Key Insights

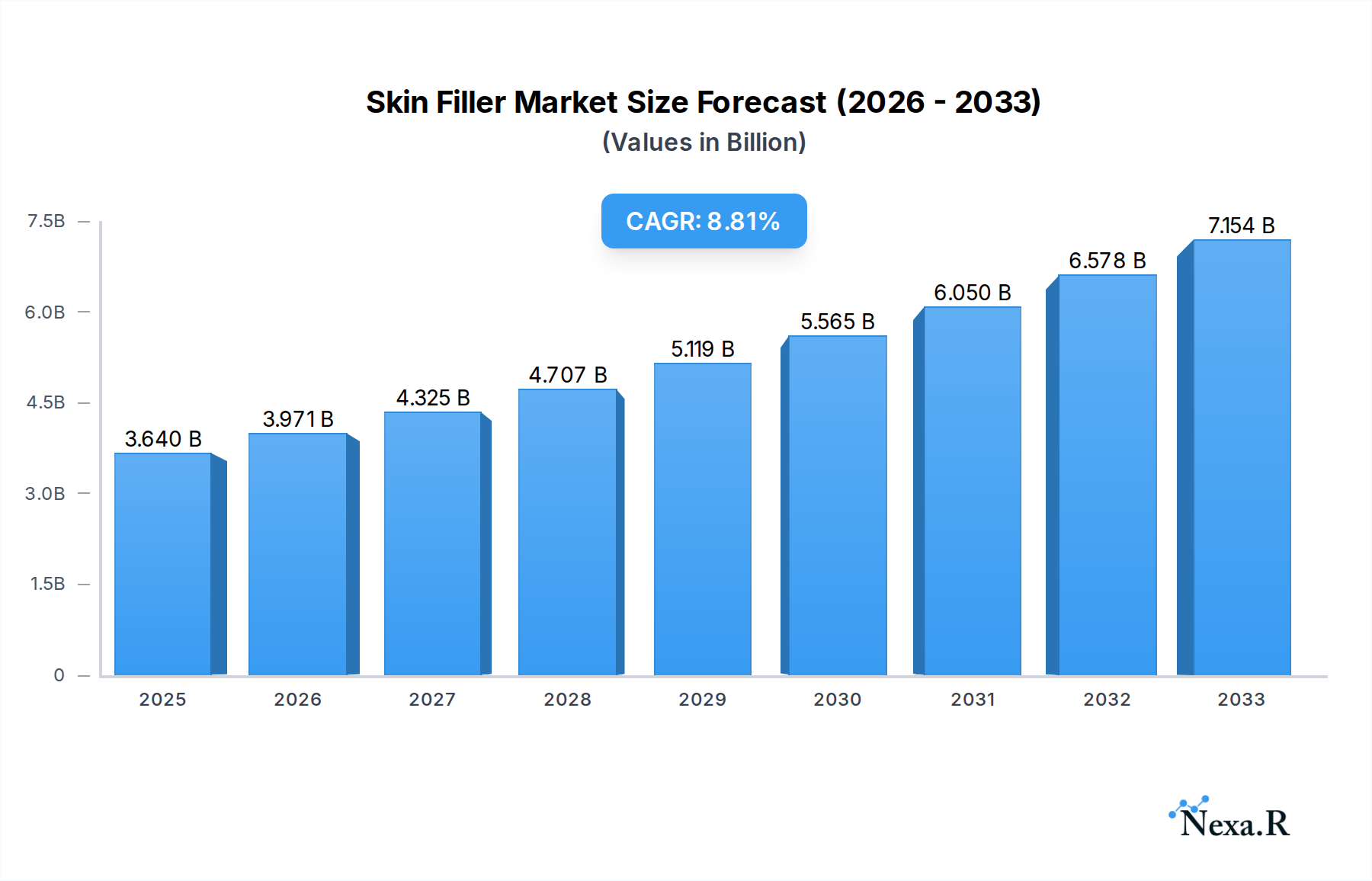

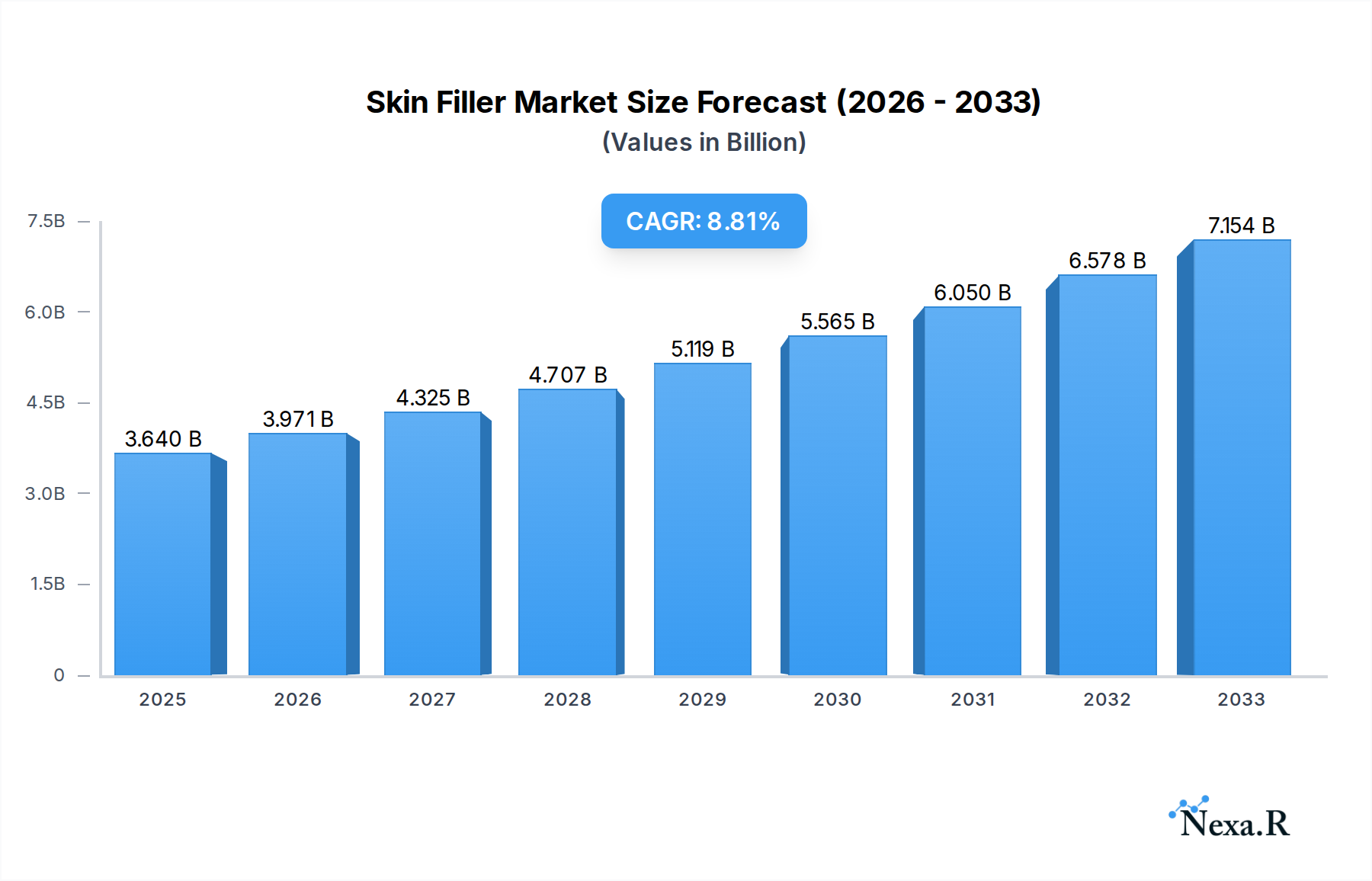

The global skin filler market is poised for significant expansion, projected to reach USD 3.64 billion in 2025 and grow at a robust CAGR of 9.25% through 2033. This impressive growth is fueled by an escalating demand for minimally invasive aesthetic procedures and a heightened consumer awareness regarding anti-aging solutions. The market is segmented by application, with micro-plastic and cosmetic applications, and anti-aging treatments dominating the landscape. The increasing adoption of hyaluronic acid (HA) fillers, known for their efficacy and safety profile, is a primary driver, alongside the growing popularity of calcium hydroxylapatite (CaHA) and poly-L-lactic acid (PLLA) for their long-lasting results. Innovations in filler formulations, including biodegradable and bio-stimulating options, are further propelling market growth, catering to a diverse range of patient needs and preferences.

Skin Filler Market Size (In Billion)

Several key trends are shaping the trajectory of the skin filler market. The rising disposable income across emerging economies, coupled with a growing emphasis on personal grooming and appearance, is creating new avenues for market penetration. Moreover, advancements in injection techniques and the development of novel filler compositions are enhancing treatment outcomes and patient satisfaction, thereby encouraging repeat usage. Leading companies such as Allergan, Galderma, and LG Life Science are actively investing in research and development, introducing advanced products and expanding their global presence. While the market exhibits strong growth potential, certain factors such as stringent regulatory approvals for new products and the potential for adverse effects, though rare, could pose minor challenges. However, the overall outlook remains exceptionally positive, driven by an aging global population and an enduring desire for youthful and radiant skin.

Skin Filler Company Market Share

Skin Filler Market Dynamics & Structure

The global Skin Filler market exhibits a moderate concentration, driven by continuous technological innovation and evolving regulatory frameworks across major economies. Key players like Allergan, Galderma, LG Life Science, Merz, Medytox, Bloomage, Bohus BioTech, Sinclair Pharma, IMEIK, Suneva Medical, and others are actively engaged in research and development to introduce novel formulations and enhance product efficacy. The competitive landscape is characterized by both in-house innovation and strategic acquisitions, aimed at expanding product portfolios and market reach. Barriers to entry include stringent regulatory approvals, substantial R&D investment requirements, and the need for extensive clinical validation. End-user demographics are increasingly shifting towards a younger, more proactive consumer base seeking preventative anti-aging solutions and aesthetic enhancements, influencing product development towards minimally invasive and natural-looking results. M&A trends are particularly pronounced in emerging markets, as established companies seek to gain a foothold through strategic partnerships and acquisitions of local leaders.

- Market Concentration: Moderate, with key players holding significant but not monopolistic market share.

- Technological Innovation Drivers: Development of advanced formulations, longer-lasting fillers, and improved safety profiles.

- Regulatory Frameworks: Stringent approval processes by bodies like the FDA and EMA, influencing product development timelines and market access.

- Competitive Product Substitutes: Growing competition from non-invasive treatments and advanced skincare technologies.

- End-User Demographics: Increasing demand from millennials and Gen Z for preventative anti-aging and subtle aesthetic enhancements.

- M&A Trends: Strategic acquisitions focused on expanding geographical presence and acquiring innovative technologies.

Skin Filler Growth Trends & Insights

The Skin Filler market is poised for robust expansion, driven by an escalating global demand for aesthetic procedures and an increasing acceptance of cosmetic enhancements across diverse age groups. The market size is projected to witness substantial growth, fueled by innovations in hyaluronic acid (HA) fillers, which currently dominate due to their safety profile, reversibility, and natural appearance. The adoption rates for skin fillers are steadily rising, not only in developed nations but also in emerging economies where disposable incomes are growing, and awareness of aesthetic treatments is increasing. Technological disruptions are a significant factor, with ongoing research into bio-stimulatory fillers like Poly-L-Lactic Acid (PLLA) and Calcium Hydroxylapatite (CaHA) offering longer-lasting results and stimulating collagen production. Consumer behavior shifts are marked by a preference for subtle, natural-looking results over dramatic transformations, leading manufacturers to develop more nuanced product lines. The market penetration of skin fillers, particularly in the micro-plastic and cosmetic application segment, is expected to deepen as accessibility improves and societal stigma diminishes. CAGR for the Skin Filler market is estimated at XX% from 2025 to 2033, reflecting this dynamic growth trajectory. The historical period (2019–2024) saw a steady recovery and initial growth post-pandemic, setting the stage for accelerated expansion in the forecast period. The base year of 2025 estimates the market at approximately $15.7 billion, with projections reaching $30.1 billion by 2033. This significant increase is underpinned by a growing preference for minimally invasive procedures over surgical alternatives, further propelled by advancements in injection techniques and post-treatment recovery times. The rise of aesthetic clinics and spas, coupled with aggressive marketing by key players, also contributes to higher adoption rates. Furthermore, the diversification of product offerings to cater to specific needs, such as lip augmentation, wrinkle reduction, and facial contouring, broadens the appeal to a wider consumer base. The influence of social media and celebrity endorsements continues to play a crucial role in shaping consumer perceptions and driving demand for these aesthetic treatments. The development of combination therapies, integrating skin fillers with other aesthetic modalities, is also expected to contribute to market growth.

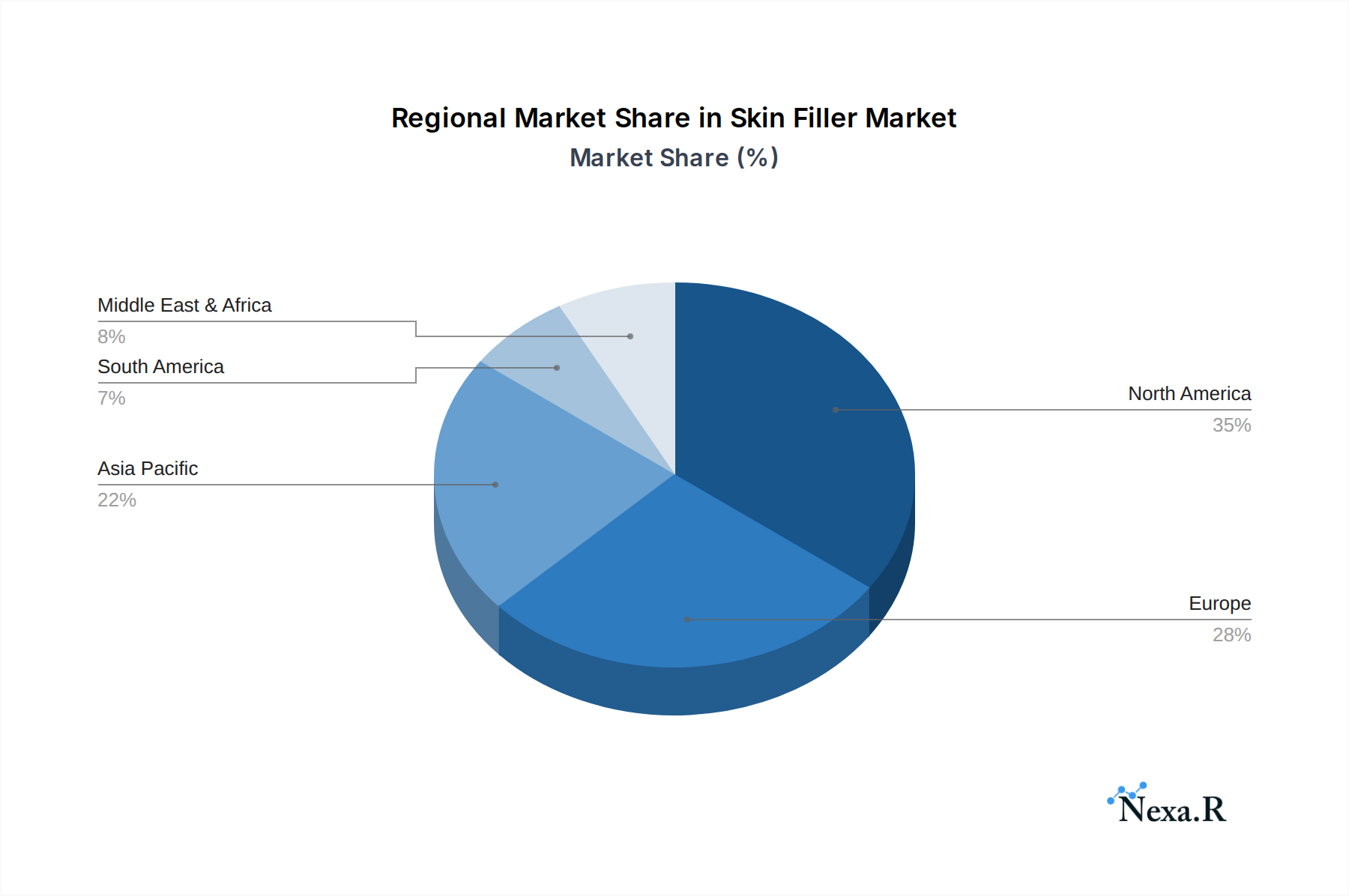

Dominant Regions, Countries, or Segments in Skin Filler

The global Skin Filler market is significantly influenced by regional economic strength, regulatory landscapes, and evolving consumer preferences. North America, particularly the United States, stands as the leading region in terms of market share and growth potential. This dominance is attributed to a combination of high disposable incomes, a well-established aesthetic industry, a high level of consumer awareness regarding cosmetic procedures, and the presence of major industry players with robust R&D capabilities. The application segment of Micro-plastic and Cosmetic procedures is the primary growth driver in this region, encompassing a wide range of treatments from wrinkle reduction to facial contouring and lip augmentation.

Hyaluronic Acid (HA) fillers remain the dominant type, owing to their excellent safety profile, biocompatibility, and reversible nature. Their widespread acceptance by both practitioners and patients contributes to their continued market leadership. However, there is a growing interest and adoption of PLLA and CaHA fillers, especially for applications requiring longer-lasting results and collagen stimulation.

Key drivers for North America's dominance include:

- High Disposable Income: Enabling a larger segment of the population to afford elective aesthetic procedures.

- Advanced Healthcare Infrastructure: Facilitating access to skilled practitioners and state-of-the-art clinics.

- Strong Regulatory Approval Pathways: While rigorous, the FDA's approval process, once met, often instills significant consumer confidence.

- Aggressive Marketing and Education: Leading manufacturers and aesthetic practices actively engage in consumer education and promotional activities.

- Cultural Acceptance: A generally more open societal attitude towards cosmetic enhancements compared to some other regions.

In terms of country-specific dominance, the United States leads, followed by key European markets like Germany, the UK, and France. Within Asia, China is emerging as a significant market due to its large population, increasing urbanization, and rising disposable incomes. The growth potential in emerging markets is substantial, driven by a desire to emulate Western beauty standards and the increasing availability of advanced treatments.

The Anti-Aging application segment is also experiencing rapid growth globally, as the aging population in many countries seeks ways to maintain a youthful appearance. This trend is particularly strong in regions with a higher proportion of older adults. The "Other" application segment, which includes reconstructive procedures and medical indications beyond purely cosmetic ones, also contributes to overall market volume, though at a slower pace.

The market share for HA fillers is estimated to be around 70% of the total market in 2025, with PLLA and CaHA collectively holding approximately 25%. The remaining 5% is attributed to PMMA and other filler types. The Micro-plastic and Cosmetic segment accounts for approximately 80% of the total application market, with Anti-Aging comprising the remaining 20%.

Skin Filler Product Landscape

The Skin Filler product landscape is characterized by continuous innovation, focusing on enhancing efficacy, safety, and patient experience. Hyaluronic Acid (HA) fillers remain the cornerstone, with advancements in cross-linking technologies leading to improved longevity and rheological properties, allowing for precise volumetric correction and contouring. Innovations extend to formulations offering varying particle sizes and cohesivities, tailored for specific treatment areas like the lips, cheeks, and tear troughs. Beyond HA, Poly-L-Lactic Acid (PLLA) and Calcium Hydroxylapatite (CaHA) fillers are gaining traction for their ability to stimulate the body's natural collagen production, offering more gradual and natural-looking rejuvenation over time. These bio-stimulatory fillers represent a significant technological leap, providing longer-lasting results. The product portfolio is expanding to include advanced delivery systems and anaesthetic additives, minimizing patient discomfort during procedures.

Key Drivers, Barriers & Challenges in Skin Filler

The Skin Filler market is propelled by several key drivers, including an escalating global demand for aesthetic and anti-aging treatments, driven by increasing disposable incomes and a growing acceptance of cosmetic enhancements. Technological advancements in filler formulations, offering improved safety profiles, longer-lasting results, and more natural outcomes, are crucial growth catalysts.

- Technological Advancements: Development of novel formulations (e.g., bio-stimulatory fillers), improved delivery systems, and enhanced longevity.

- Growing Consumer Awareness & Acceptance: Increased media coverage, social media influence, and a desire for aesthetic improvement.

- Minimally Invasive Procedures: Preference for non-surgical options with shorter recovery times.

- Aging Global Population: A significant demographic driving demand for anti-aging solutions.

Conversely, the market faces significant barriers and challenges:

- Stringent Regulatory Approvals: Lengthy and costly approval processes by health authorities worldwide.

- Potential Side Effects & Complications: Risks associated with injections, such as bruising, swelling, infection, and rare but serious adverse events, necessitating skilled practitioners.

- High Cost of Treatments: Making them inaccessible for a significant portion of the global population.

- Intense Competition: From both established players and new entrants, leading to pricing pressures.

- Supply Chain Disruptions: Potential challenges in sourcing raw materials and ensuring consistent product availability globally.

- Public Perception & Stigma: While declining, some societal stigma still exists around cosmetic procedures.

Emerging Opportunities in Skin Filler

Emerging opportunities in the Skin Filler market lie in the development of personalized treatment approaches, catering to unique individual aesthetic goals and physiological responses. The expansion of bio-stimulatory fillers with enhanced collagen induction capabilities presents a significant avenue for long-term rejuvenation. Untapped markets in developing economies, where awareness and disposable income are rising, offer substantial growth potential. Furthermore, innovations in combination therapies, integrating fillers with other aesthetic modalities like laser treatments and energy-based devices, are poised to create new revenue streams and cater to comprehensive patient needs. The development of novel delivery mechanisms that ensure even distribution and minimize trauma is also a promising area.

Growth Accelerators in the Skin Filler Industry

Long-term growth in the Skin Filler industry will be significantly accelerated by breakthroughs in regenerative medicine and biomaterials, leading to fillers that not only provide volume but also actively repair and rejuvenate skin tissue at a cellular level. Strategic partnerships between leading filler manufacturers and aesthetic device companies will foster the development of integrated treatment protocols, enhancing patient outcomes and broadening market appeal. Furthermore, the expansion of minimally invasive cosmetic surgery training programs globally will increase the pool of qualified practitioners, making advanced filler treatments more accessible and driving market penetration, especially in underserved regions. The focus on sustainability in manufacturing and product design is also expected to become a growth accelerator.

Key Players Shaping the Skin Filler Market

- Allergan

- Galderma

- LG Life Science

- Merz

- Medytox

- Bloomage

- Bohus BioTech

- Sinclair Pharma

- IMEIK

- Suneva Medical

Notable Milestones in Skin Filler Sector

- 2019: FDA approval for Juvederm Volux by Allergan, expanding options for jawline contouring.

- 2020: Launch of Restylane Defyne and Refyne by Galderma, offering different flexibility and lift for facial wrinkles.

- 2021: Medytox receives approval for Neuramis Hyaluronidase, a crucial adjunct for dissolving HA fillers.

- 2022: Sinclair Pharma's Ellanse obtains expanded indications for facial rejuvenation in various markets.

- 2023: Bloomage Biotechnology invests heavily in R&D for novel HA formulations and cross-linking techniques.

- 2024: Suneva Medical's Radiesse continues to demonstrate sustained collagen stimulation benefits, driving its popularity.

- 2025 (Estimated): Increased focus on PLLA and CaHA fillers due to demand for collagen-boosting effects.

In-Depth Skin Filler Market Outlook

The future of the Skin Filler market is exceptionally promising, driven by a confluence of technological innovation, demographic shifts, and evolving consumer desires for aesthetic enhancement. Growth accelerators will continue to focus on advanced bio-regenerative fillers, personalized treatment plans, and the integration of dermal fillers with cutting-edge energy-based devices. Strategic market expansion into emerging economies, coupled with ongoing education and training initiatives for medical professionals, will unlock significant untapped potential. The market is anticipated to witness sustained double-digit growth, solidifying its position as a cornerstone of the global aesthetic industry and offering substantial opportunities for continued investment and innovation.

Skin Filler Segmentation

-

1. Application

- 1.1. Micro-plastic and Cosmetic

- 1.2. Anti-Aging

- 1.3. Other

-

2. Types

- 2.1. HA

- 2.2. CaHA

- 2.3. PLLA

- 2.4. PMMA

- 2.5. Other

Skin Filler Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Skin Filler Regional Market Share

Geographic Coverage of Skin Filler

Skin Filler REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Skin Filler Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Micro-plastic and Cosmetic

- 5.1.2. Anti-Aging

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. HA

- 5.2.2. CaHA

- 5.2.3. PLLA

- 5.2.4. PMMA

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Skin Filler Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Micro-plastic and Cosmetic

- 6.1.2. Anti-Aging

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. HA

- 6.2.2. CaHA

- 6.2.3. PLLA

- 6.2.4. PMMA

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Skin Filler Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Micro-plastic and Cosmetic

- 7.1.2. Anti-Aging

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. HA

- 7.2.2. CaHA

- 7.2.3. PLLA

- 7.2.4. PMMA

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Skin Filler Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Micro-plastic and Cosmetic

- 8.1.2. Anti-Aging

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. HA

- 8.2.2. CaHA

- 8.2.3. PLLA

- 8.2.4. PMMA

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Skin Filler Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Micro-plastic and Cosmetic

- 9.1.2. Anti-Aging

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. HA

- 9.2.2. CaHA

- 9.2.3. PLLA

- 9.2.4. PMMA

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Skin Filler Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Micro-plastic and Cosmetic

- 10.1.2. Anti-Aging

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. HA

- 10.2.2. CaHA

- 10.2.3. PLLA

- 10.2.4. PMMA

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Allergan

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Galderma

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 LG Life Science

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Merz

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Medytox

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Bloomage

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Bohus BioTech

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Sinclair Pharma

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 IMEIK

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Suneva Medical

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Allergan

List of Figures

- Figure 1: Global Skin Filler Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Skin Filler Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Skin Filler Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Skin Filler Volume (K), by Application 2025 & 2033

- Figure 5: North America Skin Filler Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Skin Filler Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Skin Filler Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Skin Filler Volume (K), by Types 2025 & 2033

- Figure 9: North America Skin Filler Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Skin Filler Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Skin Filler Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Skin Filler Volume (K), by Country 2025 & 2033

- Figure 13: North America Skin Filler Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Skin Filler Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Skin Filler Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Skin Filler Volume (K), by Application 2025 & 2033

- Figure 17: South America Skin Filler Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Skin Filler Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Skin Filler Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Skin Filler Volume (K), by Types 2025 & 2033

- Figure 21: South America Skin Filler Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Skin Filler Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Skin Filler Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Skin Filler Volume (K), by Country 2025 & 2033

- Figure 25: South America Skin Filler Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Skin Filler Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Skin Filler Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Skin Filler Volume (K), by Application 2025 & 2033

- Figure 29: Europe Skin Filler Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Skin Filler Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Skin Filler Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Skin Filler Volume (K), by Types 2025 & 2033

- Figure 33: Europe Skin Filler Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Skin Filler Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Skin Filler Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Skin Filler Volume (K), by Country 2025 & 2033

- Figure 37: Europe Skin Filler Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Skin Filler Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Skin Filler Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Skin Filler Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Skin Filler Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Skin Filler Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Skin Filler Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Skin Filler Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Skin Filler Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Skin Filler Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Skin Filler Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Skin Filler Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Skin Filler Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Skin Filler Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Skin Filler Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Skin Filler Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Skin Filler Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Skin Filler Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Skin Filler Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Skin Filler Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Skin Filler Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Skin Filler Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Skin Filler Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Skin Filler Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Skin Filler Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Skin Filler Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Skin Filler Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Skin Filler Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Skin Filler Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Skin Filler Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Skin Filler Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Skin Filler Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Skin Filler Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Skin Filler Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Skin Filler Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Skin Filler Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Skin Filler Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Skin Filler Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Skin Filler Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Skin Filler Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Skin Filler Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Skin Filler Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Skin Filler Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Skin Filler Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Skin Filler Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Skin Filler Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Skin Filler Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Skin Filler Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Skin Filler Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Skin Filler Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Skin Filler Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Skin Filler Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Skin Filler Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Skin Filler Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Skin Filler Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Skin Filler Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Skin Filler Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Skin Filler Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Skin Filler Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Skin Filler Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Skin Filler Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Skin Filler Volume K Forecast, by Country 2020 & 2033

- Table 79: China Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Skin Filler Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Skin Filler Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Skin Filler Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Skin Filler?

The projected CAGR is approximately 9.25%.

2. Which companies are prominent players in the Skin Filler?

Key companies in the market include Allergan, Galderma, LG Life Science, Merz, Medytox, Bloomage, Bohus BioTech, Sinclair Pharma, IMEIK, Suneva Medical.

3. What are the main segments of the Skin Filler?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Skin Filler," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Skin Filler report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Skin Filler?

To stay informed about further developments, trends, and reports in the Skin Filler, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence