Key Insights

The Autonomous Vehicles Sensor market is experiencing rapid growth, projected to reach a substantial size by 2033. Driven by the increasing adoption of autonomous driving technologies globally, the market's Compound Annual Growth Rate (CAGR) of 19.60% from 2019-2024 indicates significant investor interest and technological advancements. Key drivers include the rising demand for enhanced safety features in vehicles, stricter government regulations promoting autonomous driving, and continuous improvements in sensor technology, leading to higher accuracy, reliability, and affordability. Market segmentation reveals passenger cars currently hold the largest share, followed by light commercial vehicles (LCVs). However, heavy commercial vehicles (HCVs) are expected to witness significant growth in the forecast period due to the potential for increased efficiency and safety in logistics and transportation. The emergence of innovative sensor types, like LiDAR and radar, alongside advancements in artificial intelligence and machine learning for data processing, are shaping market trends. Despite these positive developments, challenges remain, including high initial investment costs associated with autonomous vehicle development, concerns about data security and privacy, and the need for robust regulatory frameworks to ensure safe deployment.

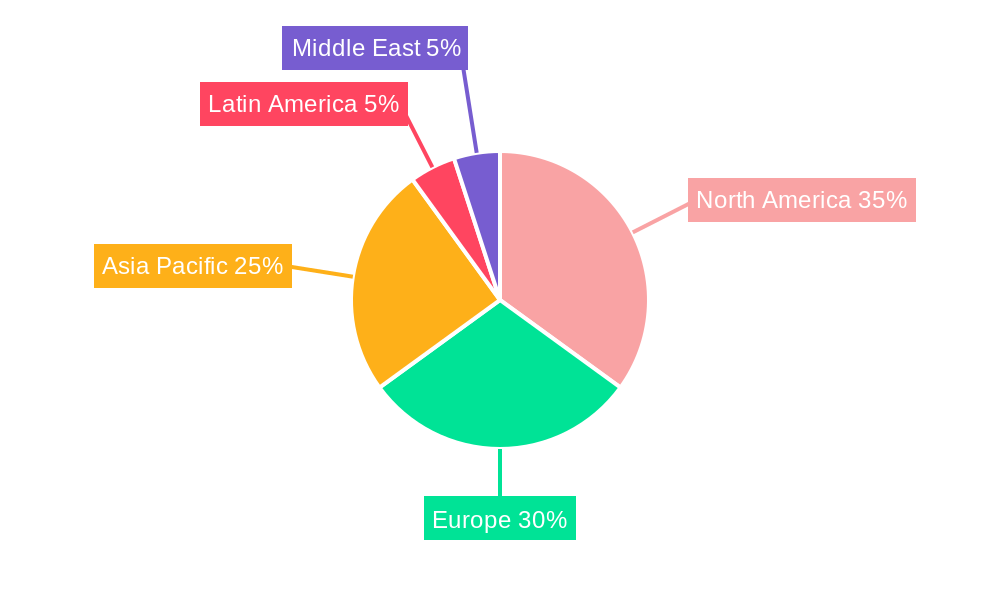

Leading players like Infineon Technologies AG, Microchip Technology Inc., and Bosch are investing heavily in research and development, driving innovation and competition. Geographic distribution shows a strong presence in North America and Europe, driven by early adoption of autonomous vehicle technologies. However, the Asia-Pacific region is expected to witness the fastest growth due to increasing investments in infrastructure and a burgeoning automotive industry. The continued expansion of 5G networks will further accelerate market growth by facilitating seamless data transmission between sensors and central processing units. Addressing the limitations through continued technological advancements and collaborative efforts between governments and industry players is critical to unlocking the full potential of the autonomous vehicle sensor market.

Autonomous Vehicles Sensor Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Autonomous Vehicles Sensor industry, encompassing market dynamics, growth trends, regional dominance, product landscape, key players, and future outlook. The study period covers 2019-2033, with a focus on the base year 2025 and a forecast period of 2025-2033. This report is crucial for industry professionals, investors, and strategists seeking to understand and capitalize on the burgeoning opportunities within this rapidly evolving sector. The parent market is the automotive industry, while the child market is specifically autonomous vehicle technology.

Autonomous Vehicles Sensor Industry Market Dynamics & Structure

The autonomous vehicles sensor market is characterized by intense competition, driven by rapid technological advancements and increasing demand for safer and more efficient autonomous driving systems. Market concentration is moderate, with several key players holding significant market share, but with numerous smaller companies also contributing to innovation. The market is shaped by stringent regulatory frameworks governing the safety and reliability of autonomous vehicles, leading to high barriers to entry for new players. Furthermore, the industry witnesses continuous technological innovation, with companies investing heavily in the development of advanced sensors such as LiDAR, radar, cameras, and ultrasonic sensors. The market also sees significant M&A activity, with larger companies acquiring smaller, more specialized sensor technology firms to enhance their product portfolios and expand their market reach.

- Market Concentration: Moderate, with top 5 players holding xx% of the market share in 2024 (estimated).

- Technological Innovation: Focus on higher resolution, improved accuracy, and sensor fusion techniques.

- Regulatory Frameworks: Stringent safety standards and compliance requirements drive innovation and cost.

- Competitive Product Substitutes: Limited direct substitutes, but continuous improvement in sensor technology creates indirect competition.

- End-User Demographics: Primarily automotive manufacturers and Tier-1 suppliers, with growing involvement of technology companies.

- M&A Trends: Increasing consolidation through acquisitions of smaller sensor technology companies. xx M&A deals were recorded between 2019 and 2024 (estimated).

Autonomous Vehicles Sensor Industry Growth Trends & Insights

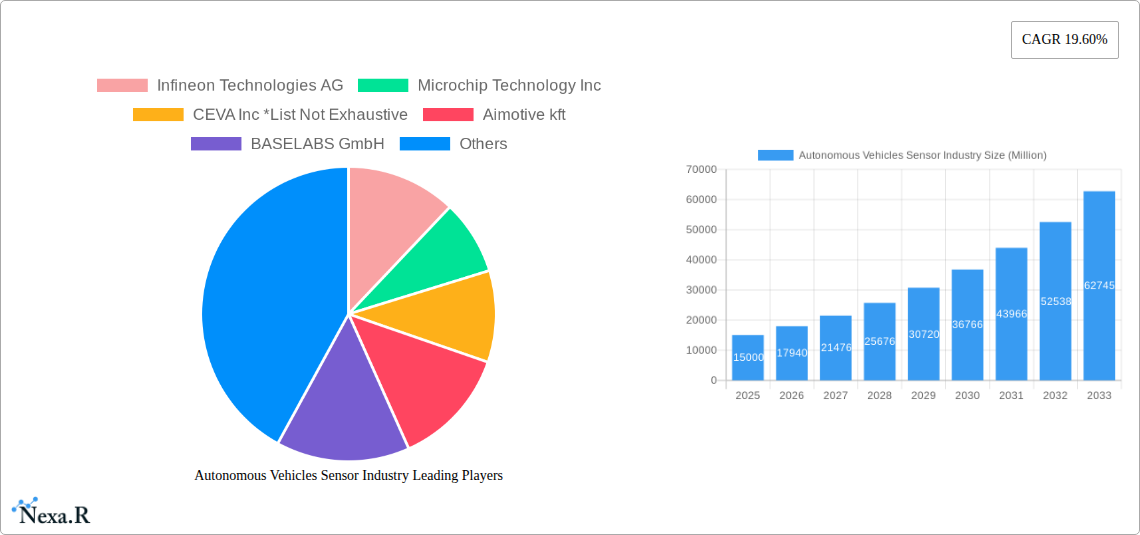

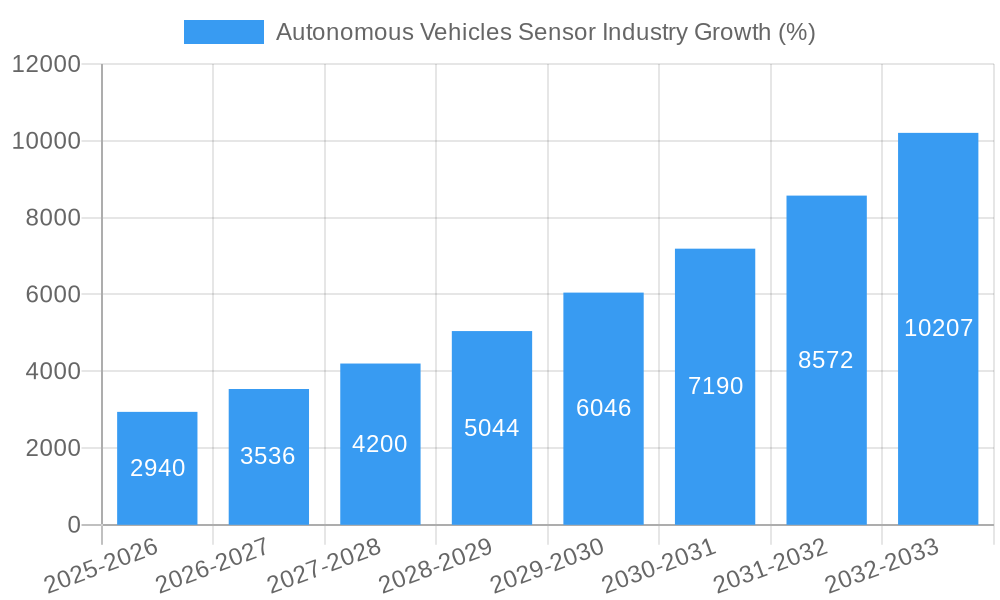

The autonomous vehicles sensor market is experiencing significant growth, driven by the increasing adoption of autonomous driving technologies globally. The market size has grown from xx million units in 2019 to xx million units in 2024, and is projected to reach xx million units by 2033. This growth is primarily attributed to technological advancements, falling sensor costs, and supportive government regulations. The adoption rate of autonomous vehicles is steadily increasing, though challenges remain concerning consumer acceptance and regulatory approvals. Technological disruptions, such as the development of more efficient and cost-effective sensors, are accelerating market growth. Consumer behavior shifts towards greater demand for safer and more convenient transportation are fueling this sector's expansion. The CAGR for the forecast period (2025-2033) is estimated at xx%. Market penetration is expected to reach xx% by 2033.

Dominant Regions, Countries, or Segments in Autonomous Vehicles Sensor Industry

North America and Europe currently dominate the autonomous vehicles sensor market, driven by high levels of technological advancement, substantial investments in R&D, and supportive government policies. However, the Asia-Pacific region is expected to witness significant growth in the coming years due to rapid economic growth, increasing urbanization, and rising demand for advanced transportation solutions. Within the "By Types of Vehicle" segmentation, passenger cars currently hold the largest market share due to high demand for advanced driver-assistance systems (ADAS) and autonomous features. However, the light commercial vehicle (LCV) and heavy commercial vehicle (HCV) segments are also expected to experience significant growth.

- Key Drivers in North America: Strong R&D investments, early adoption of autonomous technologies, supportive regulatory environment.

- Key Drivers in Europe: High technological expertise, stringent safety regulations, growing demand for ADAS features.

- Key Drivers in Asia-Pacific: Rapid economic growth, increasing urbanization, government initiatives promoting autonomous vehicles.

- Passenger Car Segment Dominance: High demand for ADAS and autonomous features in passenger vehicles.

- Growth Potential in LCV and HCV segments: Increasing demand for automation in logistics and transportation.

Autonomous Vehicles Sensor Industry Product Landscape

The autonomous vehicles sensor market offers a diverse range of products, including LiDAR, radar, cameras, and ultrasonic sensors. These sensors vary in terms of their sensing capabilities, range, accuracy, and cost. Ongoing innovations focus on enhancing sensor performance, reducing costs, and integrating multiple sensor modalities for improved reliability and accuracy. Unique selling propositions (USPs) often include higher resolution, better accuracy, extended range, and improved power efficiency. Technological advancements are driven by the development of more sophisticated algorithms for data processing and fusion.

Key Drivers, Barriers & Challenges in Autonomous Vehicles Sensor Industry

Key Drivers:

- Technological advancements leading to improved sensor performance and reduced costs.

- Increasing demand for enhanced safety and driver assistance features.

- Government regulations and incentives promoting the adoption of autonomous vehicles.

- Growing investments in R&D by both established and emerging players.

Key Barriers & Challenges:

- High initial investment costs associated with developing and deploying autonomous driving technologies.

- Safety concerns and regulatory hurdles surrounding autonomous vehicle deployment.

- Competition from established players and new entrants into the market.

- Supply chain disruptions and the availability of raw materials. These disruptions can cause delays and increased costs, impacting xx% of production in 2024 (estimated).

Emerging Opportunities in Autonomous Vehicles Sensor Industry

- Expansion into emerging markets with high growth potential.

- Development of innovative applications for autonomous vehicles in various sectors (e.g., logistics, agriculture).

- Integration of artificial intelligence and machine learning for improved sensor performance and data processing.

- Focus on environmentally sustainable and energy-efficient sensor technologies.

Growth Accelerators in the Autonomous Vehicles Sensor Industry

Long-term growth will be fueled by continuous technological innovation, resulting in smaller, cheaper, and more power-efficient sensors. Strategic partnerships between sensor manufacturers, automotive companies, and technology firms will further accelerate market expansion. Government initiatives promoting the adoption of autonomous vehicles, coupled with increasing consumer demand for safer and more convenient transportation, will also play a vital role in driving future growth.

Key Players Shaping the Autonomous Vehicles Sensor Industry Market

- Infineon Technologies AG

- Microchip Technology Inc

- CEVA Inc

- Aimotive kft

- BASELABS GmbH

- NXP Semiconductor

- STMicroelectronics NV

- Kionix Inc (Rohm Co Ltd)

- Robert Bosch GmbH

- TDK Corporation

Notable Milestones in Autonomous Vehicles Sensor Industry Sector

- January 2022: Ambarella Inc. launched the CV3 AI domain controller family, offering high AI processing performance and multi-sensor fusion capabilities. This significantly advanced the capabilities of autonomous vehicle perception systems.

- January 2022: Qualcomm launched the Snapdragon Ride Vision System, an open and scalable platform for automated driving, enhancing customization options for automakers and integrating various advanced technologies.

In-Depth Autonomous Vehicles Sensor Industry Market Outlook

The future of the autonomous vehicles sensor market is bright, with significant growth potential driven by technological advancements, increasing adoption of autonomous vehicles, and supportive government policies. Strategic partnerships and investments in R&D will further accelerate market expansion. Opportunities abound for companies that can develop innovative sensor technologies, offer cost-effective solutions, and meet the stringent safety requirements of the autonomous vehicle industry. The market is poised for significant expansion across various vehicle types and geographic regions, creating a lucrative landscape for players who can adapt to the ever-evolving demands of this dynamic sector.

Autonomous Vehicles Sensor Industry Segmentation

-

1. Types of Vehicle

- 1.1. Passenger Cars

- 1.2. Light Commercial Vehicle (LCV)

- 1.3. Heavy Commercial Vehicle (HCV)

- 1.4. Other Autonomous Vehicles

Autonomous Vehicles Sensor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Autonomous Vehicles Sensor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 19.60% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Demand for Autonomous Vehicles; Efficient Real Time Data Processing and Data Sharing Capabilities to Drive the Demand

- 3.3. Market Restrains

- 3.3.1. Lack of Standardization in Sensor Fusion Technology

- 3.4. Market Trends

- 3.4.1. Passenger Cars to Hold a Significant Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 5.1.1. Passenger Cars

- 5.1.2. Light Commercial Vehicle (LCV)

- 5.1.3. Heavy Commercial Vehicle (HCV)

- 5.1.4. Other Autonomous Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 6. North America Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 6.1.1. Passenger Cars

- 6.1.2. Light Commercial Vehicle (LCV)

- 6.1.3. Heavy Commercial Vehicle (HCV)

- 6.1.4. Other Autonomous Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 7. Europe Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 7.1.1. Passenger Cars

- 7.1.2. Light Commercial Vehicle (LCV)

- 7.1.3. Heavy Commercial Vehicle (HCV)

- 7.1.4. Other Autonomous Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 8. Asia Pacific Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 8.1.1. Passenger Cars

- 8.1.2. Light Commercial Vehicle (LCV)

- 8.1.3. Heavy Commercial Vehicle (HCV)

- 8.1.4. Other Autonomous Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 9. Latin America Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 9.1.1. Passenger Cars

- 9.1.2. Light Commercial Vehicle (LCV)

- 9.1.3. Heavy Commercial Vehicle (HCV)

- 9.1.4. Other Autonomous Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 10. Middle East Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 10.1.1. Passenger Cars

- 10.1.2. Light Commercial Vehicle (LCV)

- 10.1.3. Heavy Commercial Vehicle (HCV)

- 10.1.4. Other Autonomous Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Types of Vehicle

- 11. North America Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Europe Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Asia Pacific Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Latin America Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Middle East Autonomous Vehicles Sensor Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Infineon Technologies AG

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Microchip Technology Inc

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 CEVA Inc *List Not Exhaustive

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Aimotive kft

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 BASELABS GmbH

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 NXP Semiconductor

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 STMicroelectronics NV

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Kionix Inc (Rohm Co Ltd)

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Robert Bosch GmbH

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 TDK Corporation

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Infineon Technologies AG

List of Figures

- Figure 1: Global Autonomous Vehicles Sensor Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Autonomous Vehicles Sensor Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Autonomous Vehicles Sensor Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Autonomous Vehicles Sensor Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Latin America Autonomous Vehicles Sensor Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Latin America Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East Autonomous Vehicles Sensor Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Autonomous Vehicles Sensor Industry Revenue (Million), by Types of Vehicle 2024 & 2032

- Figure 13: North America Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2024 & 2032

- Figure 14: North America Autonomous Vehicles Sensor Industry Revenue (Million), by Country 2024 & 2032

- Figure 15: North America Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 16: Europe Autonomous Vehicles Sensor Industry Revenue (Million), by Types of Vehicle 2024 & 2032

- Figure 17: Europe Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2024 & 2032

- Figure 18: Europe Autonomous Vehicles Sensor Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: Europe Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Asia Pacific Autonomous Vehicles Sensor Industry Revenue (Million), by Types of Vehicle 2024 & 2032

- Figure 21: Asia Pacific Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2024 & 2032

- Figure 22: Asia Pacific Autonomous Vehicles Sensor Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Asia Pacific Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Latin America Autonomous Vehicles Sensor Industry Revenue (Million), by Types of Vehicle 2024 & 2032

- Figure 25: Latin America Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2024 & 2032

- Figure 26: Latin America Autonomous Vehicles Sensor Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: Latin America Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 28: Middle East Autonomous Vehicles Sensor Industry Revenue (Million), by Types of Vehicle 2024 & 2032

- Figure 29: Middle East Autonomous Vehicles Sensor Industry Revenue Share (%), by Types of Vehicle 2024 & 2032

- Figure 30: Middle East Autonomous Vehicles Sensor Industry Revenue (Million), by Country 2024 & 2032

- Figure 31: Middle East Autonomous Vehicles Sensor Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Types of Vehicle 2019 & 2032

- Table 3: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Autonomous Vehicles Sensor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Autonomous Vehicles Sensor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: Autonomous Vehicles Sensor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Autonomous Vehicles Sensor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 13: Autonomous Vehicles Sensor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Types of Vehicle 2019 & 2032

- Table 15: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Types of Vehicle 2019 & 2032

- Table 17: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Types of Vehicle 2019 & 2032

- Table 19: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Types of Vehicle 2019 & 2032

- Table 21: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Types of Vehicle 2019 & 2032

- Table 23: Global Autonomous Vehicles Sensor Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Autonomous Vehicles Sensor Industry?

The projected CAGR is approximately 19.60%.

2. Which companies are prominent players in the Autonomous Vehicles Sensor Industry?

Key companies in the market include Infineon Technologies AG, Microchip Technology Inc, CEVA Inc *List Not Exhaustive, Aimotive kft, BASELABS GmbH, NXP Semiconductor, STMicroelectronics NV, Kionix Inc (Rohm Co Ltd), Robert Bosch GmbH, TDK Corporation.

3. What are the main segments of the Autonomous Vehicles Sensor Industry?

The market segments include Types of Vehicle.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Autonomous Vehicles; Efficient Real Time Data Processing and Data Sharing Capabilities to Drive the Demand.

6. What are the notable trends driving market growth?

Passenger Cars to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Lack of Standardization in Sensor Fusion Technology.

8. Can you provide examples of recent developments in the market?

January 2022 - Ambarella Inc., an AI vision silicon company, launched the CV3 AI domain controller family during CES. This power-efficient and fully scalable CVflow family of SoCs provides the automotive industry's highest AI processing performance at up to 500 eTOPS. Furthermore, the product family enables centralized, single-chip processing for multi-sensor perception-including radar, high-resolution vision, ultrasonic, and lidar- and AV path planning and deep fusion for multiple sensor modalities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Autonomous Vehicles Sensor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Autonomous Vehicles Sensor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Autonomous Vehicles Sensor Industry?

To stay informed about further developments, trends, and reports in the Autonomous Vehicles Sensor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence