Key Insights

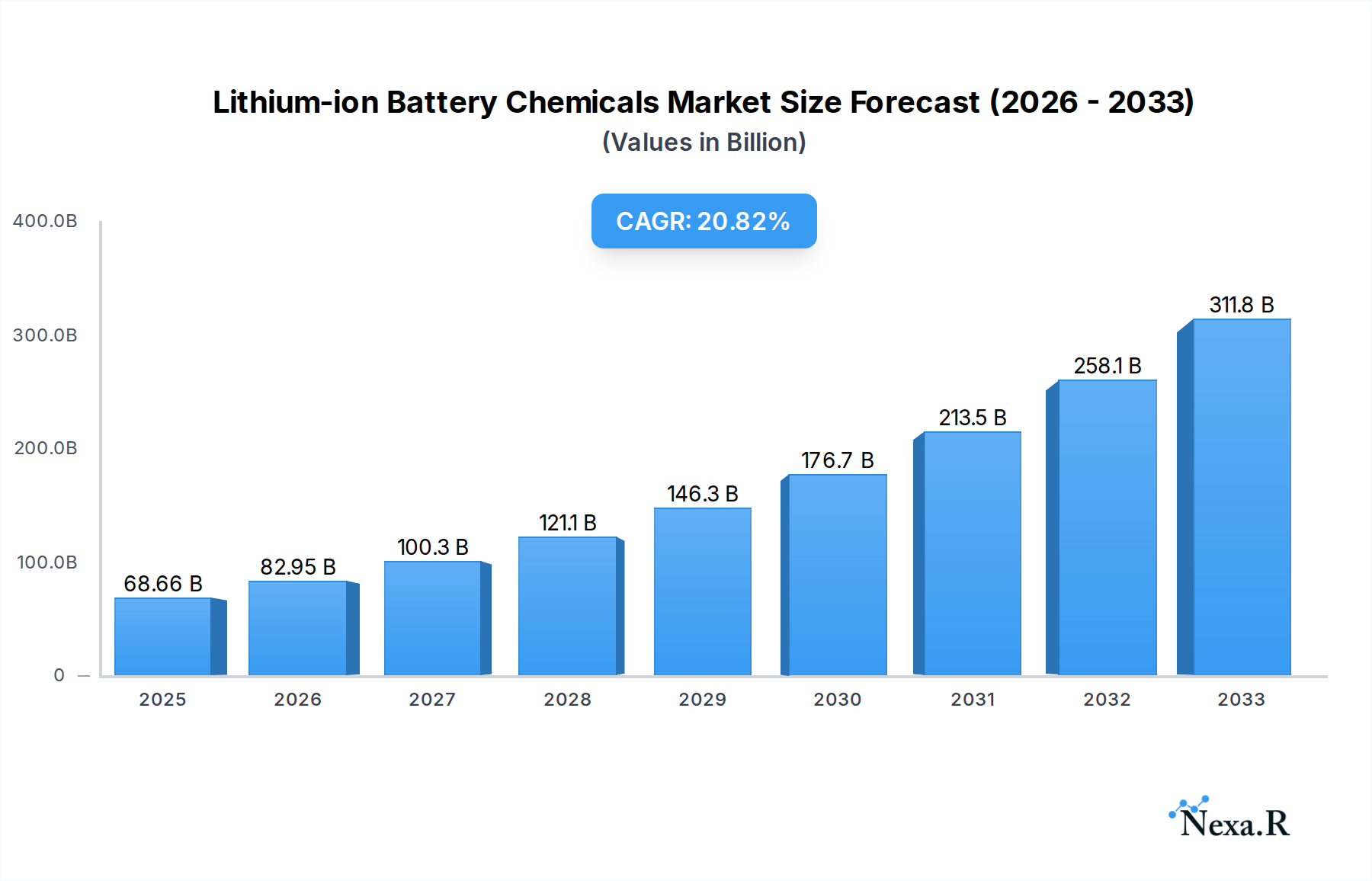

The global Lithium-ion Battery Chemicals market is poised for remarkable expansion, projected to reach USD 68.66 billion by 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of 21.1%. This robust growth is fueled by the escalating demand for electric vehicles (EVs), which heavily rely on advanced lithium-ion batteries for their energy storage solutions. The increasing adoption of renewable energy sources like solar and wind power is further accelerating the need for efficient energy storage systems, thereby bolstering the market for lithium-ion battery chemicals. Furthermore, the burgeoning consumer electronics sector, encompassing smartphones, laptops, and wearable devices, continues to be a significant contributor to this demand. Key applications within this market are segmented into energy storage lithium-ion batteries, power lithium-ion batteries, and consumer lithium-ion batteries, each showcasing substantial growth potential.

Lithium-ion Battery Chemicals Market Size (In Billion)

The market is characterized by dynamic innovation in cathode and anode materials. Ternary cathode materials, known for their high energy density, are leading the charge, alongside the growing interest in Lithium Iron Phosphate (LFP) cathode materials due to their enhanced safety and cost-effectiveness. In terms of anode technology, graphite negative electrodes remain dominant, but significant research and development are being poured into carbon silicon anodes, promising higher energy density and faster charging capabilities. The electrolyte segment is also witnessing advancements, with a focus on developing safer and more efficient formulations. Geographically, the Asia Pacific region, particularly China, is expected to dominate the market, owing to its established manufacturing base and strong government support for the EV and battery industries. The competitive landscape is shaped by a number of prominent companies, including Guangzhou Tinci Materials, Yunnan Energy New Material, and CNGR Advanced Material, all actively investing in R&D and capacity expansion to meet the burgeoning global demand.

Lithium-ion Battery Chemicals Company Market Share

Unlock the future of energy with our comprehensive Lithium-ion Battery Chemicals market report. This definitive guide provides an in-depth analysis of the global market, meticulously segmented by application and type, and driven by critical industry developments. Covering the historical period of 2019-2024, base and estimated year of 2025, and a forecast period extending to 2033, this report is your essential resource for strategic decision-making in the rapidly evolving lithium-ion battery supply chain. Gain unparalleled insights into market dynamics, growth trends, regional dominance, product innovation, key players, and emerging opportunities that will shape the $150 billion (estimated 2025 value) lithium-ion battery chemicals market.

Lithium-ion Battery Chemicals Market Dynamics & Structure

The lithium-ion battery chemicals market is characterized by a moderately concentrated structure, with a blend of established global players and emerging regional specialists. Technological innovation remains a primary driver, fueled by the relentless demand for higher energy density, faster charging capabilities, and enhanced safety in batteries for electric vehicles (EVs) and energy storage systems. Significant investment in R&D for advanced cathode materials like nickel-manganese-cobalt (NMC) and lithium iron phosphate (LFP), as well as next-generation anode materials such as silicon-graphite composites, is reshaping the competitive landscape. Regulatory frameworks, particularly those focused on environmental sustainability and critical mineral sourcing, are increasingly influencing production processes and material choices. Competitive product substitutes, such as solid-state electrolytes and alternative battery chemistries, are also emerging, albeit with longer development timelines. End-user demographics, heavily influenced by the accelerating adoption of EVs and renewable energy integration, are creating sustained demand. Mergers and acquisitions (M&A) activity is a notable trend, with companies seeking to secure raw material supply, expand production capacity, and integrate vertically. For instance, recent M&A deals in the past two years have focused on acquiring critical mineral assets and battery material manufacturing capabilities, consolidating market share and enhancing technological expertise. The market is projected to see continued consolidation as economies of scale become paramount.

- Market Concentration: Moderately concentrated, with a few key players holding significant market share, alongside a growing number of specialized manufacturers.

- Technological Innovation Drivers: Demand for higher energy density, faster charging, improved safety, and cost reduction.

- Regulatory Frameworks: Growing emphasis on sustainability, critical mineral sourcing transparency, and recycling initiatives.

- Competitive Product Substitutes: Emergence of solid-state batteries and alternative chemistries, posing long-term competitive threats.

- End-User Demographics: Driven by EV adoption, consumer electronics, and grid-scale energy storage solutions.

- M&A Trends: Strategic acquisitions focused on raw material access, capacity expansion, and technology integration.

Lithium-ion Battery Chemicals Growth Trends & Insights

The global lithium-ion battery chemicals market is on an unprecedented growth trajectory, projected to expand significantly from an estimated $150 billion in 2025 to over $300 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately xx%. This expansion is fundamentally driven by the electrifying global transition towards sustainable energy solutions. The escalating adoption of electric vehicles (EVs) across major automotive markets, coupled with the burgeoning demand for large-scale energy storage systems to support renewable energy grids, are the primary catalysts. Technological advancements continue to unlock new possibilities, with ongoing research into novel cathode and anode materials promising higher energy densities, faster charging times, and extended battery lifespans. For example, the refinement of ternary cathode materials, such as NMC 811, and the increased adoption of lithium iron phosphate (LFP) for its cost-effectiveness and safety, are directly impacting market dynamics. Similarly, advancements in anode technology, including the integration of silicon into graphite anodes, are crucial for meeting the performance demands of next-generation batteries.

Consumer behavior shifts are also playing a pivotal role. As awareness around climate change grows and governments implement supportive policies, consumers are increasingly opting for EVs and embracing smart home energy solutions. This heightened demand for lithium-ion battery-powered devices, from smartphones to power tools, further fuels market growth. The report will delve into the intricate interplay of these factors, providing detailed metrics on market size evolution, adoption rates of different battery chemistries, and the impact of disruptive technologies. Specific insights will include the penetration rates of LFP versus ternary cathode materials in different applications, the projected growth of silicon-carbon anode technologies, and the evolving consumer preferences for battery performance characteristics like energy density and charge speed. The analysis will also explore how evolving manufacturing processes and supply chain efficiencies are contributing to cost reductions, thereby accelerating market penetration. The sheer scale of investment in battery gigafactories globally underscores the sustained demand and the optimistic outlook for the lithium-ion battery chemicals sector.

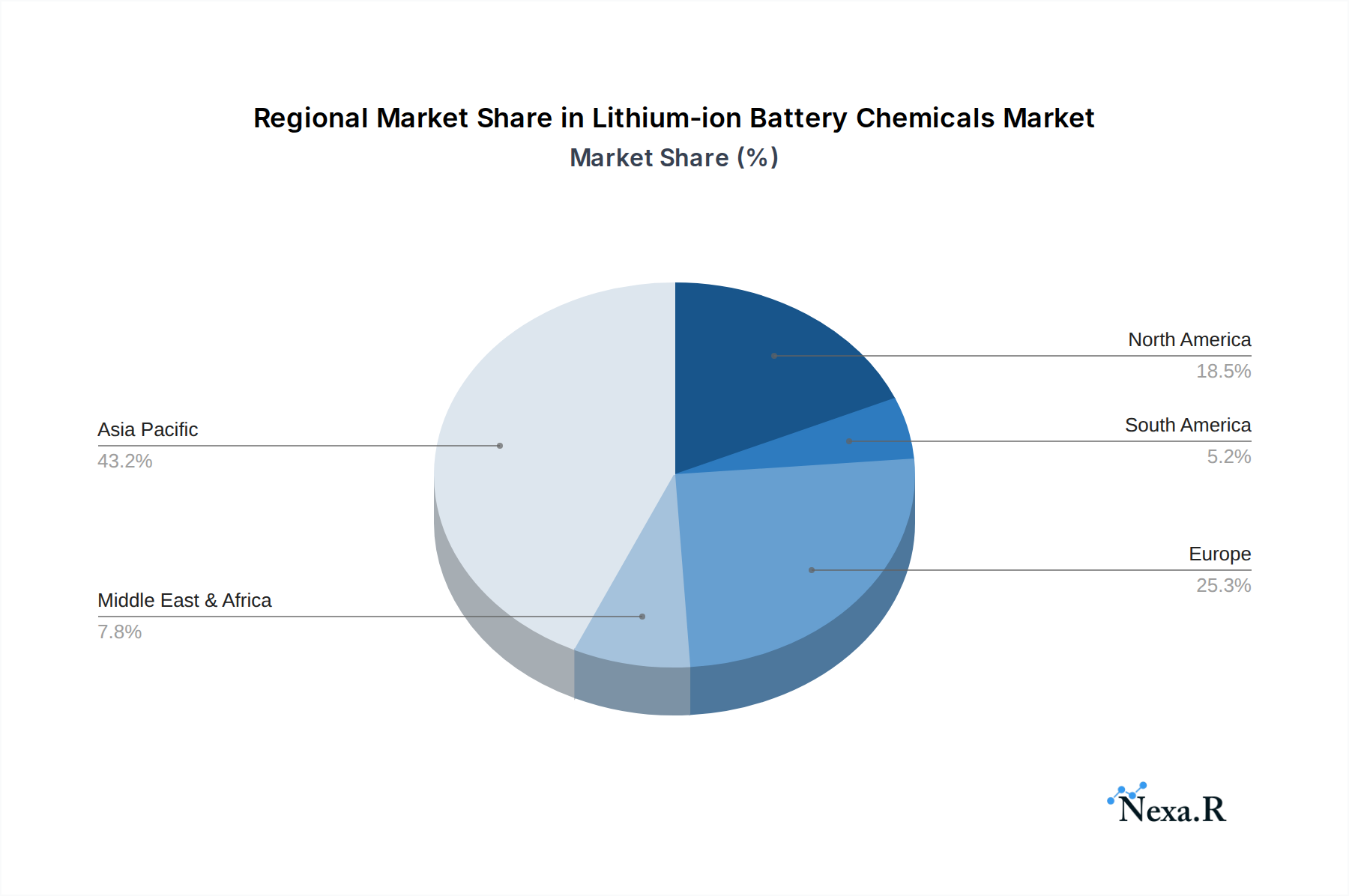

Dominant Regions, Countries, or Segments in Lithium-ion Battery Chemicals

The Energy Storage Lithium-ion Battery segment is poised to be the dominant force driving market growth in the global lithium-ion battery chemicals sector. This dominance is underpinned by the global imperative to decarbonize energy systems and the rapid expansion of renewable energy infrastructure. The increasing reliance on solar and wind power necessitates robust energy storage solutions to ensure grid stability and reliability, directly translating into a massive demand for battery chemicals. Countries with ambitious renewable energy targets and significant investments in grid modernization are leading this charge.

Within this overarching trend, specific applications and material types demonstrate significant influence:

- Application: Energy Storage Lithium-ion Battery: This segment's growth is propelled by the construction of utility-scale battery storage facilities, residential energy storage systems, and backup power solutions for critical infrastructure. The demand for long-duration storage solutions is creating new avenues for chemical innovation.

- Types: Lithium Iron Phosphate (LFP) Cathode: LFP has witnessed a remarkable resurgence, particularly in energy storage and increasingly in entry-level to mid-range EVs. Its inherent safety, cost-effectiveness, and long cycle life make it an attractive alternative to ternary cathode materials, especially in stationary applications where energy density is less critical. The projected market share for LFP in the energy storage segment is substantial.

- Types: Ternary Cathode Material (NMC): While LFP gains traction, high-nickel ternary cathode materials (e.g., NMC 811, NCA) continue to dominate in applications requiring higher energy density, such as performance EVs and premium consumer electronics. Their ability to deliver greater range and power output remains a key differentiator.

- Types: Graphite Negative Electrode: This remains the workhorse of the anode market due to its established performance and cost-effectiveness. While facing competition from newer materials, its widespread adoption in the historical period of 2019-2024 and projected continued demand ensure its significant market share.

- Types: Electrolyte: The electrolyte plays a crucial role in ion transport and battery performance. Innovations in electrolyte formulations, including the development of safer and more stable chemistries, are critical for unlocking the full potential of next-generation battery technologies. The demand for electrolyte is directly tied to the growth of all battery types.

Economical policies, such as tax incentives for renewable energy deployment and mandates for energy storage integration, are critical drivers in regions like Asia Pacific, particularly China, which is a manufacturing powerhouse for lithium-ion batteries and their constituent chemicals. North America and Europe are also witnessing substantial growth, driven by stringent emission standards and substantial government funding for EV adoption and grid modernization. Infrastructure development, including the build-out of charging networks and grid enhancements, further stimulates demand. The $150 billion global market in 2025 is significantly influenced by these regional and segment-specific dynamics, with energy storage and LFP materials showing particularly strong growth potential.

Lithium-ion Battery Chemicals Product Landscape

The lithium-ion battery chemicals product landscape is characterized by continuous innovation aimed at enhancing battery performance, safety, and cost-effectiveness. Key advancements include the development of high-nickel ternary cathode materials like NMC 811 and NCA, offering superior energy density for longer EV ranges. Simultaneously, the resurgence of lithium iron phosphate (LFP) cathodes, driven by their exceptional safety profile, thermal stability, and cost advantages, is making them a dominant choice for energy storage and entry-level EVs. On the anode side, significant strides are being made in silicon-graphite composite materials, which promise to drastically increase energy density by overcoming the volumetric expansion challenges of pure silicon. Electrolyte formulations are also evolving, with a focus on enhanced thermal stability, wider operating temperature ranges, and improved safety features, including the exploration of solid-state electrolytes for next-generation battery architectures. These product innovations are directly influencing application performance metrics such as Wh/kg, charge/discharge rates, and cycle life.

Key Drivers, Barriers & Challenges in Lithium-ion Battery Chemicals

The lithium-ion battery chemicals market is propelled by powerful drivers including the global surge in electric vehicle adoption, fueled by environmental regulations and consumer demand for sustainable transportation. The expansion of renewable energy sources like solar and wind power necessitates large-scale energy storage solutions, creating substantial demand for battery chemicals. Technological advancements in battery materials, leading to higher energy density, faster charging, and improved safety, are also key growth accelerators. Government incentives and supportive policies promoting EV sales and renewable energy integration further bolster market expansion.

However, the market faces significant barriers and challenges:

- Raw Material Scarcity and Price Volatility: Dependence on critical minerals like lithium, cobalt, and nickel, which are subject to supply chain disruptions and significant price fluctuations, poses a major challenge.

- Environmental Concerns and Sustainability: The mining and processing of raw materials raise environmental concerns, and the industry faces increasing pressure to adopt sustainable practices and improve recycling processes.

- Technological Obsolescence: Rapid technological advancements mean that existing battery chemistries and materials can become obsolete quickly, requiring continuous R&D investment.

- Geopolitical Risks: Concentration of key raw material sources in a few regions can lead to geopolitical risks and supply chain vulnerabilities, impacting production costs and availability. The cost of R&D for novel materials and scaling up production can be substantial.

Emerging Opportunities in Lithium-ion Battery Chemicals

Emerging opportunities in the lithium-ion battery chemicals sector lie in the development of next-generation battery technologies and the expansion into untapped markets. The pursuit of solid-state batteries, which promise enhanced safety and energy density by replacing liquid electrolytes with solid ones, presents a significant long-term opportunity for specialized chemical manufacturers. The increasing demand for batteries in diverse applications, such as electric aviation, advanced robotics, and grid-scale long-duration energy storage, opens new avenues for tailored chemical solutions. Furthermore, the growing emphasis on circular economy principles is driving opportunities in battery recycling and the development of sustainable sourcing practices for critical raw materials, creating a market for recovered and ethically sourced battery chemicals.

Growth Accelerators in the Lithium-ion Battery Chemicals Industry

Several key catalysts are accelerating the long-term growth of the lithium-ion battery chemicals industry. Foremost among these are continuous technological breakthroughs in material science, enabling the development of batteries with higher energy density, faster charging capabilities, and extended lifespans. Strategic partnerships and collaborations between raw material suppliers, chemical manufacturers, and battery producers are crucial for streamlining supply chains and driving innovation. Furthermore, market expansion strategies, including the penetration of emerging economies and the development of specialized battery solutions for new application segments, are vital growth drivers. Government policies that prioritize electrification and renewable energy integration, coupled with substantial investments in battery manufacturing infrastructure, further solidify the industry's growth trajectory.

Key Players Shaping the Lithium-ion Battery Chemicals Market

- Guangzhou Tinci Materials

- Yunnan Energy New Material

- CNGR Advanced Material

- Shenzhen Dynanonic

- XTC New Energy Materials

- Beijing Easpring Material

- Shinghwa Advanced Material Group

- Hunan Changyuan Lico

- Guizhou Zhenhua E-chem

- Anhui Estone Materials

- Shenzhen Capchem Technology

- Shenzhen XFH Technology

- Guangdong Fangyuan New Materials

- Jiangmen Kanhoo

- Shenzhen Senior Technology Material

- Wodgina

- Do-Fluoride New Materials

- Tonze New Energy

- Shanghai Putailai

- Btr New Material

Notable Milestones in Lithium-ion Battery Chemicals Sector

- 2022/08: Guangzhou Tinci Materials announces plans to expand LFP cathode production capacity to meet growing demand.

- 2023/01: CNGR Advanced Material secures significant supply contracts for precursor materials for ternary cathodes.

- 2023/04: Yunnan Energy New Material invests heavily in R&D for silicon-carbon anode technology.

- 2023/07: Shenzhen Capchem Technology develops a new electrolyte formulation for enhanced thermal stability in high-voltage batteries.

- 2023/11: XTC New Energy Materials completes construction of a new advanced LFP cathode production facility.

- 2024/02: Beijing Easpring Material announces a joint venture to explore next-generation anode materials.

- 2024/05: Shinghwa Advanced Material Group acquires a stake in a critical mineral mining operation to secure raw material supply.

- 2024/09: Hunan Changyuan Lico expands its production of high-purity lithium salts for electrolyte manufacturing.

- 2024/12: Do-Fluoride New Materials launches a new generation of fluorine-containing additives for electrolytes.

In-Depth Lithium-ion Battery Chemicals Market Outlook

The outlook for the lithium-ion battery chemicals market remains exceptionally robust, driven by the inescapable global transition towards electrification and sustainable energy. Growth accelerators like advancements in solid-state battery technology and the expanding applications in electric aviation and grid-scale storage will continue to fuel demand for specialized chemicals. Strategic partnerships and a concerted focus on circular economy principles, including advanced recycling techniques and sustainable sourcing, will shape the future competitive landscape. The market is projected to witness sustained investment in R&D and manufacturing capacity expansion, ensuring its pivotal role in enabling a cleaner energy future.

Lithium-ion Battery Chemicals Segmentation

-

1. Application

- 1.1. Energy Storage Lithium-ion Battery

- 1.2. Power Lithium-ion Battery

- 1.3. Consumer Lithium-ion Battery

-

2. Types

- 2.1. Ternary Cathode Material

- 2.2. Lithium Iron Phosphate Cathode

- 2.3. Other Cathode Materials

- 2.4. Graphite Negative Electrode

- 2.5. Carbon Silicon Anode

- 2.6. Other Negative Pole

- 2.7. Electrolyte

Lithium-ion Battery Chemicals Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Lithium-ion Battery Chemicals Regional Market Share

Geographic Coverage of Lithium-ion Battery Chemicals

Lithium-ion Battery Chemicals REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Energy Storage Lithium-ion Battery

- 5.1.2. Power Lithium-ion Battery

- 5.1.3. Consumer Lithium-ion Battery

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Ternary Cathode Material

- 5.2.2. Lithium Iron Phosphate Cathode

- 5.2.3. Other Cathode Materials

- 5.2.4. Graphite Negative Electrode

- 5.2.5. Carbon Silicon Anode

- 5.2.6. Other Negative Pole

- 5.2.7. Electrolyte

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Lithium-ion Battery Chemicals Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Energy Storage Lithium-ion Battery

- 6.1.2. Power Lithium-ion Battery

- 6.1.3. Consumer Lithium-ion Battery

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Ternary Cathode Material

- 6.2.2. Lithium Iron Phosphate Cathode

- 6.2.3. Other Cathode Materials

- 6.2.4. Graphite Negative Electrode

- 6.2.5. Carbon Silicon Anode

- 6.2.6. Other Negative Pole

- 6.2.7. Electrolyte

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Lithium-ion Battery Chemicals Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Energy Storage Lithium-ion Battery

- 7.1.2. Power Lithium-ion Battery

- 7.1.3. Consumer Lithium-ion Battery

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Ternary Cathode Material

- 7.2.2. Lithium Iron Phosphate Cathode

- 7.2.3. Other Cathode Materials

- 7.2.4. Graphite Negative Electrode

- 7.2.5. Carbon Silicon Anode

- 7.2.6. Other Negative Pole

- 7.2.7. Electrolyte

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Lithium-ion Battery Chemicals Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Energy Storage Lithium-ion Battery

- 8.1.2. Power Lithium-ion Battery

- 8.1.3. Consumer Lithium-ion Battery

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Ternary Cathode Material

- 8.2.2. Lithium Iron Phosphate Cathode

- 8.2.3. Other Cathode Materials

- 8.2.4. Graphite Negative Electrode

- 8.2.5. Carbon Silicon Anode

- 8.2.6. Other Negative Pole

- 8.2.7. Electrolyte

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Lithium-ion Battery Chemicals Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Energy Storage Lithium-ion Battery

- 9.1.2. Power Lithium-ion Battery

- 9.1.3. Consumer Lithium-ion Battery

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Ternary Cathode Material

- 9.2.2. Lithium Iron Phosphate Cathode

- 9.2.3. Other Cathode Materials

- 9.2.4. Graphite Negative Electrode

- 9.2.5. Carbon Silicon Anode

- 9.2.6. Other Negative Pole

- 9.2.7. Electrolyte

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Lithium-ion Battery Chemicals Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Energy Storage Lithium-ion Battery

- 10.1.2. Power Lithium-ion Battery

- 10.1.3. Consumer Lithium-ion Battery

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Ternary Cathode Material

- 10.2.2. Lithium Iron Phosphate Cathode

- 10.2.3. Other Cathode Materials

- 10.2.4. Graphite Negative Electrode

- 10.2.5. Carbon Silicon Anode

- 10.2.6. Other Negative Pole

- 10.2.7. Electrolyte

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Lithium-ion Battery Chemicals Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Energy Storage Lithium-ion Battery

- 11.1.2. Power Lithium-ion Battery

- 11.1.3. Consumer Lithium-ion Battery

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Ternary Cathode Material

- 11.2.2. Lithium Iron Phosphate Cathode

- 11.2.3. Other Cathode Materials

- 11.2.4. Graphite Negative Electrode

- 11.2.5. Carbon Silicon Anode

- 11.2.6. Other Negative Pole

- 11.2.7. Electrolyte

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Guangzhou Tinci Materials

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Yunnan Energy New Material

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 CNGR Advanced Material

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Shenzhen Dynanonic

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 XTC New Energy Materials

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Beijing Easpring Material

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Shinghwa Advanced Material Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hunan Changyuan Lico

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Guizhou Zhenhua E-chem

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Anhui Estone Materials

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Shenzhen Capchem Technology

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Shenzhen XFH Technology

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Guangdong Fangyuan New Materials

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Jiangmen Kanhoo

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Shenzhen Senior Technology Material

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Wodgina

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Do-Fluoride New Materials

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Tonze New Energy

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Shanghai Putailai

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Btr New Material

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.1 Guangzhou Tinci Materials

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Lithium-ion Battery Chemicals Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Lithium-ion Battery Chemicals Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Lithium-ion Battery Chemicals Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Lithium-ion Battery Chemicals Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Lithium-ion Battery Chemicals Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Lithium-ion Battery Chemicals Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Lithium-ion Battery Chemicals Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Lithium-ion Battery Chemicals Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Lithium-ion Battery Chemicals Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Lithium-ion Battery Chemicals Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Lithium-ion Battery Chemicals Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Lithium-ion Battery Chemicals Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Lithium-ion Battery Chemicals Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Lithium-ion Battery Chemicals Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Lithium-ion Battery Chemicals Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Lithium-ion Battery Chemicals Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Lithium-ion Battery Chemicals Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Lithium-ion Battery Chemicals Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Lithium-ion Battery Chemicals Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Lithium-ion Battery Chemicals Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Lithium-ion Battery Chemicals Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Lithium-ion Battery Chemicals Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Lithium-ion Battery Chemicals Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Lithium-ion Battery Chemicals Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Lithium-ion Battery Chemicals Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Lithium-ion Battery Chemicals Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Lithium-ion Battery Chemicals Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Lithium-ion Battery Chemicals Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Lithium-ion Battery Chemicals Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Lithium-ion Battery Chemicals Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Lithium-ion Battery Chemicals Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Lithium-ion Battery Chemicals Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Lithium-ion Battery Chemicals Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Lithium-ion Battery Chemicals?

The projected CAGR is approximately 21.1%.

2. Which companies are prominent players in the Lithium-ion Battery Chemicals?

Key companies in the market include Guangzhou Tinci Materials, Yunnan Energy New Material, CNGR Advanced Material, Shenzhen Dynanonic, XTC New Energy Materials, Beijing Easpring Material, Shinghwa Advanced Material Group, Hunan Changyuan Lico, Guizhou Zhenhua E-chem, Anhui Estone Materials, Shenzhen Capchem Technology, Shenzhen XFH Technology, Guangdong Fangyuan New Materials, Jiangmen Kanhoo, Shenzhen Senior Technology Material, Wodgina, Do-Fluoride New Materials, Tonze New Energy, Shanghai Putailai, Btr New Material.

3. What are the main segments of the Lithium-ion Battery Chemicals?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 68.66 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Lithium-ion Battery Chemicals," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Lithium-ion Battery Chemicals report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Lithium-ion Battery Chemicals?

To stay informed about further developments, trends, and reports in the Lithium-ion Battery Chemicals, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence