Key Insights

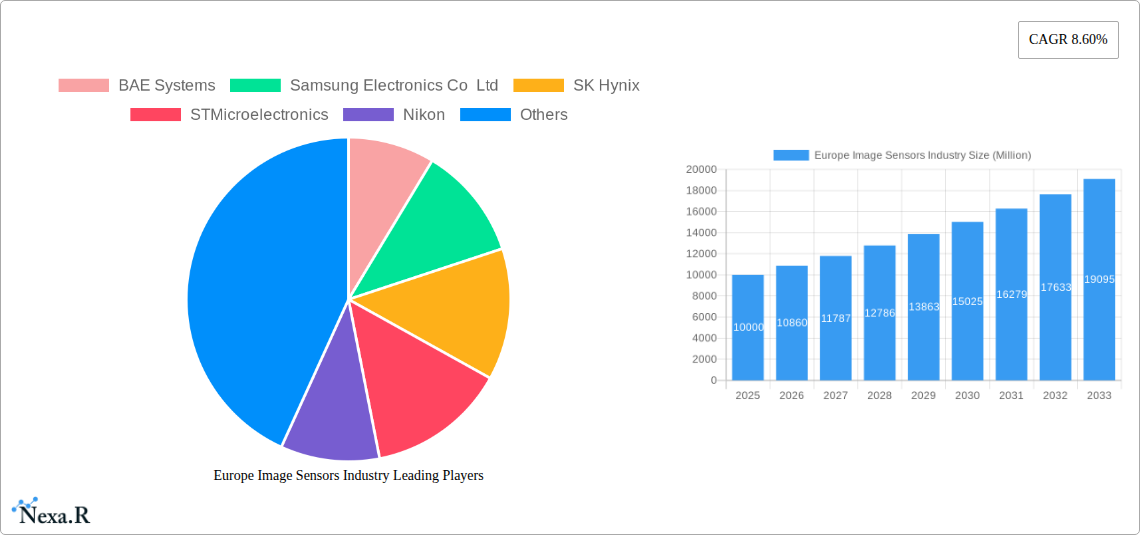

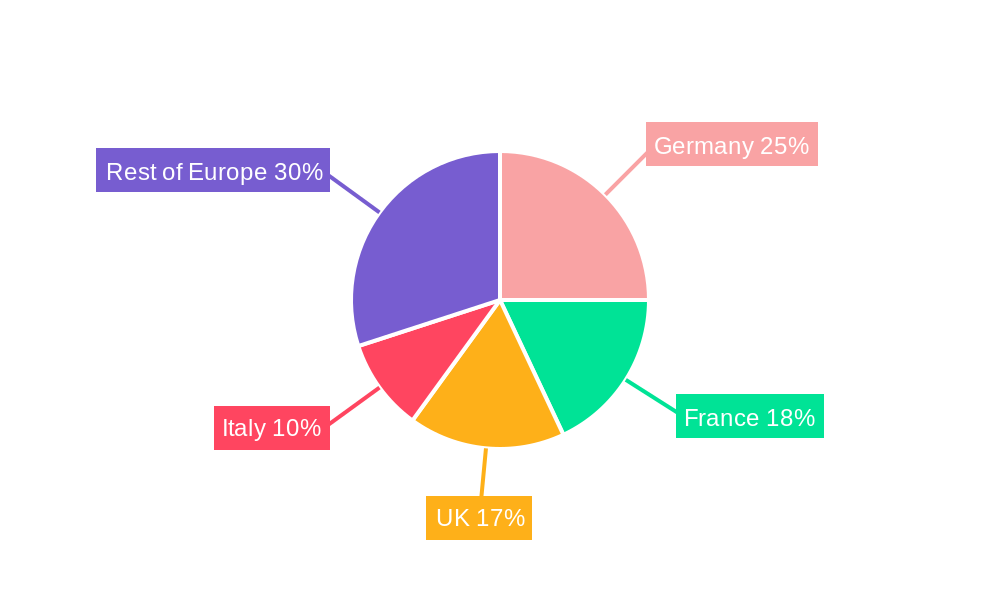

The European image sensor market, valued at approximately €10 billion in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 8.60% from 2025 to 2033. This expansion is driven by several key factors. Firstly, the surging demand for advanced imaging technologies across diverse sectors like consumer electronics (smartphones, cameras), automotive (Advanced Driver-Assistance Systems - ADAS), healthcare (medical imaging), and security & surveillance is significantly boosting market growth. The increasing adoption of artificial intelligence (AI) and machine learning (ML) in image processing further fuels this demand, enabling sophisticated applications like facial recognition, object detection, and autonomous driving. Technological advancements, such as the development of higher-resolution sensors with improved sensitivity and lower power consumption (particularly in CMOS technology), are also major contributors. Furthermore, government initiatives promoting technological innovation and digitalization across various European nations are creating a favorable environment for market expansion. Germany, France, and the United Kingdom represent the largest national markets within Europe, driven by strong manufacturing bases and significant investments in R&D.

However, the market faces certain constraints. The high initial investment required for the development and manufacturing of advanced image sensors can be a barrier to entry for smaller companies. Supply chain disruptions and fluctuations in raw material prices also pose challenges. Competition from established players, both within Europe and internationally, is intense. Nonetheless, the overall market outlook remains positive, driven by sustained technological progress and the increasing integration of image sensors in everyday devices and industrial applications. The continued growth in sectors such as automotive and healthcare is expected to propel the European image sensor market towards significant expansion in the forecast period.

Europe Image Sensors Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Europe image sensors market, covering the period from 2019 to 2033. It delves into market dynamics, growth trends, key players, and future opportunities within the parent market of electronic components and the child markets of consumer electronics, automotive, and healthcare. The report uses 2025 as its base year and offers forecasts until 2033, incorporating historical data from 2019-2024. Expect in-depth analysis expressed in million units.

Europe Image Sensors Industry Market Dynamics & Structure

The European image sensor market is characterized by a moderately concentrated landscape with several key players vying for market share. Technological innovation, particularly in CMOS sensor technology, is a primary growth driver. Stringent regulatory frameworks concerning data privacy and product safety influence market dynamics. Competitive pressures from substitutes, such as alternative sensing technologies, pose ongoing challenges. End-user demographics, especially the rising demand for high-resolution imaging in consumer electronics and automotive, are shaping market growth. Mergers and acquisitions (M&A) activity remains moderate, with strategic partnerships playing a significant role in consolidating the market.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2024 (estimated).

- Technological Innovation: Continuous advancements in CMOS technology, driving miniaturization and improved image quality.

- Regulatory Framework: Compliance with GDPR and other data privacy regulations impacts product design and data handling.

- Competitive Substitutes: Emerging technologies like LiDAR and 3D sensing present competitive threats.

- M&A Activity: xx major M&A deals recorded between 2019 and 2024 (estimated).

Europe Image Sensors Industry Growth Trends & Insights

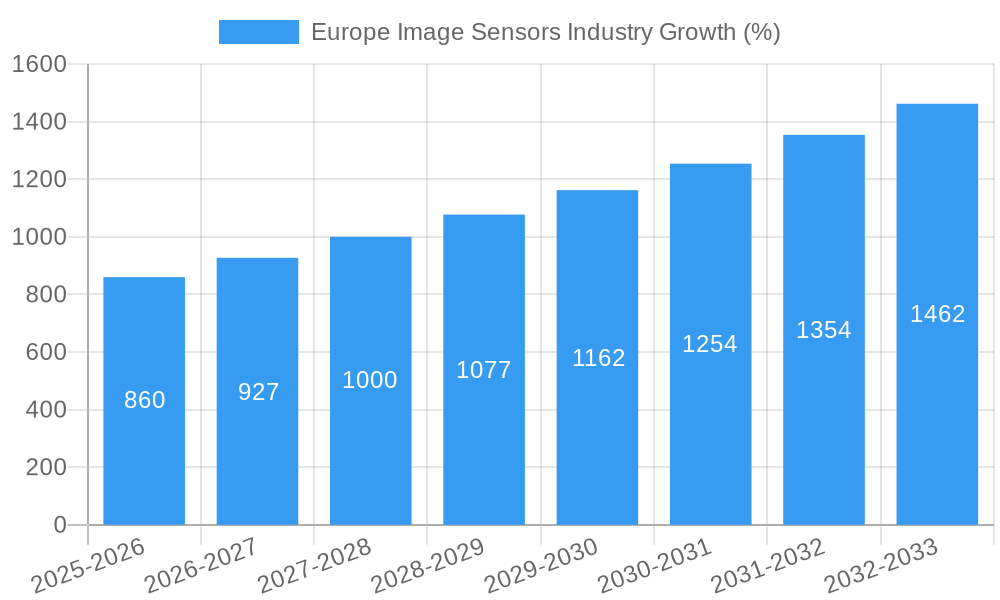

The European image sensor market experienced robust growth during the historical period (2019-2024), driven by increased demand across diverse end-user industries. The market size expanded from xx million units in 2019 to xx million units in 2024, exhibiting a CAGR of xx%. This growth is projected to continue, with a forecasted CAGR of xx% from 2025 to 2033, reaching xx million units by 2033. The adoption rate of high-resolution image sensors in smartphones, automotive applications, and medical imaging systems is a major contributor to market expansion. Technological disruptions, such as the introduction of advanced CMOS and SPAD technologies, are accelerating this trend. Consumer behavior shifts toward higher image quality and enhanced visual experiences are fueling market growth. The increasing integration of image sensors into smart devices and IoT applications is expected to further drive market expansion in the forecast period.

Dominant Regions, Countries, or Segments in Europe Image Sensors Industry

Germany, the United Kingdom, and France are the dominant countries in the European image sensor market, driven by strong technological capabilities, established manufacturing bases, and significant demand from diverse end-user industries. The CMOS segment dominates the market by type, owing to its superior performance and cost-effectiveness compared to CCD sensors. The consumer electronics industry segment accounts for the largest share of overall demand, driven by the widespread adoption of smartphones, tablets, and digital cameras. The automotive and transportation segment is experiencing rapid growth, driven by the increasing demand for advanced driver-assistance systems (ADAS) and autonomous driving technology.

- Germany: Strong automotive industry and presence of major sensor manufacturers.

- United Kingdom: Significant R&D investments and presence of key players in the aerospace and defense sector.

- France: Growing consumer electronics market and investments in industrial automation.

- CMOS: High performance, cost-effectiveness, and wide-ranging applications.

- Consumer Electronics: High demand for high-resolution cameras in smartphones and other consumer devices.

Europe Image Sensors Industry Product Landscape

The European image sensor market features a wide array of products catering to diverse applications, ranging from low-resolution sensors for basic imaging to high-resolution sensors for advanced imaging systems. Key performance metrics include resolution (in megapixels), pixel size, sensitivity, and dynamic range. Product innovation focuses on miniaturization, improved low-light performance, and enhanced image quality. Unique selling propositions often emphasize superior image processing capabilities and power efficiency. Recent advancements include the development of extremely small sensors with high megapixel counts, exceeding 200 million pixels, and advancements in SPAD technology for low-light imaging.

Key Drivers, Barriers & Challenges in Europe Image Sensors Industry

Key Drivers: The increasing demand for high-resolution imaging in consumer electronics, automotive, and healthcare is a primary growth driver. Advances in CMOS technology, leading to miniaturization and improved image quality, are fueling market expansion. Government initiatives promoting technological innovation and automation are also supporting market growth.

Key Challenges: Intense competition from Asian manufacturers, particularly in terms of cost and production scale, poses a major challenge. Supply chain disruptions and the availability of raw materials can significantly impact production and market stability. Stringent regulatory requirements concerning data privacy and product safety add to the complexity of market operations.

Emerging Opportunities in Europe Image Sensors Industry

Emerging opportunities lie in the growing adoption of image sensors in smart home devices, robotics, and industrial automation. The increasing demand for high-performance sensors in medical imaging and scientific research also presents significant growth prospects. The development of innovative applications, such as 3D sensing and augmented reality (AR), are creating new avenues for market expansion. Untapped markets in emerging economies within Europe offer further potential for growth.

Growth Accelerators in the Europe Image Sensors Industry Industry

Technological breakthroughs, such as the development of high-resolution and high-sensitivity sensors with advanced features, are significant growth accelerators. Strategic partnerships and collaborations between sensor manufacturers, system integrators, and end-users facilitate innovation and market expansion. Investments in R&D aimed at improving sensor performance and reducing production costs are crucial drivers of long-term growth. Expanding into new applications and geographic markets provides opportunities for market expansion.

Key Players Shaping the Europe Image Sensors Industry Market

- BAE Systems

- Samsung Electronics Co Ltd

- SK Hynix

- STMicroelectronics

- Nikon

- On Semiconductor

- Omnivision

- Toshiba

- Panasonic Corporation

- Sony Corporation

Notable Milestones in Europe Image Sensors Industry Sector

- December 2021: Canon develops a new image sensor using SPAD technology for superior low-light performance.

- June 2021: Samsung Electronics launches a 0.64µm 50-megapixel image sensor.

- September 2021: Samsung Electronics introduces a 0.64µm 200-megapixel image sensor.

- January 2022: SK Hynix begins mass production of 0.7µm 50-megapixel image sensors.

In-Depth Europe Image Sensors Industry Market Outlook

The European image sensor market is poised for continued strong growth driven by technological advancements, increasing demand from diverse end-user industries, and expansion into new applications. Strategic investments in R&D, strategic partnerships, and the development of innovative products and solutions will further accelerate market expansion. The market’s future potential is significant, presenting substantial strategic opportunities for established players and new entrants alike.

Europe Image Sensors Industry Segmentation

-

1. Type

- 1.1. CMOS

- 1.2. CCD

-

2. End-User Industry

- 2.1. Consumer Electronics

- 2.2. Healthcare

- 2.3. Industrial

- 2.4. Security and Surveillance

- 2.5. Automotive and Transportation

- 2.6. Aerospace and Defense

- 2.7. Other End-user Industries

Europe Image Sensors Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Image Sensors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.60% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Incorporation of high-resolution cameras with image sensors in mobile devices; Improving medical imaging solutions; Increasing expenditure on security and surveillance in public places

- 3.3. Market Restrains

- 3.3.1. High Manufacturing costs

- 3.4. Market Trends

- 3.4.1. The Automotive Segment is Expected to Drive the Market's Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Image Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. CMOS

- 5.1.2. CCD

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Consumer Electronics

- 5.2.2. Healthcare

- 5.2.3. Industrial

- 5.2.4. Security and Surveillance

- 5.2.5. Automotive and Transportation

- 5.2.6. Aerospace and Defense

- 5.2.7. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Europe Image Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Image Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Image Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Image Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Image Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Image Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Image Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 BAE Systems

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Samsung Electronics Co Ltd

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 SK Hynix

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 STMicroelectronics

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Nikon

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 On Semiconductor

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Omnivision*List Not Exhaustive

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Toshiba

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Panasonic Corporation

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Sony Corporation

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 BAE Systems

List of Figures

- Figure 1: Europe Image Sensors Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Image Sensors Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Image Sensors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Image Sensors Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Europe Image Sensors Industry Revenue Million Forecast, by End-User Industry 2019 & 2032

- Table 4: Europe Image Sensors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Europe Image Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Europe Image Sensors Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 14: Europe Image Sensors Industry Revenue Million Forecast, by End-User Industry 2019 & 2032

- Table 15: Europe Image Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: United Kingdom Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Germany Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: France Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Italy Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Spain Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Netherlands Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Belgium Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Sweden Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Norway Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Poland Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Denmark Europe Image Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Image Sensors Industry?

The projected CAGR is approximately 8.60%.

2. Which companies are prominent players in the Europe Image Sensors Industry?

Key companies in the market include BAE Systems, Samsung Electronics Co Ltd, SK Hynix, STMicroelectronics, Nikon, On Semiconductor, Omnivision*List Not Exhaustive, Toshiba, Panasonic Corporation, Sony Corporation.

3. What are the main segments of the Europe Image Sensors Industry?

The market segments include Type, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Incorporation of high-resolution cameras with image sensors in mobile devices; Improving medical imaging solutions; Increasing expenditure on security and surveillance in public places.

6. What are the notable trends driving market growth?

The Automotive Segment is Expected to Drive the Market's Growth.

7. Are there any restraints impacting market growth?

High Manufacturing costs.

8. Can you provide examples of recent developments in the market?

January 2022 - SK Hynix started to mass-produce 0.7 image sensors, getting into competition with Sony and Samsung Electronics in the global image sensor market. The company recently began volume production of 0.7 50-million-pixel image sensors, which are at the same level as Sony products. Samsung Electronics launched a 0.64 50-million-pixel image sensor, one of the industry's smallest, in June 2021 and introduced a 0.64 200-million-pixel sensor in September 2021. Recently, Omnivision of China also took the wraps off a 0.62-pixel image sensor at CES 2022.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Image Sensors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Image Sensors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Image Sensors Industry?

To stay informed about further developments, trends, and reports in the Europe Image Sensors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence