Key Insights

The global Merchant Ship Coating market is poised for substantial expansion, projected to reach an estimated USD 10.2 billion in 2025, driven by robust growth at a CAGR of 11.86%. This upward trajectory is largely attributed to the increasing demand for maritime trade, which necessitates a larger fleet of vessels and, consequently, a greater need for protective coatings. Key drivers include the growing emphasis on vessel longevity and performance, stringent environmental regulations demanding eco-friendly and low-VOC (Volatile Organic Compound) coatings, and advancements in coating technologies offering enhanced durability, corrosion resistance, and antifouling properties. The burgeoning offshore wind energy sector also contributes significantly, requiring specialized coatings for offshore structures and vessels involved in their installation and maintenance. Furthermore, the ongoing modernization of existing fleets and the construction of new, larger, and more efficient ships are continually fueling the demand for high-performance marine coatings.

Merchant Ship Coating Market Size (In Billion)

The market segmentation reveals distinct opportunities across various applications and coating types. Commercial vessels, encompassing bulk carriers, tankers, and container ships, represent the largest segment due to the sheer volume of global shipping. Military vessels, while smaller in volume, represent a high-value segment due to the demanding performance requirements and advanced coating technologies employed. Civilian vessels, including yachts and recreational boats, also contribute to market growth, albeit to a lesser extent. In terms of coating types, antifouling coatings are crucial for preventing the growth of marine organisms on hulls, thereby improving fuel efficiency and reducing maintenance costs. Anticorrosive coatings play a vital role in protecting steel structures from the harsh marine environment. Emerging trends such as smart coatings with self-healing properties and the increasing adoption of sustainable and bio-based coating solutions are shaping the future landscape of the Merchant Ship Coating market. However, the market faces restraints such as volatile raw material prices and the high cost of initial coating application, which can impact adoption rates, especially for smaller operators.

Merchant Ship Coating Company Market Share

Merchant Ship Coating Market Outlook: Global Industry Analysis & Forecast 2019-2033

Unlock unparalleled insights into the dynamic global Merchant Ship Coating market with our comprehensive, SEO-optimized report. Covering the historical period from 2019-2024 and projecting growth through 2033, this report delves into market dynamics, growth trends, regional dominance, and product innovations. Essential for industry professionals, investors, and stakeholders, this analysis provides actionable intelligence for strategic decision-making.

Merchant Ship Coating Market Dynamics & Structure

The global Merchant Ship Coating market is characterized by a moderately consolidated structure, with a few key players holding significant market share, alongside a robust presence of specialized and regional manufacturers. Technological innovation is a primary driver, particularly in the development of advanced antifouling coatings that reduce fuel consumption and environmental impact. Regulatory frameworks, such as International Maritime Organization (IMO) regulations on volatile organic compounds (VOCs) and biocide usage, are shaping product development and market entry strategies. Competitive product substitutes are emerging in the form of advanced hull cleaning technologies and in-water maintenance solutions, posing a challenge to traditional coating segments. End-user demographics are increasingly focused on sustainability, cost-efficiency, and extended asset lifespan, driving demand for high-performance and eco-friendly coating solutions. Mergers and acquisitions (M&A) activity is notable, as larger companies aim to consolidate market presence, expand their product portfolios, and gain access to new technologies. For instance, M&A deal volumes in the broader marine coatings sector have seen a steady increase over the past five years, with key transactions aimed at integrating innovative solutions and expanding geographical reach.

- Market Concentration: Moderate, with leading players like AkzoNobel, PPG, and Sherwin-Williams holding substantial market influence.

- Technological Innovation Drivers: Focus on eco-friendly biocides, silicone-based foul-release coatings, and nanotechnology for enhanced durability and performance.

- Regulatory Frameworks: IMO regulations (e.g., Ballast Water Management Convention, upcoming GHG reduction targets) significantly influence coating choices.

- Competitive Product Substitutes: Robotic hull cleaning, in-water maintenance services, and advanced propeller coatings.

- End-User Demographics: Growing demand for reduced operational costs, extended dry-docking intervals, and compliance with stringent environmental standards.

- M&A Trends: Strategic acquisitions to gain market share, access new technologies, and expand product offerings in the advanced coatings segment.

Merchant Ship Coating Growth Trends & Insights

The global Merchant Ship Coating market is poised for robust expansion, driven by increasing global trade and the demand for efficient marine transportation. The market size, estimated at $15.5 billion in 2025, is projected to reach $21.2 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 4.5% during the forecast period. This growth is underpinned by several critical trends. Firstly, the expansion of global shipping fleets, particularly in the dry bulk and container segments, directly translates to increased demand for protective and performance-enhancing coatings. Secondly, a heightened awareness of environmental regulations and the urgent need to reduce greenhouse gas emissions are compelling shipowners to adopt advanced antifouling coatings. These coatings significantly reduce hull friction, leading to substantial fuel savings and a corresponding decrease in carbon emissions. The adoption rate of these advanced coatings is steadily increasing, moving from niche applications to mainstream fleet-wide implementation.

Technological disruptions are playing a pivotal role. The development of self-polishing copolymer (SPC) antifouling coatings and silicone-based foul-release technologies has revolutionized the industry, offering longer service life and improved performance compared to traditional biocidal coatings. Furthermore, the integration of nano-materials into coatings is enhancing their durability, corrosion resistance, and anti-fouling properties, creating a competitive edge for manufacturers investing in R&D. Consumer behavior is also shifting. Shipowners are increasingly prioritizing long-term operational cost savings over initial product price. This includes factoring in reduced fuel consumption, extended periods between dry-docking, and the avoidance of costly hull damage. The lifecycle cost analysis of coatings is becoming a dominant factor in purchasing decisions. The focus on sustainability extends beyond fuel efficiency to include the environmental impact of coating application and disposal. This has spurred innovation in low-VOC and solvent-free coating formulations. The Commercial Vessels segment, encompassing bulk carriers, tankers, and container ships, is expected to dominate the market due to its sheer volume and continuous operational demands. Within this, Antifouling Coating is the largest segment by value, driven by the critical need for fuel efficiency and reduced environmental impact. The parent market of marine coatings itself is substantial, with the merchant ship segment representing a significant portion of this larger industry. The child market of specialized coatings for specific vessel types or applications, such as ice-class coatings or coatings for offshore structures, is also experiencing niche growth. The increasing complexity of shipbuilding and the demand for tailored solutions are creating opportunities for specialized coating providers.

Dominant Regions, Countries, or Segments in Merchant Ship Coating

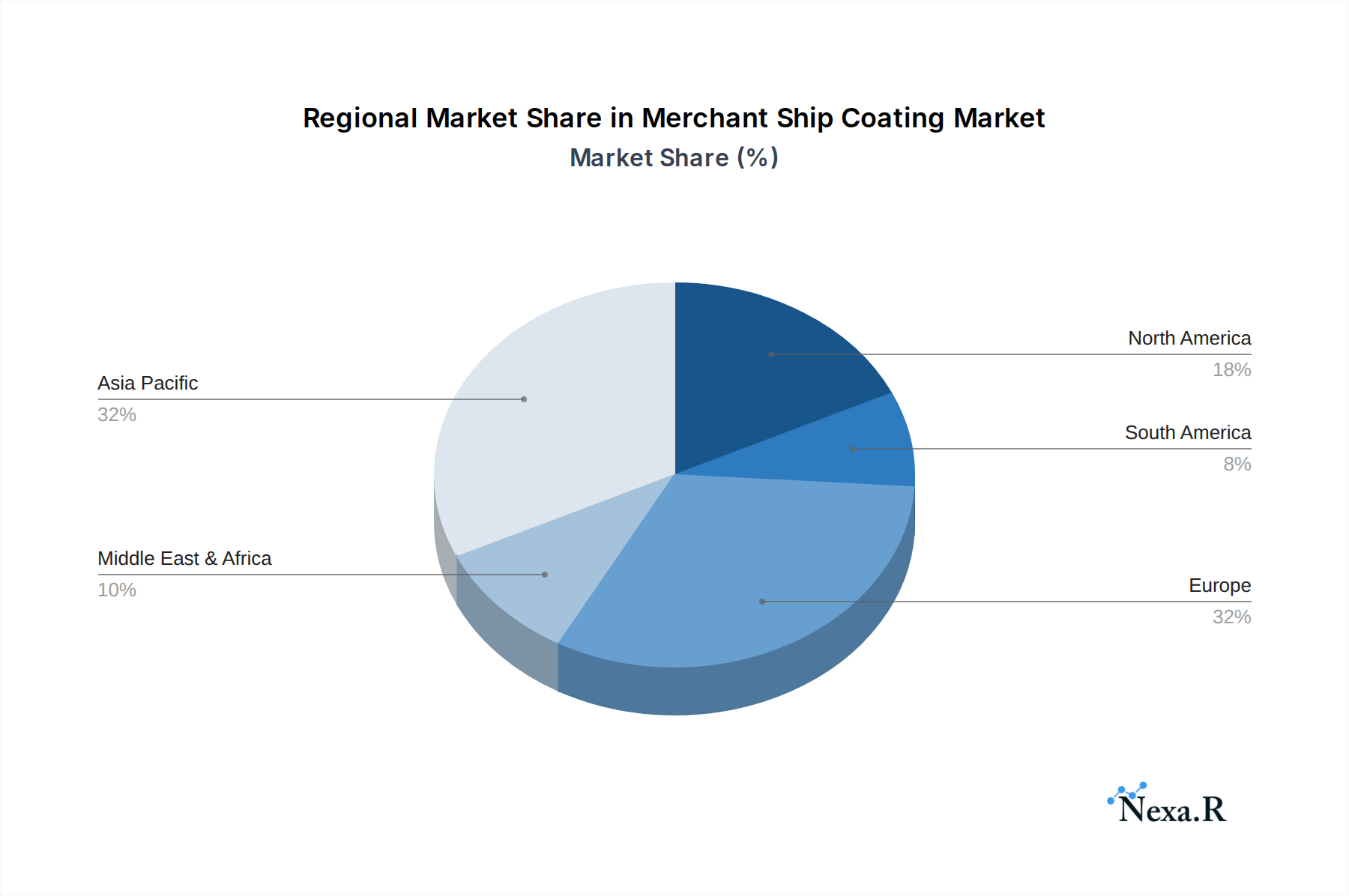

The Asia-Pacific region stands as the undisputed leader in the Merchant Ship Coating market, driven by its colossal shipbuilding capacity and a burgeoning fleet. Countries like China, South Korea, and Japan are global powerhouses in vessel construction, directly translating into immense demand for marine coatings. Furthermore, the region's extensive coastline and its pivotal role in global trade necessitate a continuous need for maintaining and protecting a vast number of commercial vessels. The economic policies and infrastructure development within these nations, focused on bolstering their maritime sectors, act as significant catalysts for market growth. For example, China's "Belt and Road Initiative" has spurred significant investment in port infrastructure and shipping, further augmenting the demand for ship coatings.

Within the broader Application segment, Commercial Vessels are the dominant force, accounting for an estimated 75% of the total market value in 2025. This segment includes bulk carriers, container ships, tankers (oil, chemical, and gas), and general cargo ships, all of which require extensive and high-performance protective coatings for prolonged operational life and efficiency. The sheer volume of these vessels and their continuous operation in diverse marine environments create a perpetual demand for coatings. The Types segment is spearheaded by Antifouling Coating, estimated to hold 55% market share by value in 2025. This dominance is attributed to the critical role antifouling coatings play in reducing drag, thereby enhancing fuel efficiency and lowering greenhouse gas emissions, a paramount concern for shipowners navigating stringent environmental regulations. The market penetration of advanced antifouling technologies, such as silicone-based foul-release coatings and self-polishing copolymers (SPC), is particularly high in this segment. The growing environmental consciousness and the economic benefits of fuel savings are compelling even traditional operators to transition to these superior coating solutions.

- Dominant Region: Asia-Pacific (China, South Korea, Japan) due to extensive shipbuilding and a large merchant fleet.

- Dominant Application Segment: Commercial Vessels, driven by the massive global fleet size and operational demands.

- Dominant Type Segment: Antifouling Coating, crucial for fuel efficiency, environmental compliance, and extended hull protection.

- Key Drivers in Asia-Pacific: Government support for maritime industries, strong shipbuilding infrastructure, and increasing international trade.

- Market Share of Antifouling Coating: Projected at 55% of the total market value in 2025, highlighting its critical importance.

- Growth Potential in Commercial Vessels: Continual fleet expansion and the increasing lifespan requirements of vessels.

Merchant Ship Coating Product Landscape

The merchant ship coating product landscape is evolving rapidly, focusing on enhanced performance, environmental compliance, and extended service life. Innovations include the development of advanced antifouling coatings leveraging copper and biocide-free technologies, such as silicone-based foul-release systems, which minimize marine growth and reduce drag without releasing harmful substances into the water. Anticorrosive coatings are incorporating novel resin technologies and inhibitive pigments to provide superior protection against aggressive marine environments, extending the intervals between dry-docking. Other specialized coatings are emerging for specific applications, such as ice-resistant coatings for Arctic vessels and friction-reducing coatings for ballast tanks. The unique selling propositions of these products lie in their ability to deliver quantifiable benefits like significant fuel savings (up to 10%), reduced maintenance costs, and compliance with increasingly stringent environmental regulations like the IMO's Ballast Water Management Convention.

Key Drivers, Barriers & Challenges in Merchant Ship Coating

Key Drivers:

- Increasing Global Trade & Fleet Expansion: A growing demand for goods necessitates larger and more numerous merchant vessels, directly driving coating demand.

- Stringent Environmental Regulations: IMO mandates for reduced emissions and biocide use push for the adoption of advanced, eco-friendly coatings.

- Fuel Efficiency Imperative: Shipowners are actively seeking coatings that reduce hull friction and thereby lower fuel consumption and operational costs.

- Technological Advancements: Development of high-performance antifouling and anticorrosive coatings with longer lifespans.

Barriers & Challenges:

- High Initial Cost of Advanced Coatings: The upfront investment for premium performance coatings can be a barrier for some operators, especially in competitive freight markets.

- Economic Downturns & Volatile Shipping Rates: Fluctuations in the global economy can impact new build orders and dry-docking schedules, affecting coating demand.

- Supply Chain Disruptions: Raw material shortages and logistical challenges can impact production and delivery timelines for coating manufacturers.

- Resistance to Change: Some operators may be hesitant to adopt new coating technologies due to familiarity with existing solutions and perceived risks.

- Skilled Labor Shortage: The application of advanced coatings often requires specialized training and expertise, leading to potential labor constraints.

Emerging Opportunities in Merchant Ship Coating

Emerging opportunities lie in the development of sustainable and smart coating solutions. The increasing focus on the circular economy within the maritime industry presents a significant avenue for innovation in coatings that are easier to remove, recycle, or are biodegradable. The integration of IoT sensors within coatings to monitor hull performance, corrosion levels, and fouling in real-time offers predictive maintenance capabilities, a highly sought-after feature by fleet managers. Untapped markets include specialized coatings for the burgeoning offshore renewable energy sector (e.g., wind farms) and the increasing demand for coatings that can withstand extreme environmental conditions in polar regions. Furthermore, there's a growing preference for localized supply chains and service networks, creating opportunities for regional players to expand their offerings.

Growth Accelerators in the Merchant Ship Coating Industry

The merchant ship coating industry's growth is being significantly accelerated by several key factors. Firstly, the continuous push for decarbonization within the shipping sector is a primary catalyst, driving demand for antifouling coatings that directly contribute to fuel savings and reduced emissions. This is further amplified by stricter international regulations. Secondly, ongoing technological breakthroughs in coating formulations, such as advanced biocide delivery systems and novel fouling-release materials, are enhancing product efficacy and lifespan, making them more attractive to shipowners. Strategic partnerships between coating manufacturers and shipyards, as well as collaborations with research institutions, are fostering innovation and accelerating the adoption of new technologies. Market expansion strategies, including penetration into emerging shipping routes and catering to the specific needs of diverse vessel types, are also playing a crucial role in driving sustained growth.

Key Players Shaping the Merchant Ship Coating Market

PPG Sherwin-Williams AkzoNobel BASF Nippon Paint Hempel Jotun Chugoku Marine Paints RPM International KCC Corporation Brunel Marine Coating Systems Lanxess Selektope Boero VENEZIANI Sea Hawk Paints Kop-Coat Soromap PLASTIMO Janssen PMP Coppercoat

Notable Milestones in Merchant Ship Coating Sector

- 2019: Increased global focus on IMO's 2020 Sulphur cap, indirectly promoting fuel-efficient operations and consequently advanced coatings.

- 2020: Launch of new biocide-free antifouling technologies by leading manufacturers, responding to environmental concerns.

- 2021: Growing adoption of silicone-based foul-release coatings for container ships and tankers to optimize fuel efficiency.

- 2022: Intensified research and development into nano-enhanced coatings for superior durability and self-cleaning properties.

- 2023: Strategic acquisitions aimed at consolidating market share and expanding product portfolios in the antifouling and anticorrosive segments.

- 2024: Increased emphasis on digitalization in coating application and monitoring through smart technologies and IoT integration.

In-Depth Merchant Ship Coating Market Outlook

The merchant ship coating market is set for sustained and robust growth, driven by a confluence of increasing global trade, stringent environmental mandates, and relentless technological innovation. The imperative for fuel efficiency and decarbonization will continue to propel the adoption of advanced antifouling solutions, with silicone-based and biocide-free technologies gaining further traction. Strategic collaborations and mergers will consolidate the market, while continuous R&D in areas like nano-coatings and smart functionalities will unlock new performance benchmarks. The focus on lifecycle cost optimization and sustainable practices will redefine purchasing decisions, creating significant opportunities for companies that can deliver demonstrable value and environmental stewardship. The overall outlook is highly positive, indicating a dynamic and evolving market with substantial potential for growth and innovation.

Merchant Ship Coating Segmentation

-

1. Application

- 1.1. Commercial Vessels

- 1.2. Military Vessels

- 1.3. Civilian Vessels

-

2. Types

- 2.1. Antifouling Coating

- 2.2. Anticorrosive Coating

- 2.3. Other

Merchant Ship Coating Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Merchant Ship Coating Regional Market Share

Geographic Coverage of Merchant Ship Coating

Merchant Ship Coating REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.86% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Merchant Ship Coating Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Vessels

- 5.1.2. Military Vessels

- 5.1.3. Civilian Vessels

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Antifouling Coating

- 5.2.2. Anticorrosive Coating

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Merchant Ship Coating Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Vessels

- 6.1.2. Military Vessels

- 6.1.3. Civilian Vessels

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Antifouling Coating

- 6.2.2. Anticorrosive Coating

- 6.2.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Merchant Ship Coating Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Vessels

- 7.1.2. Military Vessels

- 7.1.3. Civilian Vessels

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Antifouling Coating

- 7.2.2. Anticorrosive Coating

- 7.2.3. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Merchant Ship Coating Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Vessels

- 8.1.2. Military Vessels

- 8.1.3. Civilian Vessels

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Antifouling Coating

- 8.2.2. Anticorrosive Coating

- 8.2.3. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Merchant Ship Coating Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Vessels

- 9.1.2. Military Vessels

- 9.1.3. Civilian Vessels

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Antifouling Coating

- 9.2.2. Anticorrosive Coating

- 9.2.3. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Merchant Ship Coating Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Vessels

- 10.1.2. Military Vessels

- 10.1.3. Civilian Vessels

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Antifouling Coating

- 10.2.2. Anticorrosive Coating

- 10.2.3. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 PPG

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Sherwin-Williams

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AkzoNobel

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 BASF

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Nippon Paint

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hempel

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Jotun

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Chugoku Marine Paints

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 RPM International

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 KCC Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Brunel Marine Coating Systems

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Lanxess

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Selektope

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Boero

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 VENEZIANI

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Sea Hawk Paints

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Kop-Coat

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Soromap

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 PLASTIMO

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Janssen PMP

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Coppercoat

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 PPG

List of Figures

- Figure 1: Global Merchant Ship Coating Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Merchant Ship Coating Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Merchant Ship Coating Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Merchant Ship Coating Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Merchant Ship Coating Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Merchant Ship Coating Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Merchant Ship Coating Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Merchant Ship Coating Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Merchant Ship Coating Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Merchant Ship Coating Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Merchant Ship Coating Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Merchant Ship Coating Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Merchant Ship Coating Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Merchant Ship Coating Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Merchant Ship Coating Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Merchant Ship Coating Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Merchant Ship Coating Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Merchant Ship Coating Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Merchant Ship Coating Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Merchant Ship Coating Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Merchant Ship Coating Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Merchant Ship Coating Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Merchant Ship Coating Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Merchant Ship Coating Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Merchant Ship Coating Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Merchant Ship Coating Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Merchant Ship Coating Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Merchant Ship Coating Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Merchant Ship Coating Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Merchant Ship Coating Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Merchant Ship Coating Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Merchant Ship Coating Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Merchant Ship Coating Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Merchant Ship Coating Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Merchant Ship Coating Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Merchant Ship Coating Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Merchant Ship Coating Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Merchant Ship Coating Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Merchant Ship Coating Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Merchant Ship Coating Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Merchant Ship Coating Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Merchant Ship Coating Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Merchant Ship Coating Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Merchant Ship Coating Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Merchant Ship Coating Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Merchant Ship Coating Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Merchant Ship Coating Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Merchant Ship Coating Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Merchant Ship Coating Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Merchant Ship Coating Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Merchant Ship Coating?

The projected CAGR is approximately 11.86%.

2. Which companies are prominent players in the Merchant Ship Coating?

Key companies in the market include PPG, Sherwin-Williams, AkzoNobel, BASF, Nippon Paint, Hempel, Jotun, Chugoku Marine Paints, RPM International, KCC Corporation, Brunel Marine Coating Systems, Lanxess, Selektope, Boero, VENEZIANI, Sea Hawk Paints, Kop-Coat, Soromap, PLASTIMO, Janssen PMP, Coppercoat.

3. What are the main segments of the Merchant Ship Coating?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.2 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Merchant Ship Coating," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Merchant Ship Coating report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Merchant Ship Coating?

To stay informed about further developments, trends, and reports in the Merchant Ship Coating, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence