Key Insights

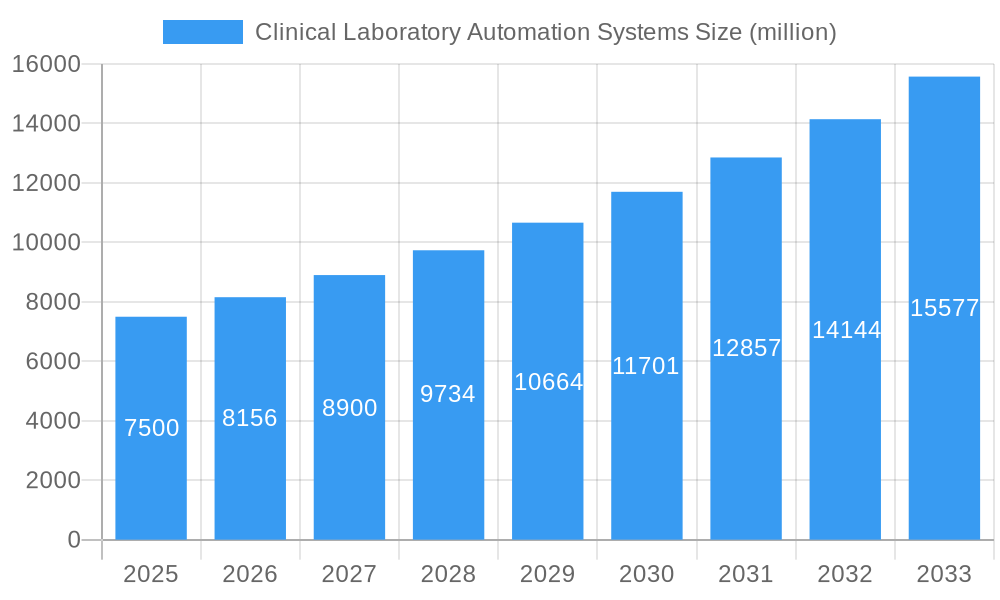

The global Clinical Laboratory Automation Systems market is poised for significant expansion, projected to reach a substantial market size of approximately USD 7,500 million by 2025. This growth trajectory is fueled by a Compound Annual Growth Rate (CAGR) of roughly 8.5%, indicating a dynamic and rapidly evolving sector. The increasing demand for enhanced diagnostic accuracy, faster turnaround times, and reduced manual labor in clinical settings are the primary drivers propelling this market forward. Advancements in robotics, artificial intelligence, and machine learning are being integrated into pre-analysis, under-analysis, and post-analysis systems, optimizing workflows from sample handling to data interpretation. Research institutions and universities are heavily investing in these automated solutions to facilitate groundbreaking research and accelerate scientific discovery. Furthermore, the rising incidence of chronic diseases and the growing global population contribute to an escalating volume of laboratory tests, necessitating efficient and scalable automation solutions.

Clinical Laboratory Automation Systems Market Size (In Billion)

Despite the robust growth, certain restraints could temper the market's full potential. High initial investment costs for sophisticated automation systems and the need for specialized technical expertise for operation and maintenance can pose challenges, particularly for smaller laboratories or those in developing regions. However, the long-term benefits of increased throughput, improved precision, and cost savings through reduced error rates are expected to outweigh these initial hurdles. Key players like Thermo Fisher, Beckman Coulter, and Roche are continuously innovating, introducing integrated platforms and modular solutions to cater to diverse laboratory needs. The market is segmented by application, with Research Institutions and Universities being major consumers, and by type, encompassing Pre-Analysis, Under-Analysis, and Post-Analysis Systems. The Asia Pacific region, particularly China and India, is expected to witness the highest growth rates due to increasing healthcare expenditure and a growing adoption of advanced medical technologies.

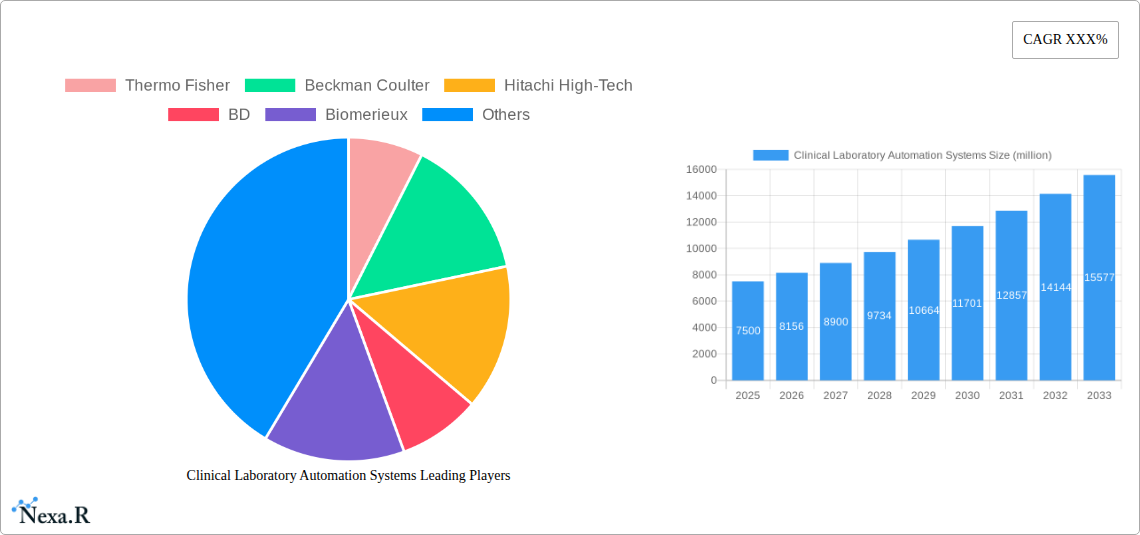

Clinical Laboratory Automation Systems Company Market Share

Clinical Laboratory Automation Systems Market Report: Unlocking Efficiency and Precision in Healthcare

This comprehensive report offers an in-depth analysis of the global Clinical Laboratory Automation Systems market, providing critical insights into market dynamics, growth trends, regional dominance, product innovations, key drivers, barriers, and emerging opportunities. Leveraging high-traffic keywords such as "clinical laboratory automation," "laboratory automation systems," "pre-analytical automation," "analytical automation," "post-analytical automation," "laboratory information systems," "diagnostic automation," and "healthcare laboratory solutions," this report is designed to maximize search engine visibility and engage industry professionals, including researchers, laboratory managers, healthcare administrators, and technology providers.

The market is segmented by Application into Research Institutions, University, and Others, and by Type into Pre-Analysis System, Under Analysis System, and Post-Analysis System. Key industry developments are meticulously analyzed to provide a holistic view of the market landscape. The study period spans from 2019 to 2033, with a base year of 2025, an estimated year of 2025, and a forecast period from 2025 to 2033, built upon a historical period from 2019 to 2024. The report presents all quantitative values in million units for clarity and comparability.

Clinical Laboratory Automation Systems Market Dynamics & Structure

The global clinical laboratory automation systems market exhibits a moderately concentrated structure, with a few dominant players controlling a significant market share. This concentration is driven by substantial R&D investments, stringent regulatory approvals, and the high capital expenditure required for developing and implementing advanced automation solutions. Technological innovation is a primary driver, with ongoing advancements in robotics, artificial intelligence (AI), machine learning (ML), and data analytics significantly enhancing the capabilities of laboratory automation systems. These innovations are focused on improving throughput, accuracy, traceability, and workflow efficiency. Regulatory frameworks, such as FDA guidelines and ISO certifications, play a crucial role in ensuring product safety, efficacy, and interoperability, influencing market entry and product development strategies. Competitive product substitutes, though limited in full-scale automation, include semi-automated instruments and manual processing, particularly in smaller or specialized laboratories. End-user demographics are shifting towards larger hospital networks, reference laboratories, and academic institutions that benefit most from economies of scale and the need for high-volume, high-throughput testing. Mergers and acquisitions (M&A) are prevalent, aimed at consolidating market presence, acquiring innovative technologies, and expanding product portfolios. Recent M&A activities reflect a strategic push for vertical integration and the acquisition of specialized automation components or software solutions.

- Market Concentration: Dominated by key players, leading to a competitive but consolidated landscape.

- Technological Innovation Drivers: AI, ML, robotics, IoT integration, and miniaturization are pushing the boundaries of what laboratory automation can achieve.

- Regulatory Frameworks: Compliance with FDA, CE Mark, and ISO standards is paramount for market access and credibility.

- Competitive Product Substitutes: Semi-automated instruments and manual processing are still utilized in specific contexts, especially in resource-limited settings or for niche applications.

- End-User Demographics: Increasing adoption in high-throughput diagnostic laboratories, major hospitals, and academic research centers.

- M&A Trends: Strategic acquisitions to gain market share, access new technologies, and broaden product offerings. For example, recent M&A deals in the past year have focused on acquiring specialized software for AI-driven diagnostics and robotics for sample handling.

Clinical Laboratory Automation Systems Growth Trends & Insights

The global clinical laboratory automation systems market is experiencing robust growth, projected to expand at a significant Compound Annual Growth Rate (CAGR) from the historical period of 2019-2024 through the forecast period of 2025-2033. This expansion is fueled by an escalating demand for enhanced diagnostic accuracy, reduced turnaround times, and improved laboratory efficiency. The increasing prevalence of chronic diseases and infectious outbreaks worldwide necessitates faster and more reliable diagnostic testing, positioning laboratory automation as an indispensable solution. Adoption rates are steadily climbing across healthcare institutions, driven by a growing awareness of the benefits of automation, including minimized human error, standardized workflows, and enhanced biosafety. Technological disruptions are continuously reshaping the market. The integration of AI and ML algorithms is revolutionizing data analysis, enabling predictive diagnostics and personalized medicine. Furthermore, the development of modular and scalable automation systems caters to a wider range of laboratory sizes and budgets. Consumer behavior shifts are also playing a pivotal role. Healthcare providers are increasingly prioritizing patient outcomes and operational efficiency, leading to greater investment in advanced laboratory technologies. Patients, in turn, benefit from quicker test results and more accurate diagnoses. The market penetration of sophisticated automation solutions is expected to deepen, particularly in emerging economies as healthcare infrastructure improves and the demand for quality diagnostics rises. The market size is anticipated to grow from approximately USD 6,500 million in 2024 to an estimated USD 12,300 million by 2033. This growth trajectory is underpinned by continuous innovation and a growing recognition of the critical role of laboratory automation in modern healthcare delivery. The adoption of track-and-trace technologies for samples and reagents further bolsters confidence and efficiency.

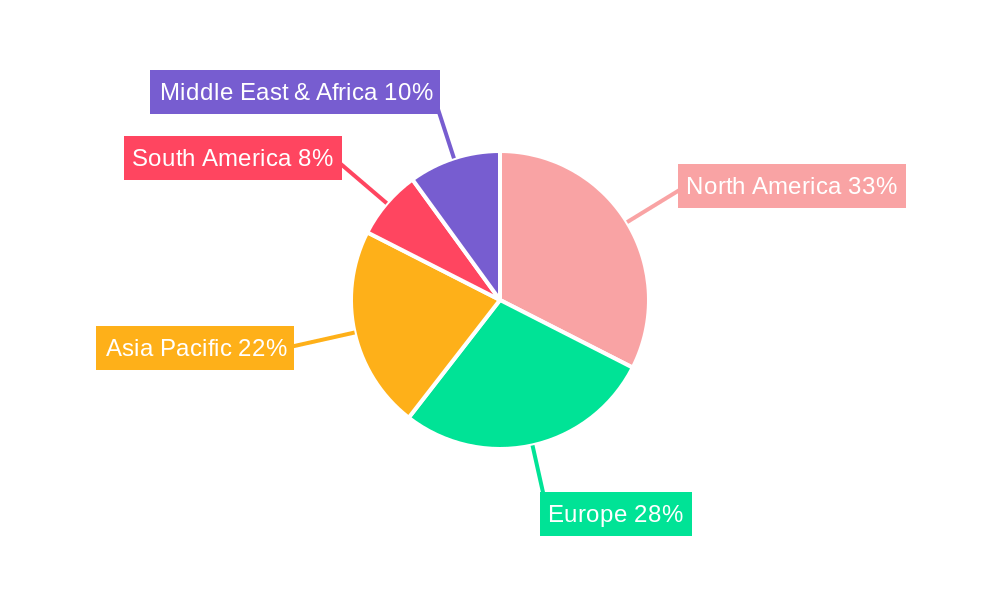

Dominant Regions, Countries, or Segments in Clinical Laboratory Automation Systems

North America currently stands as the dominant region in the clinical laboratory automation systems market, driven by its advanced healthcare infrastructure, high per capita healthcare spending, and strong emphasis on technological adoption. The United States, in particular, accounts for a substantial portion of this regional dominance. Key drivers include a well-established network of research institutions and hospitals that are early adopters of cutting-edge laboratory technologies, significant government funding for healthcare research and development, and a favorable regulatory environment that encourages innovation. The increasing burden of chronic diseases and an aging population in North America further amplify the demand for efficient and accurate diagnostic solutions.

Within the Application segment, Research Institutions and University laboratories are major contributors to market growth. These entities constantly push the boundaries of scientific discovery, requiring high-throughput, precise, and reliable automated systems for complex experimental protocols, genomics, proteomics, and drug discovery. Their need for reproducibility and data integrity makes automation a critical investment. The "Others" segment, encompassing large hospital networks and independent diagnostic laboratories, also represents a significant and growing market share, driven by the demand for routine high-volume testing and efficient patient care.

Considering the Type segment, the Pre-Analysis System is currently experiencing the most rapid growth and holds a substantial market share. This is attributed to the critical role of sample preparation in ensuring the accuracy of downstream analytical processes. Automation in pre-analysis addresses challenges such as sample tracking, sorting, aliquoting, and centrifugation, which are often labor-intensive and prone to errors. Growth in this segment is fueled by the need to streamline the initial stages of the laboratory workflow, reduce pre-analytical errors, and improve sample integrity from collection to analysis. The Under Analysis System segment also shows consistent growth, driven by the demand for sophisticated automated analyzers for various diagnostic tests, including clinical chemistry, immunoassay, hematology, and microbiology. Advancements in detection technologies and robotics are continuously improving the performance and throughput of these systems. The Post-Analysis System segment, while perhaps smaller in immediate market share, is crucial for automating tasks like data management, reporting, and result validation, which are increasingly integrated into comprehensive laboratory automation solutions.

- North America's Dominance: Fueled by advanced infrastructure, high healthcare expenditure, and rapid tech adoption.

- Key Drivers in the US: Strong R&D investment, demand for precision medicine, and a robust diagnostic testing market.

- Application Leadership: Research Institutions and Universities lead in adopting advanced automation for discovery, while large hospitals and diagnostic labs drive high-volume testing needs.

- Pre-Analysis System Growth: Rapid expansion driven by the need to minimize pre-analytical errors and enhance sample integrity.

- Under Analysis System Evolution: Continuous innovation in analytical instruments for a wide range of diagnostic assays.

- Post-Analysis System Integration: Growing importance in automating data handling and reporting for seamless workflow integration.

Clinical Laboratory Automation Systems Product Landscape

The product landscape of clinical laboratory automation systems is characterized by a continuous stream of innovations aimed at enhancing efficiency, accuracy, and flexibility. Companies are developing integrated workflow solutions that seamlessly connect pre-analytical sample processing, analytical testing, and post-analytical data management. Key product innovations include advanced robotic liquid handling systems, automated sample sorters and decappers, high-throughput immunoassay and molecular diagnostic platforms, and intelligent software solutions powered by AI for workflow optimization and data interpretation. Unique selling propositions often lie in the modularity of systems, allowing for scalability and customization to meet specific laboratory needs, as well as the integration of advanced imaging and detection technologies for improved diagnostic sensitivity and specificity. For instance, new systems are incorporating AI-driven image analysis for rapid identification of anomalies in samples, and advanced robotics are enabling unattended operation for extended periods, significantly reducing labor costs and improving turnaround times.

Key Drivers, Barriers & Challenges in Clinical Laboratory Automation Systems

Key Drivers:

- Increasing Demand for Accuracy and Efficiency: The need for faster, more accurate diagnostic results to improve patient care and reduce healthcare costs is a primary growth accelerator.

- Technological Advancements: Continuous innovation in robotics, AI, ML, and miniaturization enables the development of more sophisticated and cost-effective automation solutions.

- Growing Prevalence of Chronic Diseases and Infectious Outbreaks: These necessitate high-volume, rapid, and reliable diagnostic testing, driving demand for automated systems.

- Labor Shortages and Skilled Personnel Requirements: Automation helps alleviate the pressure of skilled labor shortages in laboratories, improving productivity and reducing staff burnout.

- Focus on Workflow Optimization: Laboratories are increasingly seeking to streamline operations, minimize manual interventions, and reduce turnaround times through integrated automation solutions.

Barriers & Challenges:

- High Initial Investment Costs: The capital expenditure required for acquiring and implementing advanced automation systems can be a significant barrier, particularly for smaller laboratories.

- Integration Complexity: Integrating new automation systems with existing laboratory information systems (LIS) and other legacy equipment can be complex and time-consuming.

- Maintenance and Service Requirements: Sophisticated automation systems require regular maintenance and specialized technical support, which can add to operational costs.

- Regulatory Hurdles: Obtaining regulatory approvals for new automation technologies can be a lengthy and stringent process, impacting market entry timelines.

- Resistance to Change: Some laboratory personnel may exhibit resistance to adopting new technologies due to concerns about job security or the learning curve associated with new systems.

- Supply Chain Disruptions: Global supply chain vulnerabilities can impact the availability of critical components and lead to production delays.

Emerging Opportunities in Clinical Laboratory Automation Systems

Emerging opportunities in the clinical laboratory automation systems market are centered around the integration of advanced technologies and the expansion into new application areas. The rise of point-of-care testing (POCT) presents a significant opportunity for developing compact, automated solutions that can deliver rapid diagnostics directly to patients. Furthermore, the increasing adoption of AI and machine learning in diagnostics is creating demand for automation systems capable of sophisticated data analysis, predictive diagnostics, and personalized treatment recommendations. The growing field of digital pathology and genomics also offers fertile ground for specialized automated solutions. The untapped potential in emerging economies, as healthcare infrastructure improves and the demand for quality diagnostics rises, represents another key growth avenue. Companies can also leverage opportunities by developing modular and scalable automation platforms that cater to a wider range of laboratory sizes and budgetary constraints, thereby democratizing access to automation.

Growth Accelerators in the Clinical Laboratory Automation Systems Industry

Several catalysts are accelerating long-term growth in the clinical laboratory automation systems industry. Technological breakthroughs in areas like microfluidics and lab-on-a-chip technologies are enabling the development of more compact, efficient, and cost-effective automation solutions. Strategic partnerships between automation manufacturers and diagnostic assay developers are crucial for creating integrated, end-to-end solutions that address specific clinical needs. Market expansion strategies targeting developing regions, coupled with government initiatives to improve healthcare infrastructure, are opening up new avenues for growth. The increasing focus on personalized medicine and companion diagnostics is also driving demand for highly specialized and accurate automated testing platforms. Furthermore, the growing emphasis on data analytics and artificial intelligence in healthcare is spurring the development of intelligent automation systems that can provide deeper insights from diagnostic data, further enhancing their value proposition.

Key Players Shaping the Clinical Laboratory Automation Systems Market

- Thermo Fisher

- Beckman Coulter

- Hitachi High-Tech

- BD

- Biomerieux

- Roche

- Abbot (GLP System)

- Copan Italia

- A & T Corporation

- Instrumentation Laboratory

Notable Milestones in Clinical Laboratory Automation Systems Sector

- 2019: Launch of advanced AI-powered sample handling robots, significantly improving throughput and reducing errors in high-volume laboratories.

- 2020: Introduction of integrated pre-analytical and analytical automation platforms designed for infectious disease testing, crucial during the pandemic.

- 2021: Significant investments in R&D for developing modular and scalable automation solutions to cater to diverse laboratory needs.

- 2022: Increased focus on cybersecurity for laboratory automation systems to protect sensitive patient data and ensure operational integrity.

- 2023: Emergence of smart algorithms for predictive maintenance of automation equipment, minimizing downtime and optimizing performance.

- 2024: Growing adoption of cloud-based LIS integration with automation systems for enhanced data accessibility and collaboration.

In-Depth Clinical Laboratory Automation Systems Market Outlook

The future outlook for the clinical laboratory automation systems market is exceptionally promising, characterized by sustained innovation and expanding adoption across the globe. Growth accelerators will continue to be driven by the relentless pursuit of diagnostic accuracy, operational efficiency, and cost-effectiveness in healthcare. The integration of advanced AI and ML capabilities will transform laboratories into intelligent hubs capable of not only performing tests but also providing predictive insights and supporting personalized medicine. Strategic collaborations, particularly between technology providers and healthcare institutions, will be vital in developing bespoke automation solutions that address evolving clinical demands. Furthermore, the growing emphasis on real-time data analytics and the need for seamless integration across the entire diagnostic workflow will fuel the demand for comprehensive automation platforms. Emerging markets, with their rapidly developing healthcare sectors, present significant untapped potential for market expansion. The market is poised for significant growth, projected to reach an estimated USD 12,300 million by 2033, reflecting its indispensable role in modern healthcare delivery.

Clinical Laboratory Automation Systems Segmentation

-

1. Application

- 1.1. Research Institutions

- 1.2. University

- 1.3. Others

-

2. Type

- 2.1. Pre-Analysis System

- 2.2. Under Analysis System

- 2.3. Post-Analysis System

Clinical Laboratory Automation Systems Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Clinical Laboratory Automation Systems Regional Market Share

Geographic Coverage of Clinical Laboratory Automation Systems

Clinical Laboratory Automation Systems REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Research Institutions

- 5.1.2. University

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Pre-Analysis System

- 5.2.2. Under Analysis System

- 5.2.3. Post-Analysis System

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Clinical Laboratory Automation Systems Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Research Institutions

- 6.1.2. University

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Pre-Analysis System

- 6.2.2. Under Analysis System

- 6.2.3. Post-Analysis System

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Clinical Laboratory Automation Systems Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Research Institutions

- 7.1.2. University

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Pre-Analysis System

- 7.2.2. Under Analysis System

- 7.2.3. Post-Analysis System

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Clinical Laboratory Automation Systems Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Research Institutions

- 8.1.2. University

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Pre-Analysis System

- 8.2.2. Under Analysis System

- 8.2.3. Post-Analysis System

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Clinical Laboratory Automation Systems Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Research Institutions

- 9.1.2. University

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Pre-Analysis System

- 9.2.2. Under Analysis System

- 9.2.3. Post-Analysis System

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Clinical Laboratory Automation Systems Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Research Institutions

- 10.1.2. University

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Pre-Analysis System

- 10.2.2. Under Analysis System

- 10.2.3. Post-Analysis System

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Clinical Laboratory Automation Systems Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Research Institutions

- 11.1.2. University

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Pre-Analysis System

- 11.2.2. Under Analysis System

- 11.2.3. Post-Analysis System

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Thermo Fisher

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Beckman Coulter

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Hitachi High-Tech

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 BD

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Biomerieux

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Roche

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Abbot(GLP System)

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Copan Italia

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 A & T Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Instrumentation Laboratory

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Thermo Fisher

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Clinical Laboratory Automation Systems Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Clinical Laboratory Automation Systems Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Clinical Laboratory Automation Systems Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Clinical Laboratory Automation Systems Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Clinical Laboratory Automation Systems Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Clinical Laboratory Automation Systems Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Clinical Laboratory Automation Systems Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Clinical Laboratory Automation Systems Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Clinical Laboratory Automation Systems Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Clinical Laboratory Automation Systems Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Clinical Laboratory Automation Systems Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Clinical Laboratory Automation Systems Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Clinical Laboratory Automation Systems Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Clinical Laboratory Automation Systems Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Clinical Laboratory Automation Systems Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Clinical Laboratory Automation Systems Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Clinical Laboratory Automation Systems Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Clinical Laboratory Automation Systems Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Clinical Laboratory Automation Systems Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Clinical Laboratory Automation Systems Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Clinical Laboratory Automation Systems Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Clinical Laboratory Automation Systems Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Clinical Laboratory Automation Systems Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Clinical Laboratory Automation Systems Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Clinical Laboratory Automation Systems Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Clinical Laboratory Automation Systems Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Clinical Laboratory Automation Systems Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Clinical Laboratory Automation Systems Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Clinical Laboratory Automation Systems Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Clinical Laboratory Automation Systems Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Clinical Laboratory Automation Systems Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Clinical Laboratory Automation Systems Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Clinical Laboratory Automation Systems Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Clinical Laboratory Automation Systems?

The projected CAGR is approximately 9.3%.

2. Which companies are prominent players in the Clinical Laboratory Automation Systems?

Key companies in the market include Thermo Fisher, Beckman Coulter, Hitachi High-Tech, BD, Biomerieux, Roche, Abbot(GLP System), Copan Italia, A & T Corporation, Instrumentation Laboratory.

3. What are the main segments of the Clinical Laboratory Automation Systems?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.27 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Clinical Laboratory Automation Systems," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Clinical Laboratory Automation Systems report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Clinical Laboratory Automation Systems?

To stay informed about further developments, trends, and reports in the Clinical Laboratory Automation Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence