Key Insights

The global Cholesterol Drug market is projected to reach $12.3 billion by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 10.31% from 2025 to 2033. This significant growth is attributed to the rising incidence of hypercholesterolemia and cardiovascular diseases, driven by an aging global population, sedentary lifestyles, and evolving dietary habits. Increased awareness regarding cholesterol management and the availability of advanced therapies, such as PCSK9 inhibitors, are key market drivers. The 30-50 year old demographic represents a substantial segment due to the early onset of lifestyle-related health conditions. While statins remain the market leaders due to their established efficacy and cost-effectiveness, PCSK9 inhibitors are rapidly gaining market share, particularly for patients with refractory hypercholesterolemia, due to their superior lipid-lowering capabilities. Personalized medicine and innovative drug delivery systems are also contributing to market dynamics.

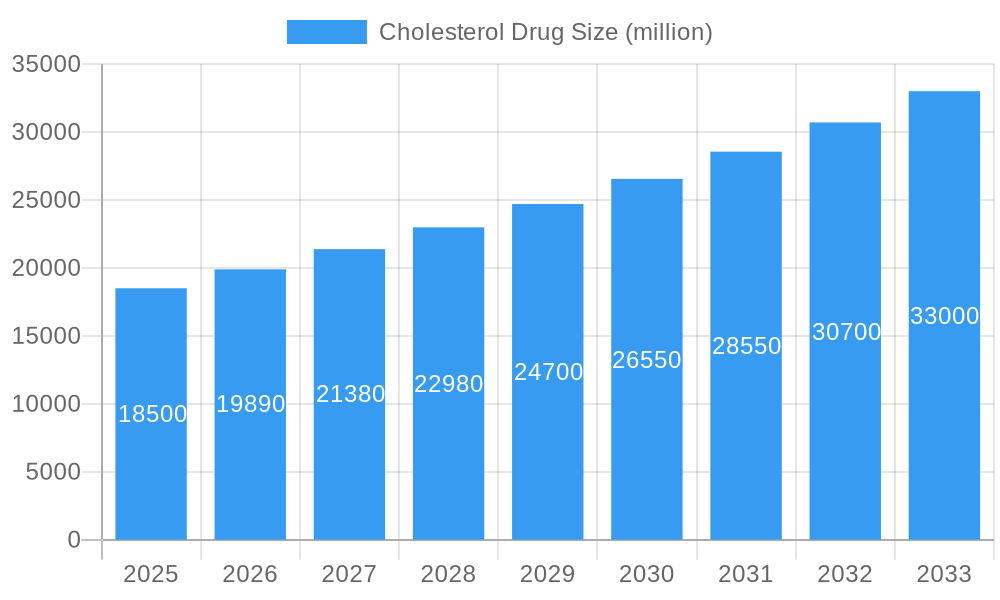

Cholesterol Drug Market Size (In Billion)

Challenges for the market include the high cost of advanced treatments, such as PCSK9 inhibitors, which can restrict access, especially in developing economies. Stringent regulatory approvals and the requirement for extensive clinical trials also present hurdles for new market entrants. However, a growing emphasis on preventive healthcare and favorable reimbursement policies in developed nations are expected to counterbalance these challenges. Key market trends include the development of combination therapies to enhance treatment outcomes and reduce the burden of cardiovascular disease. Emerging markets, particularly in the Asia Pacific region, offer substantial opportunities due to their large populations and increasing healthcare investments. Strategic collaborations and R&D investments by major pharmaceutical companies like Pfizer, Merck, and Amgen are vital for innovation and addressing unmet needs in the cholesterol drug sector.

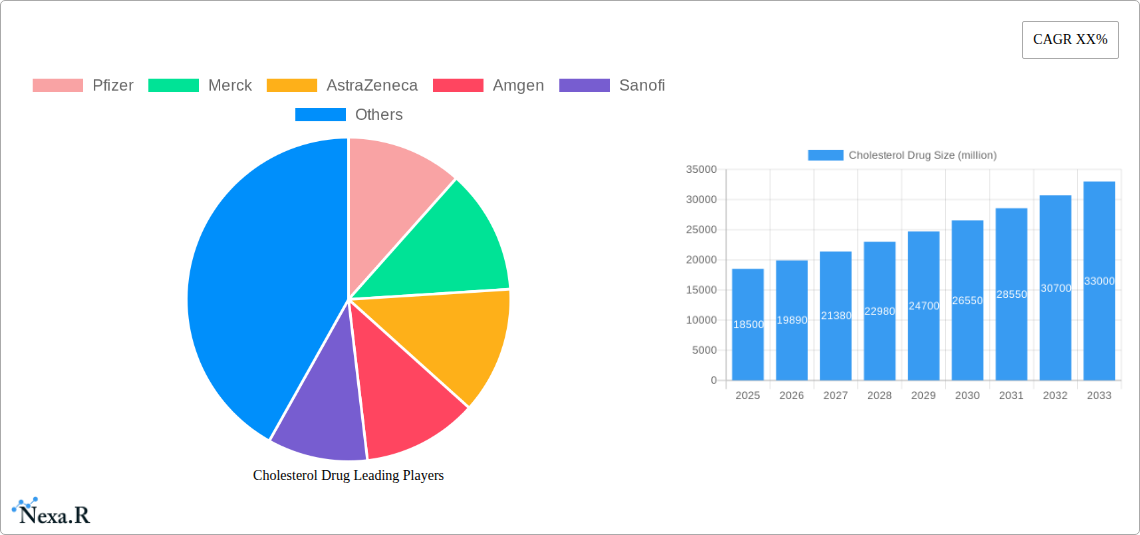

Cholesterol Drug Company Market Share

This comprehensive report provides an in-depth analysis of the global cholesterol drug market. It offers critical insights for pharmaceutical manufacturers, healthcare providers, investors, and policymakers, covering the historical period of 2019–2024, the base year of 2025, and the forecast period of 2025–2033. Utilizing advanced analytical tools and extensive research, the report delivers a robust market outlook, examining market structure, growth drivers, regional trends, product innovation, and strategic initiatives shaping this crucial pharmaceutical segment. Market values are presented in billion units.

Cholesterol Drug Market Dynamics & Structure

The global cholesterol drug market is characterized by a dynamic interplay of technological advancements, evolving regulatory landscapes, and shifting end-user demographics. While the market exhibits moderate concentration, with established players like Pfizer, Merck, and AstraZeneca holding significant shares, the emergence of innovative therapies, particularly PCSK9 inhibitors, is fostering competitive intensity. Technological innovation remains a primary driver, fueled by research into novel drug mechanisms and delivery systems aimed at improving efficacy and patient adherence. Stringent regulatory frameworks, while ensuring drug safety and efficacy, can also present barriers to entry for new market participants.

- Market Concentration: Moderate to high, dominated by key global pharmaceutical giants.

- Technological Innovation Drivers: Development of novel drug classes (e.g., PCSK9 inhibitors), advanced formulations, and personalized medicine approaches.

- Regulatory Frameworks: Strict approval processes by agencies like the FDA and EMA, impacting R&D timelines and market access.

- Competitive Product Substitutes: Advancements in lifestyle interventions (diet, exercise) and other cardiovascular disease management strategies present indirect competition.

- End-User Demographics: An aging global population and increasing prevalence of lifestyle-related diseases drive demand.

- M&A Trends: Strategic acquisitions and partnerships aimed at expanding product portfolios and market reach continue to shape the competitive landscape. For instance, M&A deal volumes in the cardiovascular drug segment averaged approximately 15-20 deals annually over the historical period, with deal values ranging from xx million to xx million USD.

Cholesterol Drug Growth Trends & Insights

The cholesterol drug market is poised for sustained growth, driven by a confluence of factors including increasing global cardiovascular disease burden, rising awareness of hyperlipidemia management, and continuous advancements in therapeutic options. The market size is projected to evolve from an estimated xx,xxx million units in 2025 to xx,xxx million units by 2033, reflecting a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period. Adoption rates for newer, more effective therapies like PCSK9 inhibitors are steadily increasing, particularly among high-risk patient populations.

Technological disruptions are fundamentally reshaping treatment paradigms. The shift from traditional statins, which will continue to hold a substantial market share due to their efficacy and cost-effectiveness, towards PCSK9 inhibitors offers significant therapeutic advantages for patients who are statin-intolerant or have refractory hypercholesterolemia. Consumer behavior is also evolving, with patients becoming more informed and proactive in managing their health, seeking personalized treatment plans and demanding greater convenience and efficacy from their medications. This trend is further amplified by increased access to healthcare information and a growing emphasis on preventative care.

Market penetration of cholesterol-lowering drugs is projected to rise, especially in emerging economies where awareness and access to healthcare are improving. The demand for effective treatments for dyslipidemia is intrinsically linked to the global rise in obesity and sedentary lifestyles, creating a robust and expanding patient pool. Future growth will also be influenced by the development of combination therapies and strategies to address medication adherence challenges. The market will likely see a continued expansion driven by both established and novel therapeutic modalities, catering to a diverse range of patient needs and treatment profiles.

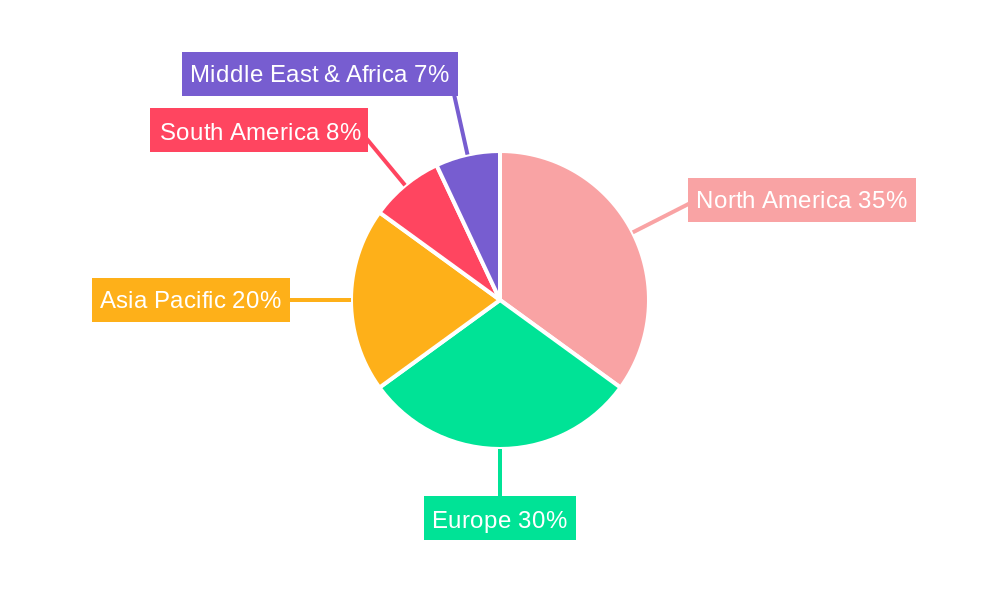

Dominant Regions, Countries, or Segments in Cholesterol Drug

The > 50 Years Old segment within the Application category is the dominant force driving growth in the global cholesterol drug market. This demographic, characterized by a higher prevalence of cardiovascular diseases and age-related health concerns, accounts for an estimated 65% of the total market share in 2025. North America, particularly the United States, currently leads in market value and volume, owing to high healthcare expenditure, advanced diagnostic capabilities, and widespread adoption of innovative therapies.

Key Drivers of Dominance in the > 50 Years Old Segment and North America:

- Aging Population: A continuously expanding elderly population globally, leading to a higher incidence of hypercholesterolemia and associated cardiovascular risks.

- Prevalence of Cardiovascular Diseases: The > 50 years old group has the highest burden of heart disease, stroke, and other cardiovascular conditions, necessitating aggressive lipid management.

- Healthcare Infrastructure & Access: Well-established healthcare systems and insurance coverage in regions like North America ensure greater access to diagnosis and treatment for cholesterol-related disorders.

- Technological Adoption: Early and widespread adoption of advanced cholesterol-lowering drugs, including PCSK9 inhibitors, within this demographic.

- Economic Policies: Government initiatives and reimbursement policies that favor the treatment of chronic diseases, including hyperlipidemia.

- Market Share: The > 50 years old segment commands approximately xx,xxx million units of the total market in 2025, with projected growth to xx,xxx million units by 2033. North America's market share in 2025 is estimated at xx,xxx million units.

- Growth Potential: While mature, this segment continues to grow due to increased life expectancy and improved diagnostic rates. Emerging markets are also showing significant growth potential in this demographic as healthcare access expands.

Among the Types of cholesterol drugs, Statins are expected to maintain their leading position due to their proven efficacy, established safety profile, and cost-effectiveness, representing a significant portion of the market volume. However, PCSK9 inhibitors are experiencing rapid growth and are projected to capture an increasing market share, particularly for high-risk patients, owing to their superior lipid-lowering capabilities. The growth potential of PCSK9 inhibitors in this segment is substantial, driven by ongoing research and expanding indications.

Cholesterol Drug Product Landscape

The cholesterol drug product landscape is marked by continuous innovation aimed at enhancing therapeutic efficacy, patient convenience, and addressing unmet medical needs. Statins, the cornerstone of cholesterol management, offer a wide range of products with varying potencies and formulations, ensuring broad applicability. Emerging therapeutic classes, notably PCSK9 inhibitors, have revolutionized treatment for refractory hypercholesterolemia, offering significantly greater LDL cholesterol reduction. Selective Cholesterol Absorption Inhibitors provide a complementary mechanism of action, often used in combination therapies. Resins continue to play a role, particularly in specific patient populations. Product differentiation centers on novel delivery systems, improved side-effect profiles, and cost-effectiveness, with ongoing research into gene therapies and novel molecular targets promising future breakthroughs.

Key Drivers, Barriers & Challenges in Cholesterol Drug

Key Drivers:

- Rising Prevalence of Cardiovascular Diseases: The escalating global burden of heart disease and stroke is the primary catalyst for cholesterol drug demand.

- Aging Global Population: Increased life expectancy leads to a larger susceptible population for hyperlipidemia and related conditions.

- Technological Advancements: Development of more effective and targeted therapies like PCSK9 inhibitors.

- Growing Healthcare Expenditure: Increased investment in healthcare globally allows for greater access to diagnostics and treatments.

- Increased Health Awareness: Patients are becoming more proactive in managing their health, seeking preventative measures and effective treatments.

Key Barriers & Challenges:

- High Cost of Novel Therapies: The premium pricing of newer drugs like PCSK9 inhibitors can limit accessibility, especially in cost-sensitive markets. For example, the annual cost of PCSK9 inhibitors can range from $14,000 to $20,000 USD per patient, a significant barrier.

- Regulatory Hurdles: Stringent approval processes and post-market surveillance can prolong time-to-market for new drugs.

- Patent Expirations and Generic Competition: The looming expiration of patents for blockbuster statins can lead to price erosion and increased competition from generics.

- Side Effect Profiles and Patient Adherence: While generally safe, some cholesterol drugs can have side effects, impacting patient adherence and treatment outcomes.

- Reimbursement Challenges: Navigating complex reimbursement landscapes and securing payer coverage for innovative therapies can be a significant challenge.

- Supply Chain Complexities: Ensuring consistent and timely supply of a diverse range of cholesterol drugs globally can be impacted by manufacturing capacity and logistical hurdles.

Emerging Opportunities in Cholesterol Drug

Emerging opportunities in the cholesterol drug market lie in the development of personalized medicine approaches tailored to individual genetic profiles and risk factors, enhancing treatment efficacy and reducing adverse events. Untapped markets in emerging economies present significant growth potential as healthcare infrastructure improves and awareness of cardiovascular disease management increases. Innovative drug delivery systems, such as long-acting injectables and oral formulations with improved bioavailability, offer opportunities to enhance patient adherence and convenience. Furthermore, the exploration of novel therapeutic targets beyond LDL cholesterol, such as Lp(a) and triglycerides, presents a vast frontier for innovative treatments. The integration of digital health solutions for patient monitoring and support also offers a burgeoning avenue for market expansion and improved patient outcomes.

Growth Accelerators in the Cholesterol Drug Industry

Long-term growth in the cholesterol drug industry will be significantly accelerated by ongoing technological breakthroughs in drug discovery and development, leading to the creation of novel, more potent, and safer therapeutic agents. Strategic partnerships and collaborations between pharmaceutical giants and smaller biotech firms will foster innovation and expedite the commercialization of promising pipeline drugs. Market expansion strategies, particularly targeting underserved populations and emerging economies, will unlock substantial growth potential. The increasing focus on preventative cardiology and the development of early intervention strategies, coupled with advancements in diagnostic tools, will drive earlier and more widespread treatment initiation. Furthermore, the development of fixed-dose combination therapies can improve patient adherence and simplify treatment regimens, acting as a significant growth catalyst.

Key Players Shaping the Cholesterol Drug Market

- Pfizer

- Merck

- AstraZeneca

- Amgen

- Sanofi

- Sun Pharm

- Mylan

- TEVA

- China National Pharmaceutical Group

- PKU Healthcare

Notable Milestones in Cholesterol Drug Sector

- 2019: FDA approval of several novel PCSK9 inhibitors for expanded patient indications.

- 2020: Increased clinical trials focusing on combination therapies and new drug targets for hyperlipidemia.

- 2021: Emergence of significant research into gene therapy for inherited forms of hypercholesterolemia.

- 2022: Expansion of statin biosimil market, increasing affordability and accessibility.

- 2023: Growing emphasis on real-world evidence studies for PCSK9 inhibitors to demonstrate long-term effectiveness and cost-effectiveness.

- 2024: Advancements in diagnostic technologies for earlier and more accurate identification of dyslipidemia.

In-Depth Cholesterol Drug Market Outlook

The cholesterol drug market is set for robust expansion, driven by persistent and growing cardiovascular disease risk factors, an aging global population, and continuous pharmaceutical innovation. Key growth accelerators include the development of next-generation therapies with enhanced efficacy and safety profiles, such as novel PCSK9 inhibitors and emerging molecular targets. Strategic market expansion into emerging economies, coupled with increasing healthcare access and disposable incomes, will unlock significant untapped potential. The integration of advanced diagnostic tools and personalized medicine approaches will foster earlier intervention and more targeted treatment strategies. Furthermore, increasing regulatory support for innovative therapies and evolving reimbursement policies are expected to facilitate broader market penetration, ensuring a positive and dynamic outlook for the cholesterol drug industry.

Cholesterol Drug Segmentation

-

1. Application

- 1.1. <30 Years Old

- 1.2. 30 ~ 50 Years Old

- 1.3. > 50 Years Old

-

2. Types

- 2.1. Statins

- 2.2. PCSK9 inhibitors

- 2.3. Selective Cholesterol Absorption Inhibitors

- 2.4. Resins

Cholesterol Drug Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cholesterol Drug Regional Market Share

Geographic Coverage of Cholesterol Drug

Cholesterol Drug REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.31% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. <30 Years Old

- 5.1.2. 30 ~ 50 Years Old

- 5.1.3. > 50 Years Old

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Statins

- 5.2.2. PCSK9 inhibitors

- 5.2.3. Selective Cholesterol Absorption Inhibitors

- 5.2.4. Resins

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Cholesterol Drug Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. <30 Years Old

- 6.1.2. 30 ~ 50 Years Old

- 6.1.3. > 50 Years Old

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Statins

- 6.2.2. PCSK9 inhibitors

- 6.2.3. Selective Cholesterol Absorption Inhibitors

- 6.2.4. Resins

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Cholesterol Drug Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. <30 Years Old

- 7.1.2. 30 ~ 50 Years Old

- 7.1.3. > 50 Years Old

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Statins

- 7.2.2. PCSK9 inhibitors

- 7.2.3. Selective Cholesterol Absorption Inhibitors

- 7.2.4. Resins

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Cholesterol Drug Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. <30 Years Old

- 8.1.2. 30 ~ 50 Years Old

- 8.1.3. > 50 Years Old

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Statins

- 8.2.2. PCSK9 inhibitors

- 8.2.3. Selective Cholesterol Absorption Inhibitors

- 8.2.4. Resins

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Cholesterol Drug Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. <30 Years Old

- 9.1.2. 30 ~ 50 Years Old

- 9.1.3. > 50 Years Old

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Statins

- 9.2.2. PCSK9 inhibitors

- 9.2.3. Selective Cholesterol Absorption Inhibitors

- 9.2.4. Resins

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Cholesterol Drug Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. <30 Years Old

- 10.1.2. 30 ~ 50 Years Old

- 10.1.3. > 50 Years Old

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Statins

- 10.2.2. PCSK9 inhibitors

- 10.2.3. Selective Cholesterol Absorption Inhibitors

- 10.2.4. Resins

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Cholesterol Drug Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. <30 Years Old

- 11.1.2. 30 ~ 50 Years Old

- 11.1.3. > 50 Years Old

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Statins

- 11.2.2. PCSK9 inhibitors

- 11.2.3. Selective Cholesterol Absorption Inhibitors

- 11.2.4. Resins

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Pfizer

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Merck

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 AstraZeneca

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Amgen

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Sanofi

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sun Pharm

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Mylan

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 TEVA

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 China National Pharmaceutical Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 PKU Healthcare

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Pfizer

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cholesterol Drug Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Cholesterol Drug Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Cholesterol Drug Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cholesterol Drug Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Cholesterol Drug Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Cholesterol Drug Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Cholesterol Drug Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cholesterol Drug Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Cholesterol Drug Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cholesterol Drug Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Cholesterol Drug Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Cholesterol Drug Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Cholesterol Drug Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cholesterol Drug Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Cholesterol Drug Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cholesterol Drug Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Cholesterol Drug Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Cholesterol Drug Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Cholesterol Drug Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cholesterol Drug Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cholesterol Drug Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cholesterol Drug Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Cholesterol Drug Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Cholesterol Drug Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cholesterol Drug Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cholesterol Drug Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Cholesterol Drug Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cholesterol Drug Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Cholesterol Drug Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Cholesterol Drug Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Cholesterol Drug Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cholesterol Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Cholesterol Drug Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Cholesterol Drug Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Cholesterol Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Cholesterol Drug Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Cholesterol Drug Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Cholesterol Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Cholesterol Drug Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Cholesterol Drug Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Cholesterol Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Cholesterol Drug Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Cholesterol Drug Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Cholesterol Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Cholesterol Drug Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Cholesterol Drug Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Cholesterol Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Cholesterol Drug Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Cholesterol Drug Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cholesterol Drug Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cholesterol Drug?

The projected CAGR is approximately 10.31%.

2. Which companies are prominent players in the Cholesterol Drug?

Key companies in the market include Pfizer, Merck, AstraZeneca, Amgen, Sanofi, Sun Pharm, Mylan, TEVA, China National Pharmaceutical Group, PKU Healthcare.

3. What are the main segments of the Cholesterol Drug?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.3 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cholesterol Drug," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cholesterol Drug report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cholesterol Drug?

To stay informed about further developments, trends, and reports in the Cholesterol Drug, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence