Key Insights

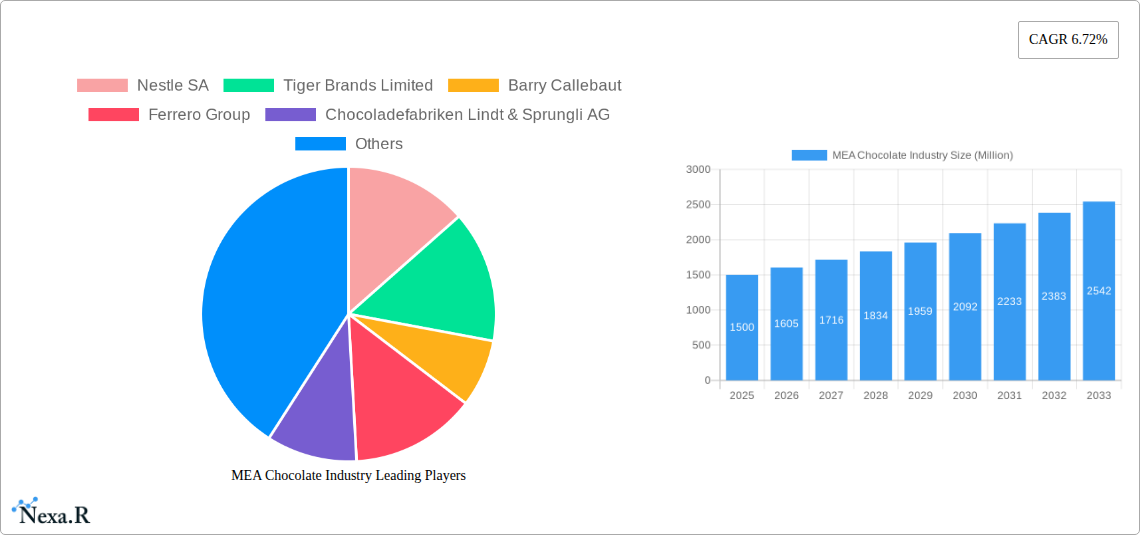

The Middle East and Africa (MEA) chocolate market, valued at approximately $X million in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 6.72% from 2025 to 2033. This expansion is driven by several key factors. Rising disposable incomes across several MEA nations, coupled with a burgeoning young population with a penchant for indulgent treats, fuel significant demand. The increasing popularity of premium chocolate brands and innovative product offerings, such as unique flavor profiles and healthier options (e.g., dark chocolate with higher cacao content), further contribute to market growth. Furthermore, the expansion of organized retail channels like supermarkets and hypermarkets, alongside the rapid growth of e-commerce platforms, provides wider access and distribution channels for chocolate manufacturers. However, the market faces certain challenges. Fluctuations in raw material prices, particularly cocoa beans, pose a risk to profitability. Additionally, the prevalence of traditional sweets and confectionery in certain regions presents competition for chocolate manufacturers. Successful players will need to strategically navigate these challenges through efficient supply chain management, targeted marketing campaigns focusing on specific demographic segments, and diversification of product lines.

The segmental analysis reveals a strong preference for milk and white chocolate over dark chocolate in several MEA countries, reflecting cultural preferences and price sensitivity. Within distribution channels, supermarkets and hypermarkets dominate, highlighting the importance of securing strong retail partnerships. The boxed assortment and countlines segments are particularly significant due to their suitability for gifting and impulse purchases. Seasonal chocolates also represent a key area of growth, particularly around religious holidays and festivals prevalent in the region. Key players like Nestlé, Ferrero, and Mondelez International, along with regional brands, are vying for market share, engaging in competitive strategies focusing on product innovation, brand building, and expanding their distribution networks across the MEA landscape. The forecast period indicates continuous growth, particularly in countries with high economic growth and increasing urbanization.

MEA Chocolate Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Middle East and Africa (MEA) chocolate industry, covering market dynamics, growth trends, key players, and future outlook. The study period spans from 2019 to 2033, with 2025 as the base and estimated year. This report is essential for industry professionals, investors, and strategists seeking to understand and capitalize on opportunities within this dynamic market.

MEA Chocolate Industry Market Dynamics & Structure

The MEA chocolate market is characterized by a blend of established multinational corporations and emerging local players. Market concentration is moderate, with a few dominant players holding significant shares, while numerous smaller companies cater to niche segments. Technological innovation, particularly in production efficiency and product diversification (e.g., healthier options, unique flavors), is a key driver. Regulatory frameworks concerning food safety and labeling influence market practices. Competitive product substitutes, such as confectionery and healthy snacks, pose challenges. End-user demographics, showing a growing young population with increasing disposable incomes, significantly impact consumption patterns. M&A activity in the region is relatively low compared to global trends, with a predicted xx million USD in deal volume during 2019-2024, indicating potential for future consolidation.

- Market Concentration: Moderate, with top 5 players holding approximately xx% market share in 2024.

- Technological Innovation: Focus on automation, sustainable sourcing, and premium product development.

- Regulatory Landscape: Stringent food safety and labeling regulations are in place across various MEA countries.

- Competitive Substitutes: Confectionery, healthy snacks, and other treats compete for consumer spending.

- End-User Demographics: A young, growing population with increasing disposable income fuels demand.

- M&A Activity: Relatively low, with projected xx million USD in deal volume during 2019-2024.

MEA Chocolate Industry Growth Trends & Insights

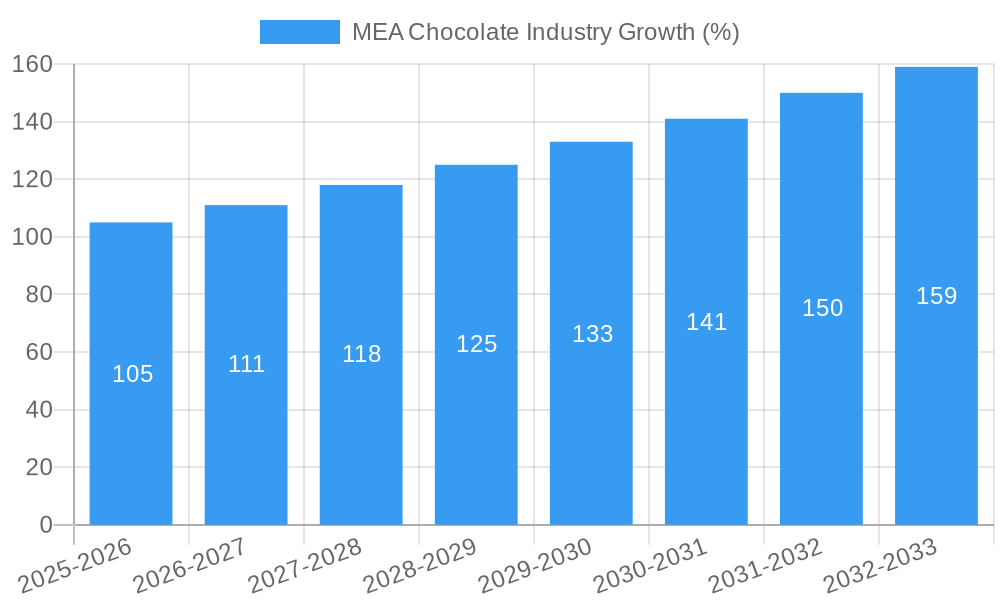

The MEA chocolate market experienced robust growth during the historical period (2019-2024), driven by factors such as rising disposable incomes, urbanization, and changing consumer preferences towards premium and healthier chocolate options. The market size is estimated at xx million in 2025, exhibiting a CAGR of xx% during the historical period. This growth is expected to continue, albeit at a slightly moderated pace, during the forecast period (2025-2033), reaching xx million by 2033. Technological disruptions, such as online retail expansion and innovative product formats, are reshaping the market landscape. Consumer behavior shifts toward healthier choices and premium experiences are influencing product development and marketing strategies. Market penetration remains relatively low in some MEA countries, presenting significant growth opportunities.

Dominant Regions, Countries, or Segments in MEA Chocolate Industry

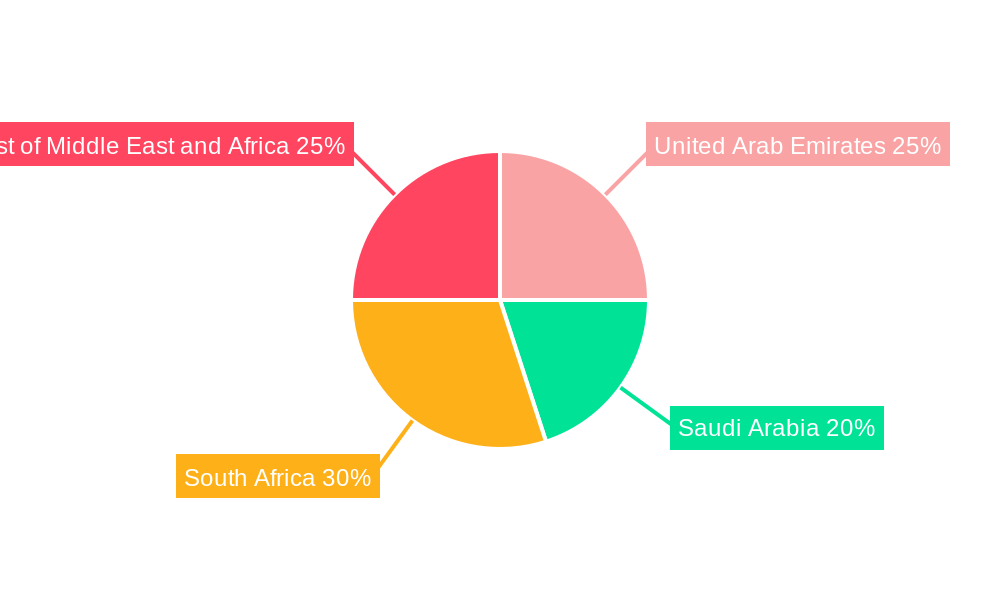

The UAE and Saudi Arabia are the leading markets within the MEA region, accounting for a combined xx% of the total market share in 2024. Strong economic growth and a higher concentration of affluent consumers contribute to this dominance. Within product segments, Milk/White chocolate commands the largest market share, followed by Dark chocolate and Boxed Assortments. Supermarkets/Hypermarkets constitute the primary distribution channel, reflecting the convenience and accessibility they offer to consumers.

- Leading Regions: UAE and Saudi Arabia, driven by high disposable incomes and population density.

- Leading Product Segments: Milk/White chocolate, Dark Chocolate, and Boxed Assortments.

- Leading Distribution Channel: Supermarkets/Hypermarkets, due to wide reach and convenience.

- Growth Drivers: Rising disposable incomes, urbanization, and tourism contribute to market expansion.

MEA Chocolate Industry Product Landscape

The MEA chocolate market showcases a diverse product landscape, ranging from traditional milk and dark chocolate bars to innovative offerings such as whole-fruit chocolates and artisan-made luxury confections. Product innovation focuses on catering to evolving consumer preferences for healthier, more premium, and uniquely flavored options. Technological advancements in production, such as automation and sustainable sourcing, enhance efficiency and quality. Unique selling propositions include organic certification, fair-trade sourcing, and novel flavor combinations.

Key Drivers, Barriers & Challenges in MEA Chocolate Industry

Key Drivers: Rising disposable incomes, increasing urbanization, changing consumer preferences toward premium and healthier options, and the growth of online retail channels fuel market expansion. Government initiatives promoting local food production and tourism also contribute to market growth.

Key Challenges: Fluctuations in raw material prices (cacao beans, sugar), stringent food safety and labeling regulations, intense competition from international and local brands, and the prevalence of counterfeit products hinder market growth. Supply chain disruptions, exacerbated by geopolitical instability in certain regions, pose additional challenges. These factors can lead to price volatility and impact profitability.

Emerging Opportunities in MEA Chocolate Industry

Untapped markets in less-developed regions of the MEA, growth of online retail channels, increasing demand for premium and specialized chocolate products (e.g., organic, fair-trade), and the rising popularity of gifting chocolates during festive seasons represent lucrative opportunities for market players. Developing innovative product formats and flavors tailored to local tastes and preferences can further unlock market potential.

Growth Accelerators in the MEA Chocolate Industry

Technological advancements in production efficiency, sustainable sourcing practices, and strategic partnerships with local farmers and distributors will accelerate market growth. Expanding distribution networks to reach wider consumer segments, particularly in rural areas, and focusing on marketing campaigns highlighting health benefits and premium attributes will further drive market expansion.

Key Players Shaping the MEA Chocolate Industry Market

- Nestle SA

- Tiger Brands Limited

- Barry Callebaut

- Ferrero Group

- Chocoladefabriken Lindt & Sprungli AG

- Mars Incorporated

- Mondelez International Inc

- Cocoa Processing Company Limited

- Kees Beyers Chocolate CC

- The Hershey Company

Notable Milestones in MEA Chocolate Industry Sector

- October 2021: Barry Callebaut opened a new Chocolate Academy in Dubai, UAE, boosting innovation and premium product development.

- February 2022: Made By Two launched a collection of glazed luxury chocolates in Dubai, highlighting the growth of the artisanal chocolate segment.

- March 2022: Barry Callebaut launched its line of whole-fruit chocolates in the UAE, showcasing innovation in healthier chocolate options.

In-Depth MEA Chocolate Industry Market Outlook

The MEA chocolate industry is poised for sustained growth, driven by a confluence of factors, including rising disposable incomes, expanding middle class, increasing urbanization, and the growing preference for premium and innovative chocolate products. Strategic partnerships, focus on sustainable sourcing, and leveraging digital marketing strategies will play pivotal roles in shaping future market leadership and unlocking significant growth potential. The market is expected to continue its upward trajectory, with opportunities for both established players and new entrants to capitalize on the region’s evolving consumer landscape and dynamic market dynamics.

MEA Chocolate Industry Segmentation

-

1. Product

- 1.1. Dark Chocolate

- 1.2. Milk/ White Chocolate

-

2. Type

- 2.1. Boxed Assortments

- 2.2. Countlines

- 2.3. Seasonal Chocolates

- 2.4. Molded Chocolates

- 2.5. Other Product Types

-

3. Distribution Channel

- 3.1. Supermarkets/ Hypermarkets

- 3.2. Specialty Stores

- 3.3. Convenience/Grocery Stores

- 3.4. Online Retail Stores

- 3.5. Other Distribution Channels

-

4. Geography

- 4.1. South Africa

- 4.2. Saudi Arabia

- 4.3. United Arab Emirates

- 4.4. Rest of Middle-East and Africa

MEA Chocolate Industry Segmentation By Geography

- 1. South Africa

- 2. Saudi Arabia

- 3. United Arab Emirates

- 4. Rest of Middle East and Africa

MEA Chocolate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.72% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Government Initiatives and E-commerce Penetration

- 3.3. Market Restrains

- 3.3.1. Detrimental Health Impact of Caffeine Intake

- 3.4. Market Trends

- 3.4.1. Countlines and Premium Dark Chocolates Hold a Major Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global MEA Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Dark Chocolate

- 5.1.2. Milk/ White Chocolate

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Boxed Assortments

- 5.2.2. Countlines

- 5.2.3. Seasonal Chocolates

- 5.2.4. Molded Chocolates

- 5.2.5. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Supermarkets/ Hypermarkets

- 5.3.2. Specialty Stores

- 5.3.3. Convenience/Grocery Stores

- 5.3.4. Online Retail Stores

- 5.3.5. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. South Africa

- 5.4.2. Saudi Arabia

- 5.4.3. United Arab Emirates

- 5.4.4. Rest of Middle-East and Africa

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. South Africa

- 5.5.2. Saudi Arabia

- 5.5.3. United Arab Emirates

- 5.5.4. Rest of Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. South Africa MEA Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Dark Chocolate

- 6.1.2. Milk/ White Chocolate

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Boxed Assortments

- 6.2.2. Countlines

- 6.2.3. Seasonal Chocolates

- 6.2.4. Molded Chocolates

- 6.2.5. Other Product Types

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Supermarkets/ Hypermarkets

- 6.3.2. Specialty Stores

- 6.3.3. Convenience/Grocery Stores

- 6.3.4. Online Retail Stores

- 6.3.5. Other Distribution Channels

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. South Africa

- 6.4.2. Saudi Arabia

- 6.4.3. United Arab Emirates

- 6.4.4. Rest of Middle-East and Africa

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Saudi Arabia MEA Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Dark Chocolate

- 7.1.2. Milk/ White Chocolate

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Boxed Assortments

- 7.2.2. Countlines

- 7.2.3. Seasonal Chocolates

- 7.2.4. Molded Chocolates

- 7.2.5. Other Product Types

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Supermarkets/ Hypermarkets

- 7.3.2. Specialty Stores

- 7.3.3. Convenience/Grocery Stores

- 7.3.4. Online Retail Stores

- 7.3.5. Other Distribution Channels

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. South Africa

- 7.4.2. Saudi Arabia

- 7.4.3. United Arab Emirates

- 7.4.4. Rest of Middle-East and Africa

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. United Arab Emirates MEA Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Dark Chocolate

- 8.1.2. Milk/ White Chocolate

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Boxed Assortments

- 8.2.2. Countlines

- 8.2.3. Seasonal Chocolates

- 8.2.4. Molded Chocolates

- 8.2.5. Other Product Types

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Supermarkets/ Hypermarkets

- 8.3.2. Specialty Stores

- 8.3.3. Convenience/Grocery Stores

- 8.3.4. Online Retail Stores

- 8.3.5. Other Distribution Channels

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. South Africa

- 8.4.2. Saudi Arabia

- 8.4.3. United Arab Emirates

- 8.4.4. Rest of Middle-East and Africa

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Rest of Middle East and Africa MEA Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Dark Chocolate

- 9.1.2. Milk/ White Chocolate

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Boxed Assortments

- 9.2.2. Countlines

- 9.2.3. Seasonal Chocolates

- 9.2.4. Molded Chocolates

- 9.2.5. Other Product Types

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Supermarkets/ Hypermarkets

- 9.3.2. Specialty Stores

- 9.3.3. Convenience/Grocery Stores

- 9.3.4. Online Retail Stores

- 9.3.5. Other Distribution Channels

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. South Africa

- 9.4.2. Saudi Arabia

- 9.4.3. United Arab Emirates

- 9.4.4. Rest of Middle-East and Africa

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. United Arab Emirates MEA Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 11. Saudi Arabia MEA Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 12. South Africa MEA Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 13. Rest of Middle East and Africa MEA Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 14. Competitive Analysis

- 14.1. Global Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 Nestle SA

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Tiger Brands Limited

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 Barry Callebaut

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 Ferrero Group

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 Chocoladefabriken Lindt & Sprungli AG

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Mars Incorporated

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Mondelez International Inc

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 Cocoa Processing Company Limited

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 Kees Beyers Chocolate CC*List Not Exhaustive

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 The Hershey Company

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.1 Nestle SA

List of Figures

- Figure 1: Global MEA Chocolate Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: MEA MEA Chocolate Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: MEA MEA Chocolate Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: South Africa MEA Chocolate Industry Revenue (Million), by Product 2024 & 2032

- Figure 5: South Africa MEA Chocolate Industry Revenue Share (%), by Product 2024 & 2032

- Figure 6: South Africa MEA Chocolate Industry Revenue (Million), by Type 2024 & 2032

- Figure 7: South Africa MEA Chocolate Industry Revenue Share (%), by Type 2024 & 2032

- Figure 8: South Africa MEA Chocolate Industry Revenue (Million), by Distribution Channel 2024 & 2032

- Figure 9: South Africa MEA Chocolate Industry Revenue Share (%), by Distribution Channel 2024 & 2032

- Figure 10: South Africa MEA Chocolate Industry Revenue (Million), by Geography 2024 & 2032

- Figure 11: South Africa MEA Chocolate Industry Revenue Share (%), by Geography 2024 & 2032

- Figure 12: South Africa MEA Chocolate Industry Revenue (Million), by Country 2024 & 2032

- Figure 13: South Africa MEA Chocolate Industry Revenue Share (%), by Country 2024 & 2032

- Figure 14: Saudi Arabia MEA Chocolate Industry Revenue (Million), by Product 2024 & 2032

- Figure 15: Saudi Arabia MEA Chocolate Industry Revenue Share (%), by Product 2024 & 2032

- Figure 16: Saudi Arabia MEA Chocolate Industry Revenue (Million), by Type 2024 & 2032

- Figure 17: Saudi Arabia MEA Chocolate Industry Revenue Share (%), by Type 2024 & 2032

- Figure 18: Saudi Arabia MEA Chocolate Industry Revenue (Million), by Distribution Channel 2024 & 2032

- Figure 19: Saudi Arabia MEA Chocolate Industry Revenue Share (%), by Distribution Channel 2024 & 2032

- Figure 20: Saudi Arabia MEA Chocolate Industry Revenue (Million), by Geography 2024 & 2032

- Figure 21: Saudi Arabia MEA Chocolate Industry Revenue Share (%), by Geography 2024 & 2032

- Figure 22: Saudi Arabia MEA Chocolate Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Saudi Arabia MEA Chocolate Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: United Arab Emirates MEA Chocolate Industry Revenue (Million), by Product 2024 & 2032

- Figure 25: United Arab Emirates MEA Chocolate Industry Revenue Share (%), by Product 2024 & 2032

- Figure 26: United Arab Emirates MEA Chocolate Industry Revenue (Million), by Type 2024 & 2032

- Figure 27: United Arab Emirates MEA Chocolate Industry Revenue Share (%), by Type 2024 & 2032

- Figure 28: United Arab Emirates MEA Chocolate Industry Revenue (Million), by Distribution Channel 2024 & 2032

- Figure 29: United Arab Emirates MEA Chocolate Industry Revenue Share (%), by Distribution Channel 2024 & 2032

- Figure 30: United Arab Emirates MEA Chocolate Industry Revenue (Million), by Geography 2024 & 2032

- Figure 31: United Arab Emirates MEA Chocolate Industry Revenue Share (%), by Geography 2024 & 2032

- Figure 32: United Arab Emirates MEA Chocolate Industry Revenue (Million), by Country 2024 & 2032

- Figure 33: United Arab Emirates MEA Chocolate Industry Revenue Share (%), by Country 2024 & 2032

- Figure 34: Rest of Middle East and Africa MEA Chocolate Industry Revenue (Million), by Product 2024 & 2032

- Figure 35: Rest of Middle East and Africa MEA Chocolate Industry Revenue Share (%), by Product 2024 & 2032

- Figure 36: Rest of Middle East and Africa MEA Chocolate Industry Revenue (Million), by Type 2024 & 2032

- Figure 37: Rest of Middle East and Africa MEA Chocolate Industry Revenue Share (%), by Type 2024 & 2032

- Figure 38: Rest of Middle East and Africa MEA Chocolate Industry Revenue (Million), by Distribution Channel 2024 & 2032

- Figure 39: Rest of Middle East and Africa MEA Chocolate Industry Revenue Share (%), by Distribution Channel 2024 & 2032

- Figure 40: Rest of Middle East and Africa MEA Chocolate Industry Revenue (Million), by Geography 2024 & 2032

- Figure 41: Rest of Middle East and Africa MEA Chocolate Industry Revenue Share (%), by Geography 2024 & 2032

- Figure 42: Rest of Middle East and Africa MEA Chocolate Industry Revenue (Million), by Country 2024 & 2032

- Figure 43: Rest of Middle East and Africa MEA Chocolate Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global MEA Chocolate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global MEA Chocolate Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 3: Global MEA Chocolate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: Global MEA Chocolate Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 5: Global MEA Chocolate Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 6: Global MEA Chocolate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: Global MEA Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: United Arab Emirates MEA Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Saudi Arabia MEA Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: South Africa MEA Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Rest of Middle East and Africa MEA Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Global MEA Chocolate Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 13: Global MEA Chocolate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 14: Global MEA Chocolate Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 15: Global MEA Chocolate Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 16: Global MEA Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: Global MEA Chocolate Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 18: Global MEA Chocolate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 19: Global MEA Chocolate Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 20: Global MEA Chocolate Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 21: Global MEA Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Global MEA Chocolate Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 23: Global MEA Chocolate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 24: Global MEA Chocolate Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 25: Global MEA Chocolate Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 26: Global MEA Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Global MEA Chocolate Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 28: Global MEA Chocolate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 29: Global MEA Chocolate Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 30: Global MEA Chocolate Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 31: Global MEA Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the MEA Chocolate Industry?

The projected CAGR is approximately 6.72%.

2. Which companies are prominent players in the MEA Chocolate Industry?

Key companies in the market include Nestle SA, Tiger Brands Limited, Barry Callebaut, Ferrero Group, Chocoladefabriken Lindt & Sprungli AG, Mars Incorporated, Mondelez International Inc, Cocoa Processing Company Limited, Kees Beyers Chocolate CC*List Not Exhaustive, The Hershey Company.

3. What are the main segments of the MEA Chocolate Industry?

The market segments include Product, Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Government Initiatives and E-commerce Penetration.

6. What are the notable trends driving market growth?

Countlines and Premium Dark Chocolates Hold a Major Market Share.

7. Are there any restraints impacting market growth?

Detrimental Health Impact of Caffeine Intake.

8. Can you provide examples of recent developments in the market?

In March 2022, Barry Callebaut launched its line of whole-fruit chocolates under the Cacao Barry brand in the United Arab Emirates. The product has 40% less sugar than conventional dark chocolate and is made from 100% pure cacao fruit. The company partnered with Cabosse Naturals, who work closely with local cacao fruit farmers in Ecuador, to source the upcycled cacao fruit pulp and peels for the product.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "MEA Chocolate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the MEA Chocolate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the MEA Chocolate Industry?

To stay informed about further developments, trends, and reports in the MEA Chocolate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence