Key Insights for Blood Collection Robot Market

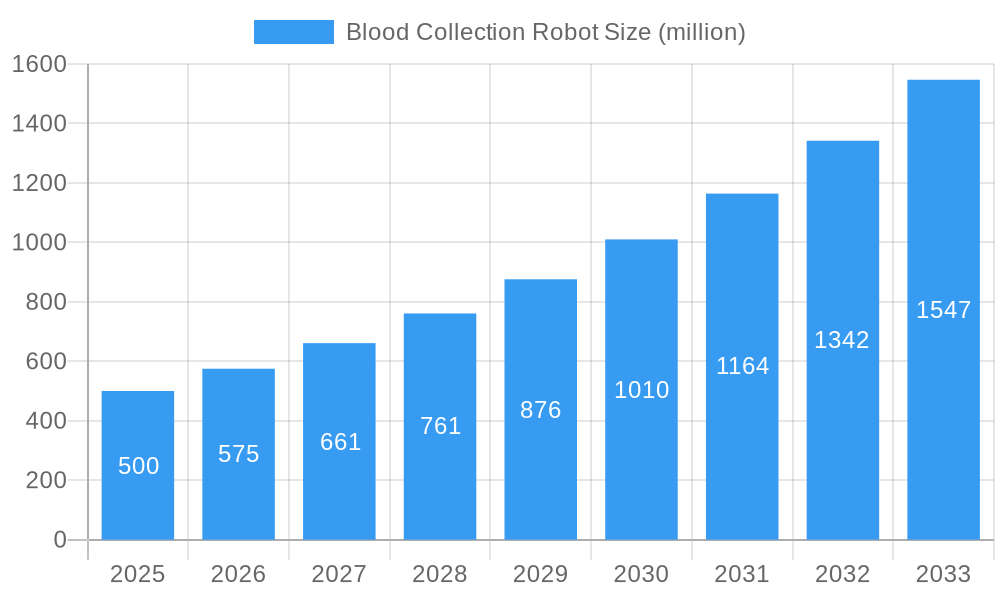

The global Blood Collection Robot Market is poised for substantial growth, driven by an escalating demand for enhanced patient safety, operational efficiency in clinical settings, and the ongoing labor shortage in healthcare. Valued at an estimated $10.8 billion in 2025, the market is projected to expand at a robust Compound Annual Growth Rate (CAGR) of 6% over the forecast period, reaching approximately $19.34 billion by 2035. This trajectory is underpinned by significant advancements in robotics, artificial intelligence, and machine vision technologies, making automated blood collection systems increasingly viable and desirable.

Blood Collection Robot Market Size (In Billion)

Key demand drivers include the imperative to minimize human error in venipuncture, reduce the risk of needlestick injuries for healthcare professionals, and improve the overall patient experience by reducing discomfort and anxiety associated with traditional blood draws. The increasing volume of diagnostic tests performed globally, coupled with an aging population requiring frequent medical monitoring, further fuels the adoption of robotic solutions. Furthermore, the integration capabilities of these robots with existing hospital information systems (HIS) and laboratory information systems (LIS) are enhancing their appeal for streamlining workflows. The broader Healthcare Robotics Market is experiencing a surge in innovation, with blood collection robots representing a critical sub-segment focused on routine, high-volume procedures. This technological shift is also contributing to the expansion of the Automated Medical Devices Market, where precision and automation are paramount. The market's growth is also influenced by the evolving landscape of the Diagnostic Testing Market, as more tests necessitate efficient and accurate sample collection. As healthcare providers seek to optimize resource allocation and enhance care quality, the strategic investment in advanced robotic systems is becoming a strategic imperative, thereby stimulating consistent market expansion.

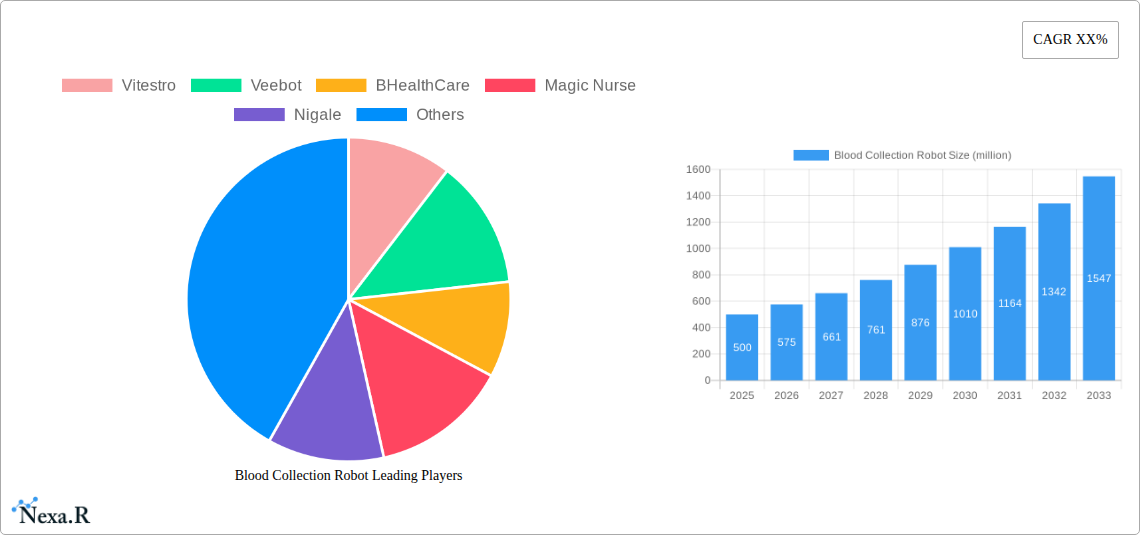

Blood Collection Robot Company Market Share

Automated Blood Collection Robots Segment Dominance in Blood Collection Robot Market

The Automated Blood Collection Robots sub-segment within the Product Type category currently holds the dominant revenue share in the Blood Collection Robot Market and is anticipated to maintain its lead throughout the forecast period. This dominance is primarily attributable to its inherent advantages in efficiency, precision, and the significant reduction of manual intervention. Fully automated systems leverage sophisticated technologies such as artificial intelligence and machine vision for accurate vein identification, robotic arm manipulation for precise needle insertion, and integrated systems for sample handling and labeling, thereby minimizing human error and enhancing patient safety. These systems are designed to perform the entire venipuncture process autonomously, from vein detection to tube filling and removal, offering a seamless and standardized procedure.

Key players in this dominant segment, such as Vitestro, Veebot, and BHealthCare, are actively developing and refining their automated platforms to meet the rigorous demands of clinical environments. Vitestro, for instance, focuses on intelligent venipuncture devices that integrate ultrasound imaging with AI to guide needle placement. Veebot specializes in systems that use infrared imaging and proprietary algorithms to identify optimal venipuncture sites. BHealthCare is expanding its portfolio to include comprehensive automated solutions that streamline not just blood collection but also subsequent sample processing. The market for these advanced automated systems is experiencing significant growth, driven by their ability to address critical challenges like skilled labor shortages, the need for consistent performance across varied patient demographics, and the increasing volume of blood tests required for diagnosis and monitoring. While semi-automated solutions offer a stepping stone to full automation, the long-term trend strongly favors fully automated robots due to their superior capability for integration into the broader Hospital Automation Market and their potential for greater cost savings through reduced labor and improved throughput. This segment's growth trajectory is further supported by the expanding Medical Device Manufacturing Market, which continuously introduces more robust and technologically advanced components into these systems.

Key Market Drivers and Constraints in Blood Collection Robot Market

The Blood Collection Robot Market is influenced by a confluence of potent drivers and significant constraints:

Market Drivers:

- Aging Global Population and Rising Chronic Disease Prevalence: The global demographic shift towards an older population, coupled with an increasing incidence of chronic diseases like diabetes and cardiovascular conditions, necessitates more frequent diagnostic blood tests. This surge in testing volumes places immense pressure on traditional phlebotomy services, making automated solutions a critical asset for managing increased workload efficiently and consistently. This driver significantly impacts the demand within the Diagnostic Testing Market.

- Escalating Healthcare Labor Shortages: Healthcare systems worldwide are grappling with severe shortages of skilled phlebotomists and nursing staff. Blood collection robots offer a viable solution to augment human resources, reduce staff burnout, and ensure uninterrupted service delivery, particularly in high-volume settings. This factor is crucial for the adoption of solutions across the Clinical Laboratory Automation Market.

- Enhanced Patient Safety and Experience: Robotic systems can significantly reduce the risk of needlestick injuries for both patients and healthcare workers, improve accuracy in vein selection, and minimize patient discomfort and anxiety through precise, consistent performance. This leads to better patient outcomes and satisfaction, driving adoption in patient-centric healthcare facilities.

- Technological Advancements in AI and Robotics: Continuous innovation in artificial intelligence and machine vision, coupled with more sophisticated robotic arms and sensor technology, is making blood collection robots more intelligent, precise, and adaptable. These advancements enhance the robots' ability to handle complex venipuncture scenarios and integrate seamlessly into existing healthcare IT infrastructure, boosting the Artificial Intelligence in Healthcare Market.

Market Constraints:

- High Initial Investment Costs: The capital expenditure required for acquiring and installing blood collection robots can be substantial, posing a significant barrier for smaller hospitals, clinics, and diagnostic centers, particularly in developing regions. This economic hurdle necessitates a strong return-on-investment justification.

- Regulatory Hurdles and Ethical Considerations: Navigating complex regulatory approval processes for medical devices, especially those involving patient contact and autonomy, can be time-consuming and expensive. Furthermore, ethical considerations regarding patient acceptance of robotic medical procedures and data privacy for image-based vein mapping systems present challenges.

- Integration Complexities with Existing Infrastructure: Seamless integration of robotic systems with diverse and often disparate hospital information systems (HIS) and laboratory information systems (LIS) can be challenging. Compatibility issues and the need for significant IT overhauls can deter adoption.

- Dependence on Medical Consumables Market: While robots automate the process, they still rely on a steady supply of specific, often proprietary, sterile consumables (e.g., tubes, needles, collection kits). Any disruption or price volatility in the Medical Consumables Market can impact operational costs and robot utility.

Competitive Ecosystem of Blood Collection Robot Market

The Blood Collection Robot Market features a developing competitive landscape, characterized by specialized startups and innovative technology firms, alongside increasing interest from established medical device manufacturers. The emphasis is on precision, safety, and seamless integration into healthcare workflows.

- Vitestro: A pioneer in autonomous blood drawing, Vitestro focuses on developing intelligent venipuncture devices that combine robotics, ultrasound imaging, and artificial intelligence to identify veins and perform blood collection with high accuracy and consistency. Their systems aim to reduce errors and improve the patient and staff experience.

- Veebot: Specializes in creating automated venipuncture robots utilizing advanced imaging and AI algorithms to locate and access veins. Veebot's technology is designed to enhance efficiency and minimize patient discomfort by ensuring precise needle placement, targeting a more streamlined blood collection process.

- BHealthCare: This company is involved in the development of robotic solutions for various medical applications, including automated blood sampling. BHealthCare aims to integrate advanced robotics with clinical workflows to improve laboratory automation and healthcare delivery efficiency, catering to a broader segment of the Healthcare Robotics Market.

- Others: This category includes emerging startups and divisions of larger medical technology corporations that are either in the research and development phase or have niche offerings in specific segments of automated blood sampling. These players contribute to market innovation through novel sensor technology and software integrations, expanding the capabilities of robotic systems in healthcare.

Recent Developments & Milestones in Blood Collection Robot Market

Recent advancements are rapidly shaping the Blood Collection Robot Market, focusing on enhanced autonomy, improved patient comfort, and broader clinical applicability.

- December 2024: A leading medical technology firm announced a strategic partnership with a prominent AI software developer to integrate advanced predictive analytics into their next-generation blood collection robots. This collaboration aims to enhance vein visualization and reduce procedure time, thereby improving throughput in diagnostic laboratories.

- October 2024: The European Medical Device Regulation (EU MDR) approval was granted to a new semi-automated blood collection robot, signifying its compliance with stringent safety and performance standards. This approval is expected to accelerate its adoption across European hospitals and diagnostic centers.

- August 2024: A significant Series C funding round was closed by a startup specializing in robotic venipuncture, securing $50 million to scale manufacturing and expand its market reach into North America. The investment highlights strong investor confidence in the long-term potential of the Automated Medical Devices Market.

- May 2024: Researchers unveiled a prototype blood collection robot at a major medical conference, featuring haptic feedback technology for enhanced operator control during complex cases and improved patient interaction. This development points towards a future of more versatile and adaptive robotic systems.

- February 2024: A hospital network in the Asia Pacific region successfully concluded a pilot program for automated blood collection robots, reporting a 25% reduction in needlestick injuries and a 15% improvement in patient satisfaction scores. This successful trial underscores the tangible benefits of robotic integration in clinical practice.

Regional Market Breakdown for Blood Collection Robot Market

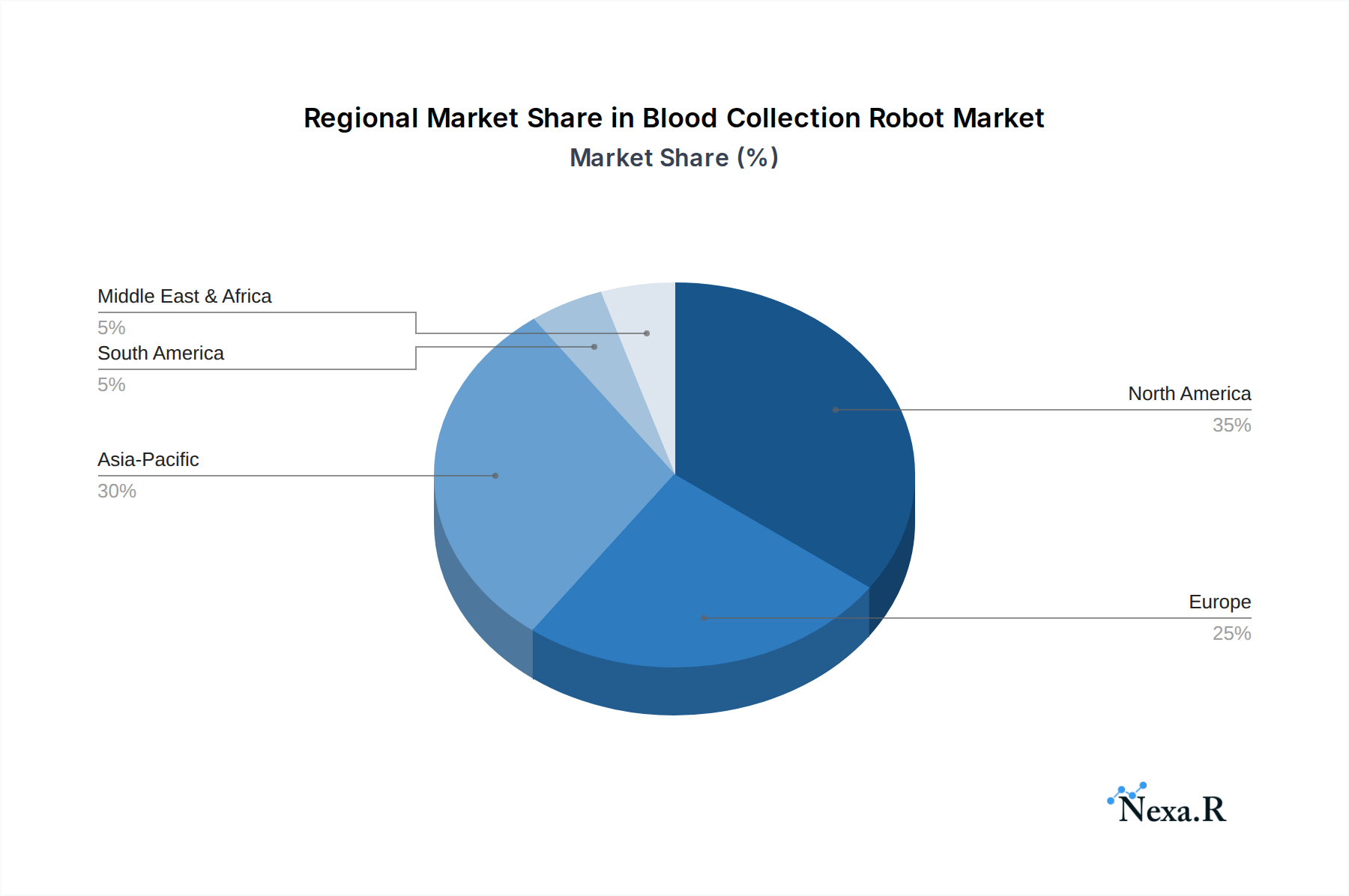

The Blood Collection Robot Market exhibits distinct regional dynamics, influenced by varying healthcare infrastructures, technological adoption rates, and regulatory landscapes. Globally, the market is poised for expansion, but specific regions are driving growth more aggressively.

North America holds the largest revenue share in the Blood Collection Robot Market, estimated at over 35% in 2025, primarily driven by high healthcare expenditure, sophisticated medical infrastructure, and a strong emphasis on automation to combat rising labor costs and improve patient outcomes. The United States, in particular, is a key market, fueled by robust research and development activities in the Healthcare Robotics Market and a high adoption rate of advanced medical technologies. The regional CAGR is projected at a steady 5.8%, with the primary demand driver being the need for efficiency in high-volume Diagnostic Testing Market environments.

Europe represents another significant market, accounting for approximately 30% of the global revenue in 2025. Countries like Germany, the UK, and France are leading the adoption due to stringent patient safety regulations, an aging population, and a strong push for hospital automation. The regional CAGR is projected at 5.5%, with the key demand driver being the emphasis on reducing healthcare-associated infections and improving workflow standardization. The presence of a mature Medical Device Manufacturing Market also supports regional innovation.

Asia Pacific is identified as the fastest-growing region, with a projected CAGR exceeding 7.5% over the forecast period. While currently holding a smaller market share, around 20% in 2025, its rapid expansion is attributed to improving healthcare infrastructure, increasing healthcare spending, a massive patient pool, and a growing awareness of advanced medical technologies in countries like China, India, and Japan. The primary demand driver here is the burgeoning demand for accessible and efficient healthcare services in densely populated areas, alongside governmental initiatives promoting medical innovation. This region is a crucial hub for the future of the Clinical Laboratory Automation Market.

Middle East & Africa (MEA) and Latin America are emerging markets, currently holding smaller shares but demonstrating promising growth trajectories. These regions are projected to experience CAGRs of 6.2% and 6.5% respectively, driven by increasing investments in healthcare infrastructure, the expansion of diagnostic centers, and a growing recognition of the benefits of automation. However, higher initial investment costs and regulatory hurdles may temper the pace of adoption compared to more developed markets. The demand is primarily spurred by the need to modernize healthcare facilities and improve basic medical service delivery.

Blood Collection Robot Regional Market Share

Investment & Funding Activity in Blood Collection Robot Market

Investment and funding activity in the Blood Collection Robot Market have seen a noticeable uptick over the past 2-3 years, reflecting growing confidence in automated healthcare solutions. Venture capital firms are increasingly channeling funds into startups developing next-generation robotic venipuncture systems, particularly those integrating advanced Artificial Intelligence in Healthcare Market solutions. For instance, late 2023 saw a Series B funding round of $35 million for a European firm specializing in AI-powered vein detection and robotic arm precision, aimed at accelerating product commercialization and market penetration. This trend suggests a strong investor focus on enabling technologies that enhance accuracy and reduce operator dependency.

Strategic partnerships are also a key feature, with established Medical Device Manufacturing Market players looking to acquire or collaborate with smaller, innovative tech companies. For example, in early 2024, a major diagnostics company entered a joint development agreement with a sensor technology specialist to integrate novel biosensors into robotic blood collection platforms, enhancing their diagnostic capabilities beyond just venipuncture. This move aims to expand the utility of these robots into more comprehensive diagnostic workflows. Acquisitions, while less frequent, often target companies with proprietary algorithms or patented robotic mechanisms, reflecting a drive for technological advantage. The sub-segments attracting the most capital are those promising greater autonomy, miniaturization, and seamless integration with existing hospital IT infrastructure, aligning with the broader push towards the Hospital Automation Market. This sustained investment is crucial for overcoming R&D challenges and bringing these complex medical devices to wider clinical adoption.

Supply Chain & Raw Material Dynamics for Blood Collection Robot Market

The Blood Collection Robot Market is inherently reliant on a complex global supply chain, marked by dependencies on specialized components and susceptible to various sourcing risks. Upstream dependencies include high-precision motors for robotic arm articulation, advanced sensor technology for vein detection and depth perception, microcontrollers and integrated circuits for computational processing, and medical-grade plastics for sterile contact components and disposables. Optical components, such as cameras and infrared sensors, are also critical for machine vision capabilities, directly impacting the accuracy and safety of the devices. The reliance on the broader Sensor Technology Market is significant, as advancements in this area directly translate to improved robotic performance.

Sourcing risks are primarily tied to geopolitical tensions, trade disputes, and global events that can disrupt the flow of electronic components, particularly semiconductors. The COVID-19 pandemic, for instance, highlighted vulnerabilities in the semiconductor supply chain, leading to delays in product development and manufacturing for many Automated Medical Devices Market players. Price volatility for key inputs, such as rare earth elements used in high-performance magnets for motors, and specific medical-grade polymers, can directly impact the cost of production and, consequently, the final market price of blood collection robots. Any significant increase in the cost of these raw materials, or a shortage, could lead to increased manufacturing costs and potential delays in product availability, affecting the growth trajectory of the Blood Collection Robot Market. Furthermore, ensuring a steady and sterile supply of proprietary Medical Consumables Market items (e.g., specialized needle sets, tube holders) that are compatible with robotic systems is crucial. Disruptions in the supply of these consumables can render advanced robots inoperable, posing a significant challenge to healthcare facilities that have invested in automation.

Blood Collection Robot Segmentation

-

1. Product Type

- 1.1. Automated Blood Collection Robots

- 1.2. Semi-Automated Blood Collection Robots

-

2. Technology

- 2.1. Artificial Intelligence and Machine Vision

- 2.2. Sensor Technology

- 2.3. Others

-

3. Application

- 3.1. Venipuncture

- 3.2. Fingerstick/Capillary Blood Collection

- 3.3. Arterial Blood Collection

-

4. End User

- 4.1. Hospitals

- 4.2. Diagnostic Centers & Laboratories

- 4.3. Blood Banks

- 4.4. Research Institutes

- 4.5. Others

Blood Collection Robot Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Blood Collection Robot Regional Market Share

Geographic Coverage of Blood Collection Robot

Blood Collection Robot REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Automated Blood Collection Robots

- 5.1.2. Semi-Automated Blood Collection Robots

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Artificial Intelligence and Machine Vision

- 5.2.2. Sensor Technology

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Venipuncture

- 5.3.2. Fingerstick/Capillary Blood Collection

- 5.3.3. Arterial Blood Collection

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Hospitals

- 5.4.2. Diagnostic Centers & Laboratories

- 5.4.3. Blood Banks

- 5.4.4. Research Institutes

- 5.4.5. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Blood Collection Robot Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Automated Blood Collection Robots

- 6.1.2. Semi-Automated Blood Collection Robots

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Artificial Intelligence and Machine Vision

- 6.2.2. Sensor Technology

- 6.2.3. Others

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Venipuncture

- 6.3.2. Fingerstick/Capillary Blood Collection

- 6.3.3. Arterial Blood Collection

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Hospitals

- 6.4.2. Diagnostic Centers & Laboratories

- 6.4.3. Blood Banks

- 6.4.4. Research Institutes

- 6.4.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Blood Collection Robot Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Automated Blood Collection Robots

- 7.1.2. Semi-Automated Blood Collection Robots

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Artificial Intelligence and Machine Vision

- 7.2.2. Sensor Technology

- 7.2.3. Others

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Venipuncture

- 7.3.2. Fingerstick/Capillary Blood Collection

- 7.3.3. Arterial Blood Collection

- 7.4. Market Analysis, Insights and Forecast - by End User

- 7.4.1. Hospitals

- 7.4.2. Diagnostic Centers & Laboratories

- 7.4.3. Blood Banks

- 7.4.4. Research Institutes

- 7.4.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. South America Blood Collection Robot Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Automated Blood Collection Robots

- 8.1.2. Semi-Automated Blood Collection Robots

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Artificial Intelligence and Machine Vision

- 8.2.2. Sensor Technology

- 8.2.3. Others

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Venipuncture

- 8.3.2. Fingerstick/Capillary Blood Collection

- 8.3.3. Arterial Blood Collection

- 8.4. Market Analysis, Insights and Forecast - by End User

- 8.4.1. Hospitals

- 8.4.2. Diagnostic Centers & Laboratories

- 8.4.3. Blood Banks

- 8.4.4. Research Institutes

- 8.4.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Europe Blood Collection Robot Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Automated Blood Collection Robots

- 9.1.2. Semi-Automated Blood Collection Robots

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Artificial Intelligence and Machine Vision

- 9.2.2. Sensor Technology

- 9.2.3. Others

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Venipuncture

- 9.3.2. Fingerstick/Capillary Blood Collection

- 9.3.3. Arterial Blood Collection

- 9.4. Market Analysis, Insights and Forecast - by End User

- 9.4.1. Hospitals

- 9.4.2. Diagnostic Centers & Laboratories

- 9.4.3. Blood Banks

- 9.4.4. Research Institutes

- 9.4.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East & Africa Blood Collection Robot Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Automated Blood Collection Robots

- 10.1.2. Semi-Automated Blood Collection Robots

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. Artificial Intelligence and Machine Vision

- 10.2.2. Sensor Technology

- 10.2.3. Others

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Venipuncture

- 10.3.2. Fingerstick/Capillary Blood Collection

- 10.3.3. Arterial Blood Collection

- 10.4. Market Analysis, Insights and Forecast - by End User

- 10.4.1. Hospitals

- 10.4.2. Diagnostic Centers & Laboratories

- 10.4.3. Blood Banks

- 10.4.4. Research Institutes

- 10.4.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Asia Pacific Blood Collection Robot Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Automated Blood Collection Robots

- 11.1.2. Semi-Automated Blood Collection Robots

- 11.2. Market Analysis, Insights and Forecast - by Technology

- 11.2.1. Artificial Intelligence and Machine Vision

- 11.2.2. Sensor Technology

- 11.2.3. Others

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Venipuncture

- 11.3.2. Fingerstick/Capillary Blood Collection

- 11.3.3. Arterial Blood Collection

- 11.4. Market Analysis, Insights and Forecast - by End User

- 11.4.1. Hospitals

- 11.4.2. Diagnostic Centers & Laboratories

- 11.4.3. Blood Banks

- 11.4.4. Research Institutes

- 11.4.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Vitestro

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Veebot

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 BHealthCare

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Others

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.1 Vitestro

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Blood Collection Robot Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Blood Collection Robot Revenue (billion), by Product Type 2025 & 2033

- Figure 3: North America Blood Collection Robot Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Blood Collection Robot Revenue (billion), by Technology 2025 & 2033

- Figure 5: North America Blood Collection Robot Revenue Share (%), by Technology 2025 & 2033

- Figure 6: North America Blood Collection Robot Revenue (billion), by Application 2025 & 2033

- Figure 7: North America Blood Collection Robot Revenue Share (%), by Application 2025 & 2033

- Figure 8: North America Blood Collection Robot Revenue (billion), by End User 2025 & 2033

- Figure 9: North America Blood Collection Robot Revenue Share (%), by End User 2025 & 2033

- Figure 10: North America Blood Collection Robot Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Blood Collection Robot Revenue Share (%), by Country 2025 & 2033

- Figure 12: South America Blood Collection Robot Revenue (billion), by Product Type 2025 & 2033

- Figure 13: South America Blood Collection Robot Revenue Share (%), by Product Type 2025 & 2033

- Figure 14: South America Blood Collection Robot Revenue (billion), by Technology 2025 & 2033

- Figure 15: South America Blood Collection Robot Revenue Share (%), by Technology 2025 & 2033

- Figure 16: South America Blood Collection Robot Revenue (billion), by Application 2025 & 2033

- Figure 17: South America Blood Collection Robot Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Blood Collection Robot Revenue (billion), by End User 2025 & 2033

- Figure 19: South America Blood Collection Robot Revenue Share (%), by End User 2025 & 2033

- Figure 20: South America Blood Collection Robot Revenue (billion), by Country 2025 & 2033

- Figure 21: South America Blood Collection Robot Revenue Share (%), by Country 2025 & 2033

- Figure 22: Europe Blood Collection Robot Revenue (billion), by Product Type 2025 & 2033

- Figure 23: Europe Blood Collection Robot Revenue Share (%), by Product Type 2025 & 2033

- Figure 24: Europe Blood Collection Robot Revenue (billion), by Technology 2025 & 2033

- Figure 25: Europe Blood Collection Robot Revenue Share (%), by Technology 2025 & 2033

- Figure 26: Europe Blood Collection Robot Revenue (billion), by Application 2025 & 2033

- Figure 27: Europe Blood Collection Robot Revenue Share (%), by Application 2025 & 2033

- Figure 28: Europe Blood Collection Robot Revenue (billion), by End User 2025 & 2033

- Figure 29: Europe Blood Collection Robot Revenue Share (%), by End User 2025 & 2033

- Figure 30: Europe Blood Collection Robot Revenue (billion), by Country 2025 & 2033

- Figure 31: Europe Blood Collection Robot Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East & Africa Blood Collection Robot Revenue (billion), by Product Type 2025 & 2033

- Figure 33: Middle East & Africa Blood Collection Robot Revenue Share (%), by Product Type 2025 & 2033

- Figure 34: Middle East & Africa Blood Collection Robot Revenue (billion), by Technology 2025 & 2033

- Figure 35: Middle East & Africa Blood Collection Robot Revenue Share (%), by Technology 2025 & 2033

- Figure 36: Middle East & Africa Blood Collection Robot Revenue (billion), by Application 2025 & 2033

- Figure 37: Middle East & Africa Blood Collection Robot Revenue Share (%), by Application 2025 & 2033

- Figure 38: Middle East & Africa Blood Collection Robot Revenue (billion), by End User 2025 & 2033

- Figure 39: Middle East & Africa Blood Collection Robot Revenue Share (%), by End User 2025 & 2033

- Figure 40: Middle East & Africa Blood Collection Robot Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East & Africa Blood Collection Robot Revenue Share (%), by Country 2025 & 2033

- Figure 42: Asia Pacific Blood Collection Robot Revenue (billion), by Product Type 2025 & 2033

- Figure 43: Asia Pacific Blood Collection Robot Revenue Share (%), by Product Type 2025 & 2033

- Figure 44: Asia Pacific Blood Collection Robot Revenue (billion), by Technology 2025 & 2033

- Figure 45: Asia Pacific Blood Collection Robot Revenue Share (%), by Technology 2025 & 2033

- Figure 46: Asia Pacific Blood Collection Robot Revenue (billion), by Application 2025 & 2033

- Figure 47: Asia Pacific Blood Collection Robot Revenue Share (%), by Application 2025 & 2033

- Figure 48: Asia Pacific Blood Collection Robot Revenue (billion), by End User 2025 & 2033

- Figure 49: Asia Pacific Blood Collection Robot Revenue Share (%), by End User 2025 & 2033

- Figure 50: Asia Pacific Blood Collection Robot Revenue (billion), by Country 2025 & 2033

- Figure 51: Asia Pacific Blood Collection Robot Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Blood Collection Robot Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Global Blood Collection Robot Revenue billion Forecast, by Technology 2020 & 2033

- Table 3: Global Blood Collection Robot Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Global Blood Collection Robot Revenue billion Forecast, by End User 2020 & 2033

- Table 5: Global Blood Collection Robot Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Blood Collection Robot Revenue billion Forecast, by Product Type 2020 & 2033

- Table 7: Global Blood Collection Robot Revenue billion Forecast, by Technology 2020 & 2033

- Table 8: Global Blood Collection Robot Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Global Blood Collection Robot Revenue billion Forecast, by End User 2020 & 2033

- Table 10: Global Blood Collection Robot Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Blood Collection Robot Revenue billion Forecast, by Product Type 2020 & 2033

- Table 15: Global Blood Collection Robot Revenue billion Forecast, by Technology 2020 & 2033

- Table 16: Global Blood Collection Robot Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Blood Collection Robot Revenue billion Forecast, by End User 2020 & 2033

- Table 18: Global Blood Collection Robot Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Brazil Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Argentina Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of South America Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Blood Collection Robot Revenue billion Forecast, by Product Type 2020 & 2033

- Table 23: Global Blood Collection Robot Revenue billion Forecast, by Technology 2020 & 2033

- Table 24: Global Blood Collection Robot Revenue billion Forecast, by Application 2020 & 2033

- Table 25: Global Blood Collection Robot Revenue billion Forecast, by End User 2020 & 2033

- Table 26: Global Blood Collection Robot Revenue billion Forecast, by Country 2020 & 2033

- Table 27: United Kingdom Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Germany Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: France Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Italy Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Spain Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Russia Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Benelux Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Nordics Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Blood Collection Robot Revenue billion Forecast, by Product Type 2020 & 2033

- Table 37: Global Blood Collection Robot Revenue billion Forecast, by Technology 2020 & 2033

- Table 38: Global Blood Collection Robot Revenue billion Forecast, by Application 2020 & 2033

- Table 39: Global Blood Collection Robot Revenue billion Forecast, by End User 2020 & 2033

- Table 40: Global Blood Collection Robot Revenue billion Forecast, by Country 2020 & 2033

- Table 41: Turkey Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Israel Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: GCC Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: North Africa Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: South Africa Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East & Africa Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Global Blood Collection Robot Revenue billion Forecast, by Product Type 2020 & 2033

- Table 48: Global Blood Collection Robot Revenue billion Forecast, by Technology 2020 & 2033

- Table 49: Global Blood Collection Robot Revenue billion Forecast, by Application 2020 & 2033

- Table 50: Global Blood Collection Robot Revenue billion Forecast, by End User 2020 & 2033

- Table 51: Global Blood Collection Robot Revenue billion Forecast, by Country 2020 & 2033

- Table 52: China Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 53: India Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 55: South Korea Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: ASEAN Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 57: Oceania Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Rest of Asia Pacific Blood Collection Robot Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Blood Collection Robot?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Blood Collection Robot?

Key companies in the market include Vitestro, Veebot, BHealthCare, Others.

3. What are the main segments of the Blood Collection Robot?

The market segments include Product Type, Technology, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Blood Collection Robot," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Blood Collection Robot report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Blood Collection Robot?

To stay informed about further developments, trends, and reports in the Blood Collection Robot, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence