Key Insights

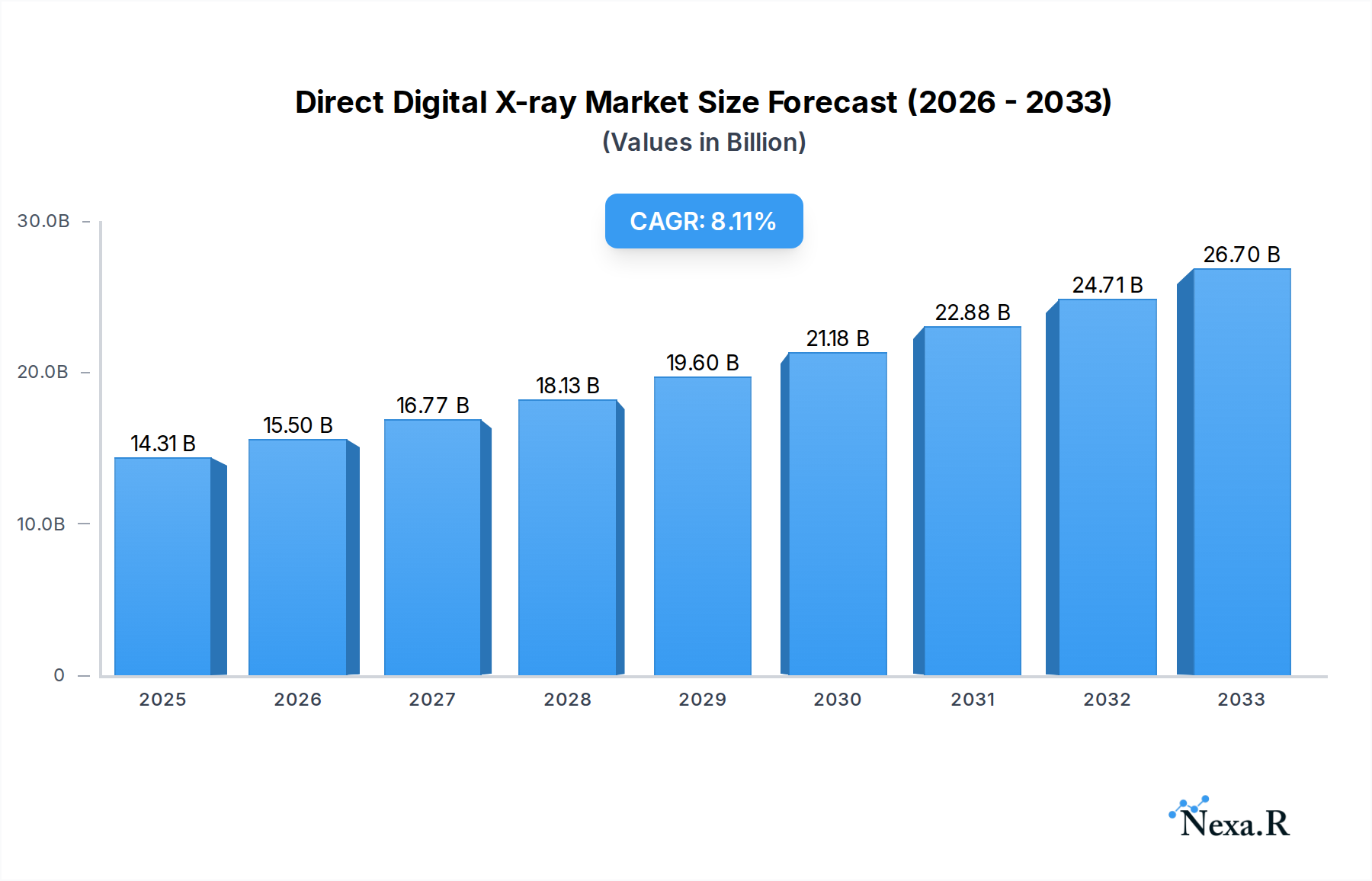

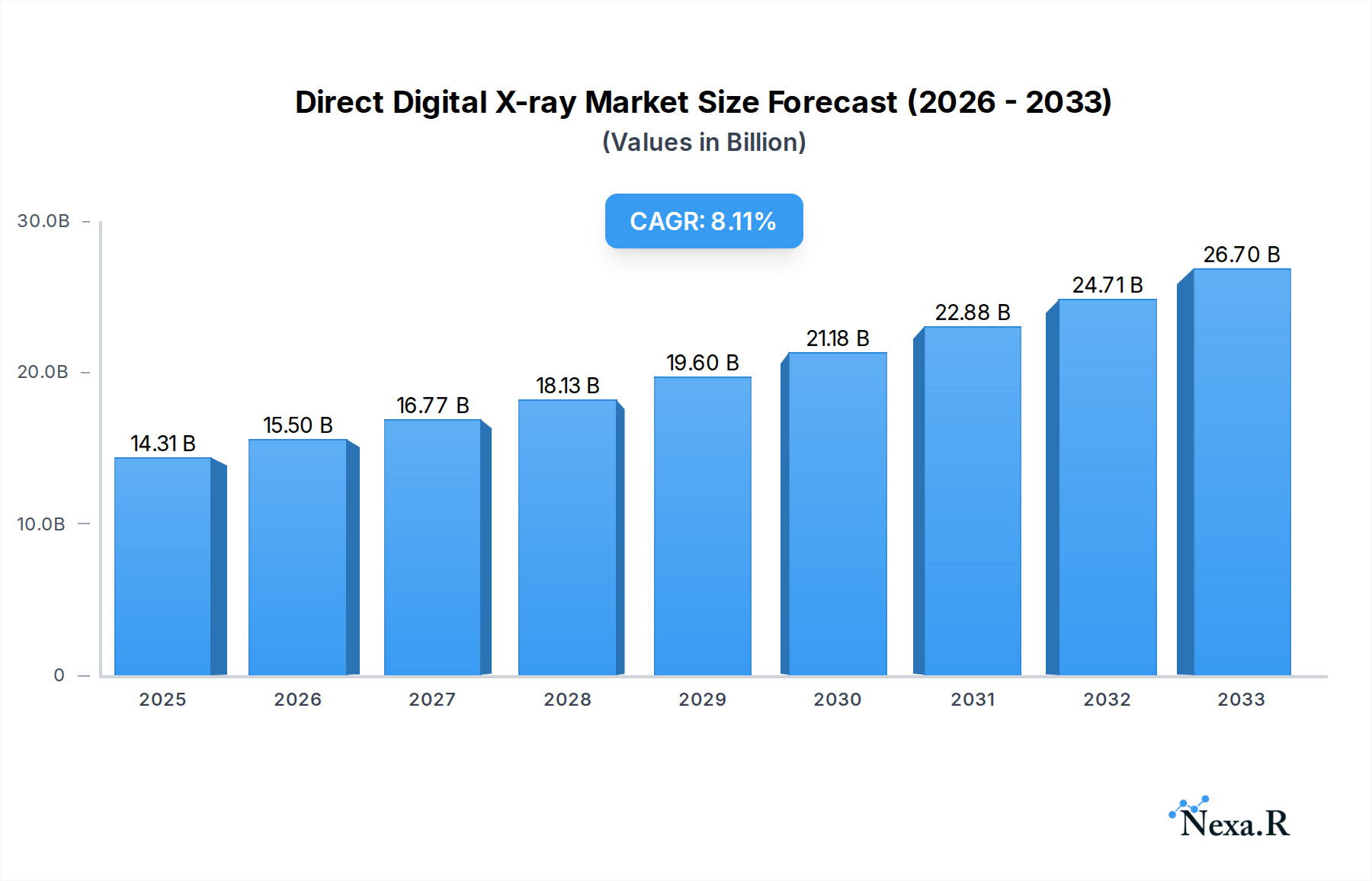

The Direct Digital X-ray market is poised for significant expansion, projected to reach $14.31 billion by 2025, driven by a CAGR of 8.3% throughout the forecast period. This robust growth is fueled by increasing adoption in hospitals and diagnostic imaging centers, where the demand for advanced radiography, fluoroscopy, and mammography systems is escalating. The inherent advantages of direct digital radiography, including superior image quality, reduced radiation exposure, and streamlined workflow, are primary catalysts. Furthermore, the growing prevalence of chronic diseases and an aging global population necessitate more sophisticated diagnostic tools, further bolstering market penetration. Technological advancements, such as the integration of artificial intelligence for image analysis and interpretation, are also creating new avenues for growth and enhancing the utility of direct digital X-ray systems. The shift towards preventative healthcare and the continuous need for accurate and timely diagnosis are fundamental drivers underpinning this upward market trajectory.

Direct Digital X-ray Market Size (In Billion)

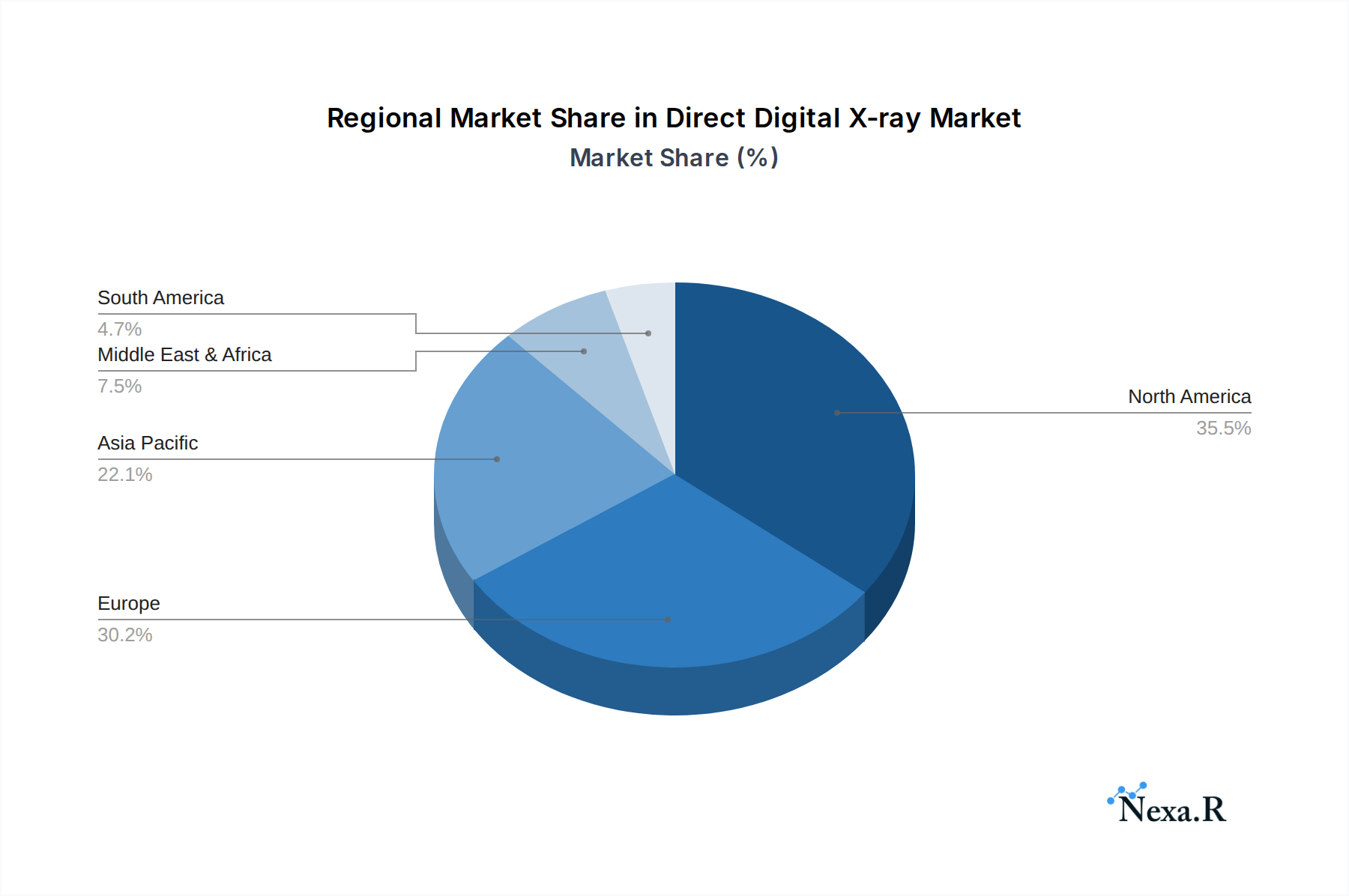

The market is characterized by a competitive landscape featuring major players like GE Healthcare, Siemens Healthcare, and Philips Healthcare, alongside emerging companies. These entities are actively investing in research and development to introduce innovative solutions and expand their product portfolios. While the market demonstrates strong growth potential, certain restraints exist, including the high initial investment costs associated with direct digital X-ray systems and the need for skilled personnel for operation and maintenance. However, government initiatives promoting healthcare infrastructure development and reimbursement policies are gradually mitigating these challenges. Regionally, North America and Europe are expected to maintain significant market shares due to advanced healthcare infrastructure and high adoption rates of new technologies. The Asia Pacific region, however, is anticipated to exhibit the fastest growth, propelled by expanding healthcare access, increasing disposable incomes, and a growing awareness of advanced diagnostic imaging. Continued innovation in detector technology and image processing will be crucial for sustained market leadership.

Direct Digital X-ray Company Market Share

Direct Digital X-ray Market Analysis: A Comprehensive Report 2019–2033

This in-depth report provides a detailed analysis of the Direct Digital X-ray market, a critical segment within the broader diagnostic imaging industry. Covering the historical period from 2019 to 2024, the base and estimated year of 2025, and a comprehensive forecast period extending to 2033, this study offers unparalleled insights for industry professionals, investors, and stakeholders. We delve into market dynamics, growth trends, regional dominance, product innovations, key drivers, barriers, emerging opportunities, and the competitive landscape, utilizing high-traffic SEO keywords to ensure maximum visibility. The report also examines the parent and child market structures to provide a holistic view of market interactions and potential.

Direct Digital X-ray Market Dynamics & Structure

The Direct Digital X-ray market is characterized by a moderately concentrated structure, with leading players like GE Healthcare, Siemens Healthcare, and Philips Healthcare holding significant market shares, estimated to be over 60% combined in 2025. Technological innovation is a primary driver, fueled by advancements in detector technology, image processing, and artificial intelligence for image analysis. Regulatory frameworks, such as FDA approvals and CE marking, play a crucial role in market entry and product adoption. Competitive product substitutes include computed radiography (CR) systems and other advanced imaging modalities like MRI and CT scans, though direct digital radiography (DR) offers superior speed and image quality for general radiography. End-user demographics are shifting towards an aging global population, increasing the demand for diagnostic imaging services, particularly in hospitals and diagnostic imaging centers. Mergers and acquisitions (M&A) trends have been observed, with larger companies acquiring smaller, innovative firms to expand their product portfolios and market reach. For instance, approximately 3-5 significant M&A deals are anticipated annually between 2025 and 2030, with deal values ranging from tens to hundreds of millions of dollars. Barriers to innovation include the high cost of research and development and the lengthy regulatory approval processes.

- Market Concentration: Moderately concentrated, with a few dominant global players.

- Technological Innovation Drivers: Detector technology, AI image analysis, portable systems.

- Regulatory Frameworks: FDA, CE Marking, national healthcare standards.

- Competitive Product Substitutes: Computed Radiography (CR), MRI, CT scans.

- End-User Demographics: Aging population, increasing chronic disease prevalence.

- M&A Trends: Strategic acquisitions to enhance technology and market presence.

Direct Digital X-ray Growth Trends & Insights

The global Direct Digital X-ray market is poised for substantial growth, projected to expand from an estimated $15.2 billion in 2025 to approximately $25.8 billion by 2033, exhibiting a compound annual growth rate (CAGR) of around 6.9% during the forecast period. This expansion is driven by increasing adoption rates of digital radiography systems in healthcare facilities worldwide, replacing older film-based technologies and computed radiography. Technological disruptions, such as the development of advanced flat-panel detectors with higher resolution and faster acquisition times, are significantly enhancing diagnostic accuracy and patient throughput. The shift in consumer behavior towards preventative healthcare and early disease detection further fuels demand for sophisticated imaging solutions. Market penetration is expected to rise considerably, especially in emerging economies where healthcare infrastructure is rapidly developing. The parent market, encompassing all X-ray imaging technologies, is valued at over $45 billion in 2025, with Direct Digital X-ray representing a significant and growing child market within it. Adoption rates for direct digital radiography in hospitals and diagnostic imaging centers are projected to reach over 85% by 2030. Key insights reveal a strong preference for integrated imaging solutions that offer seamless workflow integration and advanced post-processing capabilities. The increasing demand for portable and mobile X-ray units also contributes to market growth, enabling bedside imaging and expanding access to diagnostic services in remote areas.

Dominant Regions, Countries, or Segments in Direct Digital X-ray

North America is projected to maintain its dominance in the Direct Digital X-ray market, holding an estimated market share of over 35% in 2025, valued at approximately $5.3 billion. This leadership is attributed to factors such as high healthcare expenditure, a well-established reimbursement system, advanced healthcare infrastructure, and a strong emphasis on adopting cutting-edge medical technologies. The United States, in particular, is a major contributor due to its large patient population and the presence of leading healthcare providers and research institutions. In the parent market, North America's diagnostic imaging segment is also a significant contributor. Within this region, the Hospitals application segment is the primary growth driver, accounting for over 60% of direct digital X-ray utilization in 2025, with an estimated market value of $3.2 billion. This dominance is fueled by the continuous need for diagnostic imaging in emergency departments, surgical suites, and inpatient care.

Key drivers for regional dominance include:

- Economic Policies: Favorable government policies and investments in healthcare infrastructure.

- Infrastructure: Advanced hospital networks and a high density of diagnostic imaging centers.

- Technological Adoption: Early and widespread adoption of digital imaging technologies.

- Reimbursement Policies: Robust reimbursement schemes for diagnostic imaging procedures.

The Radiography type segment is also a dominant force within the Direct Digital X-ray market, contributing over 50% of the total market revenue in 2025, estimated at $7.6 billion. This is due to its widespread application in general diagnostic imaging for skeletal, chest, and abdominal examinations, making it a fundamental tool in every healthcare setting. The demand for high-quality, rapid radiography is consistently high across all healthcare segments.

Direct Digital X-ray Product Landscape

The Direct Digital X-ray product landscape is characterized by continuous innovation, focusing on enhanced image quality, reduced radiation dose, and improved workflow efficiency. Key product developments include the introduction of advanced amorphous silicon (a-Si) and indirect conversion detectors offering higher detective quantum efficiency (DQE) and spatial resolution. Emerging technologies such as CMOS detectors are also gaining traction for their speed and low power consumption. Applications span across general radiography, portable imaging, and specialized areas like mammography and fluoroscopy. Performance metrics emphasize faster image acquisition times, reduced patient waiting periods, and superior diagnostic accuracy. Unique selling propositions include lightweight and portable designs for bedside imaging and integrated solutions that combine imaging hardware with advanced software for image analysis and storage. Technological advancements are also focused on cybersecurity features to protect sensitive patient data.

Key Drivers, Barriers & Challenges in Direct Digital X-ray

Key Drivers:

- Technological Advancements: Continuous improvements in detector technology and image processing, leading to higher resolution and faster acquisition.

- Growing Demand for Diagnostic Imaging: Increasing prevalence of chronic diseases and an aging global population necessitate more diagnostic procedures.

- Replacement of Analog Technologies: The ongoing transition from film-based X-ray systems and computed radiography to direct digital systems.

- Government Initiatives & Healthcare Reforms: Investments in healthcare infrastructure and digital health adoption.

Key Barriers & Challenges:

- High Initial Investment Cost: The upfront cost of acquiring direct digital X-ray systems can be a significant barrier for smaller healthcare facilities.

- Regulatory Hurdles: Stringent approval processes for new technologies and devices can slow down market entry.

- Cybersecurity Concerns: Protecting sensitive patient data from breaches in digital imaging systems.

- Skilled Workforce Shortage: The need for trained personnel to operate and maintain advanced digital X-ray equipment.

- Supply Chain Disruptions: Potential for disruptions in the availability of critical components and manufacturing delays.

Emerging Opportunities in Direct Digital X-ray

Emerging opportunities in the Direct Digital X-ray market lie in the expanding use of artificial intelligence (AI) for image interpretation and workflow automation, promising to enhance diagnostic accuracy and efficiency. The growing demand for point-of-care imaging solutions, including portable and handheld X-ray devices, presents a significant opportunity to expand access to diagnostic services in remote areas and emergency settings. Furthermore, the development of advanced detector technologies with even lower radiation doses will cater to the increasing focus on patient safety and dose reduction. Untapped markets in developing economies, with their burgeoning healthcare sectors, offer substantial growth potential. Innovative applications in interventional radiology and specialized imaging techniques also present lucrative avenues.

Growth Accelerators in the Direct Digital X-ray Industry

Growth in the Direct Digital X-ray industry is being accelerated by several key factors. Continuous technological breakthroughs in detector sensitivity and resolution are driving demand for higher-quality imaging. Strategic partnerships between technology developers and healthcare providers are facilitating the integration of these advanced systems into clinical workflows. Market expansion strategies, particularly in emerging economies with rapidly developing healthcare infrastructure, are opening new avenues for growth. The increasing adoption of AI-powered diagnostic tools integrated with direct digital X-ray systems is further enhancing their value proposition and driving adoption. Investments in research and development by key players are fueling innovation and maintaining market momentum.

Key Players Shaping the Direct Digital X-ray Market

- GE Healthcare

- Siemens Healthcare

- Philips Healthcare

- Fujifilm

- Carestream Health

- AgfaHealth Care

- Hitachi

- Toshiba

- KonicaMinolta

- Shimadzu

- DEXIS

- Source-Ray

- AngellTechnology

- WandongMedical

- Mindray

- LandWind

- Mednova

Notable Milestones in Direct Digital X-ray Sector

- 2019: Introduction of AI-powered image analysis software for radiography.

- 2020: Launch of ultra-high-resolution flat-panel detectors by several leading manufacturers.

- 2021: Increased adoption of portable direct digital X-ray systems for bedside imaging in hospitals.

- 2022: Development of advanced detectors capable of significantly reducing radiation dose.

- 2023: Major collaborations between X-ray equipment manufacturers and AI software developers.

- 2024: Significant advancements in cybersecurity protocols for digital imaging systems.

In-Depth Direct Digital X-ray Market Outlook

The future outlook for the Direct Digital X-ray market is exceptionally promising, driven by continuous technological advancements and an ever-increasing global demand for accurate and efficient diagnostic imaging. Growth accelerators, including the integration of AI for enhanced diagnostics, the development of highly portable imaging solutions, and a sustained commitment to dose reduction, will fuel market expansion. Strategic partnerships and a focus on emerging markets will unlock new revenue streams. The market is expected to witness further innovation in detector technology and software solutions, solidifying its position as a cornerstone of modern diagnostic radiology. The parent market's growth also underpins the robust expansion of this vital child market, ensuring sustained investment and development.

Direct Digital X-ray Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Diagnostic Imaging Centers

- 1.3. Others

-

2. Types

- 2.1. Radiography

- 2.2. Fluoroscopy

- 2.3. Mammography

Direct Digital X-ray Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Direct Digital X-ray Regional Market Share

Geographic Coverage of Direct Digital X-ray

Direct Digital X-ray REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Diagnostic Imaging Centers

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Radiography

- 5.2.2. Fluoroscopy

- 5.2.3. Mammography

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Direct Digital X-ray Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Diagnostic Imaging Centers

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Radiography

- 6.2.2. Fluoroscopy

- 6.2.3. Mammography

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Direct Digital X-ray Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Diagnostic Imaging Centers

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Radiography

- 7.2.2. Fluoroscopy

- 7.2.3. Mammography

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Direct Digital X-ray Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Diagnostic Imaging Centers

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Radiography

- 8.2.2. Fluoroscopy

- 8.2.3. Mammography

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Direct Digital X-ray Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Diagnostic Imaging Centers

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Radiography

- 9.2.2. Fluoroscopy

- 9.2.3. Mammography

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Direct Digital X-ray Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Diagnostic Imaging Centers

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Radiography

- 10.2.2. Fluoroscopy

- 10.2.3. Mammography

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Direct Digital X-ray Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals

- 11.1.2. Diagnostic Imaging Centers

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Radiography

- 11.2.2. Fluoroscopy

- 11.2.3. Mammography

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 GE Healthcare

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Siemens Healthcare

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Philips Healthcare

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Fujifilm

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Carestream Health

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 AgfaHealth Care

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hitachi

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Toshiba

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 KonicaMinolta

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Shimadzu

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 DEXIS

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Source-Ray

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 AngellTechnology

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 WandongMedical

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Mindray

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 LandWind

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Mednova

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 GE Healthcare

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Direct Digital X-ray Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Direct Digital X-ray Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Direct Digital X-ray Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Direct Digital X-ray Volume (K), by Application 2025 & 2033

- Figure 5: North America Direct Digital X-ray Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Direct Digital X-ray Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Direct Digital X-ray Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Direct Digital X-ray Volume (K), by Types 2025 & 2033

- Figure 9: North America Direct Digital X-ray Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Direct Digital X-ray Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Direct Digital X-ray Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Direct Digital X-ray Volume (K), by Country 2025 & 2033

- Figure 13: North America Direct Digital X-ray Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Direct Digital X-ray Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Direct Digital X-ray Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Direct Digital X-ray Volume (K), by Application 2025 & 2033

- Figure 17: South America Direct Digital X-ray Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Direct Digital X-ray Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Direct Digital X-ray Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Direct Digital X-ray Volume (K), by Types 2025 & 2033

- Figure 21: South America Direct Digital X-ray Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Direct Digital X-ray Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Direct Digital X-ray Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Direct Digital X-ray Volume (K), by Country 2025 & 2033

- Figure 25: South America Direct Digital X-ray Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Direct Digital X-ray Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Direct Digital X-ray Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Direct Digital X-ray Volume (K), by Application 2025 & 2033

- Figure 29: Europe Direct Digital X-ray Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Direct Digital X-ray Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Direct Digital X-ray Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Direct Digital X-ray Volume (K), by Types 2025 & 2033

- Figure 33: Europe Direct Digital X-ray Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Direct Digital X-ray Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Direct Digital X-ray Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Direct Digital X-ray Volume (K), by Country 2025 & 2033

- Figure 37: Europe Direct Digital X-ray Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Direct Digital X-ray Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Direct Digital X-ray Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Direct Digital X-ray Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Direct Digital X-ray Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Direct Digital X-ray Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Direct Digital X-ray Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Direct Digital X-ray Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Direct Digital X-ray Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Direct Digital X-ray Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Direct Digital X-ray Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Direct Digital X-ray Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Direct Digital X-ray Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Direct Digital X-ray Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Direct Digital X-ray Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Direct Digital X-ray Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Direct Digital X-ray Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Direct Digital X-ray Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Direct Digital X-ray Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Direct Digital X-ray Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Direct Digital X-ray Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Direct Digital X-ray Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Direct Digital X-ray Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Direct Digital X-ray Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Direct Digital X-ray Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Direct Digital X-ray Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Direct Digital X-ray Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Direct Digital X-ray Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Direct Digital X-ray Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Direct Digital X-ray Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Direct Digital X-ray Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Direct Digital X-ray Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Direct Digital X-ray Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Direct Digital X-ray Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Direct Digital X-ray Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Direct Digital X-ray Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Direct Digital X-ray Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Direct Digital X-ray Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Direct Digital X-ray Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Direct Digital X-ray Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Direct Digital X-ray Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Direct Digital X-ray Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Direct Digital X-ray Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Direct Digital X-ray Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Direct Digital X-ray Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Direct Digital X-ray Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Direct Digital X-ray Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Direct Digital X-ray Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Direct Digital X-ray Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Direct Digital X-ray Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Direct Digital X-ray Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Direct Digital X-ray Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Direct Digital X-ray Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Direct Digital X-ray Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Direct Digital X-ray Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Direct Digital X-ray Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Direct Digital X-ray Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Direct Digital X-ray Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Direct Digital X-ray Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Direct Digital X-ray Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Direct Digital X-ray Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Direct Digital X-ray Volume K Forecast, by Country 2020 & 2033

- Table 79: China Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Direct Digital X-ray Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Direct Digital X-ray Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Direct Digital X-ray?

The projected CAGR is approximately 8.3%.

2. Which companies are prominent players in the Direct Digital X-ray?

Key companies in the market include GE Healthcare, Siemens Healthcare, Philips Healthcare, Fujifilm, Carestream Health, AgfaHealth Care, Hitachi, Toshiba, KonicaMinolta, Shimadzu, DEXIS, Source-Ray, AngellTechnology, WandongMedical, Mindray, LandWind, Mednova.

3. What are the main segments of the Direct Digital X-ray?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.31 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Direct Digital X-ray," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Direct Digital X-ray report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Direct Digital X-ray?

To stay informed about further developments, trends, and reports in the Direct Digital X-ray, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence