Key Insights

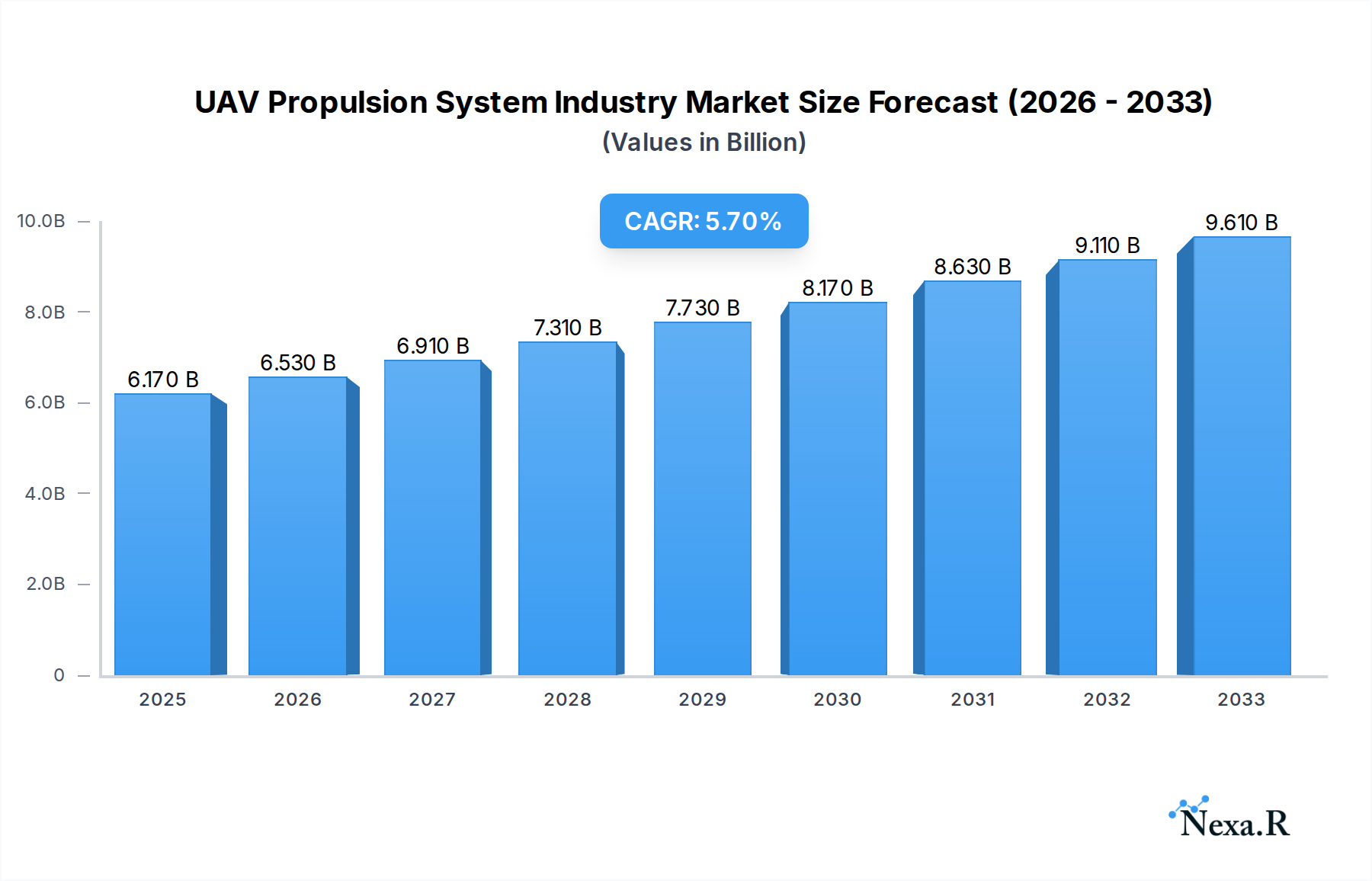

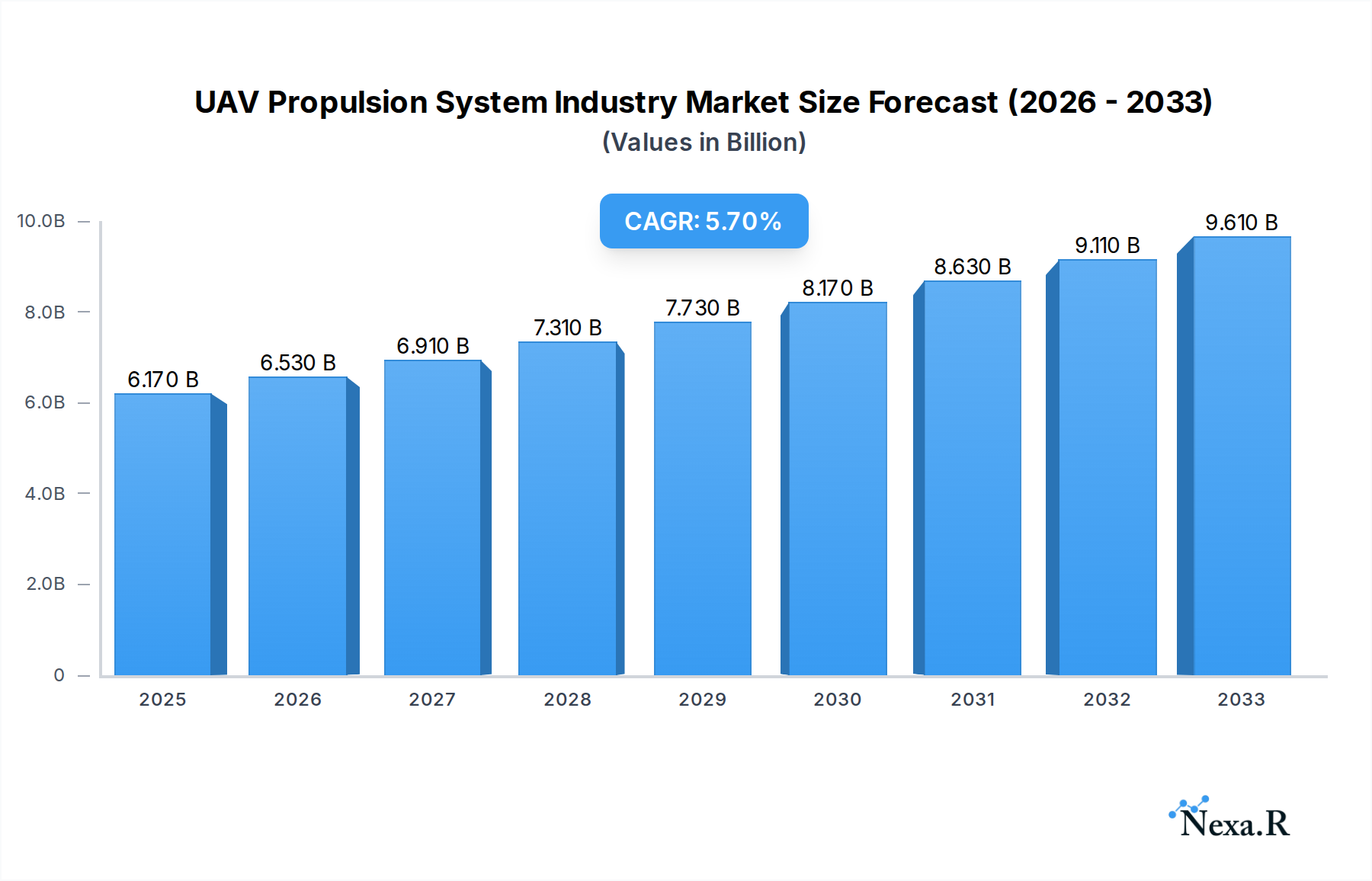

The global UAV propulsion system market is poised for significant expansion, driven by escalating demand across civil, commercial, and military sectors. With a market size estimated at $6.17 billion in 2025, the industry is projected to experience a robust compound annual growth rate (CAGR) of 5.84% through the forecast period of 2025-2033. This growth is fueled by advancements in engine technology, including the increasing adoption of hybrid and full-electric propulsion systems, offering enhanced efficiency, reduced emissions, and extended flight times. The proliferation of drones for diverse applications such as aerial surveillance, logistics, agriculture, and infrastructure inspection, alongside growing defense spending on unmanned aerial vehicles, are key market drivers. The surge in the development and deployment of micro and mini UAVs for specialized tasks, coupled with the continuous innovation in tactical, MALE, and HALE UAVs for extensive operational capabilities, further underpins this upward trajectory. Market players are focusing on developing lighter, more powerful, and quieter propulsion solutions to meet the evolving needs of the UAV ecosystem.

UAV Propulsion System Industry Market Size (In Billion)

The market landscape is characterized by a dynamic interplay of technological innovation and increasing market penetration. While conventional engine types will continue to hold a significant share, the rapid advancements and growing environmental consciousness are accelerating the adoption of hybrid and full-electric propulsion. This shift presents both opportunities and challenges, with significant investments being channeled into research and development for battery technology, fuel cells, and advanced electric motor integration. Emerging trends such as the integration of artificial intelligence for optimized propulsion management and the development of autonomous flight systems are expected to shape the future of the market. Restraints such as stringent regulatory frameworks and the high cost of advanced propulsion technologies are being addressed through ongoing technological maturation and policy adaptations. Major regional markets, including North America, Europe, and Asia Pacific, are anticipated to lead in adoption and innovation, with companies like General Electric, Pratt & Whitney, and Honeywell International playing pivotal roles in driving market growth and technological advancements.

UAV Propulsion System Industry Company Market Share

UAV Propulsion System Industry Market Dynamics & Structure

The global UAV propulsion system market is characterized by a dynamic blend of established aerospace giants and agile newcomers, fostering an environment of intense competition and rapid innovation. Market concentration is moderate, with key players like Honeywell International Inc., Rolls-Royce plc, and Pratt & Whitney (RTX Corporation) holding significant sway, particularly in the military and large UAV segments. However, the burgeoning civil and commercial drone sector is witnessing the rise of specialized manufacturers and technology providers, including Ballard Power Systems Inc. and Orbital Corporation Limited, who are driving advancements in hybrid and electric propulsion. Technological innovation is the paramount driver, fueled by the relentless pursuit of increased endurance, payload capacity, reduced emissions, and enhanced reliability. Advancements in battery technology, fuel cell efficiency, and lightweight, high-performance internal combustion engines are key areas of focus. Regulatory frameworks, while still evolving, are becoming more defined, influencing design standards, safety certifications, and operational approvals, thereby shaping market entry and product development. Competitive product substitutes are emerging, with electric propulsion systems increasingly challenging traditional internal combustion engines, particularly for smaller UAVs, due to their quieter operation and lower maintenance needs. End-user demographics are broadening significantly, encompassing not only military applications but also a growing array of civil and commercial sectors such as logistics, agriculture, infrastructure inspection, and public safety. Merger and acquisition (M&A) trends are evident as larger corporations seek to acquire specialized technological capabilities or expand their footprint in the rapidly growing UAV market. For instance, a significant number of strategic partnerships and smaller acquisitions have been observed in the past five years, targeting companies with expertise in advanced battery management systems and lightweight engine design.

- Market Concentration: Moderate, with a blend of large aerospace conglomerates and specialized technology providers.

- Key Innovation Drivers: Extended flight endurance, increased payload capacity, reduced emissions, enhanced reliability, and lower operational costs.

- Regulatory Impact: Evolving frameworks influencing safety, certification, and operational approvals, driving standardization and responsible innovation.

- Product Substitutes: Growing competition between conventional, hybrid, and full-electric propulsion systems, with electric gaining traction for specific applications.

- End-User Diversity: Expansion beyond military to logistics, agriculture, infrastructure, and public safety sectors, creating diverse demand.

- M&A Trends: Strategic acquisitions and partnerships focused on acquiring specialized technologies and market access.

UAV Propulsion System Industry Growth Trends & Insights

The UAV propulsion system industry is poised for substantial expansion, driven by a confluence of technological advancements, increasing adoption across diverse sectors, and evolving consumer preferences for autonomous aerial solutions. The global market size for UAV propulsion systems is projected to witness robust growth, with an estimated market size of $15,800 million in 2025, escalating to an impressive $38,500 million by 2033, exhibiting a compound annual growth rate (CAGR) of approximately 11.8% during the forecast period of 2025–2033. This impressive trajectory is underpinned by accelerating adoption rates in both military and civil domains. Military applications continue to be a significant revenue generator, with the demand for advanced propulsion systems for Tactical UAVs and MALE UAVs driving innovation in durability and performance under challenging conditions. Simultaneously, the civil and commercial sector is experiencing an unprecedented surge in demand, fueled by advancements in drone technology that enable a wider range of applications, from last-mile delivery and precision agriculture to aerial surveying and infrastructure monitoring.

Technological disruptions are at the forefront of this growth. The ongoing transition towards hybrid and full-electric propulsion systems is a defining trend. Full-electric propulsion systems, powered by advancements in battery energy density and power management, are becoming increasingly viable for shorter-range, lighter UAVs, offering quieter operation, reduced maintenance, and zero direct emissions. Hybrid systems, which combine the benefits of internal combustion engines with electric power, are emerging as a compelling solution for longer endurance missions, providing greater operational flexibility and mitigating range anxiety. Furthermore, the development of hydrogen fuel cell technology by companies like Ballard Power Systems Inc. and Intelligent Energy Limited holds immense promise for achieving ultra-long endurance capabilities, particularly for HALE UAVs, albeit with significant developmental hurdles still to overcome.

Consumer behavior shifts are also playing a crucial role. As the cost of UAVs decreases and their capabilities increase, businesses and individuals are increasingly exploring and integrating drone technology into their operations and services. This democratization of drone technology is creating a more diverse customer base with varied performance requirements, from the micro and mini UAV segments catering to hobbyists and niche industrial inspections to the larger MALE and HALE UAVs for sophisticated military and scientific missions. The increasing demand for autonomous operations, driven by the need for efficiency and reduced human risk, is further propelling the development of propulsion systems that offer greater autonomy, reliability, and integration with advanced navigation and control systems. The robust growth observed in the historical period from 2019–2024, with an estimated market size of $12,100 million in 2024, sets a strong foundation for this projected expansion, indicating a consistent upward trend in market penetration and technological integration.

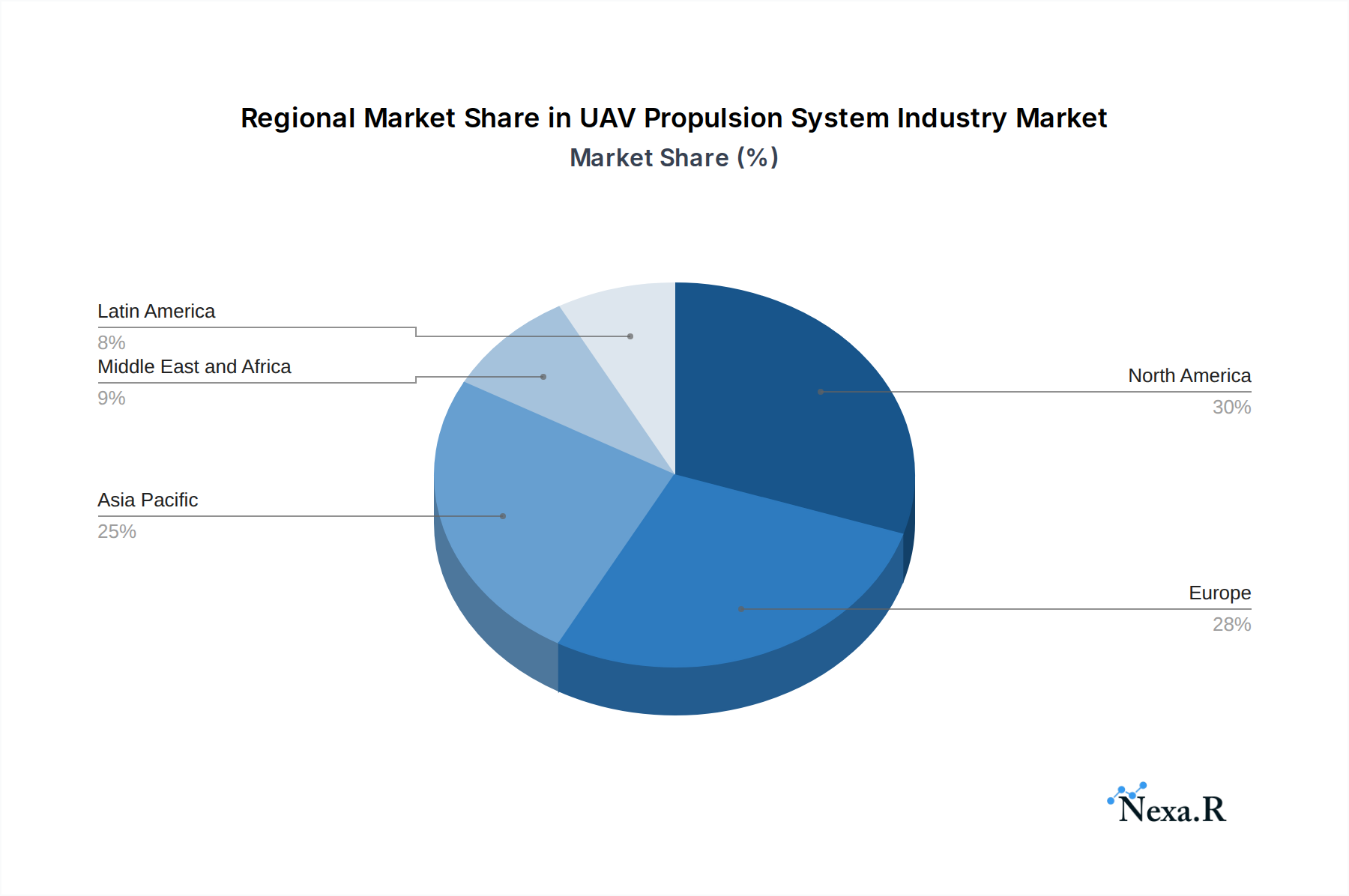

Dominant Regions, Countries, or Segments in UAV Propulsion System Industry

The global UAV propulsion system industry exhibits distinct regional dominance and segment leadership, shaped by a complex interplay of technological adoption, defense spending, regulatory environments, and the presence of key industry players. North America, particularly the United States, currently stands as the most dominant region, largely due to its substantial investments in military modernization and the burgeoning commercial drone market. The U.S. military's continuous demand for advanced UAV platforms, ranging from tactical and MALE UAVs to HALE UAVs for reconnaissance and surveillance, drives significant research, development, and procurement of cutting-edge propulsion systems. Companies like Honeywell International Inc., Pratt & Whitney (RTX Corporation), and General Electric Company, with their established aerospace expertise, are key beneficiaries of this demand. Furthermore, the rapid expansion of the commercial drone sector in North America, driven by innovation in logistics, agriculture, and infrastructure inspection, fuels the growth of propulsion systems for Mini UAVs and Tactical UAVs.

Europe also presents a strong market, with countries like Germany, the United Kingdom, and France leading in both military and civilian UAV development. The presence of major European aerospace manufacturers such as Rolls-Royce plc and Diamond Aircraft Industries GmbH, alongside specialized engine providers like BRP-Rotax GmbH & Co KG and 3W International GmbH, contributes to a competitive landscape. European nations are actively integrating UAVs into their defense strategies and are pioneers in adopting drones for a wide array of commercial applications, including environmental monitoring and public safety. The region’s emphasis on sustainability is also fostering the growth of hybrid and full-electric propulsion systems.

In terms of segments, the Military application segment is currently the largest contributor to the UAV propulsion system market. This dominance is attributed to sustained government defense budgets allocated towards advanced aerial capabilities, particularly for MALE and HALE UAVs designed for extended surveillance, reconnaissance, and strike missions. The propulsion systems in this segment are characterized by high thrust, reliability under extreme conditions, and integration with sophisticated control systems. Companies like Pratt & Whitney (RTX Corporation) and Honeywell International Inc. are major players in this domain, offering turboshaft, turboprop, and advanced jet engines.

However, the Civil and Commercial application segment is experiencing the most rapid growth. This surge is driven by the increasing affordability and accessibility of drones, coupled with their expanding use cases. The demand for propulsion systems for Micro UAVs and Mini UAVs for applications like aerial photography, inspection, and small-scale deliveries is booming. Simultaneously, the growing need for larger commercial drones for package delivery, agricultural spraying, and infrastructure monitoring is driving demand for propulsion systems for Tactical UAVs. The shift towards electric and hybrid propulsion is particularly pronounced in this segment due to its lower operational costs, reduced noise pollution, and environmental benefits.

Within Engine Type, the Conventional engine segment, encompassing internal combustion engines, still holds a significant market share due to its proven reliability and power output for larger UAVs. However, the Hybrid and Full-electric segments are projected to witness the highest growth rates. Full-electric propulsion systems are gaining traction for their environmental advantages and ease of maintenance, especially for shorter-duration flights and smaller UAVs. Hybrid systems offer a compelling balance of range and efficiency, making them suitable for a wider spectrum of applications. This ongoing technological evolution is reshaping the competitive landscape and creating new opportunities for innovation.

UAV Propulsion System Industry Product Landscape

The UAV propulsion system product landscape is rapidly evolving, driven by innovation aimed at enhancing endurance, reducing weight, improving efficiency, and lowering emissions. Manufacturers are developing advanced internal combustion engines, including robust piston engines and efficient turbine engines, with enhanced power-to-weight ratios for tactical and military applications. Simultaneously, the market is seeing a proliferation of electric motor and battery solutions, offering cleaner, quieter, and more cost-effective alternatives for smaller and medium-sized UAVs. Innovations in hybrid powertrains, integrating both combustion and electric components, are emerging to offer extended flight times and greater operational flexibility. Advanced materials and intelligent control systems are also being integrated to optimize performance and reliability across all engine types.

Key Drivers, Barriers & Challenges in UAV Propulsion System Industry

Key Drivers:

- Rising Demand for Autonomous Systems: The increasing need for automated operations across military, commercial, and civil sectors is a primary growth driver for UAVs and, consequently, their propulsion systems.

- Technological Advancements: Continuous innovation in battery technology, fuel cells, lightweight materials, and engine efficiency is enhancing UAV capabilities and expanding their application range.

- Growing Military Applications: Defense modernization programs worldwide are fueling demand for advanced UAVs with superior propulsion for reconnaissance, surveillance, and combat missions.

- Expansion of Commercial Drone Use Cases: The burgeoning adoption of drones for logistics, agriculture, infrastructure inspection, and public safety is creating a significant market for propulsion systems.

- Focus on Sustainability and Reduced Emissions: The drive for greener aviation solutions is accelerating the development and adoption of electric and hybrid propulsion systems.

Barriers & Challenges:

- Battery Technology Limitations: For electric UAVs, limitations in energy density, charging times, and lifespan of current battery technology restrict flight duration and payload capacity.

- Regulatory Hurdles and Airspace Integration: Evolving and complex regulatory frameworks for UAV operations and airspace management can hinder market growth and product deployment.

- High Research and Development Costs: Developing cutting-edge propulsion technologies, especially for advanced systems like hydrogen fuel cells, requires substantial investment, posing a barrier for smaller companies.

- Supply Chain Disruptions and Material Availability: Reliance on specialized components and raw materials can lead to supply chain vulnerabilities and price volatility.

- Noise Pollution and Public Perception: Noise generated by certain types of UAV propulsion systems can be a concern for public acceptance and operational deployment in urban areas.

- Competition from Established Aerospace Players: New entrants face challenges competing with the technological expertise, financial resources, and established distribution channels of traditional aerospace manufacturers.

Emerging Opportunities in UAV Propulsion System Industry

Emerging opportunities lie in the development of ultra-long endurance propulsion solutions, particularly through advancements in hydrogen fuel cell technology and next-generation battery chemistries, catering to the growing demand for HALE UAVs in scientific research and persistent surveillance. The integration of propulsion systems with advanced artificial intelligence for optimized power management and autonomous flight control presents a significant avenue for innovation. Furthermore, the expansion of the urban air mobility (UAM) market, although distinct from traditional UAVs, creates opportunities for scalable, efficient, and quiet propulsion systems that can eventually be adapted for smaller unmanned cargo operations in dense urban environments. The increasing focus on sustainable aviation also opens doors for bio-fueled or synthetic fuel-compatible conventional engines.

Growth Accelerators in the UAV Propulsion System Industry Industry

The growth of the UAV propulsion system industry is being significantly accelerated by breakthroughs in energy storage technologies, enabling longer flight times and higher payload capacities for electric and hybrid systems. Strategic partnerships between propulsion manufacturers, drone developers, and end-users are crucial for tailoring solutions to specific application needs and expediting market penetration. The continuous investment in R&D by both established aerospace giants and agile startups, focusing on lighter, more powerful, and efficient engine designs, is a key catalyst. Furthermore, the increasing acceptance and integration of drones into mainstream commercial and public services, driven by proven operational benefits, are creating a robust and expanding demand pipeline for advanced propulsion systems.

Key Players Shaping the UAV Propulsion System Industry Market

- BRP-Rotax GmbH & Co KG

- Honeywell International Inc.

- Ballard Power Systems Inc.

- MMC

- Orbital Corporation Limited

- Pratt & Whitney (RTX Corporation)

- Diamond Aircraft Industries GmbH

- Intelligent Energy Limited

- Rolls-Royce plc

- H3 Dynamics Holdings Pte Ltd

- 3W International GmbH

- General Electric Company

- UAV Engines Limited

- Hirth Engines GmbH

Notable Milestones in UAV Propulsion System Industry Sector

- 2019: Introduction of advanced lightweight piston engines with improved fuel efficiency for tactical UAVs.

- 2020: Significant advancements in lithium-ion battery energy density, enabling longer flight durations for electric mini UAVs.

- 2021: Increased investment and development in hydrogen fuel cell technology for long-endurance HALE UAV applications.

- 2022: Launch of hybrid-electric propulsion systems offering a balance of range and performance for MALE UAVs.

- 2023: Emergence of advanced electric motor controllers with enhanced power management for improved safety and efficiency.

- 2024: Increased regulatory clarity in several key regions, facilitating the wider adoption of commercial UAVs and their propulsion systems.

In-Depth UAV Propulsion System Industry Market Outlook

The outlook for the UAV propulsion system industry is exceptionally positive, driven by sustained technological innovation and a broadening application spectrum. Key growth accelerators include the continued maturation of electric and hybrid propulsion technologies, offering greener and more cost-effective solutions that align with global sustainability goals. Strategic collaborations between propulsion providers and drone manufacturers will further refine system integration and accelerate market adoption across diverse sectors. The robust demand from military modernization programs, coupled with the explosive growth in commercial applications like last-mile delivery and advanced surveying, will continue to fuel market expansion. Emerging opportunities in ultra-long endurance capabilities, particularly through hydrogen fuel cells, promise to unlock new frontiers for scientific research and persistent surveillance, solidifying the industry's trajectory of strong and consistent growth.

UAV Propulsion System Industry Segmentation

-

1. Engine Type

- 1.1. Conventional

- 1.2. Hybrid

- 1.3. Full-electric

-

2. Application

- 2.1. Civil and Commercial

- 2.2. Military

-

3. UAV Type

- 3.1. Micro UAV

- 3.2. Mini UAV

- 3.3. Tactical UAV

- 3.4. MALE UAV

- 3.5. HALE UAV

UAV Propulsion System Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. France

- 2.3. Germany

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Mexico

- 4.3. Rest of Latin America

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. Qatar

- 5.4. South Africa

- 5.5. Rest of Middle East and Africa

UAV Propulsion System Industry Regional Market Share

Geographic Coverage of UAV Propulsion System Industry

UAV Propulsion System Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.84% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Engine Type

- 5.1.1. Conventional

- 5.1.2. Hybrid

- 5.1.3. Full-electric

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Civil and Commercial

- 5.2.2. Military

- 5.3. Market Analysis, Insights and Forecast - by UAV Type

- 5.3.1. Micro UAV

- 5.3.2. Mini UAV

- 5.3.3. Tactical UAV

- 5.3.4. MALE UAV

- 5.3.5. HALE UAV

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Engine Type

- 6. Global UAV Propulsion System Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Engine Type

- 6.1.1. Conventional

- 6.1.2. Hybrid

- 6.1.3. Full-electric

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Civil and Commercial

- 6.2.2. Military

- 6.3. Market Analysis, Insights and Forecast - by UAV Type

- 6.3.1. Micro UAV

- 6.3.2. Mini UAV

- 6.3.3. Tactical UAV

- 6.3.4. MALE UAV

- 6.3.5. HALE UAV

- 6.1. Market Analysis, Insights and Forecast - by Engine Type

- 7. North America UAV Propulsion System Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Engine Type

- 7.1.1. Conventional

- 7.1.2. Hybrid

- 7.1.3. Full-electric

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Civil and Commercial

- 7.2.2. Military

- 7.3. Market Analysis, Insights and Forecast - by UAV Type

- 7.3.1. Micro UAV

- 7.3.2. Mini UAV

- 7.3.3. Tactical UAV

- 7.3.4. MALE UAV

- 7.3.5. HALE UAV

- 7.1. Market Analysis, Insights and Forecast - by Engine Type

- 8. Europe UAV Propulsion System Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Engine Type

- 8.1.1. Conventional

- 8.1.2. Hybrid

- 8.1.3. Full-electric

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Civil and Commercial

- 8.2.2. Military

- 8.3. Market Analysis, Insights and Forecast - by UAV Type

- 8.3.1. Micro UAV

- 8.3.2. Mini UAV

- 8.3.3. Tactical UAV

- 8.3.4. MALE UAV

- 8.3.5. HALE UAV

- 8.1. Market Analysis, Insights and Forecast - by Engine Type

- 9. Asia Pacific UAV Propulsion System Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Engine Type

- 9.1.1. Conventional

- 9.1.2. Hybrid

- 9.1.3. Full-electric

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Civil and Commercial

- 9.2.2. Military

- 9.3. Market Analysis, Insights and Forecast - by UAV Type

- 9.3.1. Micro UAV

- 9.3.2. Mini UAV

- 9.3.3. Tactical UAV

- 9.3.4. MALE UAV

- 9.3.5. HALE UAV

- 9.1. Market Analysis, Insights and Forecast - by Engine Type

- 10. Latin America UAV Propulsion System Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Engine Type

- 10.1.1. Conventional

- 10.1.2. Hybrid

- 10.1.3. Full-electric

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Civil and Commercial

- 10.2.2. Military

- 10.3. Market Analysis, Insights and Forecast - by UAV Type

- 10.3.1. Micro UAV

- 10.3.2. Mini UAV

- 10.3.3. Tactical UAV

- 10.3.4. MALE UAV

- 10.3.5. HALE UAV

- 10.1. Market Analysis, Insights and Forecast - by Engine Type

- 11. Middle East and Africa UAV Propulsion System Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Engine Type

- 11.1.1. Conventional

- 11.1.2. Hybrid

- 11.1.3. Full-electric

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Civil and Commercial

- 11.2.2. Military

- 11.3. Market Analysis, Insights and Forecast - by UAV Type

- 11.3.1. Micro UAV

- 11.3.2. Mini UAV

- 11.3.3. Tactical UAV

- 11.3.4. MALE UAV

- 11.3.5. HALE UAV

- 11.1. Market Analysis, Insights and Forecast - by Engine Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 BRP-Rotax GmbH & Co KG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Honeywell International Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ballard Power Systems Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 MMC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Orbital Corporation Limited

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Pratt & Whitney (RTX Corporation)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Diamond Aircraft Industries GmbH

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Intelligent Energy Limite

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Rolls-Royce plc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 H3 Dynamics Holdings Pte Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 3W International GmbH

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 General Electric Company

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 UAV Engines Limited

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Hirth Engines GmbH

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 BRP-Rotax GmbH & Co KG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global UAV Propulsion System Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America UAV Propulsion System Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 3: North America UAV Propulsion System Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 4: North America UAV Propulsion System Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: North America UAV Propulsion System Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America UAV Propulsion System Industry Revenue (Million), by UAV Type 2025 & 2033

- Figure 7: North America UAV Propulsion System Industry Revenue Share (%), by UAV Type 2025 & 2033

- Figure 8: North America UAV Propulsion System Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America UAV Propulsion System Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe UAV Propulsion System Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 11: Europe UAV Propulsion System Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 12: Europe UAV Propulsion System Industry Revenue (Million), by Application 2025 & 2033

- Figure 13: Europe UAV Propulsion System Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: Europe UAV Propulsion System Industry Revenue (Million), by UAV Type 2025 & 2033

- Figure 15: Europe UAV Propulsion System Industry Revenue Share (%), by UAV Type 2025 & 2033

- Figure 16: Europe UAV Propulsion System Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe UAV Propulsion System Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific UAV Propulsion System Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 19: Asia Pacific UAV Propulsion System Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 20: Asia Pacific UAV Propulsion System Industry Revenue (Million), by Application 2025 & 2033

- Figure 21: Asia Pacific UAV Propulsion System Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Asia Pacific UAV Propulsion System Industry Revenue (Million), by UAV Type 2025 & 2033

- Figure 23: Asia Pacific UAV Propulsion System Industry Revenue Share (%), by UAV Type 2025 & 2033

- Figure 24: Asia Pacific UAV Propulsion System Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific UAV Propulsion System Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America UAV Propulsion System Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 27: Latin America UAV Propulsion System Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 28: Latin America UAV Propulsion System Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Latin America UAV Propulsion System Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Latin America UAV Propulsion System Industry Revenue (Million), by UAV Type 2025 & 2033

- Figure 31: Latin America UAV Propulsion System Industry Revenue Share (%), by UAV Type 2025 & 2033

- Figure 32: Latin America UAV Propulsion System Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Latin America UAV Propulsion System Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa UAV Propulsion System Industry Revenue (Million), by Engine Type 2025 & 2033

- Figure 35: Middle East and Africa UAV Propulsion System Industry Revenue Share (%), by Engine Type 2025 & 2033

- Figure 36: Middle East and Africa UAV Propulsion System Industry Revenue (Million), by Application 2025 & 2033

- Figure 37: Middle East and Africa UAV Propulsion System Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: Middle East and Africa UAV Propulsion System Industry Revenue (Million), by UAV Type 2025 & 2033

- Figure 39: Middle East and Africa UAV Propulsion System Industry Revenue Share (%), by UAV Type 2025 & 2033

- Figure 40: Middle East and Africa UAV Propulsion System Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East and Africa UAV Propulsion System Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global UAV Propulsion System Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 2: Global UAV Propulsion System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global UAV Propulsion System Industry Revenue Million Forecast, by UAV Type 2020 & 2033

- Table 4: Global UAV Propulsion System Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global UAV Propulsion System Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 6: Global UAV Propulsion System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 7: Global UAV Propulsion System Industry Revenue Million Forecast, by UAV Type 2020 & 2033

- Table 8: Global UAV Propulsion System Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Global UAV Propulsion System Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 12: Global UAV Propulsion System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 13: Global UAV Propulsion System Industry Revenue Million Forecast, by UAV Type 2020 & 2033

- Table 14: Global UAV Propulsion System Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United Kingdom UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: France UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Germany UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global UAV Propulsion System Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 20: Global UAV Propulsion System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 21: Global UAV Propulsion System Industry Revenue Million Forecast, by UAV Type 2020 & 2033

- Table 22: Global UAV Propulsion System Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 23: China UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Japan UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: South Korea UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global UAV Propulsion System Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 29: Global UAV Propulsion System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 30: Global UAV Propulsion System Industry Revenue Million Forecast, by UAV Type 2020 & 2033

- Table 31: Global UAV Propulsion System Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: Brazil UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Mexico UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Rest of Latin America UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Global UAV Propulsion System Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 36: Global UAV Propulsion System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 37: Global UAV Propulsion System Industry Revenue Million Forecast, by UAV Type 2020 & 2033

- Table 38: Global UAV Propulsion System Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 39: United Arab Emirates UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Saudi Arabia UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: Qatar UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: South Africa UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: Rest of Middle East and Africa UAV Propulsion System Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UAV Propulsion System Industry?

The projected CAGR is approximately 5.84%.

2. Which companies are prominent players in the UAV Propulsion System Industry?

Key companies in the market include BRP-Rotax GmbH & Co KG, Honeywell International Inc, Ballard Power Systems Inc, MMC, Orbital Corporation Limited, Pratt & Whitney (RTX Corporation), Diamond Aircraft Industries GmbH, Intelligent Energy Limite, Rolls-Royce plc, H3 Dynamics Holdings Pte Ltd, 3W International GmbH, General Electric Company, UAV Engines Limited, Hirth Engines GmbH.

3. What are the main segments of the UAV Propulsion System Industry?

The market segments include Engine Type, Application, UAV Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.17 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Commercial Segment is Expected to Lead the Market During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UAV Propulsion System Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UAV Propulsion System Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UAV Propulsion System Industry?

To stay informed about further developments, trends, and reports in the UAV Propulsion System Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence