Key Insights

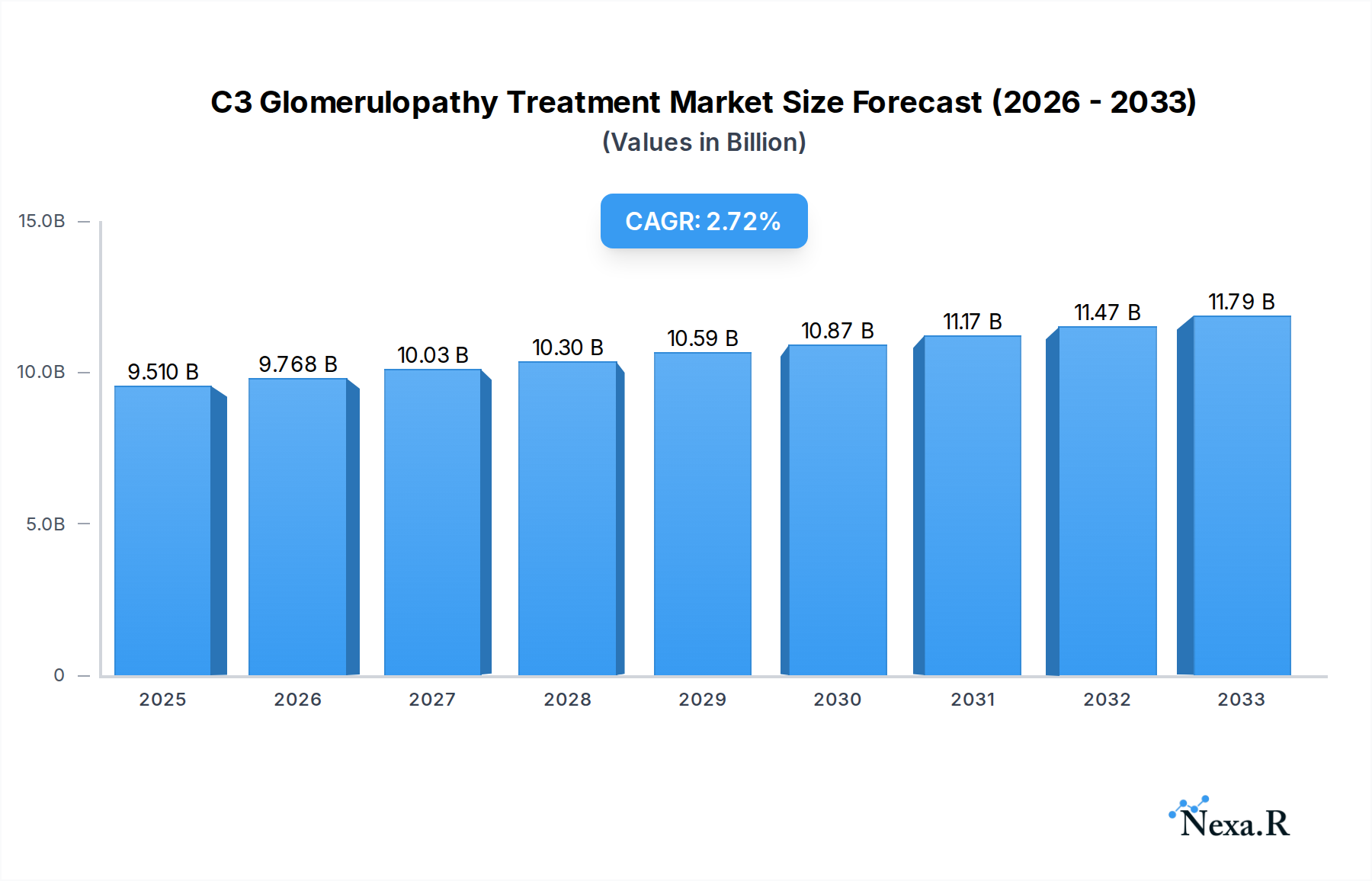

The global C3 Glomerulopathy (C3G) treatment market is projected to reach an estimated $9.51 billion by 2025, demonstrating a steady compound annual growth rate (CAGR) of 2.75% from 2019 to 2033. This growth is underpinned by increasing awareness of rare kidney diseases, advancements in diagnostic technologies enabling earlier and more accurate C3G detection, and a growing pipeline of targeted therapies. While previously underserved, the market is now witnessing significant investment in research and development, driven by a better understanding of the underlying complement system dysregulation in C3G. The rising prevalence of autoimmune disorders, which often have a link to complement-mediated kidney damage, also contributes to this market expansion. Key applications are expected to be dominated by hospital pharmacies due to the complex nature of C3G management and the need for specialized care, followed by clinics and other healthcare settings. The parenteral segment is likely to hold a significant share due to the administration route of many advanced therapeutic agents.

C3 Glomerulopathy Treatment Market Size (In Billion)

The market's trajectory is further shaped by evolving treatment paradigms that move beyond symptomatic management to address the root causes of C3G. Emerging trends include the development of complement inhibitors specifically targeting the alternative pathway, personalized medicine approaches based on genetic profiling, and increased collaborative efforts between pharmaceutical companies, research institutions, and patient advocacy groups to accelerate drug discovery and accessibility. However, challenges such as the rarity of the disease, leading to difficulties in clinical trial recruitment, and the high cost associated with novel therapies may present some restraints. Despite these hurdles, the strong emphasis on improving patient outcomes and the increasing demand for effective C3G treatments are expected to propel the market forward. Geographically, North America and Europe are anticipated to lead the market due to established healthcare infrastructures and higher healthcare spending, while the Asia Pacific region is poised for substantial growth driven by an expanding patient base and improving healthcare access.

C3 Glomerulopathy Treatment Company Market Share

Comprehensive Market Analysis: C3 Glomerulopathy Treatment Market Forecast & Opportunities (2019–2033)

This report delivers an in-depth analysis of the global C3 Glomerulopathy treatment market, a critical and evolving sector within rare kidney disease therapeutics. Examining the period from 2019 to 2033, with a base and estimated year of 2025, this comprehensive study provides actionable insights for stakeholders seeking to understand market dynamics, growth drivers, and competitive landscapes. We delve into the parent and child market segments, offering a granular view of opportunities within hospital pharmacies, clinics, and other healthcare settings, alongside an analysis of oral, parenteral, and other treatment modalities. The report leverages advanced analytics and industry expert consensus to present a robust forecast, vital for strategic planning and investment decisions in this high-potential market.

C3 Glomerulopathy Treatment Market Dynamics & Structure

The C3 glomerulopathy treatment market is characterized by a dynamic interplay of technological innovation, evolving regulatory frameworks, and increasing patient awareness. Market concentration is currently moderate, with a few key players holding significant sway, but the potential for disruption by novel therapies remains high. Technological innovation is primarily driven by advancements in understanding the complement cascade, leading to the development of targeted therapies. Regulatory bodies are increasingly streamlining approvals for orphan drugs, though stringent efficacy and safety requirements remain a barrier. Competitive product substitutes are limited but emerging, with gene therapies and personalized medicine showing promise. End-user demographics are primarily concentrated in developed nations with advanced healthcare infrastructure, though access in emerging markets presents a significant opportunity. Mergers and acquisitions (M&A) are a notable trend, as larger pharmaceutical companies seek to acquire promising pipeline assets and expand their rare disease portfolios. For instance, a significant volume of glomerulonephritis treatment market deals have been observed, indicating investor confidence in related therapeutic areas. The market faces innovation barriers such as the complexity of C3 glomerulopathy pathogenesis, the high cost of research and development for rare diseases, and the challenges in conducting large-scale clinical trials.

- Market Concentration: Moderate, with key players like Alexion Pharmaceuticals and Omeros Corporation at the forefront.

- Technological Innovation Drivers: Advances in complement inhibition, genetic sequencing, and drug delivery systems.

- Regulatory Frameworks: Orphan drug designations, accelerated approval pathways, and post-market surveillance requirements.

- Competitive Product Substitutes: Emerging gene therapies, complement pathway modulators, and supportive care advancements.

- End-User Demographics: Predominantly adult patients with C3 glomerulopathy, with a focus on regions with high prevalence and diagnostic capabilities.

- M&A Trends: Increasing acquisition of early-stage biotechnology companies and licensing agreements for promising drug candidates.

C3 Glomerulopathy Treatment Growth Trends & Insights

The C3 glomerulopathy treatment market is poised for substantial growth, driven by a confluence of factors including a rising prevalence of rare kidney diseases, advancements in diagnostic capabilities, and the development of novel therapeutic agents. The market size is projected to expand significantly over the forecast period, with a compound annual growth rate (CAGR) estimated to be in the high single digits. Adoption rates for advanced therapies are expected to accelerate as clinical evidence solidifies and reimbursement policies become more favorable. Technological disruptions, such as the refinement of complement inhibitors and the exploration of gene editing technologies, are set to redefine treatment paradigms. Consumer behavior shifts, including increased patient advocacy and a demand for personalized treatment approaches, will also play a crucial role in shaping market trajectories. The penetration of targeted therapies, initially limited by high costs and awareness, is anticipated to increase as treatment benefits become more apparent and accessibility improves across the glomerulonephritis treatment market. The unmet medical need in C3 glomerulopathy remains a significant driver, motivating sustained investment in research and development. Furthermore, the growing understanding of the underlying complement-mediated pathways offers fertile ground for innovation, leading to the development of more effective and potentially curative treatments. Patient registries and real-world data collection are also becoming instrumental in understanding disease progression and treatment outcomes, further fueling market expansion.

The market's growth is further underpinned by a strong pipeline of investigational drugs targeting various arms of the complement system. Companies are investing heavily in understanding the precise mechanisms driving C3 glomerulopathy, leading to more precise therapeutic interventions. The increasing sophistication of diagnostic tools allows for earlier and more accurate identification of patients, thereby expanding the addressable market for treatments. Economic factors, such as the increasing healthcare expenditure in developed economies and the growing disposable income in emerging markets, contribute to the overall market expansion. The competitive landscape, while still consolidating, is seeing new entrants with innovative approaches, fostering a dynamic environment for innovation and market growth. The increasing focus on rare diseases by global health organizations and governments also provides a favorable backdrop for the development and commercialization of C3 glomerulopathy treatments. The anticipated market size for C3 glomerulopathy treatments is expected to reach substantial figures in the coming years, reflecting the significant unmet need and the potential of emerging therapies.

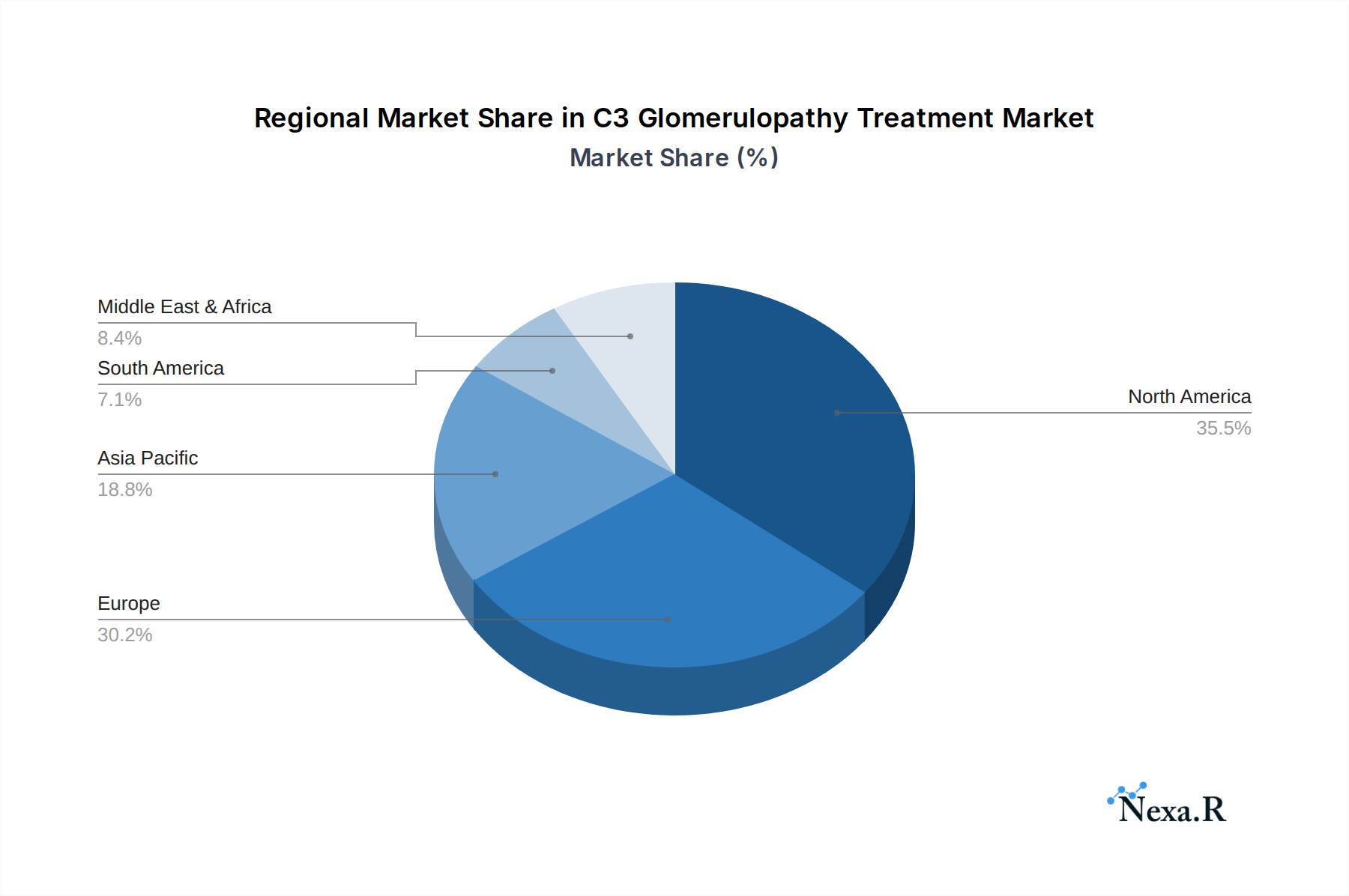

Dominant Regions, Countries, or Segments in C3 Glomerulopathy Treatment

North America currently dominates the C3 glomerulopathy treatment market, driven by a combination of robust healthcare infrastructure, high per capita healthcare spending, and a strong presence of leading pharmaceutical companies and research institutions. The United States, in particular, is a key growth engine, characterized by advanced diagnostic capabilities, a favorable regulatory environment for orphan drugs, and a high prevalence of rare kidney diseases. Economic policies that incentivize the development of treatments for underserved populations, coupled with substantial investment in research and development, further solidify North America's leading position. The established reimbursement frameworks within the region facilitate the adoption of high-cost, specialized therapies.

Within the C3 glomerulopathy treatment market, the Hospital Pharmacy application segment is projected to be the most dominant. This is attributed to the complexity of C3 glomerulopathy requiring specialized medical supervision, in-hospital administration of certain parenteral therapies, and comprehensive patient monitoring protocols typically managed within hospital settings. The Parenteral type segment also holds significant sway, as many of the most promising and currently available C3 glomerulopathy treatments are administered intravenously due to their targeted nature and the need for precise dosing.

Key drivers for dominance in this segment include:

- High Prevalence of Rare Kidney Diseases: North America, particularly the US, has a higher reported incidence of rare kidney disorders.

- Advanced Healthcare Infrastructure: Well-established hospital networks and specialized nephrology centers.

- Favorable Regulatory Environment: Accelerated approval pathways and incentives for orphan drug development.

- High Healthcare Expenditure: Significant per capita spending on healthcare ensures access to advanced treatments.

- Strong R&D Ecosystem: Presence of leading pharmaceutical companies and research institutions driving innovation.

The market share for Hospital Pharmacy applications is estimated to be substantial, reflecting the critical role of hospital settings in managing complex rare diseases. Similarly, the Parenteral administration route is expected to capture a significant portion of the market share due to the nature of current therapeutic interventions. While other regions like Europe are showing strong growth potential due to increasing awareness and improving healthcare systems, North America's established infrastructure and investment capacity currently position it as the dominant force in the C3 glomerulopathy treatment market. The child market of C3 Glomerulopathy treatments within the broader rare kidney disease market is expanding rapidly, with specialized treatments gaining traction.

C3 Glomerulopathy Treatment Product Landscape

The C3 glomerulopathy treatment product landscape is characterized by innovative therapies targeting the dysregulated complement cascade, the underlying driver of this rare kidney disease. Current and emerging products focus on inhibiting specific complement pathways, such as the alternative pathway, to mitigate kidney damage. Unique selling propositions of these advanced treatments lie in their targeted action, aiming to reduce proteinuria, slow disease progression, and improve renal function with potentially fewer off-target effects compared to broader immunosuppressants. Technological advancements are enabling the development of more potent and selective complement inhibitors, including monoclonal antibodies and small molecules. Performance metrics being closely monitored include reductions in proteinuria, stabilization or improvement of glomerular filtration rate (GFR), and a decrease in the need for kidney transplantation or dialysis.

Key Drivers, Barriers & Challenges in C3 Glomerulopathy Treatment

The C3 glomerulopathy treatment market is propelled by significant drivers, including the pressing unmet medical need for effective therapies, groundbreaking advancements in understanding complement-mediated kidney diseases, and the robust pipeline of targeted drugs. Technological innovations in complement inhibition, coupled with supportive policies for rare disease drug development, are also key accelerators.

- Technological: Targeted therapies addressing the complement cascade.

- Economic: Increasing healthcare expenditure on rare diseases.

- Policy-Driven: Orphan drug incentives and accelerated regulatory pathways.

However, the market faces considerable barriers and challenges. The rarity of C3 glomerulopathy leads to difficulties in conducting large-scale clinical trials, impacting the generation of definitive efficacy data. High treatment costs present a significant access barrier for patients and healthcare systems, and reimbursement negotiations can be protracted. Supply chain complexities for specialized biologics and the need for specialized diagnostic and treatment centers also pose hurdles.

- Supply Chain Issues: Manufacturing complexities and cold chain requirements for biologics.

- Regulatory Hurdles: Stringent efficacy and safety data requirements for novel therapies.

- Competitive Pressures: Emergence of alternative treatment modalities and off-label use concerns.

- Cost and Reimbursement: High prices of targeted therapies and challenges in securing broad insurance coverage.

Emerging Opportunities in C3 Glomerulopathy Treatment

Emerging opportunities in the C3 glomerulopathy treatment market lie in the development of next-generation complement inhibitors with improved safety profiles and enhanced efficacy. Personalized medicine approaches, leveraging genetic profiling to identify specific complement pathway dysregulation in individual patients, represent a significant untapped market. Furthermore, expanding access to diagnostics and treatments in emerging economies, where rare kidney diseases are often underdiagnosed, presents substantial growth potential. The exploration of combination therapies and the potential for regenerative medicine also offer promising avenues for future market expansion and improved patient outcomes in the broader glomerulonephritis treatment market.

Growth Accelerators in the C3 Glomerulopathy Treatment Industry

Growth in the C3 glomerulopathy treatment industry is significantly accelerated by breakthroughs in complement biology, leading to the identification of novel therapeutic targets within the complement cascade. Strategic partnerships between academic research institutions and pharmaceutical companies are fostering rapid translation of scientific discoveries into clinical development. Market expansion strategies focused on improving diagnostic rates and patient identification in under-served regions will further fuel long-term growth. The increasing availability of real-world evidence demonstrating the long-term benefits of approved therapies is also a critical catalyst, bolstering confidence among payers and clinicians.

Key Players Shaping the C3 Glomerulopathy Treatment Market

- F. Hoffmann-La Roche Ltd.

- Mylan N.V.

- Teva Pharmaceutical Industries Ltd.

- Sanofi

- Pfizer Inc.

- GSK plc

- Novartis AG

- Alexion Pharmaceuticals

- Omeros Corporation

- ChemoCentryx

Notable Milestones in C3 Glomerulopathy Treatment Sector

- 2020: Approval of the first targeted therapy for C3 glomerulopathy, marking a significant shift in treatment paradigms.

- 2021: Publication of pivotal clinical trial data demonstrating significant reductions in proteinuria and stabilization of kidney function.

- 2022: Initiation of phase III clinical trials for novel oral complement inhibitors, promising improved patient convenience.

- 2023: Expansion of diagnostic testing capabilities for complement pathway dysregulation, leading to earlier patient identification.

- 2024: Formation of a key strategic alliance between a major pharmaceutical company and a leading biotechnology firm to accelerate development of complement inhibitors.

In-Depth C3 Glomerulopathy Treatment Market Outlook

The C3 glomerulopathy treatment market outlook is exceptionally promising, driven by sustained innovation in complement inhibition and a growing understanding of disease pathogenesis. Growth accelerators, including advancements in personalized medicine and the expansion of treatment access to emerging markets, will continue to shape the future landscape. Strategic opportunities abound for companies focusing on developing novel therapeutic modalities, improving diagnostic accuracy, and forging collaborations to enhance patient care and research initiatives within the rare kidney disease sector. The anticipated market expansion underscores the critical need for effective interventions and the significant potential for positive patient outcomes.

C3 Glomerulopathy Treatment Segmentation

-

1. Application

- 1.1. Hospital Pharmacy

- 1.2. Clinic

- 1.3. Others

-

2. Types

- 2.1. Oral

- 2.2. Parenteral

- 2.3. Others

C3 Glomerulopathy Treatment Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

C3 Glomerulopathy Treatment Regional Market Share

Geographic Coverage of C3 Glomerulopathy Treatment

C3 Glomerulopathy Treatment REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.75% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital Pharmacy

- 5.1.2. Clinic

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Oral

- 5.2.2. Parenteral

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global C3 Glomerulopathy Treatment Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital Pharmacy

- 6.1.2. Clinic

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Oral

- 6.2.2. Parenteral

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America C3 Glomerulopathy Treatment Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital Pharmacy

- 7.1.2. Clinic

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Oral

- 7.2.2. Parenteral

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America C3 Glomerulopathy Treatment Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital Pharmacy

- 8.1.2. Clinic

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Oral

- 8.2.2. Parenteral

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe C3 Glomerulopathy Treatment Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital Pharmacy

- 9.1.2. Clinic

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Oral

- 9.2.2. Parenteral

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa C3 Glomerulopathy Treatment Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital Pharmacy

- 10.1.2. Clinic

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Oral

- 10.2.2. Parenteral

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific C3 Glomerulopathy Treatment Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospital Pharmacy

- 11.1.2. Clinic

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Oral

- 11.2.2. Parenteral

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 F. Hoffmann-La Roche Ltd.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Mylan N.V.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Teva Pharmaceutical Industries Ltd.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Sanofi

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Pfizer Inc.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 GSK plc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Novartis AG

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Alexion Pharmaceuticals

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Omeros Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 ChemoCentryx

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 F. Hoffmann-La Roche Ltd.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global C3 Glomerulopathy Treatment Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America C3 Glomerulopathy Treatment Revenue (billion), by Application 2025 & 2033

- Figure 3: North America C3 Glomerulopathy Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America C3 Glomerulopathy Treatment Revenue (billion), by Types 2025 & 2033

- Figure 5: North America C3 Glomerulopathy Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America C3 Glomerulopathy Treatment Revenue (billion), by Country 2025 & 2033

- Figure 7: North America C3 Glomerulopathy Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America C3 Glomerulopathy Treatment Revenue (billion), by Application 2025 & 2033

- Figure 9: South America C3 Glomerulopathy Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America C3 Glomerulopathy Treatment Revenue (billion), by Types 2025 & 2033

- Figure 11: South America C3 Glomerulopathy Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America C3 Glomerulopathy Treatment Revenue (billion), by Country 2025 & 2033

- Figure 13: South America C3 Glomerulopathy Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe C3 Glomerulopathy Treatment Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe C3 Glomerulopathy Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe C3 Glomerulopathy Treatment Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe C3 Glomerulopathy Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe C3 Glomerulopathy Treatment Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe C3 Glomerulopathy Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa C3 Glomerulopathy Treatment Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa C3 Glomerulopathy Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa C3 Glomerulopathy Treatment Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa C3 Glomerulopathy Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa C3 Glomerulopathy Treatment Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa C3 Glomerulopathy Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific C3 Glomerulopathy Treatment Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific C3 Glomerulopathy Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific C3 Glomerulopathy Treatment Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific C3 Glomerulopathy Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific C3 Glomerulopathy Treatment Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific C3 Glomerulopathy Treatment Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global C3 Glomerulopathy Treatment Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific C3 Glomerulopathy Treatment Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the C3 Glomerulopathy Treatment?

The projected CAGR is approximately 2.75%.

2. Which companies are prominent players in the C3 Glomerulopathy Treatment?

Key companies in the market include F. Hoffmann-La Roche Ltd., Mylan N.V., Teva Pharmaceutical Industries Ltd., Sanofi, Pfizer Inc., GSK plc, Novartis AG, Alexion Pharmaceuticals, Omeros Corporation, ChemoCentryx.

3. What are the main segments of the C3 Glomerulopathy Treatment?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.51 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "C3 Glomerulopathy Treatment," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the C3 Glomerulopathy Treatment report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the C3 Glomerulopathy Treatment?

To stay informed about further developments, trends, and reports in the C3 Glomerulopathy Treatment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence