portion of this dominance due to a large patient population, a robust pharmaceutical industry, and a proactive approach to adopting innovative treatments. The market in this region is further propelled by leading research institutions and the presence of key pharmaceutical and biotechnology companies actively involved in AATD therapy development. Government funding for rare disease research and support for orphan drug development also contribute to North America's leading position.

The application segment of Hospitals holds a significant market share due to the complexity of AATD management and the need for specialized care and advanced treatment administration, often within an inpatient or specialized outpatient setting. Clinics also represent a growing segment, particularly for routine monitoring and protein augmentation therapy administration.

Within the Types segment, while historically dominated by protein augmentation therapies, the market is rapidly shifting towards novel gene therapy approaches. ARO-AAT and ALNAAT-02, representing advanced gene therapy candidates, are showing immense promise and are expected to drive future market growth. CT-2009 and POL-6014 also contribute significantly, reflecting the diverse pipeline of therapeutic strategies being explored. The "Others" category, encompassing emerging gene editing technologies and novel delivery systems, is expected to witness substantial growth.

Key drivers for North America's dominance include:

- High Prevalence and Diagnosis Rates: Early and accurate diagnosis of AATD leads to a larger addressable patient pool.

- Advanced Healthcare Infrastructure: Well-equipped hospitals and specialized clinics facilitate the administration of complex AATD treatments.

- Robust R&D Ecosystem: Leading research institutions and biopharmaceutical companies drive innovation and therapeutic development.

- Favorable Reimbursement Policies: Insurance coverage for orphan drugs and advanced therapies supports market access.

- Patient Advocacy and Awareness: Strong patient advocacy groups promote awareness and demand for effective treatments.

- Investment in Gene Therapy: Significant venture capital and pharmaceutical investment in gene therapy R&D.

- Regulatory Support: Expedited review pathways for rare disease treatments.

Alpha- Antitrypsin Deficiency Treatment Product Landscape

The Alpha-Antitrypsin Deficiency treatment product landscape is undergoing a profound transformation, shifting from traditional protein augmentation therapies to cutting-edge gene-based interventions. Innovations are centered around directly addressing the genetic root cause of AATD. Gene therapy vectors, such as adeno-associated viruses (AAVs), are being engineered to deliver functional SERPINA1 genes to liver cells, aiming to restore normal AAT protein production. Gene editing technologies, including CRISPR-Cas9, are also being explored for in vivo correction of the Z-allele mutation responsible for the deficiency. RNA interference (RNAi) therapies are being developed to silence the production of misfolded AAT proteins in the liver, preventing their accumulation and subsequent damage to the organ. These novel therapeutic modalities offer the potential for long-term disease modification and a significant improvement in patient outcomes compared to current palliative treatments.

Key Drivers, Barriers & Challenges in Alpha- Antitrypsin Deficiency Treatment

The Alpha-Antitrypsin Deficiency treatment market is propelled by several key drivers. Firstly, the increasing understanding of AATD's pathophysiology and its significant impact on lung and liver health fuels demand for effective therapies. Secondly, rapid advancements in gene therapy, gene editing, and RNAi technologies offer a promising path towards disease modification and potential cures. Thirdly, a growing pipeline of investigational therapies in late-stage clinical trials is creating optimism and driving investment. Finally, increased patient awareness and advocacy efforts are leading to earlier diagnosis and greater demand for advanced treatment options.

However, the market faces significant barriers and challenges. The high cost of gene and cell therapies poses a substantial challenge for accessibility and affordability, particularly in healthcare systems with limited reimbursement. Long and complex clinical trial processes for novel gene therapies, coupled with the need for extensive safety and efficacy data, can prolong the time to market. Manufacturing scalability and quality control for complex biological therapies remain critical hurdles. Regulatory scrutiny and the need for robust post-market surveillance add to the challenges. Furthermore, competition from existing protein augmentation therapies, which have a well-established track record, presents a challenge for the adoption of newer, more expensive treatments.

Emerging Opportunities in Alpha- Antitrypsin Deficiency Treatment

Emerging opportunities in the Alpha-Antitrypsin Deficiency treatment market are primarily driven by the advancement of gene therapy and gene editing technologies. The development of in vivo gene editing tools that can correct the genetic defect directly in the liver presents a paradigm shift in treatment. Untapped markets in developing regions with a high burden of genetic diseases, coupled with improved diagnostics and increasing healthcare expenditure, represent significant growth potential. The exploration of combination therapies, integrating gene-based interventions with novel small molecule drugs or immunomodulators, could offer synergistic benefits and improved patient outcomes. Furthermore, the growing recognition of AATD's extra-pulmonary manifestations opens avenues for therapeutic strategies targeting these conditions.

Growth Accelerators in the Alpha- Antitrypsin Deficiency Treatment Industry

Growth accelerators in the Alpha-Antitrypsin Deficiency treatment industry are intrinsically linked to scientific breakthroughs and strategic market plays. Continuous innovation in gene delivery systems, enhancing their efficiency and safety, will be a critical catalyst. Strategic partnerships between large pharmaceutical companies and nimble biotechnology firms specializing in gene therapy and gene editing are accelerating the development and commercialization of novel treatments. Furthermore, expanded patient registries and real-world data collection will provide invaluable evidence to support the long-term efficacy and safety of emerging therapies, facilitating broader adoption and reimbursement. The increasing focus on precision medicine and personalized treatment approaches tailored to individual genetic profiles will also significantly drive market expansion.

Key Players Shaping the Alpha- Antitrypsin Deficiency Treatment Market

- Adverum Biotechnologies, Inc.

- Alnylam Pharmaceuticals, Inc.

- Applied Genetic Technologies Corporation

- Arrowhead Pharmaceuticals, Inc.

- Carolus Therapeutics, Inc.

- Cevec Pharmaceuticals GmbH

- Dicerna Pharmaceuticals, Inc.

- Digna Biotech, S.L.

- Editas Medicine, Inc.

- Grifols, S.A.

- Inhibrx

- Intellia Therapeutics, Inc.

- International Stem Cell Corporation

- Ionis Pharmaceuticals, Inc.

- Kamada Ltd.

- Polyphor Ltd.

- ProMetic Life Sciences Inc.

- rEVO Biologics, Inc.

- Sangamo BioSciences, Inc.

Notable Milestones in Alpha- Antitrypsin Deficiency Treatment Sector

- 2019: initiation of Phase 1/2 trials for ARO-AAT by Arrowhead Pharmaceuticals, Inc.

- 2020: Approval of Grifols, S.A.'s alpha-1 antitrypsin deficiency augmentation therapy in new markets.

- 2021: Publication of promising preclinical data for gene editing approaches by Editas Medicine, Inc.

- 2022: Advancement of Intellia Therapeutics, Inc.'s gene editing programs targeting liver diseases into clinical studies.

- 2023: Commencement of Phase 1 clinical trials for POL-6014 by Polyphor Ltd.

- 2024: Announcement of significant investment in gene therapy R&D by Alnylam Pharmaceuticals, Inc. for AATD.

- 2025 (Estimated): Expected initiation of Phase 3 trials for key gene therapy candidates.

- 2026 (Projected): Potential for first gene therapy approval for AATD in select regions.

In-Depth Alpha- Antitrypsin Deficiency Treatment Market Outlook

The future outlook for the Alpha-Antitrypsin Deficiency treatment market is exceptionally promising, fueled by ongoing scientific innovation and strategic market expansion. Growth accelerators, including the development of more efficient gene delivery systems and robust clinical trial data, will underpin market expansion. Strategic collaborations between leading biopharmaceutical companies and specialized gene therapy developers will expedite the translation of research into commercially viable treatments. The increasing emphasis on real-world evidence collection and the potential for personalized medicine approaches will further solidify the market's trajectory. As regulatory pathways become more defined and reimbursement landscapes adapt to novel therapeutic modalities, the market is expected to witness sustained and significant growth, offering hope for improved patient outcomes and long-term disease management.

Alpha- Antitrypsin Deficiency Treatment Segmentation

-

1. Application

- 1.1. Clinic

- 1.2. Hospital

- 1.3. Others

-

2. Types

- 2.1. CT-2009

- 2.2. POL-6014

- 2.3. ARO-AAT

- 2.4. ALNAAT-02

- 2.5. Others

Alpha- Antitrypsin Deficiency Treatment Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Alpha- Antitrypsin Deficiency Treatment Regional Market Share

Geographic Coverage of Alpha- Antitrypsin Deficiency Treatment

Alpha- Antitrypsin Deficiency Treatment REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.02% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Alpha- Antitrypsin Deficiency Treatment Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Clinic

- 5.1.2. Hospital

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. CT-2009

- 5.2.2. POL-6014

- 5.2.3. ARO-AAT

- 5.2.4. ALNAAT-02

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Alpha- Antitrypsin Deficiency Treatment Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Clinic

- 6.1.2. Hospital

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. CT-2009

- 6.2.2. POL-6014

- 6.2.3. ARO-AAT

- 6.2.4. ALNAAT-02

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Alpha- Antitrypsin Deficiency Treatment Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Clinic

- 7.1.2. Hospital

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. CT-2009

- 7.2.2. POL-6014

- 7.2.3. ARO-AAT

- 7.2.4. ALNAAT-02

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Alpha- Antitrypsin Deficiency Treatment Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Clinic

- 8.1.2. Hospital

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. CT-2009

- 8.2.2. POL-6014

- 8.2.3. ARO-AAT

- 8.2.4. ALNAAT-02

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Alpha- Antitrypsin Deficiency Treatment Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Clinic

- 9.1.2. Hospital

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. CT-2009

- 9.2.2. POL-6014

- 9.2.3. ARO-AAT

- 9.2.4. ALNAAT-02

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Alpha- Antitrypsin Deficiency Treatment Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Clinic

- 10.1.2. Hospital

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. CT-2009

- 10.2.2. POL-6014

- 10.2.3. ARO-AAT

- 10.2.4. ALNAAT-02

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Adverum Biotechnologies

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Inc.

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Alnylam Pharmaceuticals

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Inc.

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Applied Genetic Technologies Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Arrowhead Pharmaceuticals

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Inc.

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Carolus Therapeutics

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Inc.

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Cevec Pharmaceuticals GmbH

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Dicerna Pharmaceuticals

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Inc.

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Digna Biotech

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 S.L.

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Editas Medicine

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Inc.

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Grifols

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 S.A.

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Inhibrx

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Intellia Therapeutics

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Inc.

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 International Stem Cell Corporation

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Ionis Pharmaceuticals

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Inc.

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Kamada Ltd.

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Polyphor Ltd.

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 ProMetic Life Sciences Inc.

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 rEVO Biologics

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 Inc.

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 Sangamo BioSciences

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.31 Inc.

- 11.2.31.1. Overview

- 11.2.31.2. Products

- 11.2.31.3. SWOT Analysis

- 11.2.31.4. Recent Developments

- 11.2.31.5. Financials (Based on Availability)

- 11.2.1 Adverum Biotechnologies

List of Figures

- Figure 1: Global Alpha- Antitrypsin Deficiency Treatment Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Alpha- Antitrypsin Deficiency Treatment Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Alpha- Antitrypsin Deficiency Treatment Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Alpha- Antitrypsin Deficiency Treatment Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Alpha- Antitrypsin Deficiency Treatment Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Alpha- Antitrypsin Deficiency Treatment?

The projected CAGR is approximately 11.02%.

2. Which companies are prominent players in the Alpha- Antitrypsin Deficiency Treatment?

Key companies in the market include Adverum Biotechnologies, Inc., Alnylam Pharmaceuticals, Inc., Applied Genetic Technologies Corporation, Arrowhead Pharmaceuticals, Inc., Carolus Therapeutics, Inc., Cevec Pharmaceuticals GmbH, Dicerna Pharmaceuticals, Inc., Digna Biotech, S.L., Editas Medicine, Inc., Grifols, S.A., Inhibrx, Intellia Therapeutics, Inc., International Stem Cell Corporation, Ionis Pharmaceuticals, Inc., Kamada Ltd., Polyphor Ltd., ProMetic Life Sciences Inc., rEVO Biologics, Inc., Sangamo BioSciences, Inc..

3. What are the main segments of the Alpha- Antitrypsin Deficiency Treatment?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.84 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Alpha- Antitrypsin Deficiency Treatment," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Alpha- Antitrypsin Deficiency Treatment report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Alpha- Antitrypsin Deficiency Treatment?

To stay informed about further developments, trends, and reports in the Alpha- Antitrypsin Deficiency Treatment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence