Key Insights

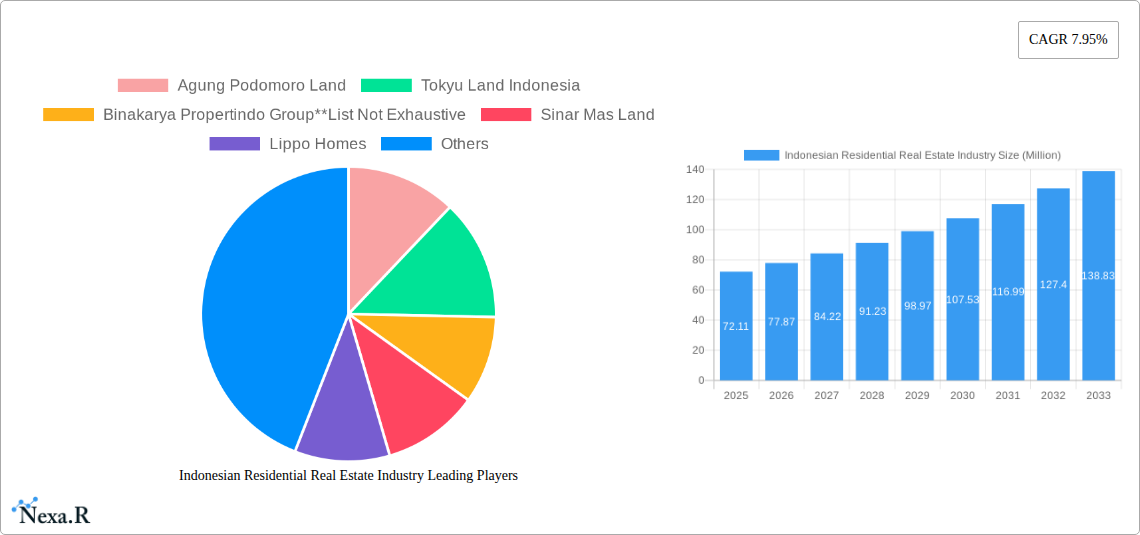

The Indonesian residential real estate market, valued at $72.11 million in 2025, exhibits robust growth potential, projected to expand at a Compound Annual Growth Rate (CAGR) of 7.95% from 2025 to 2033. This expansion is fueled by several key drivers. A burgeoning middle class with increasing disposable income is a significant factor, coupled with ongoing urbanization and government initiatives promoting affordable housing. Demand is particularly strong in key metropolitan areas like Jakarta, Greater Surabaya, and Semarang, reflecting the concentration of economic activity and employment opportunities. The market is segmented primarily by property type (condominiums/apartments, villas/landed houses) catering to diverse preferences and budgets. While growth is substantial, challenges persist. These include fluctuating interest rates, land scarcity in prime locations, and regulatory complexities that can impact project timelines and costs. Competition among established players like Agung Podomoro Land, Tokyu Land Indonesia, and Sinar Mas Land, along with the rise of smaller developers, further shapes the market dynamics. The forecast anticipates continued growth, although the rate may moderate slightly in later years as the market matures and the impact of macroeconomic factors becomes more pronounced. Strategic land acquisitions, innovative construction techniques, and focused marketing strategies targeting specific demographics will be crucial for success in this dynamic market.

The Indonesian residential real estate sector shows strong promise, but careful consideration of market fluctuations is key for stakeholders. Analyzing regional variations in demand and adapting to evolving consumer preferences will be essential for long-term success. The government’s role in providing supportive infrastructure and streamlined regulations will further influence the market's trajectory. Continued investment in sustainable development practices and the provision of financing options tailored to different income groups will help to unlock further growth potential. The strong presence of large, established players signifies market maturity, but agile adaptation and diversification are crucial for developers to maintain competitive advantage in the coming years. Careful assessment of risks, including potential economic downturns and supply chain disruptions, forms a critical component of effective market strategy.

Indonesian Residential Real Estate Industry: Market Analysis & Forecast 2019-2033

This comprehensive report provides a detailed analysis of the Indonesian residential real estate market, covering market dynamics, growth trends, key players, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as both the base and estimated year. This report is invaluable for investors, developers, policymakers, and industry professionals seeking to understand and navigate this dynamic market. The report leverages extensive data analysis to provide quantitative and qualitative insights into the Indonesian residential real estate landscape.

Indonesian Residential Real Estate Industry Market Dynamics & Structure

This section analyzes the Indonesian residential real estate market's competitive landscape, technological advancements, regulatory environment, and market trends from 2019-2024. The market is characterized by a mix of established players and emerging developers, leading to a moderately concentrated market structure. While exact market share figures for individual players fluctuate, Agung Podomoro Land, Sinar Mas Land, and Lippo Homes consistently maintain significant positions.

Market Concentration & Competition:

- High competition among major players for prime locations in major cities.

- Growing presence of foreign investors.

- Market share of top 5 developers estimated at xx% in 2024.

- Increased M&A activity observed in the historical period (2019-2024), with an estimated xx million USD in deal volume.

Technological Innovation:

- Adoption of PropTech solutions (e.g., virtual tours, online property platforms) is increasing but faces challenges in terms of digital literacy and infrastructure in some regions.

- Implementation of Building Information Modeling (BIM) and other digital design tools is improving efficiency for larger firms.

- The barrier to entry for technological adoption lies in the initial investment cost and technical expertise needed.

Regulatory Framework & Substitutes:

- Government regulations influence land availability and project approvals, impacting project timelines and costs.

- The availability of affordable housing alternatives and rental markets presents competitive substitutes.

- Recent policy changes focusing on affordable housing have increased competition in lower price segments.

End-User Demographics & M&A Trends:

- Growing middle class is the key driver of demand, particularly in the condominium and landed house segments.

- Increasing urbanization is fueling demand for residential properties in major cities.

- Future M&A activity is predicted to focus on consolidation and expansion into secondary cities.

Indonesian Residential Real Estate Industry Growth Trends & Insights

The Indonesian residential real estate market experienced [XXX - insert specific growth rate and market size data here, e.g., a CAGR of X% from 2019 to 2024, reaching a market size of YY Million units]. This growth is primarily driven by a rising middle class, rapid urbanization, and government initiatives to improve infrastructure. However, economic fluctuations and the availability of financing can significantly impact market performance. The adoption rate of technology is gradually increasing. While not fully disruptive, innovations such as virtual tours and online marketplaces are changing consumer behavior, increasing transparency and convenience. Consumer behavior shows a preference for sustainable, modern homes equipped with smart home technology, particularly in the higher-income brackets. The forecast period (2025-2033) anticipates continued growth, albeit at a potentially moderated pace due to macroeconomic factors and potential regulatory changes. We predict a market size of ZZ Million units in 2033, with a CAGR of Y%.

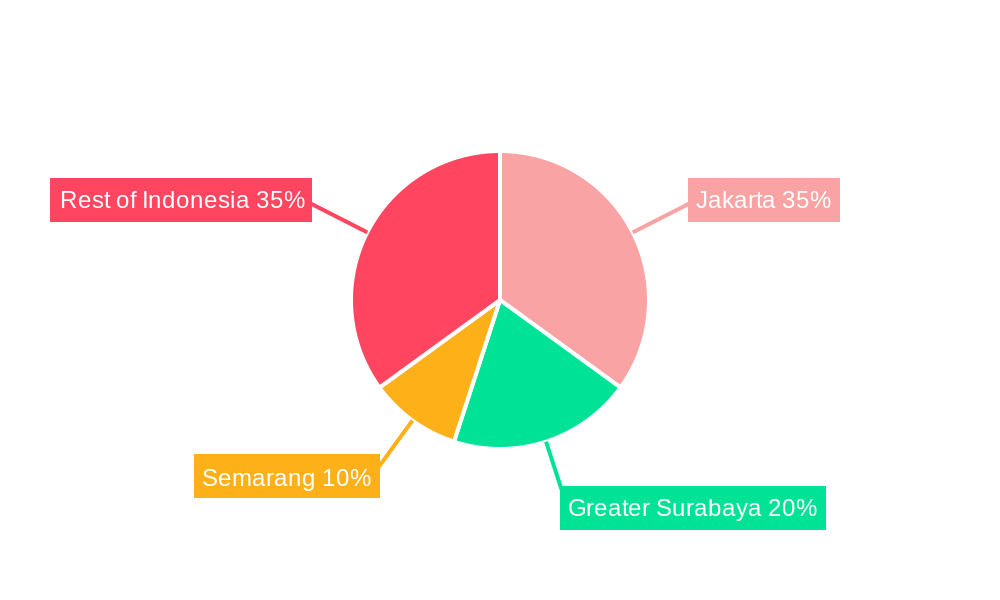

Dominant Regions, Countries, or Segments in Indonesian Residential Real Estate Industry

Jakarta remains the dominant region in the Indonesian residential real estate market, followed by Greater Surabaya and Semarang. The condominium and apartment segment dominates in urban centers due to higher population density and land scarcity. Meanwhile, landed houses and villas remain popular in suburban and peri-urban areas.

Key Drivers:

- Jakarta: Strong economic activity, concentration of employment opportunities, and limited land availability drive high demand and prices for both condominiums and landed houses.

- Greater Surabaya: Rapid urbanization, industrial growth, and a large population are major growth drivers.

- Semarang: Expanding middle class and infrastructure development contribute to growth.

- Rest of Indonesia: Significant growth potential exists in secondary cities, driven by improved infrastructure and government initiatives focused on regional development.

Dominance Factors:

- High population density and limited land supply in Jakarta contribute to its dominance.

- The availability of land and lower property prices in Greater Surabaya and Semarang attract a larger range of buyers.

- The growth potential in the "Rest of Indonesia" segment is largely dependent on improving infrastructure and access to financing.

Market Share & Growth Potential:

- Jakarta holds approximately xx% market share in 2025, with an expected growth rate of x% in the forecast period.

- Greater Surabaya and Semarang combined hold approximately xx% market share, with an expected growth rate of y% in the forecast period.

- The "Rest of Indonesia" segment is projected to experience a significant increase in market share, expected to reach xx% by 2033.

Indonesian Residential Real Estate Industry Product Landscape

The Indonesian residential real estate market offers a diverse product landscape, ranging from affordable apartments to luxurious villas. Innovation focuses on incorporating sustainable design principles, smart home technologies, and improved building materials to enhance energy efficiency, security, and convenience. Unique selling propositions often include features like communal amenities, green spaces, and strategic locations. Technological advancements are driving the incorporation of smart home features, virtual tours, and online property platforms, enhancing the buyer experience.

Key Drivers, Barriers & Challenges in Indonesian Residential Real Estate Industry

Key Drivers:

- Rapid urbanization and population growth continue to drive demand for housing.

- A growing middle class with increased purchasing power fuels market expansion.

- Government initiatives promoting affordable housing and infrastructure development are key catalysts.

Challenges & Restraints:

- Land acquisition and regulatory approvals remain significant hurdles.

- Infrastructure limitations in certain regions can hinder development and increase costs.

- Financing constraints and interest rates affect affordability for potential buyers. The impact of interest rate hikes on mortgage affordability is estimated to reduce demand by xx% in the next 2 years.

Emerging Opportunities in Indonesian Residential Real Estate Industry

Opportunities exist in developing affordable housing solutions for the burgeoning middle class, leveraging sustainable building materials and technologies, expanding into secondary and tertiary cities, and targeting specific niche markets (e.g., retirement communities, eco-friendly developments). Furthermore, incorporating smart home technologies and personalized living spaces will attract the technologically-savvy consumer.

Growth Accelerators in the Indonesian Residential Real Estate Industry

Strategic partnerships between developers and technology providers can expedite the adoption of PropTech solutions. Government policies promoting sustainable development and affordable housing will stimulate market expansion. Focusing on underserved markets in secondary cities will unlock significant growth potential.

Key Players Shaping the Indonesian Residential Real Estate Industry Market

- Agung Podomoro Land

- Tokyu Land Indonesia

- Binakarya Propertindo Group

- Sinar Mas Land

- Lippo Homes

- JABABEKA

- PT Pakuwon Jati

- Ciputra Group

- PP Properti

- Duta Anggada Realty

Notable Milestones in Indonesian Residential Real Estate Industry Sector

- 2020: Government launched a program to increase the availability of affordable housing.

- 2022: Several major developers announced significant investments in sustainable building practices.

- 2023: Several mergers and acquisitions reshaped the competitive landscape. (Specific details about these events are needed for a complete report)

In-Depth Indonesian Residential Real Estate Industry Market Outlook

The Indonesian residential real estate market is poised for continued growth, driven by urbanization, economic expansion, and ongoing government support. Strategic opportunities exist for developers who can innovate, adapt to evolving consumer preferences, and navigate regulatory challenges effectively. Focusing on sustainable development and affordable housing will prove crucial for long-term success. The market outlook is positive, with significant potential for expansion in both established and emerging regions.

Indonesian Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Condominiums and Apartments

- 1.2. Villas and landed houses

-

2. Key Cities

- 2.1. Jakarta

- 2.2. Greater Surabaya

- 2.3. Semarang

- 2.4. Rest of Indonesia

Indonesian Residential Real Estate Industry Segmentation By Geography

- 1. Indonesia

Indonesian Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.95% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Investment in Infrastructure Projects; The rising popularity of sustainable architecture

- 3.3. Market Restrains

- 3.3.1. Volatility in Raw material prices

- 3.4. Market Trends

- 3.4.1. Jakarta Emerging as a Prime Rental Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Indonesian Residential Real Estate Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Condominiums and Apartments

- 5.1.2. Villas and landed houses

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Jakarta

- 5.2.2. Greater Surabaya

- 5.2.3. Semarang

- 5.2.4. Rest of Indonesia

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Indonesia

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Agung Podomoro Land

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Tokyu Land Indonesia

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Binakarya Propertindo Group**List Not Exhaustive

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Sinar Mas Land

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Lippo Homes

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 JABABEKA

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 PT Pakuwon Jati

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Ciputra Group

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 PP Properti

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Duta Anggada Realty

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Agung Podomoro Land

List of Figures

- Figure 1: Indonesian Residential Real Estate Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Indonesian Residential Real Estate Industry Share (%) by Company 2024

List of Tables

- Table 1: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2019 & 2032

- Table 4: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 7: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2019 & 2032

- Table 8: Indonesian Residential Real Estate Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indonesian Residential Real Estate Industry?

The projected CAGR is approximately 7.95%.

2. Which companies are prominent players in the Indonesian Residential Real Estate Industry?

Key companies in the market include Agung Podomoro Land, Tokyu Land Indonesia, Binakarya Propertindo Group**List Not Exhaustive, Sinar Mas Land, Lippo Homes, JABABEKA, PT Pakuwon Jati, Ciputra Group, PP Properti, Duta Anggada Realty.

3. What are the main segments of the Indonesian Residential Real Estate Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 72.11 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Investment in Infrastructure Projects; The rising popularity of sustainable architecture.

6. What are the notable trends driving market growth?

Jakarta Emerging as a Prime Rental Market.

7. Are there any restraints impacting market growth?

Volatility in Raw material prices.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indonesian Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indonesian Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indonesian Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Indonesian Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence