Key Insights

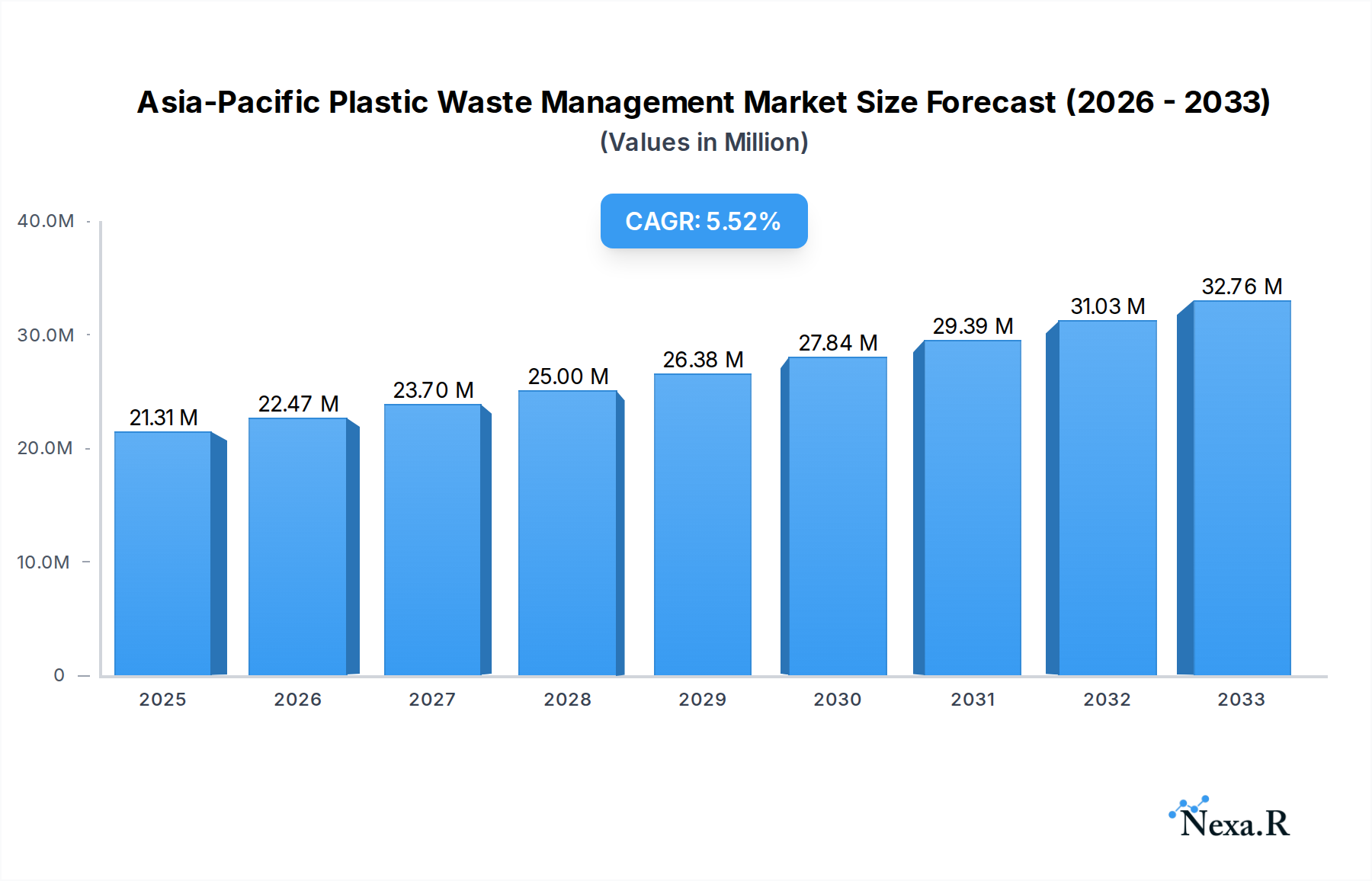

The Asia-Pacific Plastic Waste Management Market is poised for significant expansion, with an estimated market size of 21.31 Million in 2025 and projected to grow at a Compound Annual Growth Rate (CAGR) of 5.45% during the forecast period of 2025-2033. This robust growth is primarily driven by escalating plastic consumption, increasing environmental consciousness, and stringent government regulations aimed at curbing plastic pollution across the region. Key polymer segments like Polyethylene (PE) and Polypropylene (PP) dominate the waste stream due to their widespread use in packaging, textiles, and consumer goods. Residential sources contribute a substantial portion of plastic waste, followed by commercial and industrial sectors. The market is witnessing a strong shift towards advanced recycling and chemical treatment methods, moving away from traditional landfilling, as nations strive for circular economy principles and sustainable waste management solutions. Technological innovations in plastic recycling and the growing adoption of eco-friendly alternatives are also fueling market momentum.

Asia-Pacific Plastic Waste Management Market Market Size (In Million)

Several critical trends are shaping the Asia-Pacific plastic waste management landscape. The burgeoning demand for recycled plastics in manufacturing, driven by both consumer preference and regulatory incentives, is a major catalyst. Furthermore, the establishment of advanced recycling facilities and chemical recycling technologies that can process mixed and contaminated plastics are gaining traction, offering higher recovery rates and better quality recycled materials. Smart waste management solutions, leveraging IoT and AI for efficient collection and sorting, are also being implemented. However, challenges such as the lack of standardized waste collection infrastructure, the high cost of advanced recycling technologies, and public awareness gaps regarding waste segregation persist. Despite these hurdles, the region's commitment to sustainability and the substantial market opportunity presented by effective plastic waste management practices indicate a promising future for the industry.

Asia-Pacific Plastic Waste Management Market Company Market Share

Asia-Pacific Plastic Waste Management Market: A Comprehensive Analysis (2019-2033)

Unlock unparalleled insights into the dynamic Asia-Pacific Plastic Waste Management Market with this definitive report. Analyze growth drivers, emerging trends, and competitive landscapes across key segments and regions. Essential for stakeholders seeking to navigate the evolving challenges and opportunities in sustainable plastic waste solutions. Get detailed market size, CAGR, and forecast values for Polypropylene (PP), Polyethylene (PE), Polyvinyl Chloride (PVC), Terephthalate (PET), and Other Polymers across Residential, Commercial, Industrial, and Other Sources. Understand the impact of Recycling, Chemical Treatment, Landfill, and Other Treatments on the market.

Asia-Pacific Plastic Waste Management Market Market Dynamics & Structure

The Asia-Pacific plastic waste management market is characterized by a moderately concentrated structure, with a blend of large multinational corporations and agile regional players actively vying for market share. Technological innovation is a primary driver, fueled by increasing investments in advanced recycling technologies, waste-to-energy solutions, and smart waste management systems. Regulatory frameworks are becoming increasingly stringent across the region, with governments implementing Extended Producer Responsibility (EPR) schemes, landfill bans, and targets for recycled content, thereby shaping market dynamics. Competitive product substitutes, such as biodegradable plastics and reusable alternatives, are gaining traction but face challenges in terms of cost-effectiveness and scalability for mass adoption. End-user demographics are shifting, with a growing awareness of environmental issues among consumers and increasing corporate sustainability commitments driving demand for responsible waste management practices. Mergers and Acquisitions (M&A) trends indicate a consolidation phase, with companies seeking to expand their geographical reach, technological capabilities, and service offerings. For instance, strategic acquisitions of smaller, innovative waste management startups by larger entities are observed to bolster portfolios and market presence. Barriers to innovation include the high capital expenditure required for advanced recycling infrastructure and the need for standardization in plastic waste collection and sorting processes across diverse national and local contexts.

- Market Concentration: Moderately concentrated with a mix of large corporations and regional players.

- Technological Innovation: Driven by advanced recycling, waste-to-energy, and smart waste management solutions.

- Regulatory Frameworks: Increasing stringency with EPR schemes, landfill bans, and recycled content targets.

- Competitive Substitutes: Biodegradable plastics and reusable alternatives are emerging, but cost and scalability remain challenges.

- End-User Demographics: Growing consumer awareness and corporate sustainability commitments influencing demand.

- M&A Trends: Consolidation through acquisitions of startups by larger entities to expand capabilities and reach.

- Innovation Barriers: High capital expenditure for infrastructure and standardization challenges in waste collection and sorting.

Asia-Pacific Plastic Waste Management Market Growth Trends & Insights

The Asia-Pacific plastic waste management market is projected to witness substantial growth, driven by a confluence of escalating environmental concerns, robust economic development, and supportive government policies. The market size is expected to evolve from approximately USD 45,000 Million in 2025 to reach an estimated USD 78,500 Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 5.7% during the forecast period. Adoption rates for advanced waste management technologies, particularly mechanical and chemical recycling, are on an upward trajectory, propelled by increasing demand for recycled plastics in manufacturing. Technological disruptions are a constant feature, with ongoing advancements in enzymatic recycling, pyrolysis, and gasification promising more efficient and versatile plastic waste conversion methods. Consumer behavior shifts are playing a pivotal role, with a growing preference for products with a lower environmental footprint and a willingness to participate in recycling initiatives. This is further bolstered by enhanced awareness campaigns and the proliferation of collection schemes. The market penetration of formal waste management services is expected to deepen, particularly in developing economies within the region, as infrastructure development accelerates and public-private partnerships become more prevalent. For example, the increasing use of recycled PET (rPET) in the beverage and packaging industries signifies a significant market penetration for recycled materials. The rise of the circular economy model is fundamentally reshaping the industry, moving away from linear 'take-make-dispose' approaches towards closed-loop systems that emphasize resource recovery and waste reduction. This shift is supported by significant investments in research and development for innovative solutions that minimize plastic leakage into the environment and maximize the value extracted from plastic waste. The growing understanding of the health and environmental impacts of plastic pollution is also a critical factor, compelling individuals and corporations alike to seek sustainable alternatives and robust waste management strategies. The increasing adoption of smart bins and IoT-enabled waste tracking systems further contributes to the efficiency and effectiveness of plastic waste management across the region.

Dominant Regions, Countries, or Segments in Asia-Pacific Plastic Waste Management Market

The Asia-Pacific plastic waste management market exhibits significant regional variations, with East Asia emerging as a dominant force, primarily driven by the substantial economic output and stringent environmental regulations of countries like China and Japan. Within East Asia, China stands out as the leading country, accounting for a significant portion of the market share in 2025, estimated at over 35%. This dominance is attributed to its massive industrial base, large population generating vast amounts of plastic waste, and proactive government initiatives aimed at tackling pollution and promoting a circular economy.

- Dominant Region: East Asia

- Leading Country: China

Among the key segments, Polyethylene (PE) and Polypropylene (PP) are the most prevalent polymers, collectively representing over 60% of the total plastic waste generated in the region. This is largely due to their widespread use in packaging, consumer goods, and automotive industries.

- Dominant Polymers: Polyethylene (PE), Polypropylene (PP)

The Commercial and Residential sources are the largest contributors to plastic waste, with the commercial sector's waste often being more diverse and requiring specialized management. However, the sheer volume from residential areas makes it a critical focus for waste management strategies.

- Dominant Sources: Commercial, Residential

In terms of treatment methods, Recycling is the fastest-growing segment, driven by technological advancements and increasing demand for recycled materials. While landfilling still accounts for a significant portion of waste disposal, its share is expected to decline due to regulatory pressures and the promotion of sustainable alternatives. Chemical treatment methods are also gaining traction for challenging plastic waste streams.

- Dominant Treatment: Recycling

Key drivers for dominance in East Asia, particularly China, include:

- Economic Policies: Government incentives and investments in waste management infrastructure and research and development.

- Infrastructure Development: Significant expansion of recycling facilities and waste-to-energy plants.

- Strict Regulations: Implementation of policies like Extended Producer Responsibility (EPR) and bans on single-use plastics.

- Technological Adoption: High adoption rates for advanced sorting and recycling technologies.

- Market Demand for Recycled Content: Growing pressure from downstream industries to incorporate recycled plastics into their products.

- Urbanization: Rapid urbanization leading to increased waste generation and the need for efficient waste management systems.

The growth potential in this region remains high, fueled by ongoing urbanization, industrial expansion, and a continuous push towards achieving ambitious sustainability targets. The focus on innovation in recycling technologies and the development of a robust circular economy are expected to further solidify East Asia's leadership in the plastic waste management market.

Asia-Pacific Plastic Waste Management Market Product Landscape

The product landscape within the Asia-Pacific plastic waste management market is evolving rapidly, driven by innovations aimed at enhancing efficiency, sustainability, and economic viability. Key product developments include advanced sorting equipment utilizing AI and machine learning for precise material identification, and innovative chemical recycling technologies like pyrolysis and depolymerization that can break down mixed plastic waste into valuable chemical feedstocks. High-performance recycling machinery capable of handling diverse plastic types and improving yield is also a significant focus. Application areas are expanding beyond traditional packaging and textiles to include construction materials, automotive components, and even 3D printing filaments derived from recycled plastics. Unique selling propositions often revolve around achieving higher purity rates of recycled materials, reducing the energy footprint of the recycling process, and offering cost-effective solutions that compete favorably with virgin plastic production. Technological advancements are also seen in waste-to-energy solutions, with more efficient combustion and emission control systems being developed.

Key Drivers, Barriers & Challenges in Asia-Pacific Plastic Waste Management Market

Key Drivers:

The Asia-Pacific plastic waste management market is propelled by a multifaceted set of drivers. Foremost is the escalating global and regional concern over plastic pollution, leading to increased public pressure and governmental mandates. Stringent environmental regulations, including Extended Producer Responsibility (EPR) schemes and targets for recycled content, are compelling businesses to invest in sustainable practices. Rapid urbanization and industrialization across the region contribute to increased plastic waste generation, creating a consistent demand for effective management solutions. Furthermore, technological advancements in recycling and waste-to-energy are making these processes more economically viable and environmentally sound. The growing corporate commitment to sustainability and the adoption of circular economy principles are also significant catalysts, driving investment and innovation.

Barriers & Challenges:

Despite the growth drivers, the market faces considerable barriers and challenges. The sheer volume and diversity of plastic waste streams in the region pose significant logistical and operational hurdles for collection and sorting. The high capital investment required for advanced recycling infrastructure and waste-to-energy plants remains a major constraint, particularly for smaller economies and businesses. Inconsistent regulatory frameworks across different countries and sub-regions can create complexity and hinder cross-border collaboration. Supply chain issues, including price volatility of recycled plastics and the availability of consistent feedstock, can impact the economic feasibility of recycling operations. Finally, consumer awareness and participation in waste segregation and recycling programs, while improving, still require further enhancement to maximize the effectiveness of waste management systems. Competitive pressures from virgin plastic producers, often benefiting from lower production costs, also present a challenge to the widespread adoption of recycled materials.

Emerging Opportunities in Asia-Pacific Plastic Waste Management Market

Emerging opportunities in the Asia-Pacific plastic waste management market are centered around innovation and untapped potential. The growing demand for high-quality recycled plastics in niche applications, such as food-grade packaging and specialized industrial components, presents a significant opportunity for advanced recycling technologies that can achieve superior purity levels. The development of innovative business models, such as product-as-a-service for waste management solutions and digital platforms connecting waste generators with recyclers, is poised to streamline operations and create new revenue streams. Furthermore, the increasing focus on addressing plastic leakage into marine environments is opening doors for specialized technologies and initiatives targeting ocean-bound plastic. Untapped markets in developing nations within Southeast Asia and the Pacific islands, where formal waste management infrastructure is still nascent, offer substantial growth potential for scalable and cost-effective solutions. Evolving consumer preferences for sustainable products also create opportunities for companies offering closed-loop systems and visible environmental impact reporting.

Growth Accelerators in the Asia-Pacific Plastic Waste Management Market Industry

Several key catalysts are accelerating the growth of the Asia-Pacific plastic waste management industry. Technological breakthroughs in chemical recycling, such as improved catalysts and energy-efficient processes, are enhancing the ability to process a wider range of plastic types, including mixed and contaminated plastics that were previously difficult to recycle. Strategic partnerships between waste management companies, material manufacturers, and brands are crucial for establishing robust circular supply chains and driving demand for recycled content. These collaborations often involve co-investment in new facilities and the development of standardized quality specifications for recycled materials. Market expansion strategies, including geographical diversification into rapidly developing economies and the offering of integrated waste management services, are also significant growth accelerators. The increasing integration of digital technologies, such as AI-powered sorting robots and blockchain for waste traceability, is improving operational efficiency and transparency, further boosting investor confidence and market growth.

Key Players Shaping the Asia-Pacific Plastic Waste Management Market Market

- Hitachi Zosen Corporation

- Polimaster

- Banyan Nation

- Lucro

- Recity

- SUEZ

- Waste Management Inc

- Cleanaway Waste Management Limited

- Plastic Bank

- Agilyx

- GreenTech Environmental Co Ltd

Notable Milestones in Asia-Pacific Plastic Waste Management Market Sector

- April 2024: A new initiative, "Mapping Plastic Litter in Mekong Countries and Proposing Innovative Waste Management Solutions," was introduced to combat Southeast Asia's escalating plastic pollution crisis. The project's primary goal is to chart and diminish the volume of plastic waste entering the waterways of the Mekong countries, focusing on four pilot cities: Bangkok (Thailand), Vientiane (Lao PDR), Battambang (Cambodia), and Can Tho (Vietnam). This initiative highlights a regional focus on addressing transboundary plastic pollution and fostering collaborative solutions.

- March 2023: The World Bank's Board of Executives approved a USD 250 million IBRD loan. This funding aims to combat plastic pollution from municipal solid waste and agricultural plastic film in rural regions of China's Shaanxi Province. It also seeks to enhance the province's plastic waste management practices to set a blueprint for national-level initiatives. This milestone underscores significant financial backing for large-scale waste management reforms in key regional economies.

In-Depth Asia-Pacific Plastic Waste Management Market Market Outlook

The future outlook for the Asia-Pacific plastic waste management market is exceptionally positive, driven by the sustained momentum of sustainability initiatives and technological advancements. Growth accelerators, including breakthroughs in chemical recycling and the establishment of robust public-private partnerships, will continue to expand the capacity and efficiency of waste management systems. The increasing adoption of circular economy principles is set to redefine the industry, fostering innovation in product design and material utilization. Strategic investments in infrastructure, particularly in emerging economies, will create new market opportunities and improve accessibility to waste management services. The growing consumer and corporate demand for environmentally responsible solutions will further propel market expansion. Overall, the market is poised for significant growth, presenting substantial opportunities for stakeholders committed to sustainable plastic waste management and the transition towards a circular economy.

Asia-Pacific Plastic Waste Management Market Segmentation

-

1. Polymer

- 1.1. Polypropylene (PP)

- 1.2. Polyethylene (PE)

- 1.3. Polyvinyl Chloride (PVC)

- 1.4. Terephthalate (PET)

- 1.5. Other Polymers

-

2. Source

- 2.1. Residential

- 2.2. Commercial

- 2.3. Industrial

- 2.4. Other Sources (Construction, Healthcare, etc.)

-

3. Treatment

- 3.1. Recycling

- 3.2. Chemical Treatment

- 3.3. Landfill

- 3.4. Other Treatments

Asia-Pacific Plastic Waste Management Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia-Pacific Plastic Waste Management Market Regional Market Share

Geographic Coverage of Asia-Pacific Plastic Waste Management Market

Asia-Pacific Plastic Waste Management Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.45% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Polymer

- 5.1.1. Polypropylene (PP)

- 5.1.2. Polyethylene (PE)

- 5.1.3. Polyvinyl Chloride (PVC)

- 5.1.4. Terephthalate (PET)

- 5.1.5. Other Polymers

- 5.2. Market Analysis, Insights and Forecast - by Source

- 5.2.1. Residential

- 5.2.2. Commercial

- 5.2.3. Industrial

- 5.2.4. Other Sources (Construction, Healthcare, etc.)

- 5.3. Market Analysis, Insights and Forecast - by Treatment

- 5.3.1. Recycling

- 5.3.2. Chemical Treatment

- 5.3.3. Landfill

- 5.3.4. Other Treatments

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Polymer

- 6. Asia-Pacific Plastic Waste Management Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Polymer

- 6.1.1. Polypropylene (PP)

- 6.1.2. Polyethylene (PE)

- 6.1.3. Polyvinyl Chloride (PVC)

- 6.1.4. Terephthalate (PET)

- 6.1.5. Other Polymers

- 6.2. Market Analysis, Insights and Forecast - by Source

- 6.2.1. Residential

- 6.2.2. Commercial

- 6.2.3. Industrial

- 6.2.4. Other Sources (Construction, Healthcare, etc.)

- 6.3. Market Analysis, Insights and Forecast - by Treatment

- 6.3.1. Recycling

- 6.3.2. Chemical Treatment

- 6.3.3. Landfill

- 6.3.4. Other Treatments

- 6.1. Market Analysis, Insights and Forecast - by Polymer

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Hitachi Zosen Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Polimaster

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Banyan Nation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Lucro

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Recity

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 SUEZ

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Waste Management Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Cleanaway Waste Management Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Plastic Bank

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Agilyx

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 GreenTech Environmental Co Ltd*List Not Exhaustive

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Hitachi Zosen Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Plastic Waste Management Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Plastic Waste Management Market Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Plastic Waste Management Market Revenue Million Forecast, by Polymer 2020 & 2033

- Table 2: Asia-Pacific Plastic Waste Management Market Volume Billion Forecast, by Polymer 2020 & 2033

- Table 3: Asia-Pacific Plastic Waste Management Market Revenue Million Forecast, by Source 2020 & 2033

- Table 4: Asia-Pacific Plastic Waste Management Market Volume Billion Forecast, by Source 2020 & 2033

- Table 5: Asia-Pacific Plastic Waste Management Market Revenue Million Forecast, by Treatment 2020 & 2033

- Table 6: Asia-Pacific Plastic Waste Management Market Volume Billion Forecast, by Treatment 2020 & 2033

- Table 7: Asia-Pacific Plastic Waste Management Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Asia-Pacific Plastic Waste Management Market Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Asia-Pacific Plastic Waste Management Market Revenue Million Forecast, by Polymer 2020 & 2033

- Table 10: Asia-Pacific Plastic Waste Management Market Volume Billion Forecast, by Polymer 2020 & 2033

- Table 11: Asia-Pacific Plastic Waste Management Market Revenue Million Forecast, by Source 2020 & 2033

- Table 12: Asia-Pacific Plastic Waste Management Market Volume Billion Forecast, by Source 2020 & 2033

- Table 13: Asia-Pacific Plastic Waste Management Market Revenue Million Forecast, by Treatment 2020 & 2033

- Table 14: Asia-Pacific Plastic Waste Management Market Volume Billion Forecast, by Treatment 2020 & 2033

- Table 15: Asia-Pacific Plastic Waste Management Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia-Pacific Plastic Waste Management Market Volume Billion Forecast, by Country 2020 & 2033

- Table 17: China Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: China Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 19: Japan Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Japan Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 21: South Korea Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: South Korea Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 23: India Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Australia Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 27: New Zealand Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: New Zealand Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 29: Indonesia Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Indonesia Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 31: Malaysia Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Malaysia Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 33: Singapore Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Singapore Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 35: Thailand Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Thailand Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 37: Vietnam Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Vietnam Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 39: Philippines Asia-Pacific Plastic Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Philippines Asia-Pacific Plastic Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Plastic Waste Management Market?

The projected CAGR is approximately 5.45%.

2. Which companies are prominent players in the Asia-Pacific Plastic Waste Management Market?

Key companies in the market include Hitachi Zosen Corporation, Polimaster, Banyan Nation, Lucro, Recity, SUEZ, Waste Management Inc, Cleanaway Waste Management Limited, Plastic Bank, Agilyx, GreenTech Environmental Co Ltd*List Not Exhaustive.

3. What are the main segments of the Asia-Pacific Plastic Waste Management Market?

The market segments include Polymer, Source, Treatment.

4. Can you provide details about the market size?

The market size is estimated to be USD 21.31 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Plastic Consumption; Stricter Regulations and Policies Aimed at Reducing Plastic Waste.

6. What are the notable trends driving market growth?

Rapid Urbanization Exacerbates Escalating Plastic Predicament in Asia-Pacific.

7. Are there any restraints impacting market growth?

Increasing Plastic Consumption; Stricter Regulations and Policies Aimed at Reducing Plastic Waste.

8. Can you provide examples of recent developments in the market?

April 2024: A new initiative, "Mapping Plastic Litter in Mekong Countries and Proposing Innovative Waste Management Solutions," was introduced to combat Southeast Asia's escalating plastic pollution crisis. The project's primary goal is to chart and diminish the volume of plastic waste entering the waterways of the Mekong countries, focusing on four pilot cities: Bangkok (Thailand), Vientiane (Lao PDR), Battambang (Cambodia), and Can Tho (Vietnam).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Plastic Waste Management Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Plastic Waste Management Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Plastic Waste Management Market?

To stay informed about further developments, trends, and reports in the Asia-Pacific Plastic Waste Management Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence