Key Insights

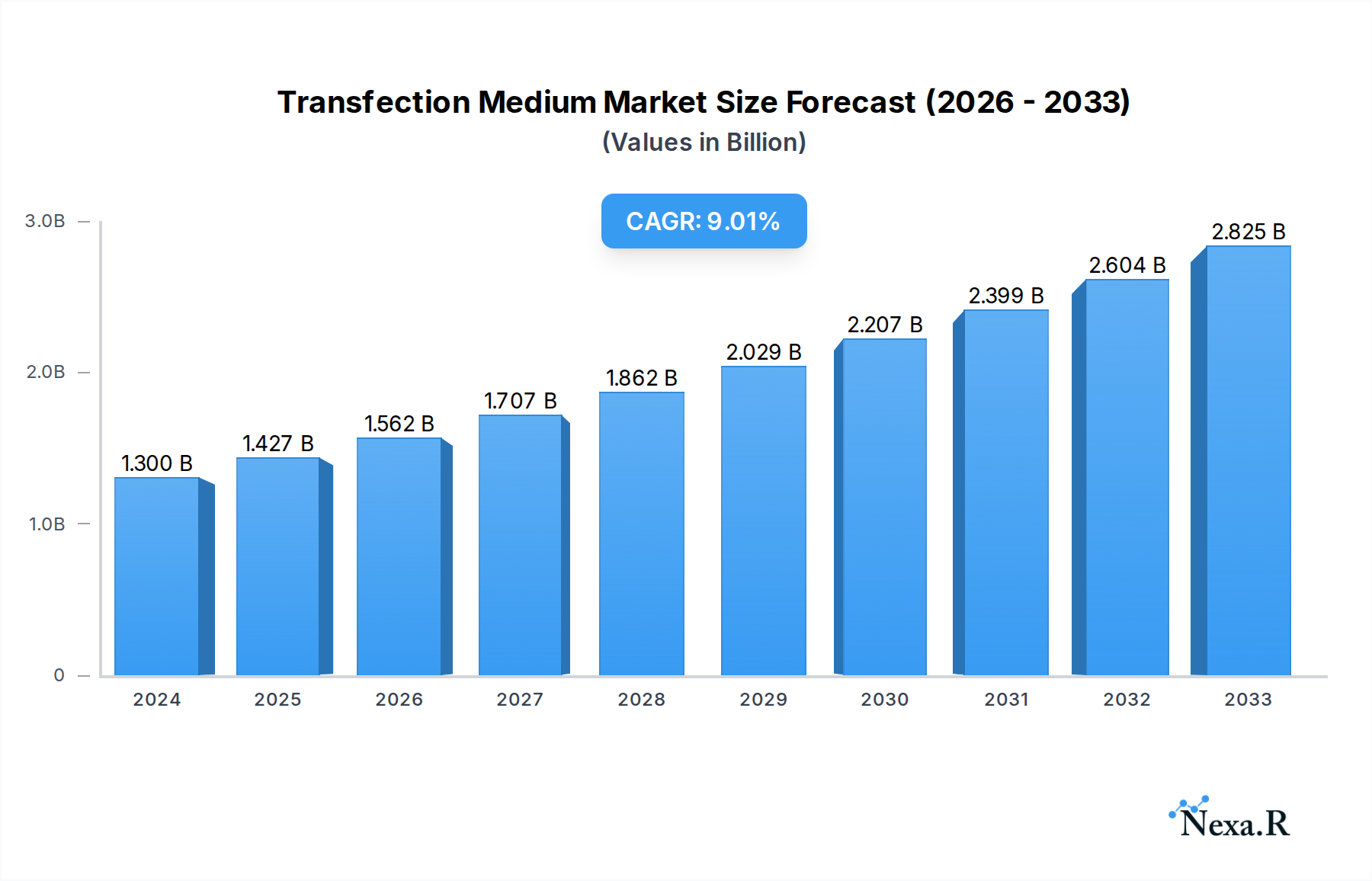

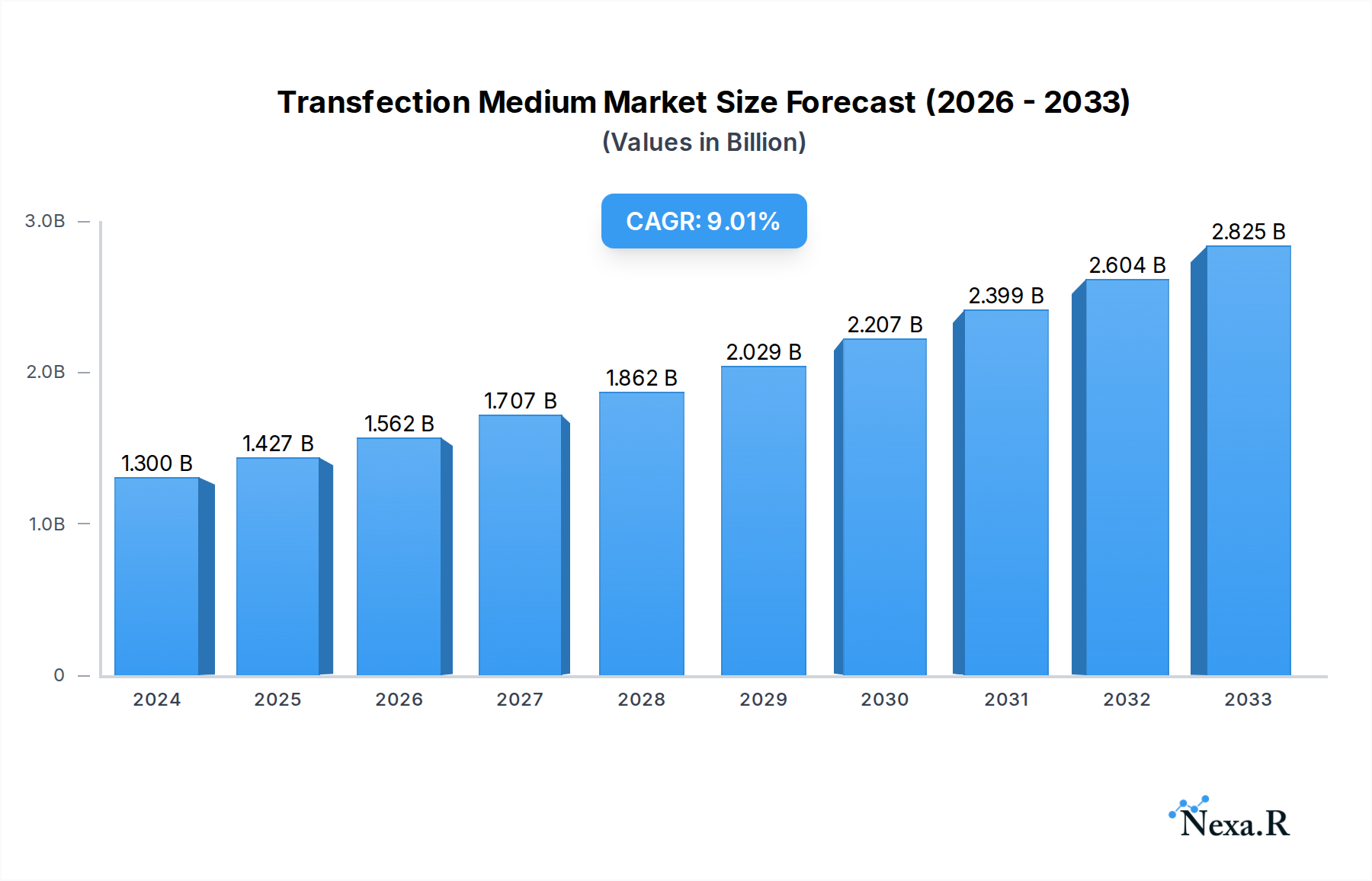

The global Transfection Medium market is poised for significant expansion, driven by an increasing demand for advanced biopharmaceutical development and a burgeoning research landscape. With a current market valuation estimated at $1.3 billion in 2024, the sector is projected to experience a robust Compound Annual Growth Rate (CAGR) of 9.64% through the forecast period of 2025-2033. This growth is primarily fueled by the expanding applications of gene therapy and cell-based research, necessitating efficient and effective transfection solutions. The pharmaceutical segment, in particular, is a key driver, as companies invest heavily in developing novel drug therapies and vaccines, many of which rely on transfected cells for production or therapeutic intervention. Furthermore, the increasing prevalence of chronic diseases and the growing need for personalized medicine are creating a fertile ground for gene editing technologies, which in turn boosts the demand for sophisticated transfection reagents and mediums.

Transfection Medium Market Size (In Billion)

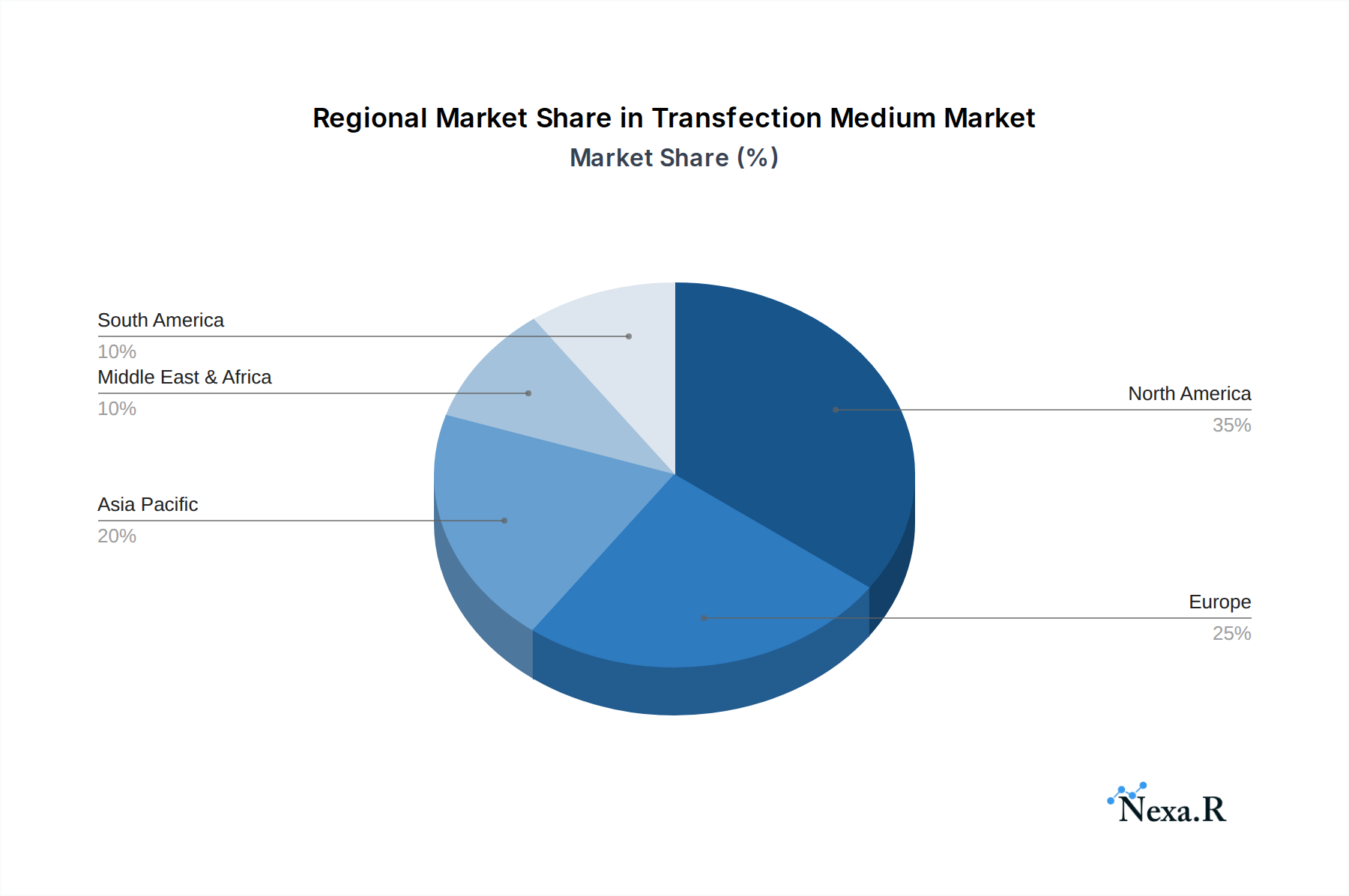

The market is characterized by a dynamic interplay of innovation and evolving research methodologies. Key trends include the development of non-viral transfection methods that offer improved safety profiles and reduced cytotoxicity compared to traditional viral vectors. The rising adoption of induced pluripotent stem cells (iPSCs) and other advanced cell models in drug discovery and regenerative medicine also contributes to market growth, as these applications often require highly optimized transfection protocols. While the market is experiencing strong tailwinds, certain restraints, such as the high cost associated with some advanced transfection reagents and the stringent regulatory landscape for cell-based therapies, could pose challenges. However, ongoing research and development efforts, coupled with strategic collaborations among leading companies like Danaher, Sartorius CellGenix, and FUJIFILM Irvine Scientific, are expected to mitigate these challenges and further propel the market forward. The Asia Pacific region, with its rapidly growing biopharmaceutical industry and increasing R&D investments, is anticipated to be a significant contributor to market expansion in the coming years.

Transfection Medium Company Market Share

Here's the SEO-optimized report description for Transfection Medium, designed for maximum visibility and engagement with industry professionals:

Transfection Medium Market Dynamics & Structure

The global transfection medium market is characterized by a dynamic and evolving landscape, driven by relentless innovation and expanding applications in biological research, pharmaceuticals, and beyond. Market concentration is moderate, with key players like Danaher, Sartorius, CellGenix, Expression Systems, Santa Cruz Biotechnology, FUJIFILM Irvine Scientific, Thousand Oaks Biopharmaceuticals, and QuaCell Biotechnology vying for market share. Technological innovation is a primary driver, with continuous development of more efficient, safer, and cell-specific transfection reagents and media. Regulatory frameworks, particularly concerning biopharmaceutical development and clinical trials, significantly influence market access and product approval processes. Competitive product substitutes, including viral vectors and electroporation, offer alternative gene delivery methods, prompting manufacturers to focus on superior transfection efficiency and reduced cellular toxicity. End-user demographics are diverse, spanning academic research institutions, contract research organizations (CROs), and biopharmaceutical companies of all sizes. Mergers and acquisitions (M&A) are a notable trend, with strategic consolidations aimed at expanding product portfolios, enhancing R&D capabilities, and gaining market access. For instance, a predicted 20 M&A deals are anticipated between 2019 and 2033, with an estimated total deal value of $5.8 billion. Innovation barriers include the high cost of R&D, stringent regulatory approvals, and the need for specialized expertise.

- Market Concentration: Moderate, with a mix of large established players and emerging biotech firms.

- Technological Innovation: Driven by demand for higher transfection efficiency, reduced cytotoxicity, and specific cell line optimization.

- Regulatory Frameworks: Evolving guidelines for gene therapy and biopharmaceutical production impact product development and market entry.

- Competitive Substitutes: Viral vectors and physical methods (electroporation, sonoporation) present ongoing competition.

- End-User Demographics: Broad spectrum from academic researchers to large-scale biopharmaceutical manufacturers.

- M&A Trends: Strategic acquisitions and partnerships are common for portfolio expansion and market consolidation.

- Innovation Barriers: High R&D investment, complex regulatory pathways, and the need for specialized technical expertise.

Transfection Medium Growth Trends & Insights

The global transfection medium market is poised for robust growth, projected to expand from an estimated $2.1 billion in 2025 to $4.5 billion by 2033, exhibiting a compound annual growth rate (CAGR) of approximately 9.8% during the forecast period. This significant market expansion is underpinned by several key trends. The escalating demand for advanced biopharmaceuticals, including monoclonal antibodies, recombinant proteins, and gene therapies, is a primary catalyst. These therapeutics often rely on efficient and reliable gene delivery methods for their production, directly driving the need for high-performance transfection media. Furthermore, the rapid advancements in genetic engineering technologies, such as CRISPR-Cas9, have democratized gene editing and manipulation, creating a burgeoning market for specialized transfection solutions. As research into complex diseases like cancer, genetic disorders, and infectious diseases intensifies, the need for precise and effective gene delivery tools in both academic and industrial settings continues to rise.

Adoption rates for various transfection techniques are steadily increasing, with non-viral methods, including chemical and physical transfection, gaining traction due to their perceived safety advantages and lower immunogenicity compared to viral vectors. This shift favors the development and adoption of innovative chemical transfection media formulations that offer improved efficiency and reduced toxicity across a wider range of cell types. Technological disruptions are continuously emerging, with a focus on developing multi-functional transfection agents that can deliver nucleic acids and other therapeutic payloads with enhanced specificity and efficacy. The development of serum-free and animal-component-free transfection media is also a significant trend, driven by concerns over contamination and ethical considerations in biopharmaceutical manufacturing.

Consumer behavior shifts, particularly within the research and biopharmaceutical sectors, are characterized by an increasing preference for customized and application-specific transfection solutions. Researchers and manufacturers are actively seeking transfection media that are optimized for specific cell lines, downstream applications, and scale-up processes. This has led to a proliferation of specialized transfection media designed for lentiviral production, mRNA synthesis, and protein expression in CHO, HEK293, and other commonly used cell lines. The growing emphasis on personalized medicine and the development of cell-based therapies are also creating new avenues for market growth, necessitating transfection media capable of supporting complex cellular manipulations. The market penetration of advanced transfection technologies is expected to deepen as R&D investments continue to pour into the life sciences, further fueling the demand for sophisticated transfection solutions.

Dominant Regions, Countries, or Segments in Transfection Medium

The global transfection medium market exhibits distinct regional dominance and segment-specific growth patterns. North America, led by the United States, currently holds the largest market share, estimated to be around 38% of the total market in 2025. This dominance is attributed to the region's robust biopharmaceutical industry, extensive government funding for life science research, a high concentration of academic institutions and research centers, and a well-established regulatory framework that supports innovation and commercialization. The presence of major pharmaceutical and biotechnology companies, coupled with significant investments in gene therapy and cell-based research, further solidifies North America's leading position.

Within the Application segment, the Pharmaceutical application is the largest and fastest-growing segment, accounting for an estimated 45% of the market in 2025 and projected to reach $1.9 billion by 2033. This growth is directly linked to the escalating demand for biologics, vaccines, and advanced therapies. The biological research segment follows closely, driven by academic research, drug discovery, and fundamental scientific investigations. The Research segment, encompassing academic institutions and smaller biotech firms, also represents a significant portion of the market, fueled by ongoing efforts to understand cellular mechanisms and develop novel therapeutic approaches.

In terms of Type, Liquid Transfection Medium dominates the market, holding an estimated 75% share in 2025. Its widespread use is due to ease of handling, precise dosing, and compatibility with automated liquid handling systems commonly employed in research and manufacturing. Dry Powder Transfection Medium, while a smaller segment, is experiencing considerable growth due to its longer shelf life, reduced shipping costs, and convenience for storage, making it increasingly attractive for global distribution and remote research facilities.

Key drivers contributing to this dominance include supportive government policies promoting biotechnology and pharmaceutical R&D, substantial venture capital funding, and the presence of a highly skilled workforce. The robust research infrastructure and a culture of innovation further propel the adoption of cutting-edge transfection technologies. For example, the U.S. National Institutes of Health (NIH) allocates billions of dollars annually to biomedical research, much of which directly or indirectly fuels the demand for transfection reagents and media. Furthermore, the increasing prevalence of chronic diseases and the growing aging population in regions like North America and Europe are driving demand for advanced therapies, which heavily rely on efficient transfection technologies.

- Dominant Region: North America (specifically the United States).

- Dominant Application Segment: Pharmaceutical.

- Dominant Type Segment: Liquid Transfection Medium.

- Key Drivers in Dominant Segments:

- North America: Strong biopharmaceutical industry, significant R&D funding, advanced research infrastructure, favorable regulatory environment.

- Pharmaceutical Application: Growing demand for biologics, gene therapies, and vaccines; increasing focus on personalized medicine.

- Liquid Transfection Medium: Ease of use, precise dosing, automation compatibility.

- Growth Potential: High for Dry Powder Transfection Medium due to logistical advantages.

Transfection Medium Product Landscape

The transfection medium product landscape is marked by continuous innovation, driven by the pursuit of higher transfection efficiency, lower cytotoxicity, and improved cell viability across diverse cell types. Leading manufacturers are focusing on developing sophisticated formulations that cater to specific applications, such as lentiviral vector production, mRNA synthesis, and stable cell line development. Product performance metrics are increasingly being scrutinized, with a focus on achieving transfection efficiencies exceeding 90% in various cell lines, while maintaining cellular health and genetic integrity. Unique selling propositions often revolve around proprietary lipid-based or polymer-based chemistries, optimized buffer compositions, and serum-free formulations that minimize batch-to-batch variability and reduce the risk of contamination. Technological advancements are also seen in the development of transfection media that facilitate easier downstream processing and scale-up for industrial applications.

Key Drivers, Barriers & Challenges in Transfection Medium

Key Drivers: The primary forces propelling the transfection medium market include the burgeoning biopharmaceutical industry, characterized by an escalating demand for biologics and advanced therapies such as gene and cell therapies. Significant advancements in genetic engineering technologies, including CRISPR-Cas9, are democratizing gene editing, thereby increasing the need for efficient and precise transfection solutions. Growing investments in life science research, both from government agencies and private entities, further fuel market expansion. The increasing focus on personalized medicine and the development of novel therapeutic modalities necessitates highly effective transfection tools.

Barriers & Challenges: Despite the promising growth, the market faces several challenges. The high cost of research and development for novel transfection media, coupled with stringent and time-consuming regulatory approval processes, poses a significant barrier. Supply chain disruptions, especially in the sourcing of raw materials, can impact production and lead to increased costs. Fierce competition from alternative gene delivery methods, such as viral vectors and electroporation, requires continuous innovation and cost-effectiveness. Furthermore, achieving consistent and high transfection efficiency across a wide array of primary cells and sensitive cell lines remains a technical hurdle. Supply chain issues for specialized reagents can lead to lead times of up to 6 months, impacting research timelines.

Emerging Opportunities in Transfection Medium

Emerging opportunities in the transfection medium market lie in the development of specialized media for ex vivo gene therapy manufacturing, where precise control and scalability are paramount. The growing field of mRNA therapeutics presents a substantial opportunity for novel lipid nanoparticle (LNP) formulations and delivery systems. Untapped markets in emerging economies with developing biopharmaceutical sectors offer significant expansion potential. Evolving consumer preferences for sustainable and cost-effective solutions are also creating opportunities for innovative product designs and manufacturing processes. The development of transfection media for 3D cell culture and organoid technologies is another burgeoning area.

Growth Accelerators in the Transfection Medium Industry

Several catalysts are accelerating growth in the transfection medium industry. Technological breakthroughs in nanotechnology and material science are enabling the development of next-generation transfection agents with enhanced targeting capabilities and payload delivery. Strategic partnerships between reagent manufacturers and biopharmaceutical companies are crucial for co-developing optimized transfection solutions for specific drug candidates and therapeutic applications. The increasing adoption of automated liquid handling systems and high-throughput screening platforms in research laboratories and manufacturing facilities is driving demand for compatible and efficient transfection media. Furthermore, market expansion strategies focusing on emerging markets and niche therapeutic areas are contributing to sustained growth.

Key Players Shaping the Transfection Medium Market

- Danaher

- Sartorius

- CellGenix

- Expression Systems

- Santa Cruz Biotechnology

- FUJIFILM Irvine Scientific

- Thousand Oaks Biopharmaceuticals

- QuaCell Biotechnology

Notable Milestones in Transfection Medium Sector

- 2019: Launch of next-generation lipid-based transfection reagents offering improved safety profiles.

- 2020: Increased demand for transfection media for COVID-19 vaccine research and development.

- 2021: Major advancements in non-viral gene delivery for in vivo applications.

- 2022: Expansion of serum-free and animal-component-free transfection media portfolios.

- 2023: Strategic acquisitions aimed at enhancing product offerings in gene therapy.

- 2024: Emergence of enhanced transfection media for stable protein expression in CHO cells.

- 2025: Predicted increase in the adoption of dry powder transfection media for global distribution.

In-Depth Transfection Medium Market Outlook

The outlook for the transfection medium market remains exceptionally bright, driven by a confluence of scientific innovation and therapeutic demand. Growth accelerators such as continuous improvements in transfection efficiency, the expansion of gene and cell therapy applications, and the increasing global investment in life sciences research will continue to fuel market expansion. Strategic partnerships and collaborations will play a pivotal role in bringing novel transfection solutions to market and addressing specific customer needs. The increasing focus on personalized medicine and the development of complex biologics will further underscore the indispensable role of advanced transfection technologies. The market is poised for sustained growth, offering significant opportunities for stakeholders who can navigate the evolving technological landscape and regulatory environment.

Transfection Medium Segmentation

-

1. Application

- 1.1. Biological

- 1.2. Pharmaceutical

- 1.3. Research

- 1.4. Others

-

2. Type

- 2.1. Liquid Transfection Medium

- 2.2. Dry Powder Transfection Medium

Transfection Medium Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Transfection Medium Regional Market Share

Geographic Coverage of Transfection Medium

Transfection Medium REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.64% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Transfection Medium Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Biological

- 5.1.2. Pharmaceutical

- 5.1.3. Research

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Liquid Transfection Medium

- 5.2.2. Dry Powder Transfection Medium

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Transfection Medium Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Biological

- 6.1.2. Pharmaceutical

- 6.1.3. Research

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Liquid Transfection Medium

- 6.2.2. Dry Powder Transfection Medium

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Transfection Medium Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Biological

- 7.1.2. Pharmaceutical

- 7.1.3. Research

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Liquid Transfection Medium

- 7.2.2. Dry Powder Transfection Medium

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Transfection Medium Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Biological

- 8.1.2. Pharmaceutical

- 8.1.3. Research

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Liquid Transfection Medium

- 8.2.2. Dry Powder Transfection Medium

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Transfection Medium Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Biological

- 9.1.2. Pharmaceutical

- 9.1.3. Research

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Liquid Transfection Medium

- 9.2.2. Dry Powder Transfection Medium

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Transfection Medium Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Biological

- 10.1.2. Pharmaceutical

- 10.1.3. Research

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Liquid Transfection Medium

- 10.2.2. Dry Powder Transfection Medium

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Danaher

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Sartorius CellGenix

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Expression Systems

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Santa Cruz Biotechnology

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 FUJIFILM Irvine Scientific

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Thousand Oaks Biopharmaceuticals

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 QuaCell Biotechnology

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.1 Danaher

List of Figures

- Figure 1: Global Transfection Medium Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Transfection Medium Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Transfection Medium Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Transfection Medium Volume (K), by Application 2025 & 2033

- Figure 5: North America Transfection Medium Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Transfection Medium Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Transfection Medium Revenue (undefined), by Type 2025 & 2033

- Figure 8: North America Transfection Medium Volume (K), by Type 2025 & 2033

- Figure 9: North America Transfection Medium Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Transfection Medium Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Transfection Medium Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Transfection Medium Volume (K), by Country 2025 & 2033

- Figure 13: North America Transfection Medium Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Transfection Medium Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Transfection Medium Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Transfection Medium Volume (K), by Application 2025 & 2033

- Figure 17: South America Transfection Medium Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Transfection Medium Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Transfection Medium Revenue (undefined), by Type 2025 & 2033

- Figure 20: South America Transfection Medium Volume (K), by Type 2025 & 2033

- Figure 21: South America Transfection Medium Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Transfection Medium Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Transfection Medium Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Transfection Medium Volume (K), by Country 2025 & 2033

- Figure 25: South America Transfection Medium Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Transfection Medium Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Transfection Medium Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Transfection Medium Volume (K), by Application 2025 & 2033

- Figure 29: Europe Transfection Medium Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Transfection Medium Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Transfection Medium Revenue (undefined), by Type 2025 & 2033

- Figure 32: Europe Transfection Medium Volume (K), by Type 2025 & 2033

- Figure 33: Europe Transfection Medium Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Transfection Medium Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Transfection Medium Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Transfection Medium Volume (K), by Country 2025 & 2033

- Figure 37: Europe Transfection Medium Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Transfection Medium Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Transfection Medium Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Transfection Medium Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Transfection Medium Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Transfection Medium Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Transfection Medium Revenue (undefined), by Type 2025 & 2033

- Figure 44: Middle East & Africa Transfection Medium Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Transfection Medium Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Transfection Medium Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Transfection Medium Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Transfection Medium Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Transfection Medium Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Transfection Medium Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Transfection Medium Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Transfection Medium Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Transfection Medium Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Transfection Medium Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Transfection Medium Revenue (undefined), by Type 2025 & 2033

- Figure 56: Asia Pacific Transfection Medium Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Transfection Medium Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Transfection Medium Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Transfection Medium Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Transfection Medium Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Transfection Medium Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Transfection Medium Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Transfection Medium Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Transfection Medium Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Transfection Medium Revenue undefined Forecast, by Type 2020 & 2033

- Table 4: Global Transfection Medium Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Transfection Medium Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Transfection Medium Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Transfection Medium Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Transfection Medium Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Transfection Medium Revenue undefined Forecast, by Type 2020 & 2033

- Table 10: Global Transfection Medium Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Transfection Medium Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Transfection Medium Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Transfection Medium Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Transfection Medium Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Transfection Medium Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Global Transfection Medium Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Transfection Medium Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Transfection Medium Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Transfection Medium Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Transfection Medium Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Transfection Medium Revenue undefined Forecast, by Type 2020 & 2033

- Table 34: Global Transfection Medium Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Transfection Medium Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Transfection Medium Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Transfection Medium Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Transfection Medium Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Transfection Medium Revenue undefined Forecast, by Type 2020 & 2033

- Table 58: Global Transfection Medium Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Transfection Medium Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Transfection Medium Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Transfection Medium Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Transfection Medium Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Transfection Medium Revenue undefined Forecast, by Type 2020 & 2033

- Table 76: Global Transfection Medium Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Transfection Medium Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Transfection Medium Volume K Forecast, by Country 2020 & 2033

- Table 79: China Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Transfection Medium Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Transfection Medium Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Transfection Medium?

The projected CAGR is approximately 9.64%.

2. Which companies are prominent players in the Transfection Medium?

Key companies in the market include Danaher, Sartorius CellGenix, Expression Systems, Santa Cruz Biotechnology, FUJIFILM Irvine Scientific, Thousand Oaks Biopharmaceuticals, QuaCell Biotechnology.

3. What are the main segments of the Transfection Medium?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Transfection Medium," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Transfection Medium report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Transfection Medium?

To stay informed about further developments, trends, and reports in the Transfection Medium, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence