Key Insights

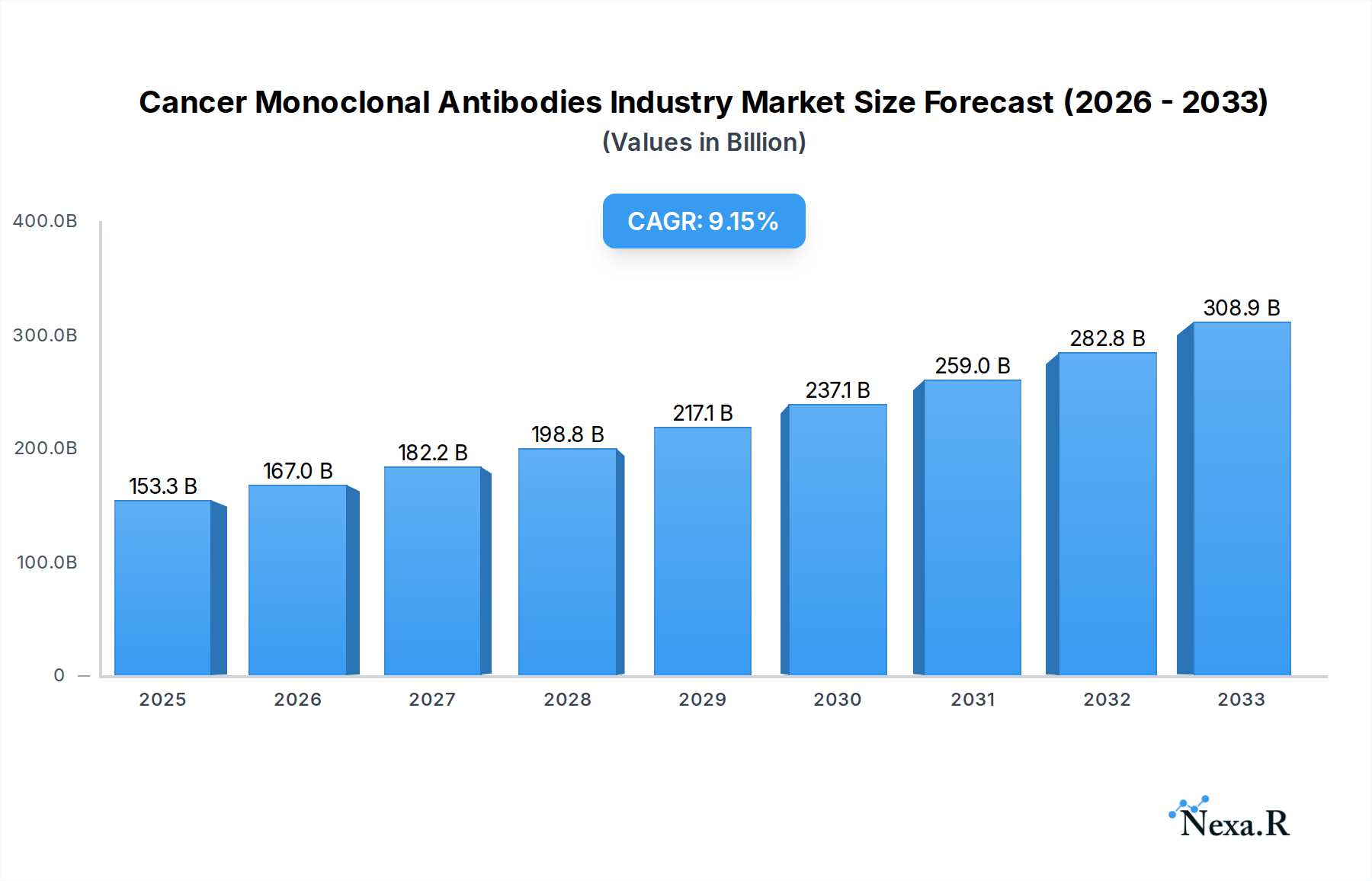

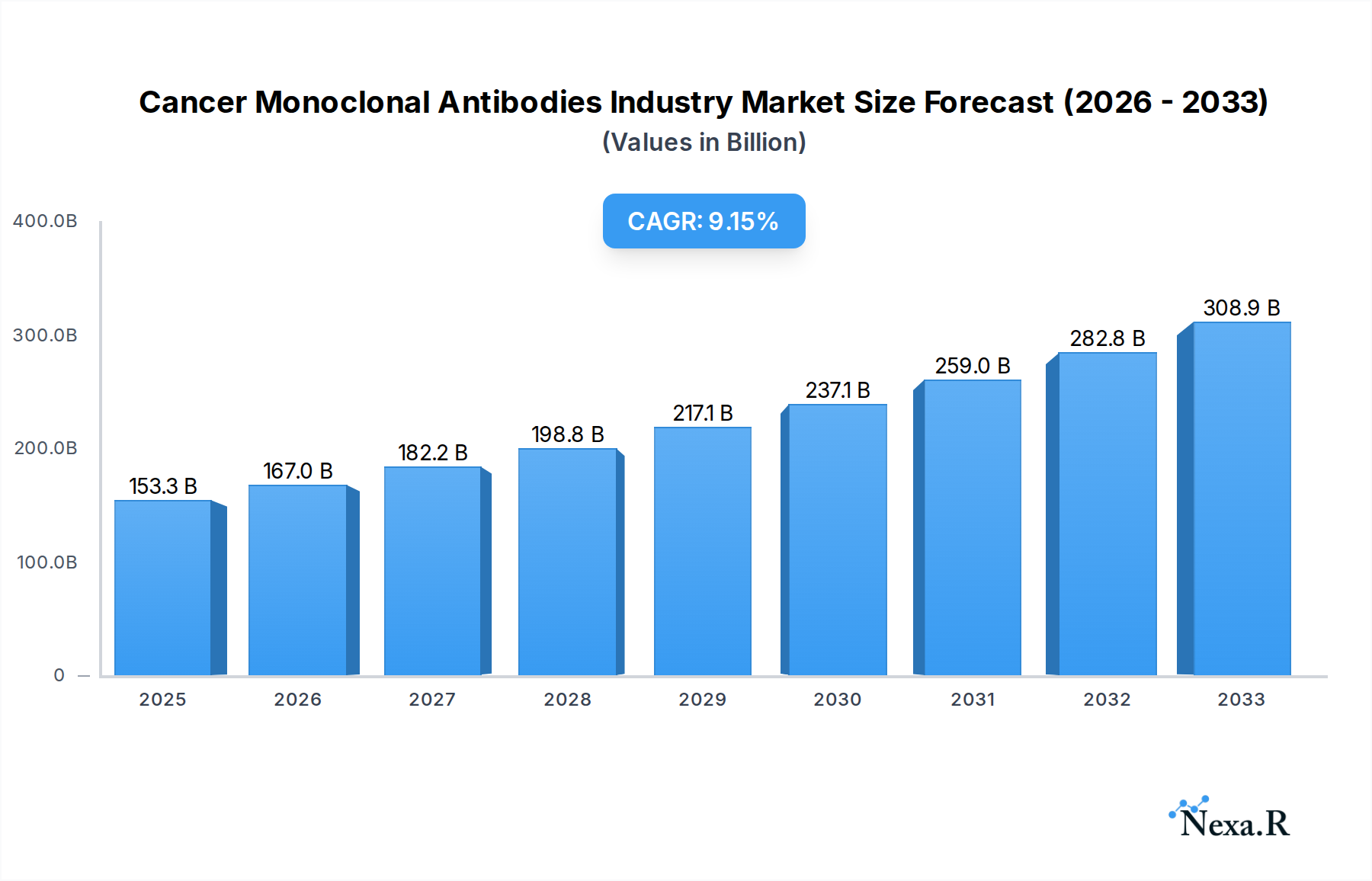

The Cancer Monoclonal Antibodies Market is experiencing robust growth, projected to reach USD 153.27 billion in 2025 and expand at a compound annual growth rate (CAGR) of 9.02% through 2033. This significant expansion is propelled by several key drivers, including the increasing incidence of various cancers globally, advancements in targeted therapy research, and a growing pipeline of novel monoclonal antibody drugs. The personalized nature of these therapies, offering improved efficacy and reduced side effects compared to traditional chemotherapy, is a major factor driving adoption across a wide range of cancer types, from breast and blood cancers to liver, brain, and colorectal cancers. Furthermore, the continuous development of innovative antibody formats and the expansion of their therapeutic applications are contributing to sustained market momentum.

Cancer Monoclonal Antibodies Industry Market Size (In Billion)

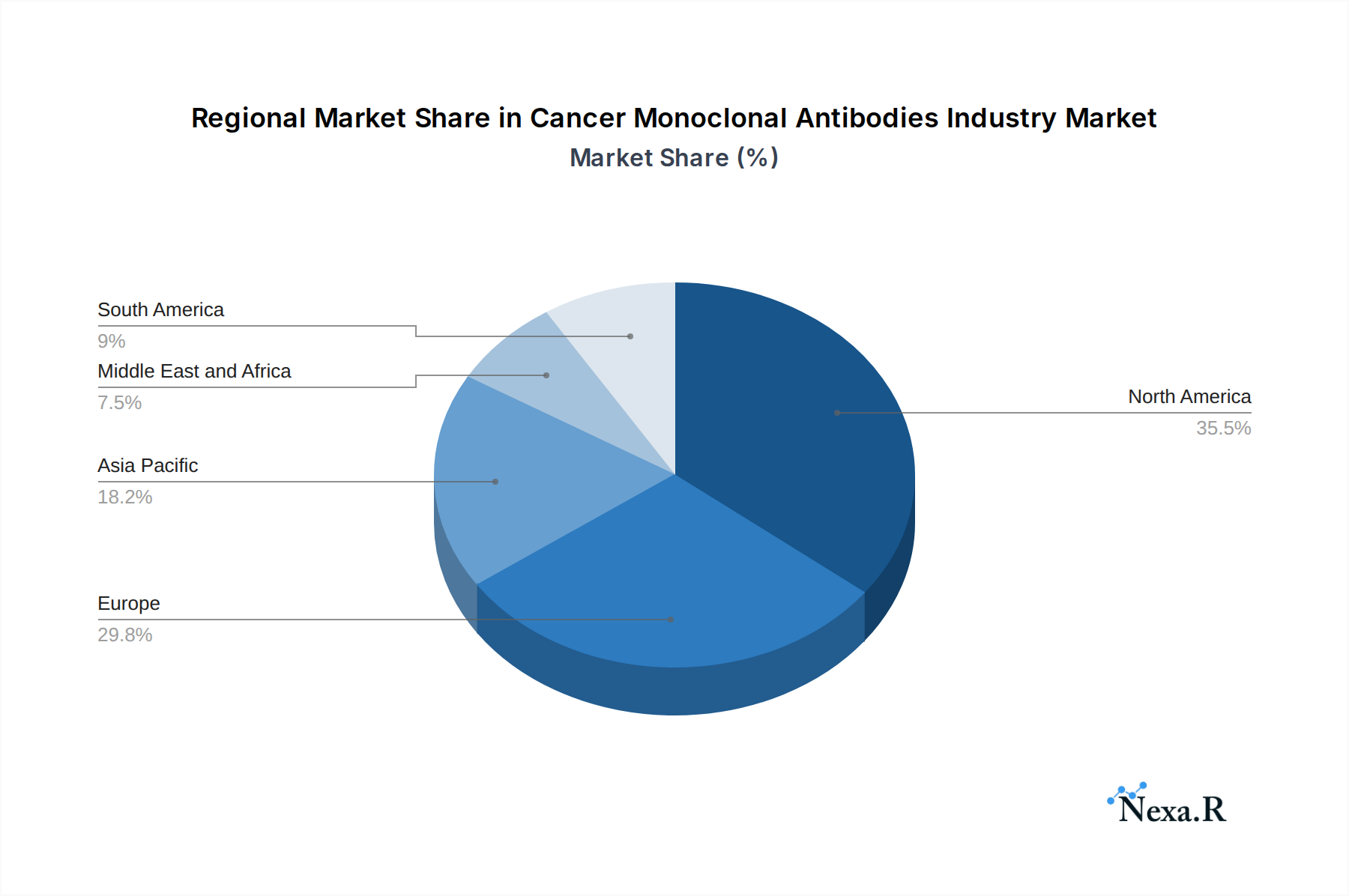

The market is segmented into various types of monoclonal antibodies, including Murine, Chimeric, and Humanized antibodies, with a significant focus on established therapies such as Bevacizumab (Avastin), Rituximab (Rituxan), and Trastuzumab (Herceptin), alongside emerging treatments. Leading pharmaceutical companies like Genmab AS, Novartis AG, and F Hoffmann-La Roche Ltd are heavily invested in research and development, fueling innovation and market competition. Geographically, North America and Europe currently dominate the market due to advanced healthcare infrastructure and high cancer prevalence. However, the Asia Pacific region is anticipated to witness substantial growth, driven by increasing healthcare expenditure, a growing patient pool, and the expanding accessibility of advanced cancer treatments. Addressing challenges such as high treatment costs and regulatory hurdles will be crucial for unlocking the full potential of this dynamic market.

Cancer Monoclonal Antibodies Industry Company Market Share

Here's the SEO-optimized report description for the Cancer Monoclonal Antibodies Industry:

Cancer Monoclonal Antibodies Industry Market Dynamics & Structure

The global Cancer Monoclonal Antibodies market is characterized by a moderate concentration of key players, with innovation in therapeutic development and stringent regulatory approvals acting as significant drivers. Technological advancements in antibody engineering, particularly in areas like bispecific antibodies and antibody-drug conjugates (ADCs), are continuously pushing the boundaries of treatment efficacy and patient outcomes. The market's growth is underpinned by increasing global cancer incidence, a growing pipeline of novel antibody therapies, and supportive government initiatives for research and development. However, high development costs, complex manufacturing processes, and the emergence of competitive biosimilars present notable barriers. End-user demographics, primarily aging populations and rising cancer awareness, contribute to sustained demand. Mergers, acquisitions, and strategic partnerships are frequently observed as companies seek to expand their portfolios, acquire promising technologies, and gain market share. The interplay between these factors shapes a dynamic and evolving industry landscape.

- Market Concentration: Dominated by a mix of large pharmaceutical giants and specialized biopharmaceutical companies.

- Technological Innovation: Focus on next-generation antibodies (e.g., bispecific, ADCs) for enhanced efficacy and reduced side effects.

- Regulatory Frameworks: FDA, EMA, and NMPA approvals are critical gatekeepers, influencing market entry and product lifecycle.

- Competitive Product Substitutes: Advancements in other cancer treatment modalities like immunotherapy (checkpoint inhibitors) and targeted therapies pose a competitive threat.

- End-User Demographics: Increasing global cancer burden and aging populations drive demand.

- M&A Trends: Frequent consolidation and strategic alliances to leverage R&D pipelines and market access.

Cancer Monoclonal Antibodies Industry Growth Trends & Insights

The Cancer Monoclonal Antibodies market is poised for substantial expansion, driven by an escalating global cancer burden and remarkable advancements in therapeutic modalities. The market size is projected to witness robust growth from an estimated $50.1 billion in 2025 to $95.8 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 8.2% during the forecast period. This growth is fueled by an increasing number of cancer diagnoses worldwide, coupled with a higher adoption rate of targeted therapies, including monoclonal antibodies, due to their improved efficacy and reduced side effects compared to traditional chemotherapy.

Technological disruptions are continuously reshaping the landscape. The development of novel antibody formats, such as bispecific antibodies and antibody-drug conjugates (ADCs), is expanding the therapeutic arsenal and opening new avenues for treating previously intractable cancers. These innovations allow for more precise targeting of cancer cells, minimizing damage to healthy tissues and thereby enhancing patient tolerance and treatment outcomes. Furthermore, advancements in genetic sequencing and biomarker identification are enabling more personalized treatment approaches, where monoclonal antibodies are tailored to specific patient profiles and tumor mutations.

Consumer behavior shifts, influenced by increased awareness of advanced treatment options and a greater emphasis on personalized medicine, are also playing a crucial role. Patients and healthcare providers are increasingly opting for targeted therapies that offer better quality of life and potentially higher survival rates. The growing pipeline of monoclonal antibodies in various stages of clinical trials, addressing a wide spectrum of cancers, further solidifies the positive market outlook. The base year of 2025 marks a significant point, with an estimated market size of $50.1 billion, setting the stage for this impressive trajectory through 2033. The historical period from 2019 to 2024 has laid the foundation for this accelerated growth, with consistent progress in R&D and regulatory approvals.

Dominant Regions, Countries, or Segments in Cancer Monoclonal Antibodies Industry

North America currently stands as the dominant region in the Cancer Monoclonal Antibodies industry, driven by a confluence of factors that foster innovation, market access, and high adoption rates of advanced therapies. The region's robust healthcare infrastructure, significant investment in biomedical research and development, and a high prevalence of cancer cases contribute to its leading position. The United States, in particular, accounts for a substantial share of the global market, owing to the presence of leading pharmaceutical and biotechnology companies, a well-established regulatory framework for drug approvals (e.g., FDA), and a strong emphasis on personalized medicine. The substantial healthcare expenditure in North America allows for wider accessibility and reimbursement of expensive monoclonal antibody treatments, further accelerating market penetration.

Within the Types of Monoclonal Antibody, Humanized Antibodies represent a pivotal segment due to their reduced immunogenicity and enhanced therapeutic efficacy, making them a preferred choice for a wide range of cancer indications. In terms of Monoclonal Antibody Therapies, Bevacizumab (Avastin) and Rituximab (Rituxan) have historically held significant market share owing to their established efficacy in treating various cancers like colorectal, lung, and blood cancers. However, newer entrants and therapies targeting specific mutations are rapidly gaining traction.

The Application segment of Breast Cancer and Blood Cancer are major revenue generators, reflecting the high incidence of these diseases and the availability of numerous targeted monoclonal antibody treatments. The significant R&D efforts focused on these cancers, coupled with successful clinical trial outcomes, have led to a strong market presence. For instance, the approval of CARVYKTI for relapsed or refractory multiple myeloma underscores the immense potential within blood cancer therapies. Furthermore, ongoing research into treating liver cancer and brain cancer with monoclonal antibodies, though currently smaller segments, presents considerable growth potential. Economic policies supporting biopharmaceutical innovation, favorable reimbursement landscapes, and the presence of key opinion leaders championing these therapies are critical drivers of dominance in these regions and segments.

Cancer Monoclonal Antibodies Industry Product Landscape

The Cancer Monoclonal Antibodies industry is defined by a dynamic product landscape characterized by continuous innovation and targeted therapeutic applications. Leading products like Bevacizumab (Avastin), Rituximab (Rituxan), and Trastuzumab (Herceptin) have set benchmarks in treating various cancers, including colorectal, blood, and breast cancers, respectively. Recent advancements have seen the emergence of novel antibody formats, such as bispecific antibodies and antibody-drug conjugates (ADCs), offering enhanced potency and precision in targeting cancer cells. The development of CARVYKTI, a CAR T-cell therapy utilizing monoclonal antibody technology, signifies a paradigm shift in treating relapsed or refractory multiple myeloma. These products distinguish themselves through their specific mechanisms of action, target antigens, and improved safety profiles, addressing unmet medical needs and expanding treatment options for patients globally.

Key Drivers, Barriers & Challenges in Cancer Monoclonal Antibodies Industry

Key Drivers:

- Rising Cancer Incidence: Increasing global prevalence of various cancers directly fuels demand for effective treatments.

- Technological Advancements: Innovations in antibody engineering, bispecific antibodies, and ADCs are expanding therapeutic possibilities.

- Biomarker Discovery & Personalized Medicine: Tailoring treatments to individual patient profiles enhances efficacy and adoption.

- Supportive Regulatory Environment: Favorable regulatory pathways and incentives for R&D in oncology.

- Growing R&D Pipeline: A robust pipeline of novel monoclonal antibodies in clinical development promises future growth.

Barriers & Challenges:

- High Development & Manufacturing Costs: The intricate process of developing and manufacturing monoclonal antibodies is exceptionally expensive.

- Stringent Regulatory Approvals: Navigating complex and lengthy regulatory approval processes can delay market entry.

- Competition from Biosimilars: The advent of biosimilars can lead to pricing pressures and reduced market share for innovator products.

- Supply Chain Complexities: Ensuring consistent and secure supply of these complex biologics globally.

- Limited Efficacy in Some Cancers: Despite advancements, some cancer types remain challenging to treat effectively with current monoclonal antibodies.

- Side Effects and Immunogenicity: While generally better tolerated than chemotherapy, side effects and the potential for immune reactions remain a concern.

Emerging Opportunities in Cancer Monoclonal Antibodies Industry

Emerging opportunities within the Cancer Monoclonal Antibodies industry lie in the untapped potential of rare and underserved cancers, where specific monoclonal antibody targets can offer significant therapeutic benefits. The growing emphasis on combination therapies, integrating monoclonal antibodies with other immunotherapies or targeted agents, presents a fertile ground for innovation and enhanced treatment outcomes. Furthermore, the expansion of monoclonal antibody applications into earlier stages of cancer treatment, beyond palliative or late-stage interventions, represents a significant growth avenue. The increasing exploration of antibody engineering for novel drug delivery mechanisms, such as targeted delivery to the tumor microenvironment, also holds considerable promise for improving treatment efficacy and reducing systemic toxicity.

Growth Accelerators in the Cancer Monoclonal Antibodies Industry Industry

Long-term growth in the Cancer Monoclonal Antibodies industry is being significantly accelerated by breakthroughs in our understanding of cancer biology and immunology. The continuous refinement of antibody engineering techniques allows for the development of more potent and selective therapeutics. Strategic partnerships between large pharmaceutical companies and innovative biotechs are crucial for leveraging complementary expertise and R&D pipelines, expediting the journey of promising candidates from lab to market. Furthermore, the expansion of these therapies into new geographical markets, particularly in emerging economies with growing healthcare expenditure and increasing cancer burdens, acts as a significant growth catalyst. The development of advanced manufacturing technologies also contributes to increased efficiency and scalability, supporting broader market access.

Key Players Shaping the Cancer Monoclonal Antibodies Industry Market

- Genmab AS

- Novartis AG

- Amgen Inc

- Merck & Co Inc

- F Hoffmann-La Roche Ltd

- Spectrum Pharmaceuticals Inc

- Eli Lilly and Company

- Bristol Myers Squibb Company

- Johnson & Johnson

- GlaxoSmithKline PLC

Notable Milestones in Cancer Monoclonal Antibodies Industry Sector

- February 2022: The Janssen Pharmaceutical Companies of Johnson & Johnson received United States Food and Drug Administration (FDA) approval for CARVYKTI (ciltacabtagene autoleucel; cilta-cel) for the treatment of adults with relapsed or refractory multiple myeloma (RRMM) after four or more prior lines of therapy, including a proteasome inhibitor, an immunomodulatory agent, and an anti-CD38 monoclonal antibody.

- January 2022: Akeso received approval from the Center for Drug Evaluation (CDE) of China's National Medical Products Administration to commence a Phase II clinical trial of monoclonal antibody ligufalimab (AK117) and bispecific antibody ivonescimab (AK112) for first-line breast cancer.

In-Depth Cancer Monoclonal Antibodies Industry Market Outlook

The future outlook for the Cancer Monoclonal Antibodies industry is exceptionally bright, driven by sustained innovation and an expanding therapeutic reach. Key growth accelerators include the ongoing breakthroughs in understanding cancer immunology, leading to the development of novel antibody targets and mechanisms of action. Strategic collaborations and acquisitions among key players are poised to streamline R&D pipelines and enhance market penetration. Furthermore, the increasing adoption of these advanced therapies in emerging markets, coupled with favorable reimbursement policies and growing healthcare investments, will significantly contribute to market expansion. The continuous evolution of antibody engineering, focusing on enhanced specificity, reduced immunogenicity, and improved delivery systems, will further solidify the pivotal role of monoclonal antibodies in oncology.

Cancer Monoclonal Antibodies Industry Segmentation

-

1. Types of Monoclonal Antibody

- 1.1. Murine Antibodies

- 1.2. Chimeric Antibodies

- 1.3. Humanized Antibodies

-

2. Monoclonal Antibody Therapies

- 2.1. Bevacizumab (Avastin)

- 2.2. Rituximab (Rituxan)

- 2.3. Trastuzumab (Herceptin)

- 2.4. Cetuximab (Erbitux)

- 2.5. Panitumumab (Vectibix)

- 2.6. Other Monoclonal Antibody Therapies

-

3. Application

- 3.1. Breast Cancer

- 3.2. Blood Cancer

- 3.3. Liver Cancer

- 3.4. Brain Cancer

- 3.5. Colorectal Cancer

- 3.6. Other Applications

Cancer Monoclonal Antibodies Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Cancer Monoclonal Antibodies Industry Regional Market Share

Geographic Coverage of Cancer Monoclonal Antibodies Industry

Cancer Monoclonal Antibodies Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 5.1.1. Murine Antibodies

- 5.1.2. Chimeric Antibodies

- 5.1.3. Humanized Antibodies

- 5.2. Market Analysis, Insights and Forecast - by Monoclonal Antibody Therapies

- 5.2.1. Bevacizumab (Avastin)

- 5.2.2. Rituximab (Rituxan)

- 5.2.3. Trastuzumab (Herceptin)

- 5.2.4. Cetuximab (Erbitux)

- 5.2.5. Panitumumab (Vectibix)

- 5.2.6. Other Monoclonal Antibody Therapies

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Breast Cancer

- 5.3.2. Blood Cancer

- 5.3.3. Liver Cancer

- 5.3.4. Brain Cancer

- 5.3.5. Colorectal Cancer

- 5.3.6. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 6. Cancer Monoclonal Antibodies Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 6.1.1. Murine Antibodies

- 6.1.2. Chimeric Antibodies

- 6.1.3. Humanized Antibodies

- 6.2. Market Analysis, Insights and Forecast - by Monoclonal Antibody Therapies

- 6.2.1. Bevacizumab (Avastin)

- 6.2.2. Rituximab (Rituxan)

- 6.2.3. Trastuzumab (Herceptin)

- 6.2.4. Cetuximab (Erbitux)

- 6.2.5. Panitumumab (Vectibix)

- 6.2.6. Other Monoclonal Antibody Therapies

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Breast Cancer

- 6.3.2. Blood Cancer

- 6.3.3. Liver Cancer

- 6.3.4. Brain Cancer

- 6.3.5. Colorectal Cancer

- 6.3.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 7. North America Cancer Monoclonal Antibodies Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 7.1.1. Murine Antibodies

- 7.1.2. Chimeric Antibodies

- 7.1.3. Humanized Antibodies

- 7.2. Market Analysis, Insights and Forecast - by Monoclonal Antibody Therapies

- 7.2.1. Bevacizumab (Avastin)

- 7.2.2. Rituximab (Rituxan)

- 7.2.3. Trastuzumab (Herceptin)

- 7.2.4. Cetuximab (Erbitux)

- 7.2.5. Panitumumab (Vectibix)

- 7.2.6. Other Monoclonal Antibody Therapies

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Breast Cancer

- 7.3.2. Blood Cancer

- 7.3.3. Liver Cancer

- 7.3.4. Brain Cancer

- 7.3.5. Colorectal Cancer

- 7.3.6. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 8. Europe Cancer Monoclonal Antibodies Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 8.1.1. Murine Antibodies

- 8.1.2. Chimeric Antibodies

- 8.1.3. Humanized Antibodies

- 8.2. Market Analysis, Insights and Forecast - by Monoclonal Antibody Therapies

- 8.2.1. Bevacizumab (Avastin)

- 8.2.2. Rituximab (Rituxan)

- 8.2.3. Trastuzumab (Herceptin)

- 8.2.4. Cetuximab (Erbitux)

- 8.2.5. Panitumumab (Vectibix)

- 8.2.6. Other Monoclonal Antibody Therapies

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Breast Cancer

- 8.3.2. Blood Cancer

- 8.3.3. Liver Cancer

- 8.3.4. Brain Cancer

- 8.3.5. Colorectal Cancer

- 8.3.6. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 9. Asia Pacific Cancer Monoclonal Antibodies Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 9.1.1. Murine Antibodies

- 9.1.2. Chimeric Antibodies

- 9.1.3. Humanized Antibodies

- 9.2. Market Analysis, Insights and Forecast - by Monoclonal Antibody Therapies

- 9.2.1. Bevacizumab (Avastin)

- 9.2.2. Rituximab (Rituxan)

- 9.2.3. Trastuzumab (Herceptin)

- 9.2.4. Cetuximab (Erbitux)

- 9.2.5. Panitumumab (Vectibix)

- 9.2.6. Other Monoclonal Antibody Therapies

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Breast Cancer

- 9.3.2. Blood Cancer

- 9.3.3. Liver Cancer

- 9.3.4. Brain Cancer

- 9.3.5. Colorectal Cancer

- 9.3.6. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 10. Middle East and Africa Cancer Monoclonal Antibodies Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 10.1.1. Murine Antibodies

- 10.1.2. Chimeric Antibodies

- 10.1.3. Humanized Antibodies

- 10.2. Market Analysis, Insights and Forecast - by Monoclonal Antibody Therapies

- 10.2.1. Bevacizumab (Avastin)

- 10.2.2. Rituximab (Rituxan)

- 10.2.3. Trastuzumab (Herceptin)

- 10.2.4. Cetuximab (Erbitux)

- 10.2.5. Panitumumab (Vectibix)

- 10.2.6. Other Monoclonal Antibody Therapies

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Breast Cancer

- 10.3.2. Blood Cancer

- 10.3.3. Liver Cancer

- 10.3.4. Brain Cancer

- 10.3.5. Colorectal Cancer

- 10.3.6. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 11. South America Cancer Monoclonal Antibodies Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 11.1.1. Murine Antibodies

- 11.1.2. Chimeric Antibodies

- 11.1.3. Humanized Antibodies

- 11.2. Market Analysis, Insights and Forecast - by Monoclonal Antibody Therapies

- 11.2.1. Bevacizumab (Avastin)

- 11.2.2. Rituximab (Rituxan)

- 11.2.3. Trastuzumab (Herceptin)

- 11.2.4. Cetuximab (Erbitux)

- 11.2.5. Panitumumab (Vectibix)

- 11.2.6. Other Monoclonal Antibody Therapies

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Breast Cancer

- 11.3.2. Blood Cancer

- 11.3.3. Liver Cancer

- 11.3.4. Brain Cancer

- 11.3.5. Colorectal Cancer

- 11.3.6. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Types of Monoclonal Antibody

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Genmab AS

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Novartis AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Amgen Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Merck & Co Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 F Hoffmann-La Roche Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Spectrum Pharmaceuticals Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Eli Lilly and Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Bristol Myers Squibb Company

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Johnson & Johnson

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 GlaxoSmithKline PLC

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Genmab AS

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Cancer Monoclonal Antibodies Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Cancer Monoclonal Antibodies Industry Share (%) by Company 2025

List of Tables

- Table 1: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 2: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 3: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 4: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 5: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 7: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 10: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 11: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 12: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 13: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 15: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: United States Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Canada Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Mexico Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 24: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 25: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 26: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 27: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Germany Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: France Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Italy Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Spain Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 44: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 45: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 46: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 47: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 48: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 49: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: China Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: India Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Australia Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South korea Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: South korea Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 64: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 65: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 66: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 67: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 68: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 69: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 70: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: GCC Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: South Africa Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 78: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Types of Monoclonal Antibody 2020 & 2033

- Table 79: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 80: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Monoclonal Antibody Therapies 2020 & 2033

- Table 81: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 82: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 83: Cancer Monoclonal Antibodies Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 84: Cancer Monoclonal Antibodies Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: Brazil Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: Argentina Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Cancer Monoclonal Antibodies Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Cancer Monoclonal Antibodies Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cancer Monoclonal Antibodies Industry?

The projected CAGR is approximately 8.2%.

2. Which companies are prominent players in the Cancer Monoclonal Antibodies Industry?

Key companies in the market include Genmab AS, Novartis AG, Amgen Inc, Merck & Co Inc, F Hoffmann-La Roche Ltd, Spectrum Pharmaceuticals Inc , Eli Lilly and Company, Bristol Myers Squibb Company, Johnson & Johnson, GlaxoSmithKline PLC.

3. What are the main segments of the Cancer Monoclonal Antibodies Industry?

The market segments include Types of Monoclonal Antibody, Monoclonal Antibody Therapies, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 286.32 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Prevalence of Cancer; Increasing Investment in Research and Development of Genomic Studies; Rising Advancements and Preference toward Specificity of Monoclonal Antibodies to Target Cancer.

6. What are the notable trends driving market growth?

Trastuzumab (Herceptin) is Expected to Hold Significant Market Share in Monoclonal Antibody Therapies.

7. Are there any restraints impacting market growth?

Stringent Regulatory Guidelines; Long Duration of Research and Development with Rising Failures in Clinical Trials.

8. Can you provide examples of recent developments in the market?

In February 2022, the Janssen Pharmaceutical Companies of Johnson & Johnson received United States Food and Drug Administration (FDA) approval for CARVYKTI (ciltacabtagene autoleucel; cilta-cel) for the treatment of adults with relapsed or refractory multiple myeloma (RRMM) after four or more prior lines of therapy, including a proteasome inhibitor, an immunomodulatory agent, and an anti-CD38 monoclonal antibody.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cancer Monoclonal Antibodies Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cancer Monoclonal Antibodies Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cancer Monoclonal Antibodies Industry?

To stay informed about further developments, trends, and reports in the Cancer Monoclonal Antibodies Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence