Key Insights

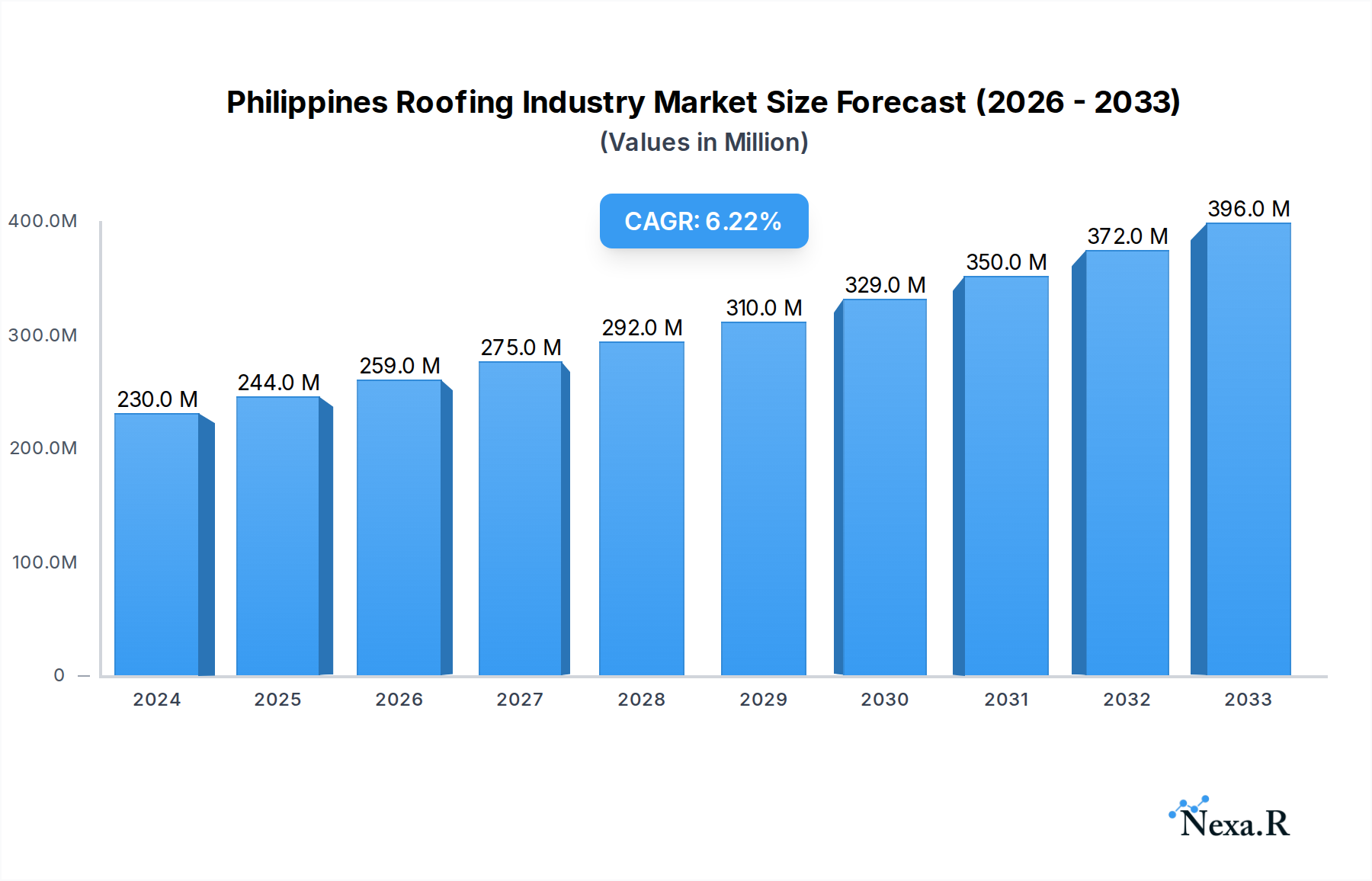

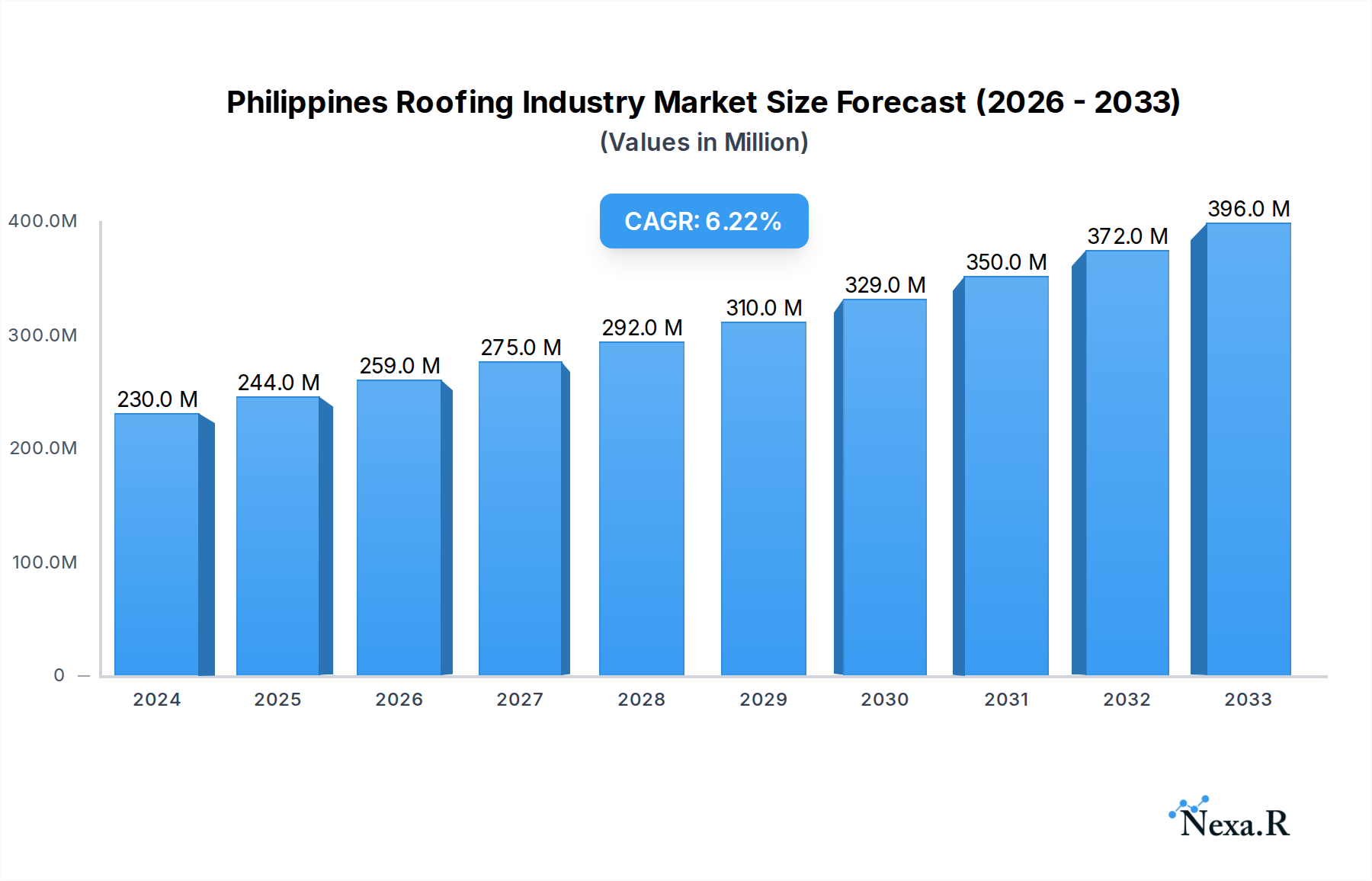

The Philippines roofing industry is poised for substantial growth, driven by increasing construction activities and a growing demand for durable and aesthetically pleasing roofing solutions. With a current estimated market size of USD 230 million in 2024, the sector is projected to expand at a robust Compound Annual Growth Rate (CAGR) of 6.1% from 2025 to 2033. This upward trajectory is fueled by several key factors. The residential sector, in particular, is experiencing a surge due to urbanization, a growing middle class with higher disposable incomes, and a need for home improvements and new constructions. Similarly, the non-residential segment, encompassing commercial buildings, industrial facilities, and infrastructure projects, also contributes significantly to market expansion, supported by government investments in development and private sector expansion. The increasing adoption of metal roofing and advanced asphalt shingles, known for their longevity, weather resistance, and aesthetic appeal, further propels market demand.

Philippines Roofing Industry Market Size (In Million)

Emerging trends such as the focus on sustainable and energy-efficient roofing materials, coupled with advancements in manufacturing technologies, are shaping the competitive landscape. While the market presents significant opportunities, certain restraints need to be considered. Fluctuations in raw material prices, particularly for steel and asphalt, can impact profitability. Furthermore, the availability of skilled labor for installation and the upfront cost of premium roofing materials can pose challenges. Despite these hurdles, the overall outlook for the Philippines roofing industry remains highly positive. Key players like Jacinto Color Steel Inc., Metalink, and Philsteel Holdings Corporation are continuously innovating and expanding their product portfolios to cater to diverse consumer needs and capitalize on the burgeoning market potential. The demand for roofing solutions across various product types, including asphalt shingles, tile roofing, and metal roofing, is expected to grow steadily, reflecting the dynamic and evolving nature of the construction sector in the Philippines.

Philippines Roofing Industry Company Market Share

Philippines Roofing Industry Market Dynamics & Structure

The Philippines roofing industry exhibits a moderately concentrated market structure, with a blend of large established players and a significant number of smaller, regional manufacturers. Technological innovation is primarily driven by the demand for more durable, energy-efficient, and aesthetically pleasing roofing solutions. Government regulations, particularly those related to building codes and environmental standards, play a crucial role in shaping market entry and product development. Competitive product substitutes, such as advanced composite materials and innovative waterproofing systems, continuously challenge traditional offerings. End-user demographics are shifting, with a growing middle class and increased urbanization driving demand for both residential and commercial roofing. Mergers and acquisitions (M&A) are becoming more prevalent as larger companies seek to consolidate market share and expand their product portfolios.

- Market Concentration: Dominated by a few key players, but with significant presence of SMEs.

- Technological Drivers: Focus on sustainability, energy efficiency, and enhanced durability.

- Regulatory Impact: Building codes, environmental policies, and safety standards influence product adoption.

- Product Substitutes: Competition from advanced materials and integrated roofing systems.

- End-User Demographics: Growth in middle-income households and increasing commercial development.

- M&A Trends: Consolidation to enhance scale, market reach, and innovation capabilities.

Philippines Roofing Industry Growth Trends & Insights

The Philippines roofing industry is poised for significant growth, driven by robust construction activity and increasing consumer awareness of quality roofing solutions. The market size is projected to witness a substantial expansion from approximately $2,500 million in 2023 to an estimated $3,900 million by 2033, reflecting a Compound Annual Growth Rate (CAGR) of roughly 4.4% during the forecast period of 2025–2033. Adoption rates of modern roofing materials, such as metal roofing and advanced asphalt shingles, are steadily increasing, fueled by their superior performance characteristics, longevity, and aesthetic appeal. Technological disruptions are emerging in the form of solar-integrated roofing systems and smart roofing solutions designed for energy management and climate control, although their market penetration remains relatively low. Consumer behavior shifts are characterized by a greater emphasis on long-term investment, prioritizing durability, low maintenance, and energy savings over initial cost. The residential sector, in particular, is witnessing a demand for roofing that offers better insulation against the tropical climate and provides protection against frequent typhoons. The non-residential segment, encompassing commercial buildings, industrial facilities, and infrastructure projects, also contributes significantly to market growth, driven by ongoing development and the need for robust, long-lasting roofing. Government initiatives promoting sustainable construction and housing development further bolster market expansion, creating a favorable environment for innovation and investment in the Philippines roofing sector. The base year of 2025 sets a crucial benchmark for understanding the industry's trajectory, with historical data from 2019–2024 providing a foundation for accurate forecasting. The estimated year of 2025 allows for immediate insights into the current market landscape.

Dominant Regions, Countries, or Segments in Philippines Roofing Industry

Metal Roofing is the undisputed leader within the Philippines roofing industry's product type segmentation, consistently capturing a dominant market share estimated to be around 55% of the total roofing market value. This dominance is fueled by several key factors. Its inherent durability, resistance to extreme weather conditions including typhoons and heavy rainfall, and long lifespan make it an exceptionally attractive option for the Philippine climate. Furthermore, the versatility in design, color options, and finishes available in metal roofing allows it to cater to diverse architectural styles, from modern residential homes to large-scale industrial complexes. The increasing availability of technologically advanced metal roofing products, such as those with enhanced insulation properties and anti-corrosion coatings, further solidifies its market position.

The Residential end-user industry segment is another significant driver of market growth, accounting for approximately 60% of the total roofing market value. This dominance is primarily attributed to the large and growing population of the Philippines, coupled with a rising middle class that is increasingly investing in new home constructions and renovations. The demand for safe, comfortable, and aesthetically pleasing homes translates directly into a strong need for reliable roofing solutions. Government initiatives aimed at promoting affordable housing and providing housing loans also contribute to the sustained demand in this segment.

Metal Roofing Dominance:

- Superior Durability & Weather Resistance: Ideal for typhoon-prone regions and tropical climates.

- Long Lifespan & Low Maintenance: Offers cost-effectiveness over the product's lifecycle.

- Aesthetic Versatility: Wide range of designs, colors, and finishes to suit various architectural needs.

- Technological Advancements: Innovations in insulation, corrosion resistance, and reflective coatings enhance appeal.

- Government Support: Policies promoting infrastructure and housing development indirectly boost metal roofing demand.

Residential End-User Industry Dominance:

- Large & Growing Population: Consistent demand for new housing units.

- Rising Middle Class: Increased disposable income for homeownership and renovations.

- Housing Initiatives: Government programs and financial schemes for affordable housing.

- Consumer Preference: Growing awareness of the importance of quality and durable roofing for home protection.

- Urbanization: Expanding urban areas necessitate new residential constructions.

While Tile Roofing holds a significant share, estimated at 25%, and Asphalt Shingles are gaining traction, especially in specific housing developments, their growth is outpaced by the consistent demand and technological advancements in metal roofing. Other Product Types, encompassing a variety of specialized materials, represent a smaller but growing niche. The Non-residential segment, including commercial and industrial buildings, contributes around 40% to the market value, driven by significant infrastructure projects and commercial property development, but the sheer volume of individual residential units still positions the residential sector as the larger contributor to overall roofing market demand.

Philippines Roofing Industry Product Landscape

The Philippines roofing industry is characterized by a dynamic product landscape, with manufacturers continuously innovating to meet evolving consumer needs and environmental demands. Metal roofing, including standing seam, corrugated, and concealed fastener systems, leads in terms of market penetration due to its exceptional durability, weather resistance, and longevity, with products offering warranties of up to 50 years. Tile roofing, both clay and concrete variants, remains popular for its aesthetic appeal and fire resistance, with advancements focusing on lighter-weight designs and improved water-shedding capabilities. Asphalt shingles, while a more traditional option, are seeing innovation in enhanced UV resistance and granular technology for improved performance in the tropical climate. Emerging product types include advanced composite roofing materials, offering a blend of sustainability and performance, and innovative cool roofing solutions designed to reflect solar heat, reducing building energy consumption.

Key Drivers, Barriers & Challenges in Philippines Roofing Industry

The Philippines roofing industry is propelled by several key drivers. The robust growth in construction and infrastructure development, fueled by government spending and foreign direct investment, is a primary catalyst. Increasing disposable incomes and a growing middle class are driving demand for new residential constructions and home renovations. Technological advancements leading to more durable, energy-efficient, and aesthetically pleasing roofing solutions also encourage adoption. Furthermore, government regulations promoting sustainable building practices and stricter building codes necessitate the use of higher-quality roofing materials.

However, the industry faces significant barriers and challenges. The volatile prices of raw materials, particularly steel and bitumen, can impact profitability and pricing strategies. Intense competition among a large number of manufacturers, including both local and international players, can lead to price wars and squeezed profit margins. Supply chain disruptions, exacerbated by logistical challenges in an archipelagic nation, can affect the timely delivery of materials and finished products. Furthermore, a lack of skilled labor for installation and maintenance can hinder the adoption of more complex roofing systems.

Key Drivers:

- Robust Construction Activity: Driven by infrastructure projects and private sector investment.

- Growing Middle Class & Disposable Income: Fuels demand for new housing and renovations.

- Technological Innovations: Enhanced durability, energy efficiency, and aesthetics.

- Stringent Building Codes & Sustainability Standards: Encouraging adoption of quality materials.

Barriers & Challenges:

- Raw Material Price Volatility: Fluctuations in steel, bitumen, and other key inputs.

- Intense Market Competition: Price pressures and margin erosion.

- Supply Chain & Logistics Issues: Archipelagic nature of the Philippines.

- Skilled Labor Shortages: Affecting installation and maintenance quality.

- Economic Downturns: Potential to dampen construction activity.

Emerging Opportunities in Philippines Roofing Industry

Emerging opportunities in the Philippines roofing industry lie in the growing demand for sustainable and energy-efficient solutions. The development and adoption of cool roofing technologies, which reduce heat island effects and lower energy consumption, present a significant avenue for growth, especially in urban centers. The integration of solar panels into roofing systems, creating building-integrated photovoltaics (BIPV), is another promising area, aligning with the Philippines' focus on renewable energy. The expansion of the construction sector into previously underserved rural areas also offers untapped market potential. Furthermore, the increasing awareness and adoption of advanced composite materials that mimic natural aesthetics while offering superior performance and environmental benefits are creating new market niches.

Growth Accelerators in the Philippines Roofing Industry Industry

Several growth accelerators are poised to propel the Philippines roofing industry forward. Government initiatives focused on promoting disaster-resilient infrastructure and affordable housing will continue to be a major catalyst. The increasing adoption of advanced manufacturing technologies, such as automated production lines and digital design tools, will enhance efficiency and product quality. Strategic partnerships between material suppliers, manufacturers, and construction companies can streamline the supply chain and foster innovation. Furthermore, the growing emphasis on green building certifications and sustainable construction practices will drive demand for eco-friendly roofing solutions, creating a competitive advantage for companies offering such products.

Key Players Shaping the Philippines Roofing Industry Market

- Jacinto Color Steel Inc

- Metalink

- Sheehan Inc

- Onduline

- Colorsteel Systems Corporation

- Sanlex Roofmaster Center Co Inc

- DN Steel

- Puyat Steel Corporation

- TERREAL

- Alpha Pro Steel Makers

- Marusugi Co Ltd

- BP Canada

- Union Galvasteel Corporation

- Philsteel Holdings Corporation

*List Not Exhaustive

Notable Milestones in Philippines Roofing Industry Sector

- 2019: Introduction of stricter building codes mandating higher wind resistance for roofing materials, boosting demand for metal roofing.

- 2020: Increased focus on home improvement and renovation due to pandemic-related lockdowns, leading to a surge in residential roofing projects.

- 2021: Launch of several new product lines emphasizing recycled content and energy-saving features by leading manufacturers.

- 2022: Significant investments in new manufacturing facilities by key players to meet growing demand and improve production efficiency.

- 2023: Growing interest and initial adoption of integrated solar roofing solutions in commercial and high-end residential projects.

- 2024: Enhanced government support for disaster-resilient construction, further solidifying the market for durable roofing materials.

In-Depth Philippines Roofing Industry Market Outlook

The Philippines roofing industry is set for a dynamic and expansive future, driven by a confluence of strong economic fundamentals and evolving consumer preferences. The sustained growth in construction, coupled with government-driven infrastructure development and a burgeoning middle class, will continue to fuel demand across both residential and non-residential segments. Innovations in sustainable materials, energy-efficient designs, and integrated smart roofing technologies are poised to redefine market standards, offering significant opportunities for forward-thinking companies. The increasing awareness of climate change and the need for resilient structures against natural disasters will further solidify the market for high-performance, long-lasting roofing solutions. Strategic partnerships, technological advancements in manufacturing, and a continued focus on product quality and durability will be key to capitalizing on the immense growth potential projected for the coming years.

Philippines Roofing Industry Segmentation

-

1. Product Type

- 1.1. Asphalt Shingles

- 1.2. Tile Roofing

- 1.3. Metal Roofing

- 1.4. Other Product Types

-

2. End-user Industry

- 2.1. Residential

- 2.2. Non-residential

Philippines Roofing Industry Segmentation By Geography

- 1. Philippines

Philippines Roofing Industry Regional Market Share

Geographic Coverage of Philippines Roofing Industry

Philippines Roofing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Asphalt Shingles

- 5.1.2. Tile Roofing

- 5.1.3. Metal Roofing

- 5.1.4. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Residential

- 5.2.2. Non-residential

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Philippines

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Philippines Roofing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Asphalt Shingles

- 6.1.2. Tile Roofing

- 6.1.3. Metal Roofing

- 6.1.4. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Residential

- 6.2.2. Non-residential

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Jacinto Color Steel Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Metalink

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Sheehan Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Onduline

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Colorsteel Systems Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Sanlex Roofmaster Center Co Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 DN Steel

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Puyat Steel Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 TERREAL

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Alpha Pro Steel Makers

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Marusugi Co Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 BP Canada

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Union Galvasteel Corporation*List Not Exhaustive

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Philsteel Holdings Corporation

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.1 Jacinto Color Steel Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Philippines Roofing Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Philippines Roofing Industry Share (%) by Company 2025

List of Tables

- Table 1: Philippines Roofing Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 2: Philippines Roofing Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 3: Philippines Roofing Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Philippines Roofing Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 5: Philippines Roofing Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 6: Philippines Roofing Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Philippines Roofing Industry?

The projected CAGR is approximately 6.1%.

2. Which companies are prominent players in the Philippines Roofing Industry?

Key companies in the market include Jacinto Color Steel Inc, Metalink, Sheehan Inc, Onduline, Colorsteel Systems Corporation, Sanlex Roofmaster Center Co Inc, DN Steel, Puyat Steel Corporation, TERREAL, Alpha Pro Steel Makers, Marusugi Co Ltd, BP Canada, Union Galvasteel Corporation*List Not Exhaustive, Philsteel Holdings Corporation.

3. What are the main segments of the Philippines Roofing Industry?

The market segments include Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 230 million as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Construction Activities in the Country; Gain in the Trend of Green Buildings.

6. What are the notable trends driving market growth?

Metal Roofing to Dominate the Market.

7. Are there any restraints impacting market growth?

; Unfavorable Conditions Arising due to the Impact of COVID-19; Other Restraints.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Philippines Roofing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Philippines Roofing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Philippines Roofing Industry?

To stay informed about further developments, trends, and reports in the Philippines Roofing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence