Key Insights into the Diabetic Neuropathy Market

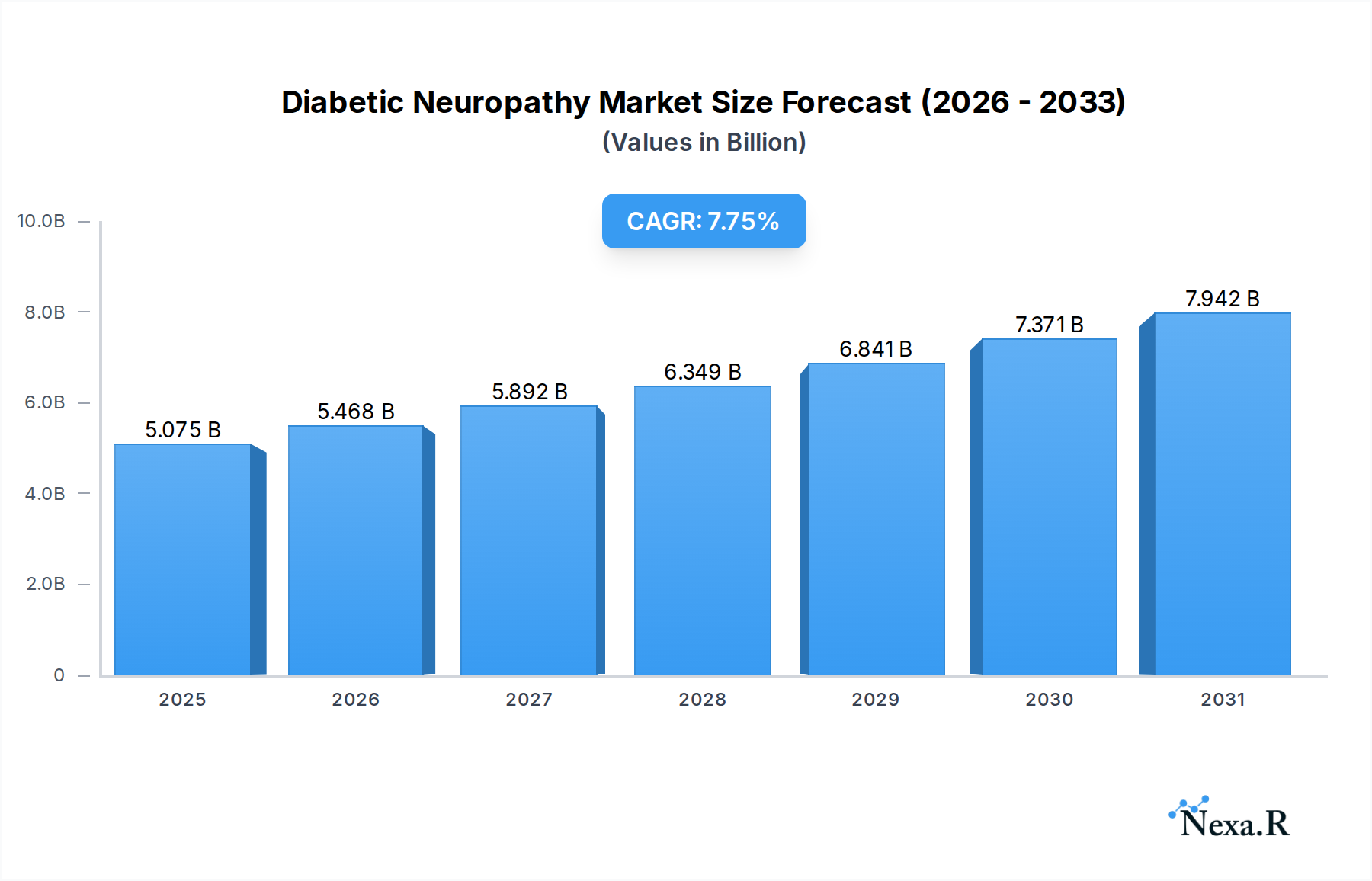

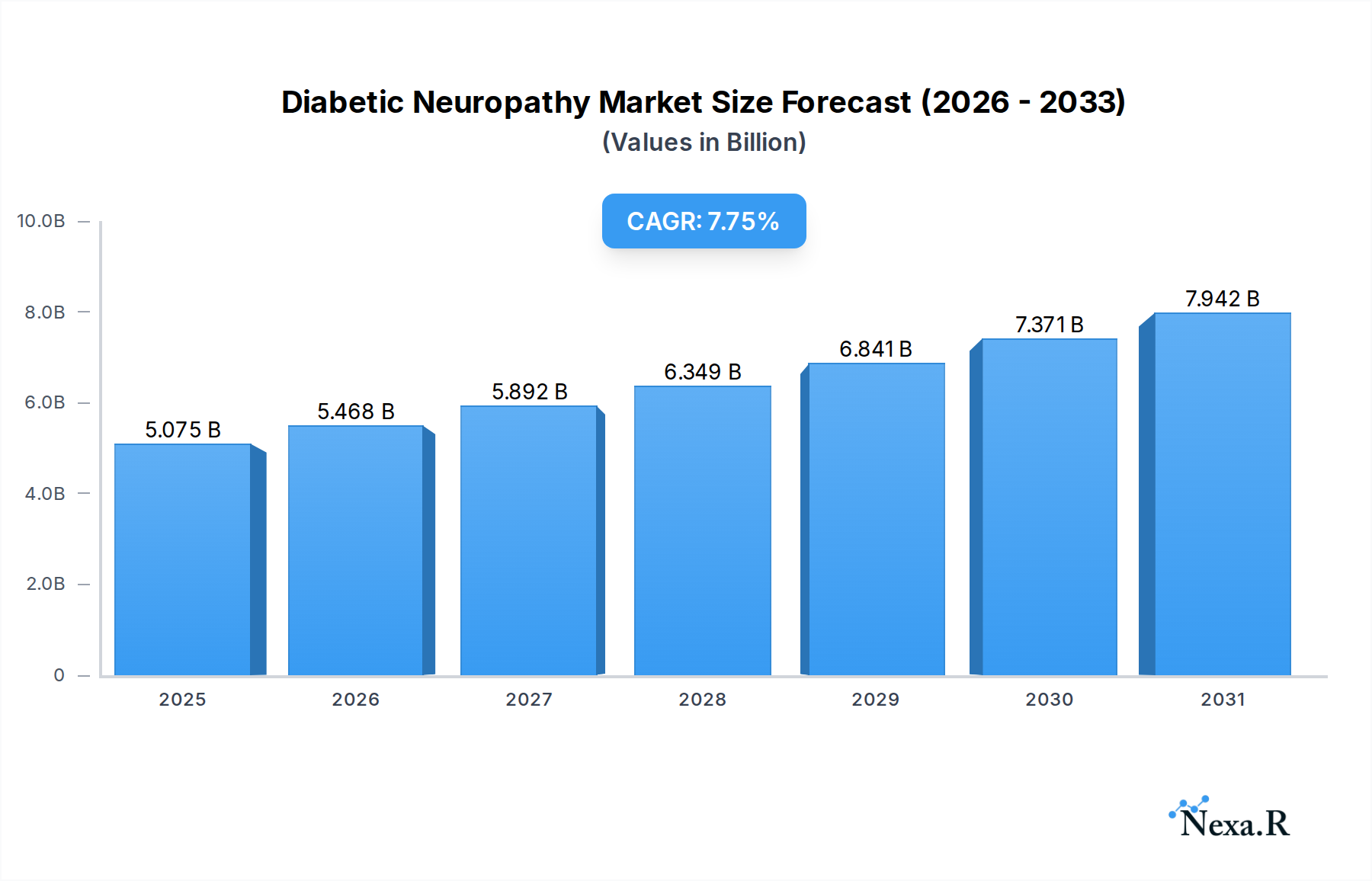

The global Diabetic Neuropathy Market was valued at an estimated $4.71 billion in 2024, poised for robust expansion with a projected Compound Annual Growth Rate (CAGR) of 7.75% through the forecast period. This significant growth trajectory is predominantly driven by the escalating global prevalence of diabetes, a chronic metabolic disorder that progressively leads to nerve damage, a condition medically termed diabetic neuropathy. The increasing aging population, which is more susceptible to long-term diabetic complications, further fuels demand for effective diagnostic and therapeutic solutions. Macroeconomic tailwinds such as improving healthcare infrastructure, particularly in emerging economies, and growing awareness among both patients and healthcare providers regarding early diagnosis and management of neuropathic symptoms are pivotal. Advancements in pharmaceutical research, focusing on novel drug targets and improved delivery systems, are also contributing to market expansion. The market outlook remains positive, underscored by the chronic nature of the disease, the significant unmet need for disease-modifying therapies, and the continuous innovation in pain management and neurological care. While symptomatic relief remains the cornerstone of current treatment strategies, the pipeline for therapies aimed at nerve regeneration and disease reversal is growing, promising a transformative shift in patient outcomes. North America currently holds a dominant share due to advanced healthcare systems and high patient awareness, whereas the Asia Pacific region is anticipated to exhibit the fastest growth, propelled by a vast diabetic population and increasing healthcare expenditure. Key therapeutic classes like Anticonvulsants Market and Serotonin-Norepinephrine Reuptake Inhibitors Market are critical components of the current treatment paradigm, addressing the debilitating neuropathic pain. The expanding reach of the Pharmaceuticals Market, in general, is a significant driver, supporting the development and commercialization of new treatments. The demand for targeted interventions across various end-user segments, including Diabetes Specialty Clinics Market, is accelerating, emphasizing integrated care models. Challenges such as the high cost of advanced treatments and side effect profiles of existing drugs persist, necessitating continued research into more efficacious and tolerable options.

Diabetic Neuropathy Market Size (In Billion)

The Peripheral Neuropathy Segment in Diabetic Neuropathy Market

The Peripheral Neuropathy segment is unequivocally the dominant disease type within the broader Diabetic Neuropathy Market, accounting for the largest share of revenue due to its high prevalence and direct impact on patients' quality of life. Peripheral neuropathy, affecting the nerves typically in the feet and hands, is the most common form of diabetic neuropathy, impacting up to 50% of individuals with long-standing diabetes. Its dominance is attributed to its early onset and significant symptomatic burden, including debilitating pain, numbness, tingling, and muscle weakness, which necessitate immediate medical intervention. The primary focus of the Diabetic Neuropathy Market, therefore, revolves heavily around managing the symptoms and progression of this specific manifestation. Treatment strategies for peripheral neuropathy are multifaceted, primarily involving pharmaceutical interventions aimed at pain management and glycemic control to slow disease progression. Within the pharmaceutical landscape, the Anticonvulsants Market plays a crucial role, with drugs like gabapentin and pregabalin being first-line agents for neuropathic pain. These medications work by modulating neuronal excitability, thereby reducing pain signals. Similarly, the Serotonin-Norepinephrine Reuptake Inhibitors Market (SNRIs), including duloxetine and venlafaxine, are widely prescribed for their dual action on both pain and mood, which is often affected in chronic pain conditions. The Tricyclic Antidepressants Market (TCAs), such as amitriptyline and nortriptyline, also hold a significant position, particularly in cases resistant to other treatments, despite their broader side-effect profiles. Key players such as Pfizer Inc. and Eli Lilly and Company are prominent in this segment, offering a range of these approved medications. The market dynamics for peripheral neuropathy treatments are characterized by a blend of established generic medications and ongoing innovation to develop novel compounds with improved efficacy and safety. The rising number of diagnosed cases, coupled with an increasing emphasis on proactive diabetes management, ensures sustained growth for therapies targeting peripheral neuropathy. Furthermore, the increasing accessibility of healthcare services through channels like the Online Pharmacies Market facilitates wider reach for these treatments, while specialized centers like the Diabetes Specialty Clinics Market are crucial for comprehensive diagnosis and ongoing management, ensuring that patients receive tailored care and support to manage this chronic condition effectively.

Diabetic Neuropathy Company Market Share

Advancements in Therapeutics and Diagnostics Driving Diabetic Neuropathy Market

The Diabetic Neuropathy Market is significantly shaped by a confluence of demand drivers and enduring constraints. A primary driver is the burgeoning global prevalence of diabetes itself. According to recent epidemiological studies, the number of adults living with diabetes is projected to increase substantially over the next decade, with a corresponding rise in complications such as neuropathy. This demographic shift provides a vast and expanding patient pool requiring treatment. Secondly, advancements in therapeutic modalities have been instrumental. The focus has been on developing more effective pain management solutions, with a shift towards non-opioid options to mitigate addiction risks. New drug approvals, enhanced formulations, and combination therapies are improving treatment efficacy. The underlying Active Pharmaceutical Ingredients Market is pivotal here, enabling the synthesis of complex molecules that form the basis of these advanced drugs. Furthermore, the growing awareness among both healthcare professionals and patients regarding the importance of early diagnosis and proactive management of diabetic neuropathy is a key accelerator. Public health campaigns and better screening protocols are leading to earlier detection, preventing more severe complications. Technological innovations also serve as a crucial driver. The integration of advanced diagnostic tools, such as quantitative sensory testing and nerve conduction studies, allows for more precise assessment of nerve damage. Concurrently, the Pain Management Devices Market and the Neuromodulation Devices Market are contributing with non-pharmacological interventions like spinal cord stimulators and transcutaneous electrical nerve stimulation (TENS) units, offering alternative or adjunct therapies for intractable pain. Despite these drivers, several constraints impede market growth. The high cost associated with novel treatments, coupled with variable reimbursement policies, creates significant access barriers, especially in developing regions. Moreover, the side effect profiles of existing pharmacological therapies, which can range from gastrointestinal issues to cognitive impairment, often lead to patient non-adherence. A persistent challenge is the lack of truly disease-modifying drugs that can halt or reverse nerve damage, leaving current treatments primarily symptomatic. Addressing these constraints through innovative R&D and accessible healthcare policies will be crucial for unlocking the full potential of the Diabetic Neuropathy Market.

Competitive Ecosystem of Diabetic Neuropathy Market

The competitive landscape of the Diabetic Neuropathy Market is characterized by the presence of a mix of large multinational pharmaceutical companies, specialized device manufacturers, and emerging biopharmaceutical firms. Innovation in drug development, advanced diagnostics, and non-pharmacological interventions are key battlegrounds.

- Abbott: A diversified healthcare company, Abbott focuses on diagnostics and medical devices which are crucial for early detection and management of diabetic complications, including neuropathy. Their diagnostic platforms play a significant role in assessing nerve damage and monitoring disease progression.

- Johnson & Johnson: A global pharmaceutical and medical device giant, J&J has a broad portfolio that includes treatments for pain management and neurological conditions, with ongoing R&D in related areas and contributions to general diabetes care.

- Boehringer Ingelheim GmbH: This research-driven pharmaceutical company is active in various therapeutic areas, including diabetes and its complications, contributing to the understanding and treatment of associated neuropathies through its robust drug development pipeline.

- NeuroMetrix, Inc.: A medical device company specializing in diagnostic and therapeutic solutions for neurological conditions, NeuroMetrix provides technologies specifically for the assessment and management of neuropathic pain, offering unique tools for diagnosis and monitoring.

- Eli Lilly and Company: A major player in the diabetes care sector, Eli Lilly has a strong pipeline and existing medications for diabetes, often extending their focus to managing associated complications like neuropathy through integrated solutions.

- GlaxoSmithKline plc: GSK is a global biopharmaceutical company with a presence in pain management and neurological disorders, investing in research for novel approaches to chronic pain, including neuropathic pain, and contributing to patient education.

- Lupin Limited: An Indian multinational pharmaceutical company, Lupin is involved in the development and manufacturing of a wide range of generic and branded formulations, including those for pain and neurological conditions, enhancing access to affordable treatments.

- Pfizer Inc.: A leading global pharmaceutical company, Pfizer is well-known for its contributions to pain management, offering several key medications used in the symptomatic treatment of diabetic neuropathy, holding a strong position in the segment.

- Astellas Pharma Inc.: A Japanese pharmaceutical company with a focus on therapeutic areas including pain and urology, Astellas may have drugs that address specific symptoms or complications of diabetic neuropathy, diversifying the therapeutic options.

- Glenmark Pharmaceuticals Ltd.: Another Indian pharmaceutical company, Glenmark focuses on discovery and development of new chemical entities and generic products, with a portfolio spanning various therapeutic segments, including pain management.

- Arbor Pharmaceuticals, LLC: A specialty pharmaceutical company, Arbor often targets specific therapeutic niches, potentially including products for pain or neurological conditions relevant to diabetic neuropathy, catering to specific patient populations.

- Depomed, Inc.: Formerly focused on pain and neurological disorders, Depomed developed treatments for chronic pain conditions, including those related to neuropathy, contributing to the pharmacological management of symptoms.

Recent Developments & Milestones in Diabetic Neuropathy Market

The dynamic landscape of the Diabetic Neuropathy Market is continuously evolving with strategic advancements aimed at improving patient care and treatment outcomes. These developments reflect a concerted effort to address the significant unmet needs within this patient population:

- Q4 2023: Introduction of novel non-opioid analgesic formulations for neuropathic pain by a leading pharmaceutical entity, marking a pivotal step towards safer and more effective chronic pain management and reducing reliance on traditional opioid therapies.

- Q3 2023: Strategic partnerships were forged between medical device manufacturers and pharmaceutical companies, aimed at integrating advanced diagnostics with targeted therapeutic interventions, fostering a holistic approach to disease management.

- Q1 2024: Launch of a global patient education campaign focusing on early detection and comprehensive management strategies for diabetic neuropathy, supported by prominent diabetes associations, significantly increasing public awareness and promoting timely intervention.

- Q2 2024: Regulatory approval was granted for a new sustained-release drug delivery system, designed to improve patient adherence and reduce systemic side effects in diabetic neuropathy treatment, enhancing the safety and convenience profile of existing drugs.

- Q4 2024: Increased R&D investment by biotechnology firms into gene therapies and stem cell-based treatments targeting nerve regeneration for advanced cases of diabetic neuropathy, signaling a future shift towards potentially disease-reversing therapies.

- Q1 2025: Expansion of telehealth services for chronic pain management, enabling remote monitoring and prescription adjustments for patients in the Diabetic Neuropathy Market, significantly improving access to specialized care, especially in underserved areas.

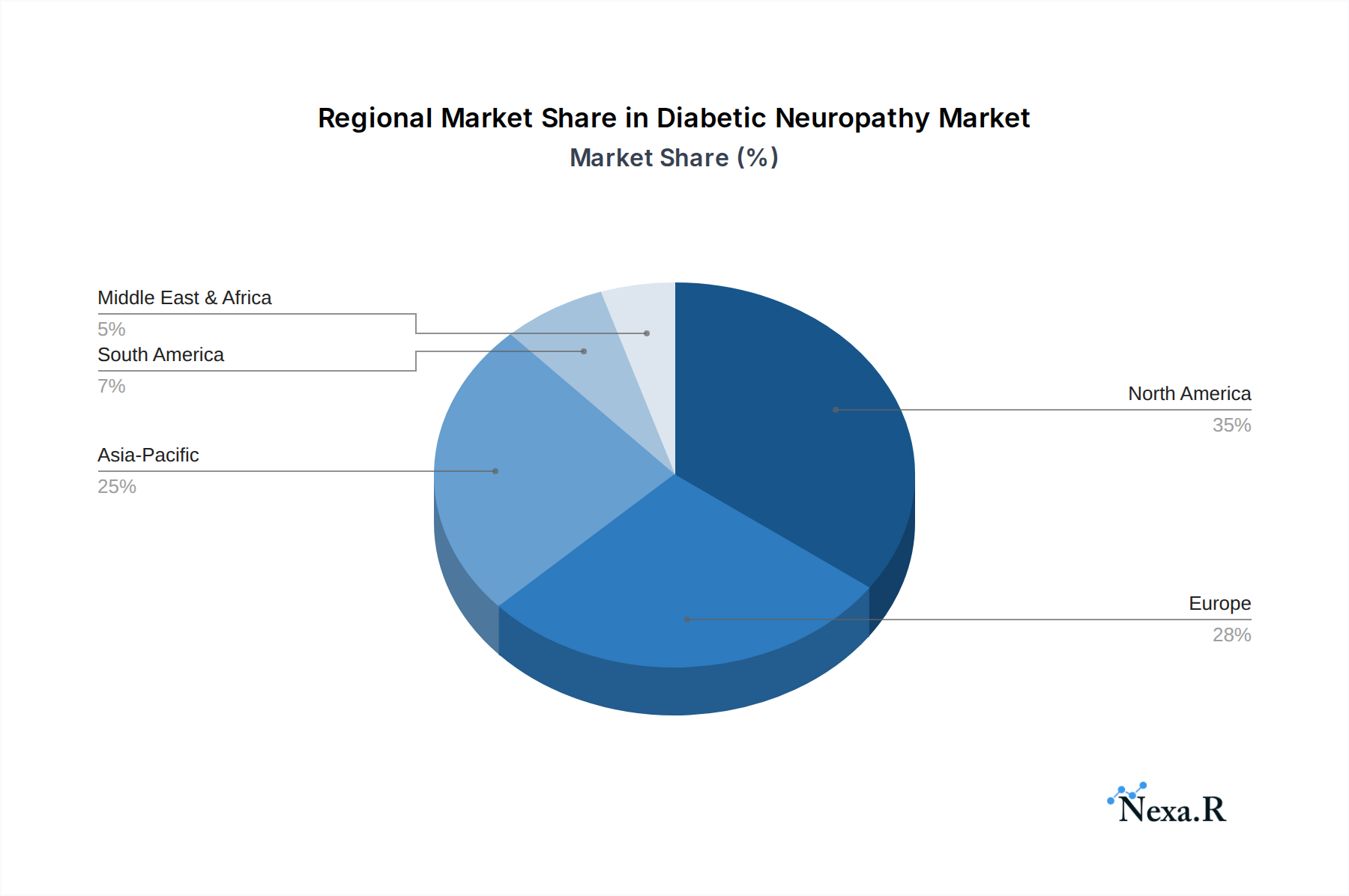

Regional Market Breakdown for Diabetic Neuropathy Market

The global Diabetic Neuropathy Market exhibits significant regional variations in terms of market size, growth drivers, and demand patterns. Analyzing these regional dynamics is crucial for understanding the market's overall trajectory.

North America holds the largest revenue share in the Diabetic Neuropathy Market. This dominance is primarily attributed to a high prevalence of diabetes, well-established healthcare infrastructure, high awareness among the populace and healthcare providers, and robust reimbursement policies for diagnostic tests and therapeutic interventions. The presence of key market players and a strong focus on R&D for novel treatments further solidify its leading position. The region demonstrates a moderate CAGR, reflecting its mature market status but continuous innovation and patient demand.

Europe represents another substantial market for diabetic neuropathy treatments. Countries like Germany, the UK, and France are significant contributors, characterized by advanced healthcare systems and a considerable aging population with a high incidence of diabetes. Stringent regulatory frameworks ensure high-quality therapeutic options, and a strong emphasis on evidence-based medicine drives the adoption of effective treatments. However, market growth in Europe is generally slower compared to emerging economies, reflecting its maturity.

Asia Pacific is projected to be the fastest-growing region in the Diabetic Neuropathy Market. This rapid expansion is fueled by an enormous and rapidly growing diabetic population, particularly in countries like China and India. Improving economic conditions, increasing healthcare expenditure, and the expansion of healthcare access, including the development of new Diabetes Specialty Clinics Market and the proliferation of Online Pharmacies Market, are key drivers. While per capita spending on advanced treatments may be lower than in Western nations, the sheer volume of patients and increasing awareness present immense growth opportunities.

Middle East & Africa is an emerging market with substantial growth potential. The region faces a rapidly increasing burden of diabetes, particularly in the GCC countries. Investment in healthcare infrastructure is on the rise, and growing health awareness is leading to better diagnosis rates. However, challenges such as limited access to specialized care in some areas and varying reimbursement landscapes can hinder market penetration.

South America also contributes to the global market, with Brazil and Argentina being key countries. The region is witnessing growing awareness of diabetic complications and increasing access to modern medical treatments. However, economic instabilities and disparities in healthcare access across different regions within the continent can influence market growth and product adoption.

Diabetic Neuropathy Regional Market Share

Investment & Funding Activity in Diabetic Neuropathy Market

Investment and funding activity within the Diabetic Neuropathy Market has shown a consistent upward trend over the past 2-3 years, reflecting growing confidence in addressing this chronic and debilitating condition. Venture funding rounds have primarily targeted startups and biotechnology firms engaged in developing novel therapeutic compounds, especially those exploring non-opioid analgesics and regenerative medicine approaches. Sub-segments attracting the most capital include therapies for pain management with fewer side effects, as well as diagnostic tools that enable earlier and more precise detection of nerve damage. For instance, companies innovating in small fiber neuropathy diagnostics or developing bio-marker driven prognostics have seen considerable seed and Series A funding. Strategic partnerships and collaborations between large pharmaceutical companies and smaller biotech entities are also prevalent. These alliances often aim to leverage the innovative research of startups with the extensive R&D, clinical trial, and commercialization capabilities of established players. Mergers and acquisitions, while not as frequent as venture rounds, have occurred, typically involving larger entities acquiring promising therapeutic assets or specialized technology platforms that complement their existing portfolios in pain management or diabetes care. The rationale behind this increased capital inflow is multifaceted: the large and expanding patient population, the significant unmet need for disease-modifying therapies, and the potential for substantial market returns from successful product development. Furthermore, the global Pharmaceuticals Market views diabetic neuropathy as a high-priority area due to its impact on patient quality of life and healthcare costs, driving sustained investment in research and development.

Pricing Dynamics & Margin Pressure in Diabetic Neuropathy Market

The pricing dynamics in the Diabetic Neuropathy Market are complex, influenced by a blend of innovation, competition, and regulatory pressures. Average Selling Prices (ASPs) for novel, branded pharmacological treatments for neuropathic pain tend to be high, reflecting the substantial R&D investments and the value proposition of improved efficacy or reduced side effects. These premium prices support robust margin structures for innovative pharmaceutical companies, especially during patent exclusivity periods. However, the market also experiences significant margin pressure from generic drug manufacturers. As patents expire for established medications like specific anticonvulsants or SNRIs, generic versions enter the market at substantially lower price points, leading to a rapid erosion of ASPs and intense competition. This dynamic directly impacts the Anticonvulsants Market and the Serotonin-Norepinephrine Reuptake Inhibitors Market, where generic penetration is high. Key cost levers across the value chain include the cost of Active Pharmaceutical Ingredients Market, which can fluctuate based on supply chain dynamics and geopolitical factors, impacting manufacturing costs. Clinical trial expenses, regulatory approval costs, and marketing efforts also contribute significantly to the overall cost structure. Competitive intensity is heightened by the presence of multiple therapeutic options and the constant influx of new entrants, particularly in the non-pharmacological segment such as the Pain Management Devices Market. Healthcare payers and governments increasingly negotiate for lower prices, further constraining margins. Moreover, the long-term, chronic nature of diabetic neuropathy means that treatment costs are sustained over many years, making affordability a critical factor. The overall Pharmaceuticals Market trends, including the drive towards value-based care and pressure on drug prices, inevitably cascade down to the Diabetic Neuropathy Market, forcing companies to innovate continuously while optimizing their cost structures to maintain profitability.

Diabetic Neuropathy Segmentation

-

1. Drug Type

- 1.1. Anticonvulsants

- 1.2. Serotonin-Norepinephrine Reuptake Inhibitors (SNRIs)

- 1.3. Tricyclic Antidepressants (TCAs)

- 1.4. Opioid Analgesics

- 1.5. Others

-

2. Disease Type

- 2.1. Peripheral Neuropathy

- 2.2. Autonomic Neuropathy

- 2.3. Proximal Neuropathy

- 2.4. Focal Neuropathy

-

3. Route of Administration

- 3.1. Oral

- 3.2. Injectable

- 3.3. Topical

-

4. Distribution Channel

- 4.1. Hospital Pharmacies

- 4.2. Retail Pharmacies

- 4.3. Online Pharmacies

-

5. End User

- 5.1. Hospitals

- 5.2. Diabetes Specialty Clinics

- 5.3. Neurology Clinics

- 5.4. Academic Research Centers

- 5.5. Others

Diabetic Neuropathy Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Diabetic Neuropathy Regional Market Share

Geographic Coverage of Diabetic Neuropathy

Diabetic Neuropathy REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.75% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Drug Type

- 5.1.1. Anticonvulsants

- 5.1.2. Serotonin-Norepinephrine Reuptake Inhibitors (SNRIs)

- 5.1.3. Tricyclic Antidepressants (TCAs)

- 5.1.4. Opioid Analgesics

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Disease Type

- 5.2.1. Peripheral Neuropathy

- 5.2.2. Autonomic Neuropathy

- 5.2.3. Proximal Neuropathy

- 5.2.4. Focal Neuropathy

- 5.3. Market Analysis, Insights and Forecast - by Route of Administration

- 5.3.1. Oral

- 5.3.2. Injectable

- 5.3.3. Topical

- 5.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.4.1. Hospital Pharmacies

- 5.4.2. Retail Pharmacies

- 5.4.3. Online Pharmacies

- 5.5. Market Analysis, Insights and Forecast - by End User

- 5.5.1. Hospitals

- 5.5.2. Diabetes Specialty Clinics

- 5.5.3. Neurology Clinics

- 5.5.4. Academic Research Centers

- 5.5.5. Others

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Drug Type

- 6. Global Diabetic Neuropathy Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Drug Type

- 6.1.1. Anticonvulsants

- 6.1.2. Serotonin-Norepinephrine Reuptake Inhibitors (SNRIs)

- 6.1.3. Tricyclic Antidepressants (TCAs)

- 6.1.4. Opioid Analgesics

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Disease Type

- 6.2.1. Peripheral Neuropathy

- 6.2.2. Autonomic Neuropathy

- 6.2.3. Proximal Neuropathy

- 6.2.4. Focal Neuropathy

- 6.3. Market Analysis, Insights and Forecast - by Route of Administration

- 6.3.1. Oral

- 6.3.2. Injectable

- 6.3.3. Topical

- 6.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.4.1. Hospital Pharmacies

- 6.4.2. Retail Pharmacies

- 6.4.3. Online Pharmacies

- 6.5. Market Analysis, Insights and Forecast - by End User

- 6.5.1. Hospitals

- 6.5.2. Diabetes Specialty Clinics

- 6.5.3. Neurology Clinics

- 6.5.4. Academic Research Centers

- 6.5.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Drug Type

- 7. North America Diabetic Neuropathy Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Drug Type

- 7.1.1. Anticonvulsants

- 7.1.2. Serotonin-Norepinephrine Reuptake Inhibitors (SNRIs)

- 7.1.3. Tricyclic Antidepressants (TCAs)

- 7.1.4. Opioid Analgesics

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Disease Type

- 7.2.1. Peripheral Neuropathy

- 7.2.2. Autonomic Neuropathy

- 7.2.3. Proximal Neuropathy

- 7.2.4. Focal Neuropathy

- 7.3. Market Analysis, Insights and Forecast - by Route of Administration

- 7.3.1. Oral

- 7.3.2. Injectable

- 7.3.3. Topical

- 7.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.4.1. Hospital Pharmacies

- 7.4.2. Retail Pharmacies

- 7.4.3. Online Pharmacies

- 7.5. Market Analysis, Insights and Forecast - by End User

- 7.5.1. Hospitals

- 7.5.2. Diabetes Specialty Clinics

- 7.5.3. Neurology Clinics

- 7.5.4. Academic Research Centers

- 7.5.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Drug Type

- 8. South America Diabetic Neuropathy Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Drug Type

- 8.1.1. Anticonvulsants

- 8.1.2. Serotonin-Norepinephrine Reuptake Inhibitors (SNRIs)

- 8.1.3. Tricyclic Antidepressants (TCAs)

- 8.1.4. Opioid Analgesics

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Disease Type

- 8.2.1. Peripheral Neuropathy

- 8.2.2. Autonomic Neuropathy

- 8.2.3. Proximal Neuropathy

- 8.2.4. Focal Neuropathy

- 8.3. Market Analysis, Insights and Forecast - by Route of Administration

- 8.3.1. Oral

- 8.3.2. Injectable

- 8.3.3. Topical

- 8.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.4.1. Hospital Pharmacies

- 8.4.2. Retail Pharmacies

- 8.4.3. Online Pharmacies

- 8.5. Market Analysis, Insights and Forecast - by End User

- 8.5.1. Hospitals

- 8.5.2. Diabetes Specialty Clinics

- 8.5.3. Neurology Clinics

- 8.5.4. Academic Research Centers

- 8.5.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Drug Type

- 9. Europe Diabetic Neuropathy Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Drug Type

- 9.1.1. Anticonvulsants

- 9.1.2. Serotonin-Norepinephrine Reuptake Inhibitors (SNRIs)

- 9.1.3. Tricyclic Antidepressants (TCAs)

- 9.1.4. Opioid Analgesics

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Disease Type

- 9.2.1. Peripheral Neuropathy

- 9.2.2. Autonomic Neuropathy

- 9.2.3. Proximal Neuropathy

- 9.2.4. Focal Neuropathy

- 9.3. Market Analysis, Insights and Forecast - by Route of Administration

- 9.3.1. Oral

- 9.3.2. Injectable

- 9.3.3. Topical

- 9.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.4.1. Hospital Pharmacies

- 9.4.2. Retail Pharmacies

- 9.4.3. Online Pharmacies

- 9.5. Market Analysis, Insights and Forecast - by End User

- 9.5.1. Hospitals

- 9.5.2. Diabetes Specialty Clinics

- 9.5.3. Neurology Clinics

- 9.5.4. Academic Research Centers

- 9.5.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Drug Type

- 10. Middle East & Africa Diabetic Neuropathy Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Drug Type

- 10.1.1. Anticonvulsants

- 10.1.2. Serotonin-Norepinephrine Reuptake Inhibitors (SNRIs)

- 10.1.3. Tricyclic Antidepressants (TCAs)

- 10.1.4. Opioid Analgesics

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Disease Type

- 10.2.1. Peripheral Neuropathy

- 10.2.2. Autonomic Neuropathy

- 10.2.3. Proximal Neuropathy

- 10.2.4. Focal Neuropathy

- 10.3. Market Analysis, Insights and Forecast - by Route of Administration

- 10.3.1. Oral

- 10.3.2. Injectable

- 10.3.3. Topical

- 10.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.4.1. Hospital Pharmacies

- 10.4.2. Retail Pharmacies

- 10.4.3. Online Pharmacies

- 10.5. Market Analysis, Insights and Forecast - by End User

- 10.5.1. Hospitals

- 10.5.2. Diabetes Specialty Clinics

- 10.5.3. Neurology Clinics

- 10.5.4. Academic Research Centers

- 10.5.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Drug Type

- 11. Asia Pacific Diabetic Neuropathy Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Drug Type

- 11.1.1. Anticonvulsants

- 11.1.2. Serotonin-Norepinephrine Reuptake Inhibitors (SNRIs)

- 11.1.3. Tricyclic Antidepressants (TCAs)

- 11.1.4. Opioid Analgesics

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Disease Type

- 11.2.1. Peripheral Neuropathy

- 11.2.2. Autonomic Neuropathy

- 11.2.3. Proximal Neuropathy

- 11.2.4. Focal Neuropathy

- 11.3. Market Analysis, Insights and Forecast - by Route of Administration

- 11.3.1. Oral

- 11.3.2. Injectable

- 11.3.3. Topical

- 11.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.4.1. Hospital Pharmacies

- 11.4.2. Retail Pharmacies

- 11.4.3. Online Pharmacies

- 11.5. Market Analysis, Insights and Forecast - by End User

- 11.5.1. Hospitals

- 11.5.2. Diabetes Specialty Clinics

- 11.5.3. Neurology Clinics

- 11.5.4. Academic Research Centers

- 11.5.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Drug Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Abbott

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Johnson & Johnson

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Boehringer Ingelheim GmbH

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 NeuroMetrix Inc.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Eli Lilly and Company

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 GlaxoSmithKline plc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Lupin Limited

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Pfizer Inc.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Astellas Pharma Inc.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Glenmark Pharmaceuticals Ltd.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Arbor Pharmaceuticals LLC

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Depomed Inc.

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Others

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Abbott

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Diabetic Neuropathy Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Diabetic Neuropathy Revenue (billion), by Drug Type 2025 & 2033

- Figure 3: North America Diabetic Neuropathy Revenue Share (%), by Drug Type 2025 & 2033

- Figure 4: North America Diabetic Neuropathy Revenue (billion), by Disease Type 2025 & 2033

- Figure 5: North America Diabetic Neuropathy Revenue Share (%), by Disease Type 2025 & 2033

- Figure 6: North America Diabetic Neuropathy Revenue (billion), by Route of Administration 2025 & 2033

- Figure 7: North America Diabetic Neuropathy Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 8: North America Diabetic Neuropathy Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 9: North America Diabetic Neuropathy Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America Diabetic Neuropathy Revenue (billion), by End User 2025 & 2033

- Figure 11: North America Diabetic Neuropathy Revenue Share (%), by End User 2025 & 2033

- Figure 12: North America Diabetic Neuropathy Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Diabetic Neuropathy Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Diabetic Neuropathy Revenue (billion), by Drug Type 2025 & 2033

- Figure 15: South America Diabetic Neuropathy Revenue Share (%), by Drug Type 2025 & 2033

- Figure 16: South America Diabetic Neuropathy Revenue (billion), by Disease Type 2025 & 2033

- Figure 17: South America Diabetic Neuropathy Revenue Share (%), by Disease Type 2025 & 2033

- Figure 18: South America Diabetic Neuropathy Revenue (billion), by Route of Administration 2025 & 2033

- Figure 19: South America Diabetic Neuropathy Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 20: South America Diabetic Neuropathy Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 21: South America Diabetic Neuropathy Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 22: South America Diabetic Neuropathy Revenue (billion), by End User 2025 & 2033

- Figure 23: South America Diabetic Neuropathy Revenue Share (%), by End User 2025 & 2033

- Figure 24: South America Diabetic Neuropathy Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Diabetic Neuropathy Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Diabetic Neuropathy Revenue (billion), by Drug Type 2025 & 2033

- Figure 27: Europe Diabetic Neuropathy Revenue Share (%), by Drug Type 2025 & 2033

- Figure 28: Europe Diabetic Neuropathy Revenue (billion), by Disease Type 2025 & 2033

- Figure 29: Europe Diabetic Neuropathy Revenue Share (%), by Disease Type 2025 & 2033

- Figure 30: Europe Diabetic Neuropathy Revenue (billion), by Route of Administration 2025 & 2033

- Figure 31: Europe Diabetic Neuropathy Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 32: Europe Diabetic Neuropathy Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 33: Europe Diabetic Neuropathy Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 34: Europe Diabetic Neuropathy Revenue (billion), by End User 2025 & 2033

- Figure 35: Europe Diabetic Neuropathy Revenue Share (%), by End User 2025 & 2033

- Figure 36: Europe Diabetic Neuropathy Revenue (billion), by Country 2025 & 2033

- Figure 37: Europe Diabetic Neuropathy Revenue Share (%), by Country 2025 & 2033

- Figure 38: Middle East & Africa Diabetic Neuropathy Revenue (billion), by Drug Type 2025 & 2033

- Figure 39: Middle East & Africa Diabetic Neuropathy Revenue Share (%), by Drug Type 2025 & 2033

- Figure 40: Middle East & Africa Diabetic Neuropathy Revenue (billion), by Disease Type 2025 & 2033

- Figure 41: Middle East & Africa Diabetic Neuropathy Revenue Share (%), by Disease Type 2025 & 2033

- Figure 42: Middle East & Africa Diabetic Neuropathy Revenue (billion), by Route of Administration 2025 & 2033

- Figure 43: Middle East & Africa Diabetic Neuropathy Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 44: Middle East & Africa Diabetic Neuropathy Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 45: Middle East & Africa Diabetic Neuropathy Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: Middle East & Africa Diabetic Neuropathy Revenue (billion), by End User 2025 & 2033

- Figure 47: Middle East & Africa Diabetic Neuropathy Revenue Share (%), by End User 2025 & 2033

- Figure 48: Middle East & Africa Diabetic Neuropathy Revenue (billion), by Country 2025 & 2033

- Figure 49: Middle East & Africa Diabetic Neuropathy Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Diabetic Neuropathy Revenue (billion), by Drug Type 2025 & 2033

- Figure 51: Asia Pacific Diabetic Neuropathy Revenue Share (%), by Drug Type 2025 & 2033

- Figure 52: Asia Pacific Diabetic Neuropathy Revenue (billion), by Disease Type 2025 & 2033

- Figure 53: Asia Pacific Diabetic Neuropathy Revenue Share (%), by Disease Type 2025 & 2033

- Figure 54: Asia Pacific Diabetic Neuropathy Revenue (billion), by Route of Administration 2025 & 2033

- Figure 55: Asia Pacific Diabetic Neuropathy Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 56: Asia Pacific Diabetic Neuropathy Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 57: Asia Pacific Diabetic Neuropathy Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 58: Asia Pacific Diabetic Neuropathy Revenue (billion), by End User 2025 & 2033

- Figure 59: Asia Pacific Diabetic Neuropathy Revenue Share (%), by End User 2025 & 2033

- Figure 60: Asia Pacific Diabetic Neuropathy Revenue (billion), by Country 2025 & 2033

- Figure 61: Asia Pacific Diabetic Neuropathy Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Diabetic Neuropathy Revenue billion Forecast, by Drug Type 2020 & 2033

- Table 2: Global Diabetic Neuropathy Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 3: Global Diabetic Neuropathy Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 4: Global Diabetic Neuropathy Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global Diabetic Neuropathy Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Diabetic Neuropathy Revenue billion Forecast, by Region 2020 & 2033

- Table 7: Global Diabetic Neuropathy Revenue billion Forecast, by Drug Type 2020 & 2033

- Table 8: Global Diabetic Neuropathy Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 9: Global Diabetic Neuropathy Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 10: Global Diabetic Neuropathy Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 11: Global Diabetic Neuropathy Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Diabetic Neuropathy Revenue billion Forecast, by Country 2020 & 2033

- Table 13: United States Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Canada Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Mexico Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Diabetic Neuropathy Revenue billion Forecast, by Drug Type 2020 & 2033

- Table 17: Global Diabetic Neuropathy Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 18: Global Diabetic Neuropathy Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 19: Global Diabetic Neuropathy Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 20: Global Diabetic Neuropathy Revenue billion Forecast, by End User 2020 & 2033

- Table 21: Global Diabetic Neuropathy Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Brazil Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Argentina Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Rest of South America Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Global Diabetic Neuropathy Revenue billion Forecast, by Drug Type 2020 & 2033

- Table 26: Global Diabetic Neuropathy Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 27: Global Diabetic Neuropathy Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 28: Global Diabetic Neuropathy Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 29: Global Diabetic Neuropathy Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global Diabetic Neuropathy Revenue billion Forecast, by Country 2020 & 2033

- Table 31: United Kingdom Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Germany Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: France Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Italy Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Spain Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Russia Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Benelux Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Nordics Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of Europe Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Global Diabetic Neuropathy Revenue billion Forecast, by Drug Type 2020 & 2033

- Table 41: Global Diabetic Neuropathy Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 42: Global Diabetic Neuropathy Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 43: Global Diabetic Neuropathy Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 44: Global Diabetic Neuropathy Revenue billion Forecast, by End User 2020 & 2033

- Table 45: Global Diabetic Neuropathy Revenue billion Forecast, by Country 2020 & 2033

- Table 46: Turkey Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Israel Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: GCC Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 49: North Africa Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: South Africa Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East & Africa Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Global Diabetic Neuropathy Revenue billion Forecast, by Drug Type 2020 & 2033

- Table 53: Global Diabetic Neuropathy Revenue billion Forecast, by Disease Type 2020 & 2033

- Table 54: Global Diabetic Neuropathy Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 55: Global Diabetic Neuropathy Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 56: Global Diabetic Neuropathy Revenue billion Forecast, by End User 2020 & 2033

- Table 57: Global Diabetic Neuropathy Revenue billion Forecast, by Country 2020 & 2033

- Table 58: China Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 59: India Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: Japan Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 61: South Korea Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: ASEAN Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 63: Oceania Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Rest of Asia Pacific Diabetic Neuropathy Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diabetic Neuropathy?

The projected CAGR is approximately 7.75%.

2. Which companies are prominent players in the Diabetic Neuropathy?

Key companies in the market include Abbott, Johnson & Johnson, Boehringer Ingelheim GmbH, NeuroMetrix, Inc., Eli Lilly and Company, GlaxoSmithKline plc, Lupin Limited, Pfizer Inc., Astellas Pharma Inc., Glenmark Pharmaceuticals Ltd., Arbor Pharmaceuticals, LLC, Depomed, Inc., Others.

3. What are the main segments of the Diabetic Neuropathy?

The market segments include Drug Type, Disease Type, Route of Administration, Distribution Channel, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.71 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Diabetic Neuropathy," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Diabetic Neuropathy report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Diabetic Neuropathy?

To stay informed about further developments, trends, and reports in the Diabetic Neuropathy, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence