Key Insights

The China telecom industry, currently valued at $491.90 million in 2025, is projected to experience steady growth, driven by increasing smartphone penetration, rising data consumption fueled by the popularity of OTT services and online gaming, and the expansion of 5G networks. Key players like China Telecom Corp, China Mobile, and China United Network Communications Group Co Ltd are investing heavily in infrastructure upgrades and service diversification to capitalize on this growth. The segment analysis reveals that data and messaging services, including internet and handset data packages, are the largest revenue generators, benefiting from lucrative package discounts and competitive pricing strategies. Voice services, while remaining a significant component, are experiencing slower growth compared to data services, reflecting the shift towards digital communication. The burgeoning OTT and PayTV services market represents a significant growth opportunity, with companies like Tencent Holdings Ltd playing a crucial role. While regulatory changes and competition from smaller players pose some restraints, the overall market outlook remains positive. The continued expansion of 5G infrastructure, government initiatives promoting digital transformation, and the growing adoption of innovative technologies like cloud computing and IoT are expected to further stimulate market expansion throughout the forecast period (2025-2033).

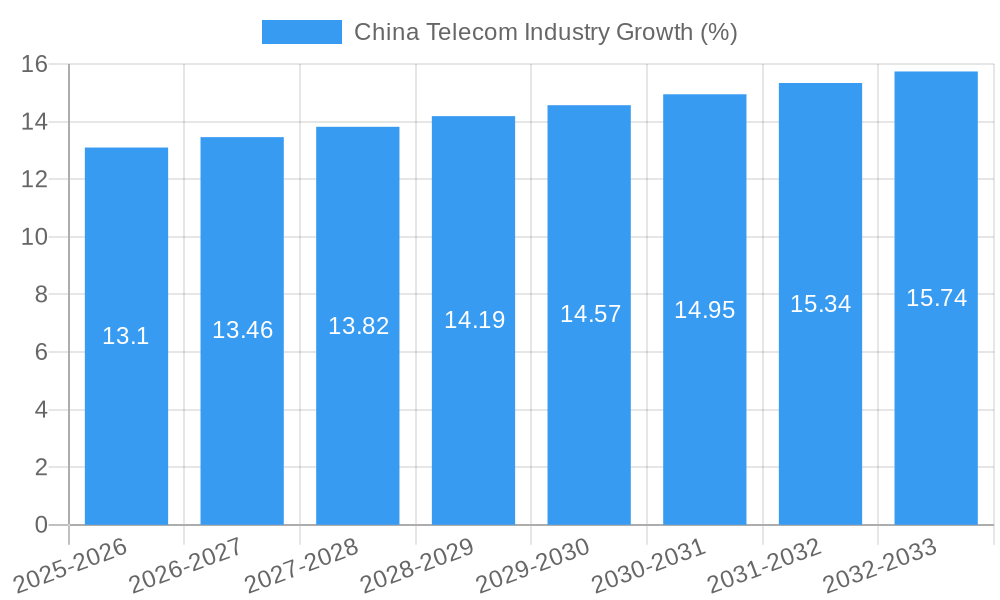

The industry's Compound Annual Growth Rate (CAGR) of 2.71% suggests a gradual but consistent growth trajectory. This relatively modest CAGR could be attributed to market saturation in certain areas and intense competition among established players. However, the untapped potential within rural areas and the ongoing development of advanced technologies offer substantial opportunities for further expansion. Profitability is likely to be influenced by factors such as effective cost management, strategic partnerships, and the ability to innovate and offer competitive pricing strategies for data packages and value-added services. The successful navigation of regulatory landscapes and the ongoing adaptation to evolving consumer preferences will be critical for long-term success within this dynamic and competitive market.

China Telecom Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the China Telecom industry, encompassing market dynamics, growth trends, competitive landscape, and future outlook. With a study period spanning 2019-2033 (base year 2025, forecast period 2025-2033), this report is an essential resource for industry professionals, investors, and strategic planners seeking to navigate the complexities of this rapidly evolving sector. The report delves into key segments like Voice Services, Wireless Data & Messaging, and OTT & PayTV Services, providing detailed market size estimations (in Million units) and average revenue per user (ARPU) analysis.

China Telecom Industry Market Dynamics & Structure

This section analyzes the competitive intensity and technological innovation drivers within China's telecom sector. Market concentration is high, with a few dominant players commanding significant market share. The regulatory framework, characterized by government policies promoting digital infrastructure development and 5G expansion, significantly influences market growth. Technological innovation, primarily focused on 5G deployment, cloud computing, and IoT, shapes the competitive landscape. The increasing adoption of cloud-based services and the rise of over-the-top (OTT) platforms present both opportunities and challenges for traditional telecom providers. Significant M&A activity continues to reshape the industry landscape, consolidating market power and driving technological integration.

- Market Concentration: High, with China Mobile holding a dominant position. China Telecom and China Unicom hold substantial but smaller market shares. xx% of the market is controlled by the top 3 players.

- Technological Innovation Drivers: 5G rollout, cloud computing, IoT, AI, Big Data analytics.

- Regulatory Framework: Favorable government policies supporting digital infrastructure and 5G expansion. Stringent regulations regarding data privacy and cybersecurity.

- Competitive Product Substitutes: OTT platforms (e.g., Tencent), VoIP services, and alternative communication platforms.

- End-User Demographics: A large and growing middle class fuels demand for advanced telecom services. Urban areas show higher penetration rates than rural areas.

- M&A Trends: Consolidation through mergers and acquisitions to achieve economies of scale and expand service offerings. xx major M&A deals were recorded between 2019-2024.

China Telecom Industry Growth Trends & Insights

The China Telecom industry exhibits robust growth, driven by the increasing demand for data and broadband services. High smartphone penetration and the rising adoption of mobile internet have propelled significant growth in wireless data and messaging services. Market size has expanded considerably over the historical period (2019-2024), exhibiting a Compound Annual Growth Rate (CAGR) of xx%. Technological advancements, particularly the deployment of 5G networks, have further accelerated this expansion. Consumer behavior is shifting towards data-intensive applications, fueling demand for high-speed internet access and value-added services. The increasing adoption of OTT platforms and pay-TV services presents both opportunities and challenges for traditional telecom operators.

Dominant Regions, Countries, or Segments in China Telecom Industry

The coastal regions of China (e.g., Guangdong, Shanghai, Jiangsu) are the dominant drivers of market growth, due to higher economic activity, denser populations, and advanced infrastructure. Among the services segments, Wireless Data and Messaging Services demonstrate the highest growth potential, driven by rising smartphone penetration, increased internet usage, and the proliferation of data-intensive applications.

- Key Drivers:

- Rapid urbanization and increasing disposable incomes.

- Government initiatives promoting digital infrastructure development.

- High smartphone penetration and increasing internet usage.

- Dominant Segments: Wireless Data & Messaging Services show the highest growth, followed by OTT & PayTV. Voice services are experiencing a decline in revenue but remain a significant part of the market.

- Market Share & Growth Potential: Wireless data commands the largest market share, with an estimated xx% in 2025, and is projected to grow at a CAGR of xx% during the forecast period. OTT and PayTV segments exhibit strong growth potential fueled by increasing consumer demand for entertainment content.

- Average Revenue Per User (ARPU): ARPU for the overall services segment is estimated at xx in 2025. Wireless Data & Messaging has the highest ARPU at xx, indicating high profitability in this segment.

Market Size Estimates (in Million units):

| Segment | 2020 | 2021 | 2022 | 2023 (Est) | 2024 (Est) | 2025 (Est) | 2027 (Est) | |----------------------|-------|-------|-------|------------|------------|------------|------------| | Voice Services | 1500 | 1450 | 1400 | 1350 | 1300 | 1250 | 1100 | | Wireless Data | 2000 | 2500 | 3000 | 3500 | 4000 | 4500 | 5500 | | OTT & PayTV Services | 500 | 600 | 700 | 800 | 900 | 1000 | 1200 |

China Telecom Industry Product Landscape

The product landscape is characterized by a wide range of services, including voice, data, messaging, broadband internet, fixed-line telephony, and value-added services. Innovation focuses on enhancing network speed and capacity (5G), improving service quality, and expanding the range of smart home and IoT applications. Key features include flexible data packages, bundled services, and personalized offers tailored to different customer segments. Technological advancements in areas like network virtualization, cloud computing, and edge computing are improving efficiency, scalability, and customer experience.

Key Drivers, Barriers & Challenges in China Telecom Industry

Key Drivers:

- Rising smartphone penetration and internet usage.

- Government initiatives promoting digital infrastructure.

- Growing demand for data-intensive applications.

- Increasing adoption of cloud-based services.

Key Challenges & Restraints:

- Intense competition from both established players and new entrants.

- Increasing regulatory scrutiny and compliance costs.

- Infrastructure limitations in some regions.

- Cybersecurity threats and data privacy concerns.

- The need for continuous investment in network upgrades and expansion to meet growing demand and maintain competitiveness.

Emerging Opportunities in China Telecom Industry

- Untapped markets in rural areas.

- Growth in IoT and smart city applications.

- Expanding applications of 5G technology.

- Opportunities in the development of industry-specific telecom solutions.

- Development of innovative services targeted at the expanding aging population.

Growth Accelerators in the China Telecom Industry

Technological breakthroughs in 5G and edge computing will significantly boost growth. Strategic partnerships with technology companies and content providers will expand service offerings and broaden market reach. Aggressive market expansion strategies in under-served regions, will further drive growth.

Key Players Shaping the China Telecom Industry Market

- China Telecom Corp

- ZTE Corporation

- FiberHome Telecommunication Technologies Co Ltd

- China Satellite Communications Co Ltd

- Wingtech Technology Co Ltd

- China Railway Signal & Communication Co Ltd

- Singtel Optus Pty

- Jiangsu Zhongtian Technology Co Ltd

- Tencent Holdings Ltd

- China United Network Communications Group Co Ltd

Notable Milestones in China Telecom Industry Sector

- August 2022: China Telecom adds 44 million 5G subscribers, reaching 231.7 million (60% of its mobile base).

- September 2022: ZTE Corporation launches a new-generation 4K Wi-Fi 6 mesh media gateway set-top box.

In-Depth China Telecom Industry Market Outlook

The future of the China Telecom industry is bright, driven by sustained growth in data consumption, 5G adoption, and the expansion of the IoT sector. Strategic investments in network infrastructure, coupled with innovative service offerings and strategic partnerships, will unlock significant growth potential. The continued development of cloud computing, AI, and Big Data analytics will further shape the industry landscape, fostering increased efficiency and creating new opportunities for market players.

China Telecom Industry Segmentation

-

1. Segmenta

-

1.1. Voice Services

- 1.1.1. Wired

- 1.1.2. Wireless

- 1.2. Data and

- 1.3. OTT and PayTV Services

-

1.1. Voice Services

China Telecom Industry Segmentation By Geography

- 1. China

China Telecom Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.71% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Continuous roll out of 5G; Growth of high-quality defensive companies; Demand for new digital services

- 3.3. Market Restrains

- 3.3.1. High Cost of Satellite Imaging Data Acquisition and Processing; High-resolution Images Offered by Other Imaging Technologies

- 3.4. Market Trends

- 3.4.1. Stellar performance of 5G would trigger wireless segment growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Telecom Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Segmenta

- 5.1.1. Voice Services

- 5.1.1.1. Wired

- 5.1.1.2. Wireless

- 5.1.2. Data and

- 5.1.3. OTT and PayTV Services

- 5.1.1. Voice Services

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. China

- 5.1. Market Analysis, Insights and Forecast - by Segmenta

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 China Satellite Communications Co Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 China Telecom Corp

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 FiberHome Telecommunication Technologies Co Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Wingtech Technology Co Ltd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 China Railway Signal & Communication Co Ltd

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 ZTE Corporation

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Singtel Optus Pty

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Jiangsu Zhongtian Technology Co Ltd

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Tencent Holdings Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 China United Network Communications Group Co Ltd

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 China Satellite Communications Co Ltd

List of Figures

- Figure 1: China Telecom Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Telecom Industry Share (%) by Company 2024

List of Tables

- Table 1: China Telecom Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Telecom Industry Revenue Million Forecast, by Segmenta 2019 & 2032

- Table 3: China Telecom Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: China Telecom Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: China Telecom Industry Revenue Million Forecast, by Segmenta 2019 & 2032

- Table 6: China Telecom Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Telecom Industry?

The projected CAGR is approximately 2.71%.

2. Which companies are prominent players in the China Telecom Industry?

Key companies in the market include China Satellite Communications Co Ltd, China Telecom Corp, FiberHome Telecommunication Technologies Co Ltd, Wingtech Technology Co Ltd, China Railway Signal & Communication Co Ltd, ZTE Corporation, Singtel Optus Pty, Jiangsu Zhongtian Technology Co Ltd, Tencent Holdings Ltd, China United Network Communications Group Co Ltd.

3. What are the main segments of the China Telecom Industry?

The market segments include Segmenta.

4. Can you provide details about the market size?

The market size is estimated to be USD 491.90 Million as of 2022.

5. What are some drivers contributing to market growth?

Continuous roll out of 5G; Growth of high-quality defensive companies; Demand for new digital services.

6. What are the notable trends driving market growth?

Stellar performance of 5G would trigger wireless segment growth.

7. Are there any restraints impacting market growth?

High Cost of Satellite Imaging Data Acquisition and Processing; High-resolution Images Offered by Other Imaging Technologies.

8. Can you provide examples of recent developments in the market?

In August 2022, according to data provided in its most recent financial report, China Telecom added about 44 million more consumers to its 5G package during the first half of this year, bringing the number at the end of June to 231.7 million - more than 60% of its whole mobile client base of 384.2 million. However, it still lags behind the market leader, China Mobile, which, according to its most recent financial report, has 970 million mobile subscribers, 511 million of whom have signed up for 5G packages.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Telecom Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Telecom Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Telecom Industry?

To stay informed about further developments, trends, and reports in the China Telecom Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence