Key Insights

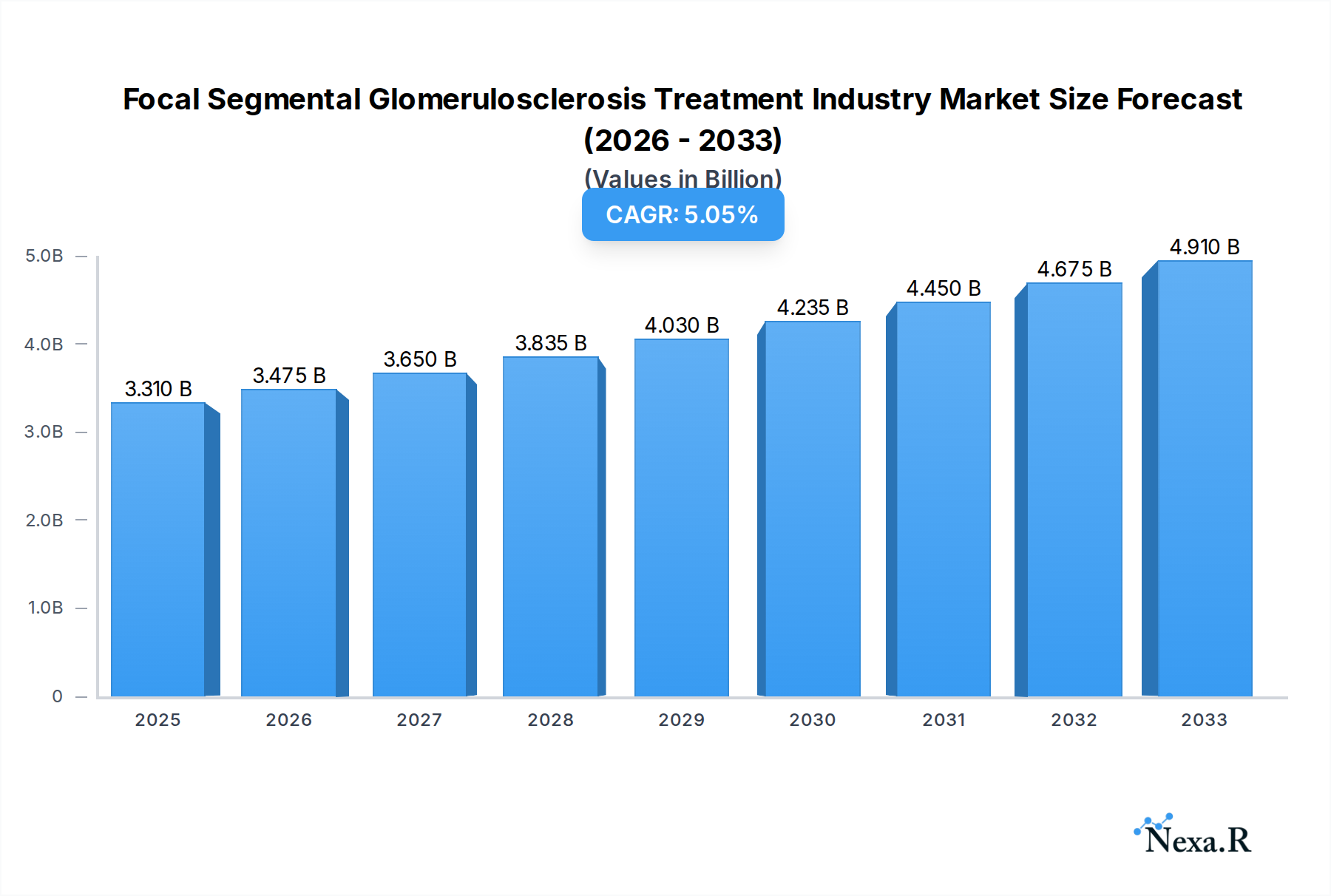

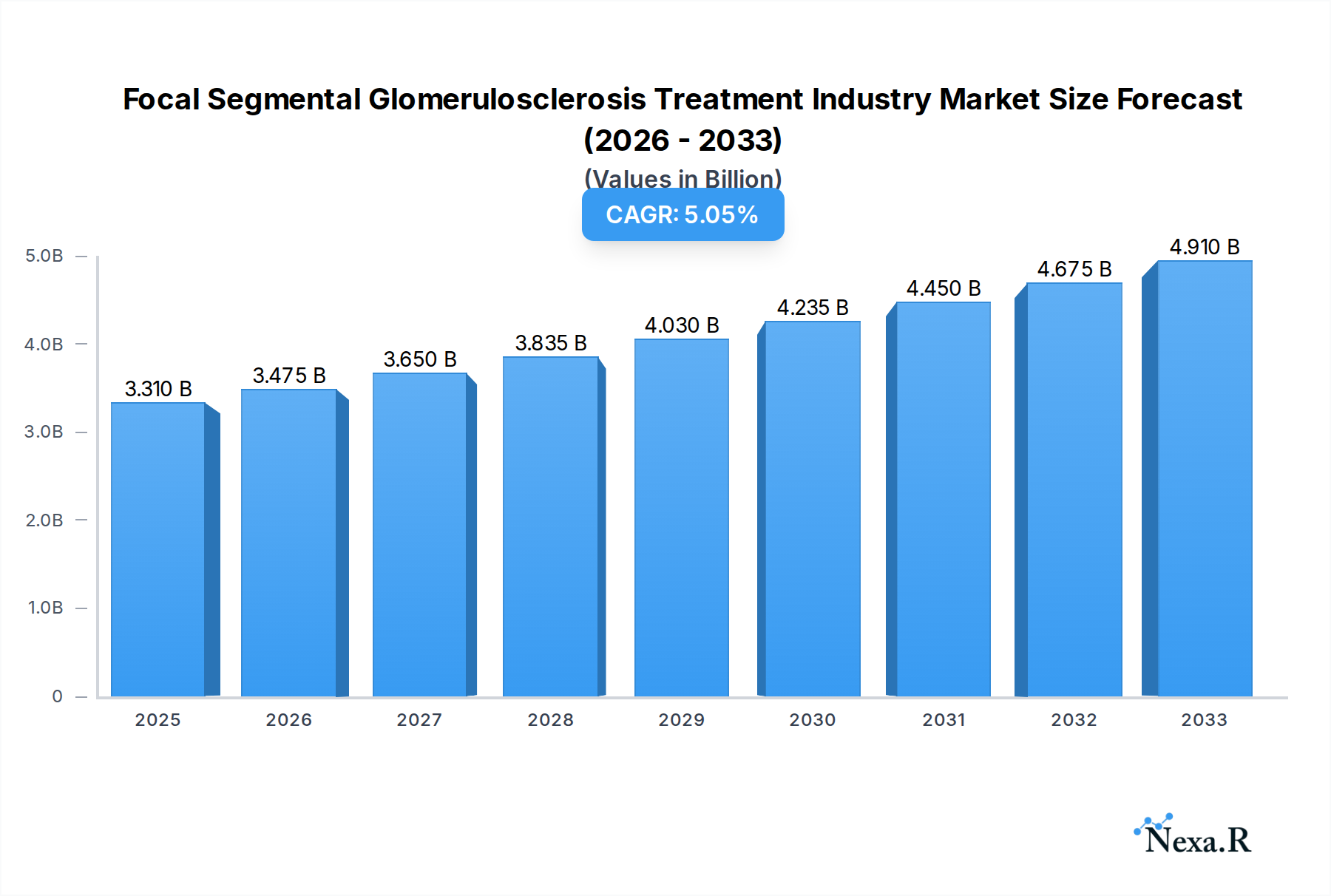

The Focal Segmental Glomerulosclerosis (FSGS) Treatment Market is poised for significant expansion, projected to reach USD 3.31 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 5% anticipated throughout the forecast period of 2025-2033. This growth trajectory is underpinned by a confluence of factors, most notably the increasing prevalence of both primary and secondary FSGS, driven by rising rates of obesity, hypertension, and certain genetic predispositions. Advances in diagnostic tools, leading to earlier and more accurate identification of the disease, coupled with the development of novel therapeutic approaches beyond traditional drug therapy, such as targeted immunotherapies and improved dialysis techniques, are also critical drivers. The market's expansion is further supported by a growing understanding of the underlying pathologies of FSGS, encouraging greater investment in research and development by both established pharmaceutical giants and specialized biotech firms.

Focal Segmental Glomerulosclerosis Treatment Industry Market Size (In Billion)

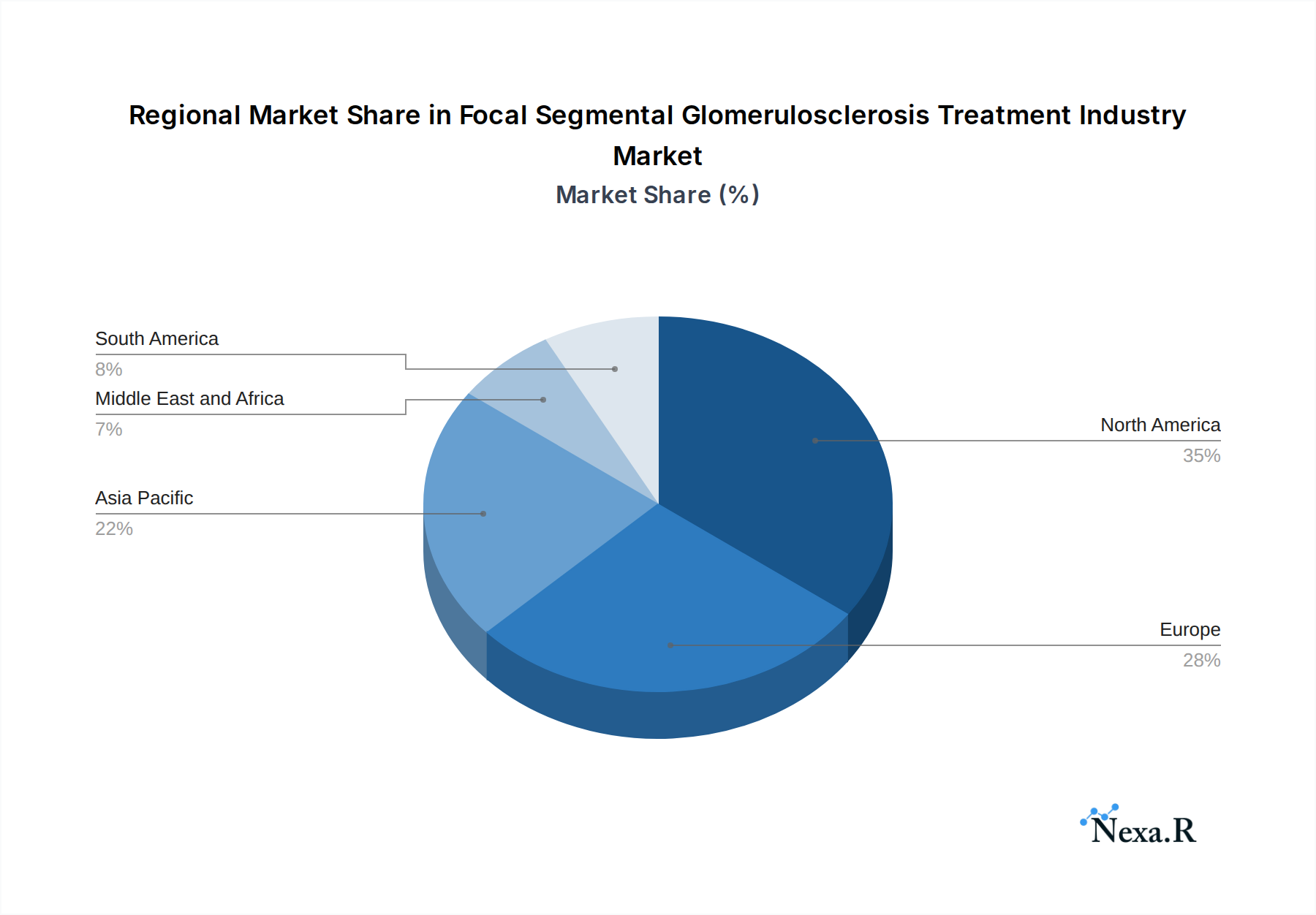

The market's segmentation reveals key areas of focus and opportunity. Disease management, encompassing diagnosis and treatment, forms the core of market activity. Diagnosis, relying on sophisticated methods like kidney biopsies and creatinine tests, is becoming more refined, while treatment options are diversifying. Drug therapy remains a cornerstone, but the increasing reliance on dialysis and the growing demand for kidney transplants highlight the severity of the condition and the need for comprehensive care solutions. Geographically, North America is expected to lead the market, attributed to its advanced healthcare infrastructure, high patient awareness, and significant healthcare expenditure. However, the Asia Pacific region is anticipated to witness the fastest growth, driven by improving healthcare access, a large patient pool, and increasing adoption of advanced treatments. Emerging restraints, such as the high cost of some advanced therapies and challenges in drug development for rare diseases, are being addressed through ongoing research and policy initiatives aimed at improving patient access and affordability.

Focal Segmental Glomerulosclerosis Treatment Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Focal Segmental Glomerulosclerosis (FSGS) Treatment Industry, covering market dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, opportunities, and major players. With a study period from 2019–2033 and a base year of 2025, this report offers critical insights for stakeholders seeking to understand the evolving FSGS treatment market, including the burgeoning pediatric FSGS treatment and adult FSGS treatment segments, as well as advancements in FSGS drug therapy and FSGS transplant options.

Focal Segmental Glomerulosclerosis Treatment Industry Market Dynamics & Structure

The Focal Segmental Glomerulosclerosis (FSGS) treatment market is characterized by a moderate level of concentration, with a few key pharmaceutical giants and specialized biotech firms leading innovation. Technological innovation is a primary driver, focusing on novel therapeutic targets for both primary FSGS and secondary FSGS. Regulatory frameworks, including FDA approvals for new FSGS medications and patient access programs, significantly influence market entry and growth. Competitive product substitutes include existing immunosuppressants and supportive care, but the pursuit of targeted therapies for FSGS is intensifying. End-user demographics are shifting, with increasing recognition of FSGS in both pediatric and adult populations, driving demand for tailored FSGS diagnosis and treatment. Mergers and acquisitions (M&A) are a growing trend, as larger companies seek to acquire promising early-stage FSGS therapies. For instance, the number of strategic partnerships and licensing deals is projected to rise by an estimated 15% in the forecast period. Innovation barriers include the rarity of FSGS, complex disease pathogenesis, and the high cost and lengthy duration of clinical trials for FSGS rare disease treatments.

- Market Concentration: Dominated by a blend of large pharmaceutical companies and emerging biotech firms.

- Technological Innovation Drivers: Focus on precision medicine, targeted therapies, and improved diagnostic tools for FSGS.

- Regulatory Frameworks: FDA, EMA, and other health authorities play a crucial role in drug approval and market access for FSGS treatments.

- Competitive Product Substitutes: Existing immunosuppressants, supportive therapies, and the ongoing development of novel FSGS drugs.

- End-User Demographics: Increasing diagnosis rates in both pediatric and adult populations, driving demand for diverse FSGS treatment approaches.

- M&A Trends: Growing strategic partnerships and acquisitions to leverage innovative FSGS pipelines.

Focal Segmental Glomerulosclerosis Treatment Industry Growth Trends & Insights

The Focal Segmental Glomerulosclerosis (FSGS) Treatment Industry is poised for significant expansion, driven by a confluence of factors including increasing disease awareness, advancements in diagnostic techniques, and the development of novel therapeutic agents. The global market size for FSGS treatment is projected to reach an estimated $15.8 billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of 7.2% during the forecast period. Adoption rates of new FSGS therapies are expected to accelerate as clinical trial data matures and regulatory approvals are secured. Technological disruptions, such as the integration of artificial intelligence in disease diagnosis and drug discovery for FSGS, are set to revolutionize the treatment landscape. Consumer behavior shifts are also influencing the market, with patients and their families actively seeking information and advocating for personalized treatment plans. The prevalence of rare kidney diseases, including FSGS, is a key indicator of future market growth, necessitating greater investment in FSGS research and development. The increasing focus on preserving kidney function and delaying or preventing the need for dialysis and kidney transplantation will further fuel the demand for effective FSGS management strategies. Early diagnosis through improved FSGS screening and access to specialized nephrology care for FSGS will be paramount in optimizing treatment outcomes.

Dominant Regions, Countries, or Segments in Focal Segmental Glomerulosclerosis Treatment Industry

The Focal Segmental Glomerulosclerosis (FSGS) Treatment Industry exhibits distinct regional dominance and growth drivers across various segments. North America, particularly the United States, currently leads the market due to its advanced healthcare infrastructure, substantial investment in R&D for rare kidney diseases, and a high prevalence of diagnosed FSGS cases. Europe follows closely, with countries like Germany and the UK contributing significantly to market growth through strong reimbursement policies and a growing number of clinical trials for FSGS drugs. The Asia Pacific region is emerging as a high-growth area, driven by increasing healthcare expenditure, a rising diagnosis rate for kidney diseases, and government initiatives to improve access to specialized treatments, including FSGS supportive care.

Within disease types, primary FSGS accounts for a larger market share due to its idiopathic nature and the ongoing search for definitive treatments. However, secondary FSGS, often linked to other conditions like obesity or certain viral infections, presents a growing segment as these associated conditions become more prevalent globally.

In terms of disease management, Treatment is the dominant segment. Within treatment modalities, Drug Therapy is experiencing the most rapid growth, fueled by the development of novel immunosuppressants, targeted biologics, and antifibrotic agents for FSGS. While Dialysis and Kidney Transplant remain crucial interventions, the focus is shifting towards therapeutic interventions that can prevent or delay the need for these more invasive procedures. Diagnosis, while a smaller segment in terms of direct revenue, is foundational. Kidney Biopsy remains the gold standard for definitive diagnosis, but advancements in non-invasive diagnostic markers and imaging techniques are gaining traction, promising earlier and more accurate detection of FSGS. The increasing understanding of genetic predispositions is also opening avenues for more precise FSGS diagnostic testing.

Focal Segmental Glomerulosclerosis Treatment Industry Product Landscape

The product landscape in the Focal Segmental Glomerulosclerosis (FSGS) Treatment Industry is rapidly evolving, characterized by a strong emphasis on novel drug therapies and targeted treatments. Key innovations include the development of selective immunosuppressants designed to minimize off-target effects, as well as therapies aimed at addressing the underlying molecular pathways implicated in FSGS pathogenesis, such as podocyte damage and proteinuria. The performance metrics of these new agents are being rigorously evaluated based on their ability to reduce proteinuria, preserve kidney function, and improve patient quality of life. Unique selling propositions often revolve around improved safety profiles, higher efficacy in specific FSGS subtypes, and potential for disease modification rather than just symptomatic relief. Technological advancements are enabling the development of precision medicines, personalized treatment approaches, and potential combination therapies for more effective FSGS patient management.

Key Drivers, Barriers & Challenges in Focal Segmental Glomerulosclerosis Treatment Industry

The Focal Segmental Glomerulosclerosis (FSGS) Treatment Industry is propelled by several key drivers. The increasing incidence and prevalence of FSGS, coupled with a growing understanding of its complex pathophysiology, are significant motivators for research and development. Advances in diagnostic technologies, enabling earlier and more accurate identification of FSGS, are also crucial. Furthermore, the expanding pipeline of novel therapeutic candidates, particularly those targeting specific molecular pathways, is a major growth accelerator. Government initiatives supporting research into rare diseases and the increasing demand for effective treatments that can delay or prevent kidney failure are also playing a vital role.

However, the industry faces considerable barriers and challenges. The rarity of FSGS often leads to high development costs and a limited patient pool for clinical trials, hindering faster drug development. The complex and heterogeneous nature of FSGS, with multiple underlying causes, makes it challenging to develop a one-size-fits-all treatment. Regulatory hurdles for approving novel therapies for rare diseases can be stringent and time-consuming. Supply chain complexities for specialized biological drugs and the high cost of advanced treatments can also pose significant challenges to market access and patient affordability, impacting the cost of FSGS treatment.

Emerging Opportunities in Focal Segmental Glomerulosclerosis Treatment Industry

Emerging opportunities within the Focal Segmental Glomerulosclerosis (FSGS) Treatment Industry are centered around precision medicine and the development of targeted therapies that address the specific underlying causes of FSGS in individual patients. The increasing understanding of genetic and molecular drivers of FSGS presents a significant opportunity for the development of personalized treatment regimens, potentially including gene therapies or advanced cell-based therapies. The unmet need for effective treatments that can halt or reverse kidney damage in FSGS is driving innovation in antifibrotic agents and therapies that protect podocytes. Furthermore, advancements in digital health and remote patient monitoring offer opportunities to improve adherence to treatment and track disease progression more effectively, especially for patients in remote areas or those with limited access to specialized care. The growing emphasis on early diagnosis and preventative strategies for kidney diseases also opens avenues for new diagnostic tools and screening programs tailored for FSGS.

Growth Accelerators in the Focal Segmental Glomerulosclerosis Treatment Industry Industry

Several catalysts are accelerating the growth of the Focal Segmental Glomerulosclerosis (FSGS) Treatment Industry. Technological breakthroughs in genomics and proteomics are enabling a deeper understanding of FSGS subtypes, paving the way for more targeted and effective therapies. Strategic partnerships and collaborations between academic research institutions, biotech startups, and large pharmaceutical companies are fostering innovation and accelerating the drug development process. Market expansion strategies, including the penetration of emerging economies and increased access to healthcare services, are also contributing to sustained growth. The growing awareness of rare kidney diseases among healthcare professionals and the patient community is leading to earlier diagnosis and a greater demand for advanced treatment options, further fueling the industry's expansion. The increasing focus on patient-centric care and the development of therapies that improve quality of life are also powerful growth engines.

Key Players Shaping the Focal Segmental Glomerulosclerosis Treatment Industry Market

- Dimerix Ltd

- ChemoCentryx Inc

- Complexa Inc

- Beckman Coulter Inc (Danaher)

- Medtronic PLC

- Variant Pharmaceuticals Inc

- B Braun Melsungen AG

- Retrophin Inc

- Baxter International Inc

- Pfizer Inc

Notable Milestones in Focal Segmental Glomerulosclerosis Treatment Industry Sector

- February 2022: Goldfinch Bio announced positive preliminary data from a phase 2 clinical trial evaluating gfb-887 as a precision medicine for patients with focal segmental glomerulosclerosis (FSGS). This milestone signifies progress in targeted therapies.

- September 2021: Vifor Pharma and Travere Therapeutics inked a collaboration and licensing partnership to commercialize sparsentan in Europe, Australia, and New Zealand. The drug is being made to treat FSGS and IgAN, which are both rare, progressive kidney diseases that lead to end-stage kidney disease more often than other diseases. This partnership highlights the growing strategic alliances aimed at expanding access to promising FSGS treatments.

In-Depth Focal Segmental Glomerulosclerosis Treatment Industry Market Outlook

The future outlook for the Focal Segmental Glomerulosclerosis (FSGS) Treatment Industry is exceptionally promising, driven by continued innovation and increasing investment. Growth accelerators will be heavily influenced by the successful translation of promising FSGS clinical trial results into approved therapies. The expanding pipeline of targeted treatments, including those addressing specific genetic mutations and molecular pathways, will significantly enhance the efficacy and safety of FSGS management. Strategic partnerships between key players will continue to be instrumental in bringing these novel therapies to market. Furthermore, the growing emphasis on early diagnosis and intervention, facilitated by advancements in diagnostic technologies, will lead to improved patient outcomes and a larger addressable market for effective FSGS treatments. The increasing global burden of kidney diseases and the persistent unmet medical need for better FSGS therapies will ensure sustained demand and investment in this critical sector. The projected market size of $15.8 billion by 2033 underscores the substantial growth potential and the transformative impact of ongoing research and development.

Focal Segmental Glomerulosclerosis Treatment Industry Segmentation

-

1. Disease Type

- 1.1. Primary FSGS

- 1.2. Secondary FSGS

-

2. Disease Management

-

2.1. Diagnosis

- 2.1.1. Kidney Biopsy

- 2.1.2. Creatinine Test

- 2.1.3. Other Diagnoses

-

2.2. Treatment

- 2.2.1. Drug Therapy

- 2.2.2. Dialysis

- 2.2.3. Kidney Transplant

-

2.1. Diagnosis

Focal Segmental Glomerulosclerosis Treatment Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Focal Segmental Glomerulosclerosis Treatment Industry Regional Market Share

Geographic Coverage of Focal Segmental Glomerulosclerosis Treatment Industry

Focal Segmental Glomerulosclerosis Treatment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Disease Type

- 5.1.1. Primary FSGS

- 5.1.2. Secondary FSGS

- 5.2. Market Analysis, Insights and Forecast - by Disease Management

- 5.2.1. Diagnosis

- 5.2.1.1. Kidney Biopsy

- 5.2.1.2. Creatinine Test

- 5.2.1.3. Other Diagnoses

- 5.2.2. Treatment

- 5.2.2.1. Drug Therapy

- 5.2.2.2. Dialysis

- 5.2.2.3. Kidney Transplant

- 5.2.1. Diagnosis

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Disease Type

- 6. Global Focal Segmental Glomerulosclerosis Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Disease Type

- 6.1.1. Primary FSGS

- 6.1.2. Secondary FSGS

- 6.2. Market Analysis, Insights and Forecast - by Disease Management

- 6.2.1. Diagnosis

- 6.2.1.1. Kidney Biopsy

- 6.2.1.2. Creatinine Test

- 6.2.1.3. Other Diagnoses

- 6.2.2. Treatment

- 6.2.2.1. Drug Therapy

- 6.2.2.2. Dialysis

- 6.2.2.3. Kidney Transplant

- 6.2.1. Diagnosis

- 6.1. Market Analysis, Insights and Forecast - by Disease Type

- 7. North America Focal Segmental Glomerulosclerosis Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Disease Type

- 7.1.1. Primary FSGS

- 7.1.2. Secondary FSGS

- 7.2. Market Analysis, Insights and Forecast - by Disease Management

- 7.2.1. Diagnosis

- 7.2.1.1. Kidney Biopsy

- 7.2.1.2. Creatinine Test

- 7.2.1.3. Other Diagnoses

- 7.2.2. Treatment

- 7.2.2.1. Drug Therapy

- 7.2.2.2. Dialysis

- 7.2.2.3. Kidney Transplant

- 7.2.1. Diagnosis

- 7.1. Market Analysis, Insights and Forecast - by Disease Type

- 8. Europe Focal Segmental Glomerulosclerosis Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Disease Type

- 8.1.1. Primary FSGS

- 8.1.2. Secondary FSGS

- 8.2. Market Analysis, Insights and Forecast - by Disease Management

- 8.2.1. Diagnosis

- 8.2.1.1. Kidney Biopsy

- 8.2.1.2. Creatinine Test

- 8.2.1.3. Other Diagnoses

- 8.2.2. Treatment

- 8.2.2.1. Drug Therapy

- 8.2.2.2. Dialysis

- 8.2.2.3. Kidney Transplant

- 8.2.1. Diagnosis

- 8.1. Market Analysis, Insights and Forecast - by Disease Type

- 9. Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Disease Type

- 9.1.1. Primary FSGS

- 9.1.2. Secondary FSGS

- 9.2. Market Analysis, Insights and Forecast - by Disease Management

- 9.2.1. Diagnosis

- 9.2.1.1. Kidney Biopsy

- 9.2.1.2. Creatinine Test

- 9.2.1.3. Other Diagnoses

- 9.2.2. Treatment

- 9.2.2.1. Drug Therapy

- 9.2.2.2. Dialysis

- 9.2.2.3. Kidney Transplant

- 9.2.1. Diagnosis

- 9.1. Market Analysis, Insights and Forecast - by Disease Type

- 10. Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Disease Type

- 10.1.1. Primary FSGS

- 10.1.2. Secondary FSGS

- 10.2. Market Analysis, Insights and Forecast - by Disease Management

- 10.2.1. Diagnosis

- 10.2.1.1. Kidney Biopsy

- 10.2.1.2. Creatinine Test

- 10.2.1.3. Other Diagnoses

- 10.2.2. Treatment

- 10.2.2.1. Drug Therapy

- 10.2.2.2. Dialysis

- 10.2.2.3. Kidney Transplant

- 10.2.1. Diagnosis

- 10.1. Market Analysis, Insights and Forecast - by Disease Type

- 11. South America Focal Segmental Glomerulosclerosis Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Disease Type

- 11.1.1. Primary FSGS

- 11.1.2. Secondary FSGS

- 11.2. Market Analysis, Insights and Forecast - by Disease Management

- 11.2.1. Diagnosis

- 11.2.1.1. Kidney Biopsy

- 11.2.1.2. Creatinine Test

- 11.2.1.3. Other Diagnoses

- 11.2.2. Treatment

- 11.2.2.1. Drug Therapy

- 11.2.2.2. Dialysis

- 11.2.2.3. Kidney Transplant

- 11.2.1. Diagnosis

- 11.1. Market Analysis, Insights and Forecast - by Disease Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Dimerix Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ChemoCentryx Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Complexa Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Beckman Coulter Inc (Danaher)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Medtronic PLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Variant Pharmaceuticals Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 B Braun Melsungen AG

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Retrophin Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Baxter International Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Pfizer Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Dimerix Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Disease Type 2025 & 2033

- Figure 4: North America Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Disease Type 2025 & 2033

- Figure 5: North America Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 6: North America Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Disease Type 2025 & 2033

- Figure 7: North America Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Disease Management 2025 & 2033

- Figure 8: North America Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Disease Management 2025 & 2033

- Figure 9: North America Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Disease Management 2025 & 2033

- Figure 10: North America Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Disease Management 2025 & 2033

- Figure 11: North America Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Disease Type 2025 & 2033

- Figure 16: Europe Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Disease Type 2025 & 2033

- Figure 17: Europe Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 18: Europe Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Disease Type 2025 & 2033

- Figure 19: Europe Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Disease Management 2025 & 2033

- Figure 20: Europe Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Disease Management 2025 & 2033

- Figure 21: Europe Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Disease Management 2025 & 2033

- Figure 22: Europe Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Disease Management 2025 & 2033

- Figure 23: Europe Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Country 2025 & 2033

- Figure 24: Europe Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Disease Type 2025 & 2033

- Figure 28: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Disease Type 2025 & 2033

- Figure 29: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 30: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Disease Type 2025 & 2033

- Figure 31: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Disease Management 2025 & 2033

- Figure 32: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Disease Management 2025 & 2033

- Figure 33: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Disease Management 2025 & 2033

- Figure 34: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Disease Management 2025 & 2033

- Figure 35: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Country 2025 & 2033

- Figure 36: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Disease Type 2025 & 2033

- Figure 40: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Disease Type 2025 & 2033

- Figure 41: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 42: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Disease Type 2025 & 2033

- Figure 43: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Disease Management 2025 & 2033

- Figure 44: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Disease Management 2025 & 2033

- Figure 45: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Disease Management 2025 & 2033

- Figure 46: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Disease Management 2025 & 2033

- Figure 47: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: South America Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Disease Type 2025 & 2033

- Figure 52: South America Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Disease Type 2025 & 2033

- Figure 53: South America Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 54: South America Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Disease Type 2025 & 2033

- Figure 55: South America Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Disease Management 2025 & 2033

- Figure 56: South America Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Disease Management 2025 & 2033

- Figure 57: South America Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Disease Management 2025 & 2033

- Figure 58: South America Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Disease Management 2025 & 2033

- Figure 59: South America Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined), by Country 2025 & 2033

- Figure 60: South America Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: South America Focal Segmental Glomerulosclerosis Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: South America Focal Segmental Glomerulosclerosis Treatment Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 2: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Type 2020 & 2033

- Table 3: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Management 2020 & 2033

- Table 4: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Management 2020 & 2033

- Table 5: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 8: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Type 2020 & 2033

- Table 9: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Management 2020 & 2033

- Table 10: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Management 2020 & 2033

- Table 11: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Mexico Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 20: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Type 2020 & 2033

- Table 21: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Management 2020 & 2033

- Table 22: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Management 2020 & 2033

- Table 23: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Germany Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Germany Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: United Kingdom Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: France Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: France Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Italy Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Italy Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Spain Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: Spain Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Europe Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 38: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Type 2020 & 2033

- Table 39: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Management 2020 & 2033

- Table 40: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Management 2020 & 2033

- Table 41: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 42: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 43: China Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: China Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Japan Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Japan Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: India Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: India Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Australia Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Australia Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: South Korea Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: South Korea Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Rest of Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Asia Pacific Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 56: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Type 2020 & 2033

- Table 57: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Management 2020 & 2033

- Table 58: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Management 2020 & 2033

- Table 59: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: GCC Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: GCC Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: South Africa Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: South Africa Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: Rest of Middle East and Africa Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 67: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Type 2020 & 2033

- Table 68: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Type 2020 & 2033

- Table 69: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Disease Management 2020 & 2033

- Table 70: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Disease Management 2020 & 2033

- Table 71: Global Focal Segmental Glomerulosclerosis Treatment Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 72: Global Focal Segmental Glomerulosclerosis Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 73: Brazil Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 74: Brazil Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Argentina Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 76: Argentina Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Rest of South America Focal Segmental Glomerulosclerosis Treatment Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 78: Rest of South America Focal Segmental Glomerulosclerosis Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Focal Segmental Glomerulosclerosis Treatment Industry?

The projected CAGR is approximately 5%.

2. Which companies are prominent players in the Focal Segmental Glomerulosclerosis Treatment Industry?

Key companies in the market include Dimerix Ltd, ChemoCentryx Inc, Complexa Inc, Beckman Coulter Inc (Danaher), Medtronic PLC, Variant Pharmaceuticals Inc , B Braun Melsungen AG, Retrophin Inc, Baxter International Inc, Pfizer Inc.

3. What are the main segments of the Focal Segmental Glomerulosclerosis Treatment Industry?

The market segments include Disease Type, Disease Management.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Burden of Focal Segmental Glomerulosclerosis (FSGS); High Focus on Developing New Treatment Options4.2.3.

6. What are the notable trends driving market growth?

Primary FSGS Segment is Expected to Witness High Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Cost of Dialysis and Kidney Transplant.

8. Can you provide examples of recent developments in the market?

February 2022: Goldfinch Bio announced positive preliminary data from a phase 2 clinical trial evaluating gfb-887 as a precision medicine for patients with focal segmental glomerulosclerosis (FSGS).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Focal Segmental Glomerulosclerosis Treatment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Focal Segmental Glomerulosclerosis Treatment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Focal Segmental Glomerulosclerosis Treatment Industry?

To stay informed about further developments, trends, and reports in the Focal Segmental Glomerulosclerosis Treatment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence