Key Insights

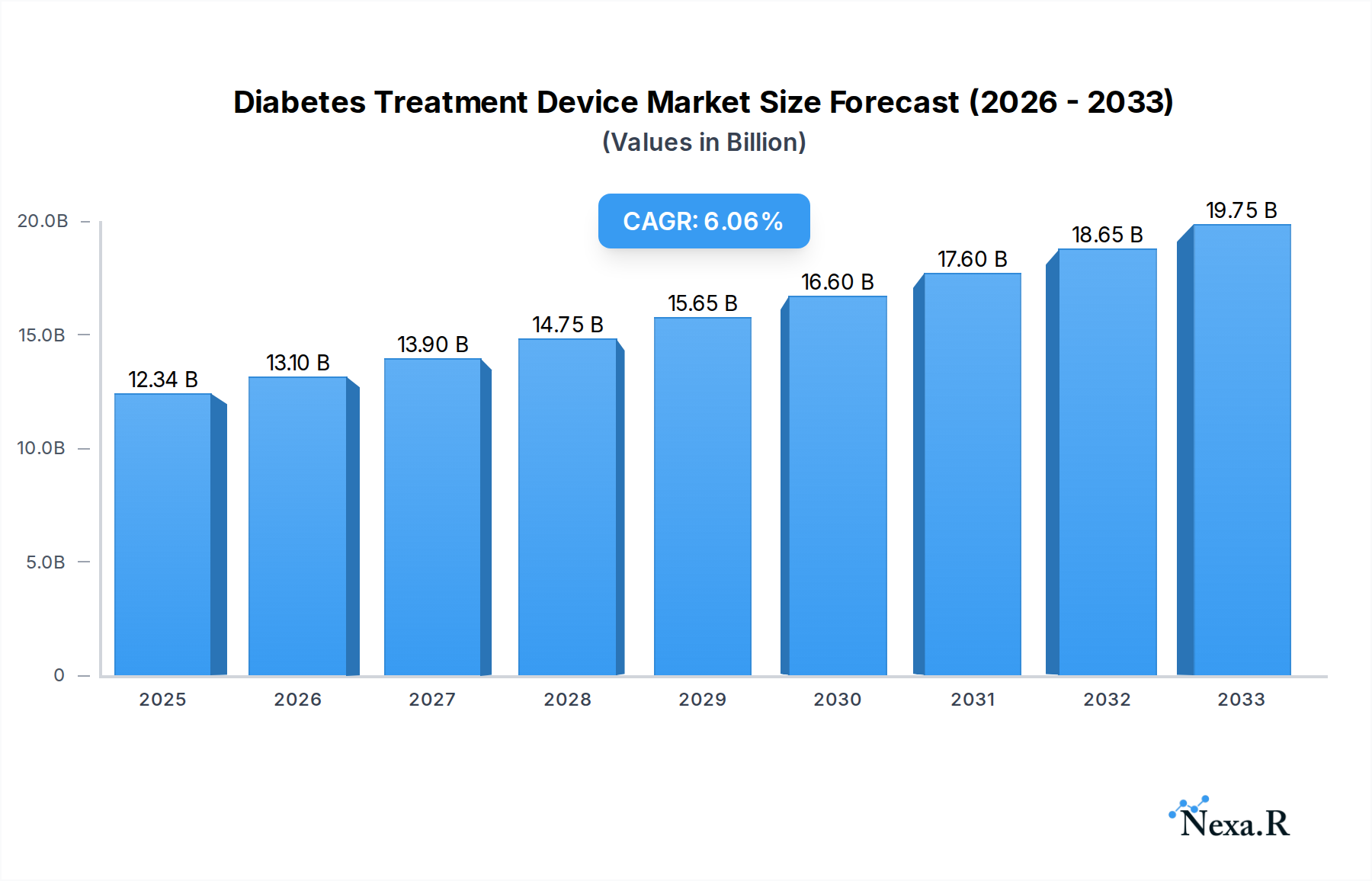

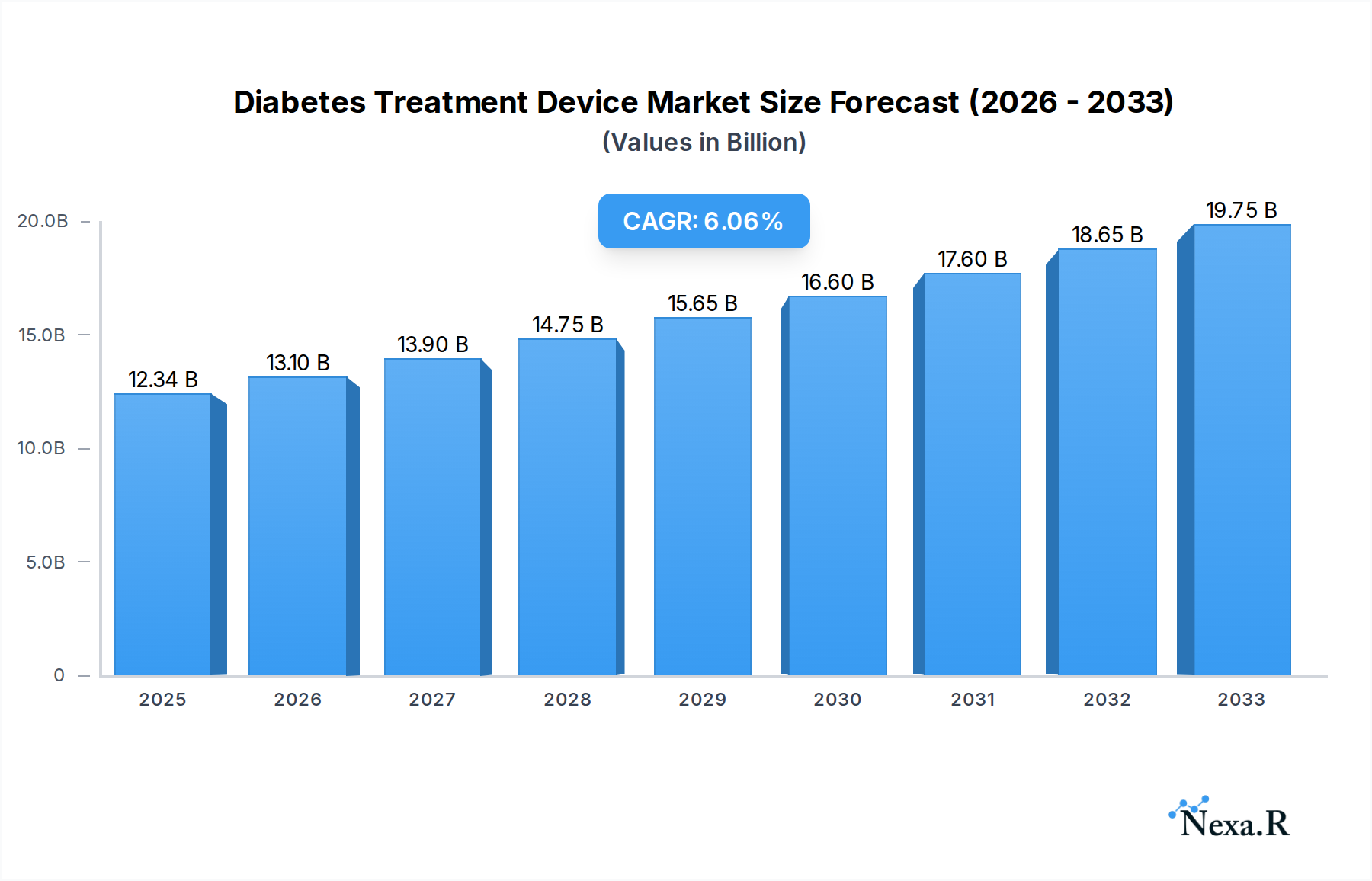

The global Diabetes Treatment Device market is poised for significant expansion, projected to reach a market size of $12.34 billion in 2025. This growth is underpinned by a healthy CAGR of 6.3%, indicating a robust upward trajectory through 2033. The primary drivers fueling this surge include the escalating global prevalence of diabetes, the increasing adoption of advanced diabetes management technologies, and a growing awareness among patients and healthcare providers regarding the benefits of integrated treatment solutions. Technological advancements, such as continuous glucose monitoring (CGM) systems and smart insulin pens, are revolutionizing patient care, offering greater accuracy, convenience, and personalized treatment regimens. Furthermore, the rising disposable income in emerging economies and supportive government initiatives for diabetes management are contributing to market accessibility and demand. The market is segmented into various applications, with Hospitals and Clinics representing a substantial share due to established healthcare infrastructure and patient influx. The Homecare segment is also experiencing rapid growth, driven by the convenience and autonomy these devices offer to patients. In terms of types, Insulin Pens and Insulin Pumps are leading the charge, reflecting a shift towards more sophisticated and user-friendly insulin delivery systems.

Diabetes Treatment Device Market Size (In Billion)

Despite the promising outlook, certain restraints could temper market expansion. These include the high cost of advanced diabetes treatment devices, which can limit accessibility for a significant portion of the global population, particularly in price-sensitive markets. Reimbursement policies and regulatory hurdles in various regions also present challenges for widespread adoption. Moreover, a lack of awareness and understanding regarding the latest technological advancements among certain patient demographics could slow down market penetration. Nevertheless, the overarching trend towards personalized medicine and the increasing burden of diabetes globally are expected to outweigh these restraints. Key players like Roche, Medtronic, and Abbott are actively investing in research and development to innovate and expand their product portfolios, further stimulating market growth. The Asia Pacific region, with its large and growing diabetic population, is anticipated to emerge as a significant growth engine for the diabetes treatment device market.

Diabetes Treatment Device Company Market Share

The global diabetes treatment device market is characterized by a moderate to high market concentration, with key players like Roche, Tandem Diabetes Care, Inc., B. Braun Melsungen AG, Medtronic, BD, Novo Nordisk A/S, Abbott, and Sanofi continuously vying for market share. Technological innovation is a primary driver, with continuous advancements in insulin pumps, smart insulin delivery systems, and integrated continuous glucose monitoring (CGM) solutions redefining patient care. Regulatory frameworks, primarily overseen by bodies like the FDA and EMA, are crucial in ensuring product safety and efficacy, influencing market entry and product development cycles. Competitive product substitutes, including advancements in oral antidiabetic medications and novel therapeutic approaches, present a dynamic competitive landscape. End-user demographics are shifting, with an increasing aging population and a rise in diabetes prevalence worldwide, particularly in developing economies, driving demand. Mergers and acquisitions (M&A) activity remains robust, signaling strategic consolidation and expansion efforts by leading companies. For instance, recent M&A deals have focused on integrating digital health platforms with existing device portfolios, aiming to offer end-to-end diabetes management solutions. Innovation barriers, such as the high cost of R&D and stringent clinical trial requirements, are significant, yet the potential for improved patient outcomes and a growing market continually incentivizes investment.

Diabetes Treatment Device Growth Trends & Insights

The global diabetes treatment device market is poised for significant expansion, driven by an escalating prevalence of diabetes worldwide and a growing demand for sophisticated management solutions. The market size evolution is projected to be substantial, with current estimates for the base year 2025 indicating a valuation of approximately XX billion units. This growth is underpinned by increasing adoption rates of advanced diabetes management technologies, most notably insulin pumps and continuous glucose monitoring (CGM) systems, which are gradually replacing traditional insulin syringes and pens in developed markets. Technological disruptions are at the forefront, with the integration of artificial intelligence (AI) and machine learning (ML) into smart insulin delivery systems promising more personalized and automated glycemic control. These innovations are enhancing the efficacy and convenience of treatment, leading to improved patient adherence and better health outcomes.

Consumer behavior shifts are also playing a pivotal role. Patients are becoming more proactive in managing their diabetes, actively seeking out user-friendly, connected devices that offer real-time data and seamless integration with mobile health applications. The rise of telehealth and remote patient monitoring further fuels this trend, enabling healthcare providers to offer more personalized care and timely interventions. The CAGR for the forecast period 2025–2033 is anticipated to be robust, with projections suggesting an average annual growth rate of XX%. This impressive trajectory is driven by several factors. Firstly, the growing awareness among patients and healthcare professionals about the benefits of advanced diabetes management devices in preventing long-term complications is a key accelerator. Secondly, favorable reimbursement policies and increasing healthcare expenditure in both developed and emerging economies are making these devices more accessible.

Furthermore, the continuous influx of new product launches and upgrades by leading manufacturers, including Roche, Tandem Diabetes Care, Inc., Medtronic, Abbott, and Novo Nordisk A/S, ensures a dynamic market with ongoing innovation. The increasing focus on developing closed-loop systems, often referred to as artificial pancreas systems, which automate insulin delivery based on real-time glucose readings, represents a significant technological leap. These systems are crucial in improving the quality of life for individuals with Type 1 diabetes and are gradually gaining traction in Type 2 diabetes management. The penetration of these advanced devices is expected to rise significantly in the homecare segment, reflecting a broader trend of decentralizing healthcare delivery and empowering patients to manage their conditions effectively outside traditional clinical settings. The market's growth is further bolstered by strategic partnerships and collaborations between device manufacturers, pharmaceutical companies, and technology providers, aimed at developing integrated solutions that address the multifaceted needs of diabetes patients.

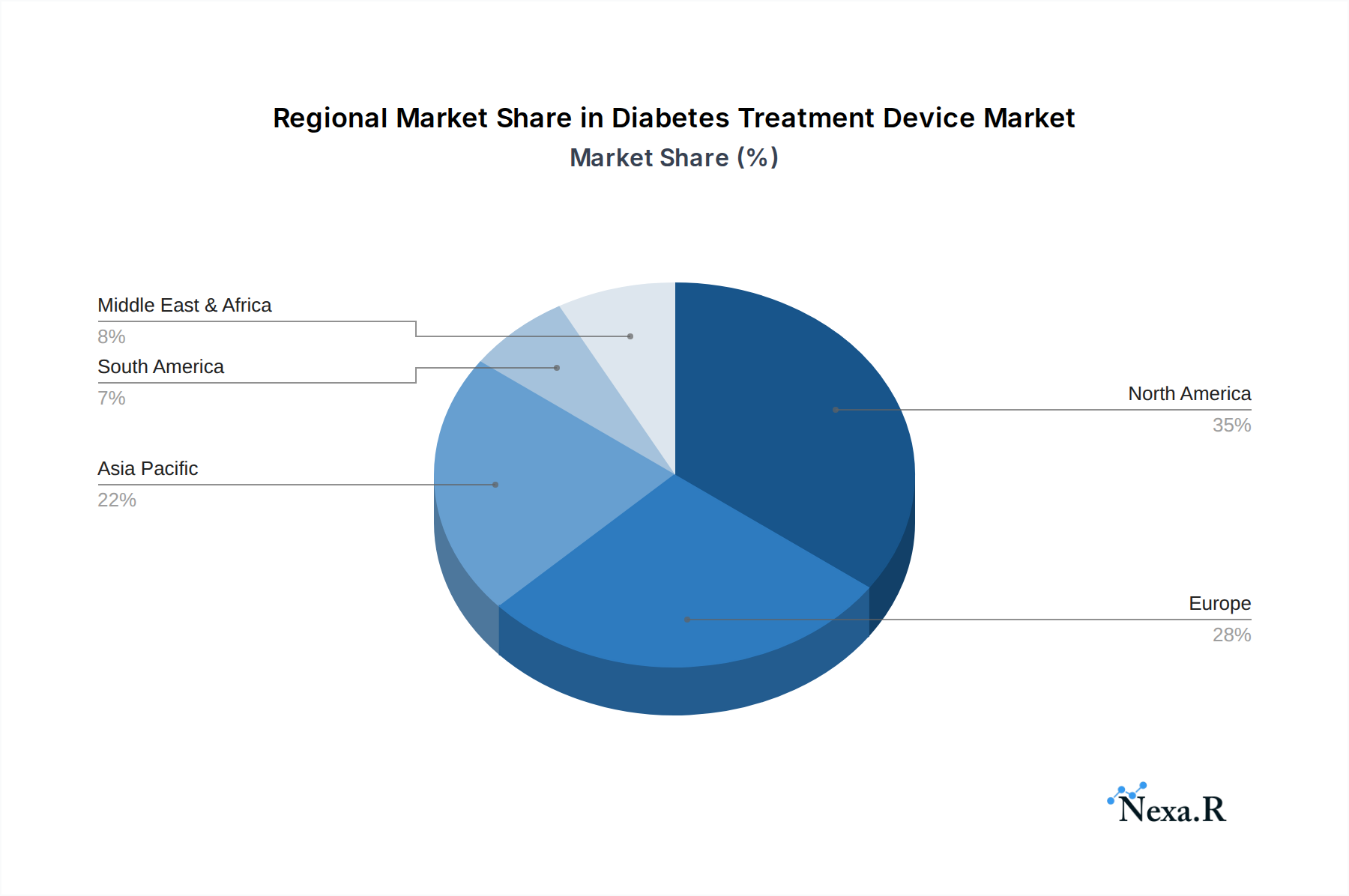

Dominant Regions, Countries, or Segments in Diabetes Treatment Device

The global diabetes treatment device market’s dominance is intricately linked to a confluence of economic strength, healthcare infrastructure, and patient demographics, with North America currently emerging as the leading region. The Application segment of Homecare is experiencing unparalleled growth, driven by a significant shift in patient preference towards self-management and the increasing adoption of advanced technologies in domestic settings. This shift is further amplified by technological advancements in wearable and connected devices, making them indispensable tools for daily diabetes management.

North America, particularly the United States, holds a commanding position due to its high prevalence of diabetes, advanced healthcare infrastructure, and strong economic capacity to invest in and adopt new medical technologies. The presence of major market players like Medtronic, Abbott, and Tandem Diabetes Care, Inc., coupled with favorable reimbursement policies and a highly health-conscious population, further solidifies its leadership. In terms of Types, Insulin Pumps are a significant growth driver within North America. These devices offer a more sophisticated and personalized approach to insulin delivery compared to traditional methods, leading to improved glycemic control and enhanced quality of life for patients. The increasing demand for automated insulin delivery systems, such as closed-loop systems, is a testament to the region's embrace of cutting-edge solutions.

The Clinics application segment also plays a crucial role, acting as key centers for diagnosis, treatment initiation, and patient education on the use of advanced diabetes devices. Healthcare professionals in clinics are instrumental in guiding patients towards the most suitable treatment options, thereby influencing purchasing decisions. Furthermore, the robust presence of research and development facilities and a strong emphasis on clinical trials contribute to the rapid introduction and validation of new diabetes treatment devices in this region.

Emerging economies, particularly in the Asia Pacific region, are exhibiting substantial growth potential, fueled by rising diabetes rates, increasing disposable incomes, and government initiatives to improve healthcare access. While North America currently leads, the Homecare application segment is projected to witness the highest CAGR globally, reflecting a paradigm shift in diabetes management towards patient empowerment and remote monitoring. This growth is propelled by the increasing affordability and user-friendliness of connected devices, making them accessible to a wider population. The Insulin Pumps segment, within the broader Types category, is also a key growth engine across all major regions, underscoring the global trend towards advanced insulin delivery solutions. The market's trajectory indicates a future where home-based, technologically integrated diabetes management becomes the norm, supported by a diverse range of innovative devices.

Diabetes Treatment Device Product Landscape

The diabetes treatment device landscape is characterized by continuous innovation, focusing on enhancing patient convenience, accuracy, and overall glycemic control. Key product advancements include the development of smart insulin pens equipped with memory functions and connectivity features, providing users with detailed historical data on insulin delivery. Insulin pumps are evolving towards more sophisticated closed-loop systems that seamlessly integrate with continuous glucose monitoring (CGM) devices, offering automated insulin adjustments and minimizing the risk of hypoglycemia and hyperglycemia. These devices often boast unique selling propositions such as discreet designs, extended battery life, and intuitive user interfaces. Technological advancements are also evident in insulin jet injectors, offering needle-free delivery, and in the development of more precise and user-friendly insulin syringes with enhanced safety features. The overarching trend is towards digital integration, empowering patients with real-time data and enabling remote monitoring by healthcare providers.

Key Drivers, Barriers & Challenges in Diabetes Treatment Device

Key Drivers:

- Increasing global prevalence of diabetes: The ever-growing number of diagnosed and undiagnosed diabetes cases worldwide creates a sustained and expanding demand for effective treatment devices.

- Technological advancements and innovation: Continuous development in areas like artificial intelligence, sensor technology, and miniaturization leads to more sophisticated, user-friendly, and effective devices.

- Growing awareness and patient empowerment: Patients are increasingly seeking active roles in managing their health, driving demand for advanced self-management tools.

- Favorable reimbursement policies and increasing healthcare expenditure: Governments and insurance providers are recognizing the long-term cost-effectiveness of advanced diabetes management, leading to better coverage for devices.

- Rising demand for homecare and remote monitoring solutions: The shift towards decentralized healthcare models encourages the adoption of devices that facilitate self-care and remote patient management.

Barriers & Challenges:

- High cost of advanced devices: The initial purchase price and ongoing costs associated with sophisticated devices like insulin pumps and CGM systems can be prohibitive for a significant portion of the population, especially in developing economies.

- Stringent regulatory approvals and lengthy clinical trials: The rigorous testing and approval processes for medical devices can delay market entry and increase R&D expenses for manufacturers.

- Limited access to healthcare infrastructure and trained professionals: In many regions, a lack of adequate healthcare facilities and trained personnel hinders the effective prescription, use, and support for complex diabetes treatment devices.

- Data privacy and security concerns: The increasing connectivity of diabetes devices raises concerns about the protection of sensitive patient health data, necessitating robust cybersecurity measures.

- User adoption and adherence challenges: Despite technological advancements, patient adherence can be a significant challenge due to the complexity of some devices, the need for regular maintenance, and lifestyle adjustments required. Supply chain disruptions and shortages of essential components can also impact product availability and lead to price fluctuations.

Emerging Opportunities in Diabetes Treatment Device

Emerging opportunities in the diabetes treatment device market lie in the development of affordable and accessible solutions for low- and middle-income countries, where the diabetes burden is rapidly increasing. The integration of AI and machine learning for predictive analytics and personalized treatment recommendations presents a significant avenue for growth, enabling proactive rather than reactive diabetes management. Furthermore, the expansion of non-invasive or minimally invasive glucose monitoring technologies holds immense potential to overcome current adoption barriers. Untapped markets in emerging economies, coupled with evolving consumer preferences for integrated digital health ecosystems that connect devices, wearables, and health platforms, offer substantial opportunities for market expansion and product diversification.

Growth Accelerators in the Diabetes Treatment Device Industry

The long-term growth of the diabetes treatment device industry is significantly propelled by groundbreaking technological breakthroughs, particularly in the realm of closed-loop artificial pancreas systems and novel sensor technologies for continuous glucose monitoring. Strategic partnerships and collaborations between device manufacturers, pharmaceutical giants like Sanofi and Novo Nordisk A/S, and technology companies are accelerating the development and integration of comprehensive diabetes management solutions. Market expansion strategies focused on penetrating underserved regions and addressing the unique needs of diverse patient populations, including pediatric and geriatric segments, are also crucial growth catalysts. The increasing focus on preventative care and early intervention further stimulates demand for accurate and accessible diagnostic and monitoring devices.

Key Players Shaping the Diabetes Treatment Device Market

- Roche

- Tandem Diabetes Care, Inc.

- B. Braun Melsungen AG

- Medtronic

- BD

- Novo Nordisk A/S

- Abbott

- Sanofi

Notable Milestones in Diabetes Treatment Device Sector

- 2019: Launch of next-generation smart insulin pens with advanced connectivity and data logging capabilities, enhancing patient tracking.

- 2020: Significant advancements in closed-loop insulin pump systems, leading to improved automated insulin delivery and reduced glycemic variability.

- 2021: Introduction of novel, longer-lasting insulin formulations that complement the use of advanced delivery devices.

- 2022: Increased adoption and market penetration of integrated continuous glucose monitoring (CGM) and insulin pump systems, offering a more holistic approach.

- 2023: Expansion of digital health platforms and mobile applications offering remote patient monitoring and telehealth integration for diabetes management.

- 2024: Growing focus on AI-driven predictive analytics for diabetes management, enabling proactive interventions and personalized treatment plans.

In-Depth Diabetes Treatment Device Market Outlook

The diabetes treatment device market is projected to witness sustained and robust growth, driven by ongoing technological innovation, an increasing global diabetes prevalence, and a growing emphasis on patient empowerment. The expansion of closed-loop systems, the development of more accurate and non-invasive monitoring technologies, and the integration of AI for personalized care are key growth accelerators that will redefine diabetes management in the coming years. Strategic partnerships and market penetration into emerging economies will further fuel this trajectory, creating significant opportunities for companies that can deliver innovative, accessible, and integrated solutions. The future market outlook is exceptionally promising, indicating a sustained demand for devices that enhance patient outcomes and improve the overall quality of life for individuals living with diabetes.

Diabetes Treatment Device Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Clinics

- 1.3. Homecare

-

2. Types

- 2.1. Insulin Pens

- 2.2. Insulin Pumps

- 2.3. Insulin Jet Injectors

- 2.4. Insulin Syringes

- 2.5. Others

Diabetes Treatment Device Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Diabetes Treatment Device Regional Market Share

Geographic Coverage of Diabetes Treatment Device

Diabetes Treatment Device REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Clinics

- 5.1.3. Homecare

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Insulin Pens

- 5.2.2. Insulin Pumps

- 5.2.3. Insulin Jet Injectors

- 5.2.4. Insulin Syringes

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Diabetes Treatment Device Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Clinics

- 6.1.3. Homecare

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Insulin Pens

- 6.2.2. Insulin Pumps

- 6.2.3. Insulin Jet Injectors

- 6.2.4. Insulin Syringes

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Diabetes Treatment Device Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Clinics

- 7.1.3. Homecare

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Insulin Pens

- 7.2.2. Insulin Pumps

- 7.2.3. Insulin Jet Injectors

- 7.2.4. Insulin Syringes

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Diabetes Treatment Device Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Clinics

- 8.1.3. Homecare

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Insulin Pens

- 8.2.2. Insulin Pumps

- 8.2.3. Insulin Jet Injectors

- 8.2.4. Insulin Syringes

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Diabetes Treatment Device Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Clinics

- 9.1.3. Homecare

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Insulin Pens

- 9.2.2. Insulin Pumps

- 9.2.3. Insulin Jet Injectors

- 9.2.4. Insulin Syringes

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Diabetes Treatment Device Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Clinics

- 10.1.3. Homecare

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Insulin Pens

- 10.2.2. Insulin Pumps

- 10.2.3. Insulin Jet Injectors

- 10.2.4. Insulin Syringes

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Diabetes Treatment Device Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals

- 11.1.2. Clinics

- 11.1.3. Homecare

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Insulin Pens

- 11.2.2. Insulin Pumps

- 11.2.3. Insulin Jet Injectors

- 11.2.4. Insulin Syringes

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Roche

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Tandem Diabetes Care

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Inc.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 B. Braun Melsungen AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Medtronic

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 BD

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Novo Nordisk A/S

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Abbott

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sanofi

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Roche

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Diabetes Treatment Device Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Diabetes Treatment Device Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Diabetes Treatment Device Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Diabetes Treatment Device Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Diabetes Treatment Device Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Diabetes Treatment Device Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Diabetes Treatment Device Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Diabetes Treatment Device Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Diabetes Treatment Device Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Diabetes Treatment Device Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Diabetes Treatment Device Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Diabetes Treatment Device Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Diabetes Treatment Device Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Diabetes Treatment Device Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Diabetes Treatment Device Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Diabetes Treatment Device Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Diabetes Treatment Device Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Diabetes Treatment Device Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Diabetes Treatment Device Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Diabetes Treatment Device Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Diabetes Treatment Device Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Diabetes Treatment Device Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Diabetes Treatment Device Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Diabetes Treatment Device Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Diabetes Treatment Device Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Diabetes Treatment Device Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Diabetes Treatment Device Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Diabetes Treatment Device Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Diabetes Treatment Device Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Diabetes Treatment Device Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Diabetes Treatment Device Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Diabetes Treatment Device Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Diabetes Treatment Device Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Diabetes Treatment Device Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Diabetes Treatment Device Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Diabetes Treatment Device Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Diabetes Treatment Device Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Diabetes Treatment Device Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Diabetes Treatment Device Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Diabetes Treatment Device Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Diabetes Treatment Device Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Diabetes Treatment Device Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Diabetes Treatment Device Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Diabetes Treatment Device Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Diabetes Treatment Device Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Diabetes Treatment Device Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Diabetes Treatment Device Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Diabetes Treatment Device Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Diabetes Treatment Device Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Diabetes Treatment Device Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diabetes Treatment Device?

The projected CAGR is approximately 6.3%.

2. Which companies are prominent players in the Diabetes Treatment Device?

Key companies in the market include Roche, Tandem Diabetes Care, Inc., B. Braun Melsungen AG, Medtronic, BD, Novo Nordisk A/S, Abbott, Sanofi.

3. What are the main segments of the Diabetes Treatment Device?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.34 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Diabetes Treatment Device," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Diabetes Treatment Device report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Diabetes Treatment Device?

To stay informed about further developments, trends, and reports in the Diabetes Treatment Device, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence