Key Insights

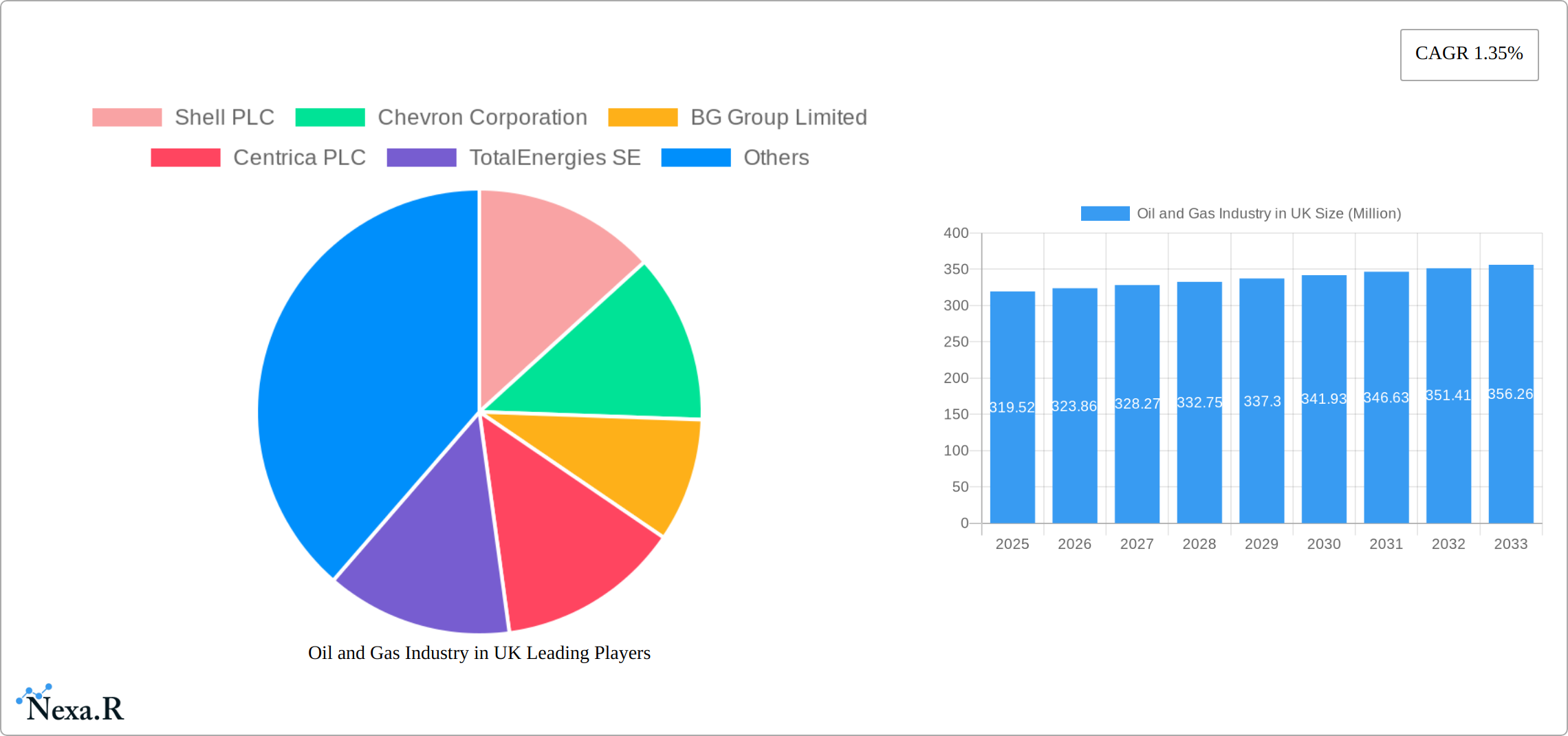

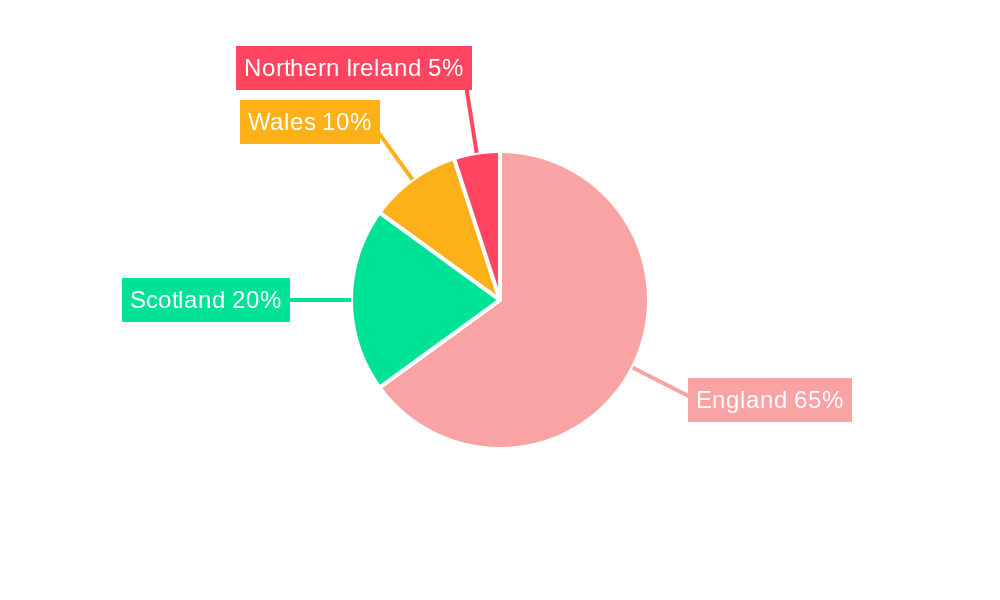

The UK oil and gas industry, valued at £319.52 million in 2025, exhibits a relatively modest compound annual growth rate (CAGR) of 1.35% projected from 2025 to 2033. This moderate growth reflects a complex interplay of factors. While the upstream sector (exploration and production) faces challenges from declining North Sea reserves and increasing operational costs, the midstream (transportation and storage) and downstream (refining and distribution) segments are experiencing more stability, driven by consistent domestic demand and strategic investments in infrastructure upgrades to enhance efficiency and safety. Furthermore, the ongoing energy transition towards renewables presents both opportunities and restraints. The government's commitment to net-zero emissions necessitates a shift away from fossil fuels, potentially impacting long-term investment in exploration and production. However, the UK's role as a significant gas importer and the need for a secure energy supply in the transition period will likely sustain demand for natural gas in the coming years, creating opportunities within the midstream and downstream sectors for companies like Shell, BP, and Centrica. The regional distribution of activity is largely concentrated in England, Scotland, and Wales, with Northern Ireland having a comparatively smaller footprint. This necessitates a regional strategy focusing on infrastructure improvements and localized energy solutions to support the transition.

The forecast period of 2025-2033 will see a gradual increase in market size, influenced by fluctuating global energy prices, government policies promoting energy security and diversification, and technological advancements in exploration and production. Major players like Shell, BP, and TotalEnergies will play crucial roles in shaping the industry's future trajectory through strategic investments, mergers and acquisitions, and adapting to the changing regulatory landscape. While the long-term outlook for oil and gas is subject to uncertainty related to renewable energy penetration, the short-to-medium term will likely see a continued albeit modest growth, primarily supported by natural gas demand and existing infrastructure. The industry needs to adapt to the energy transition, focusing on decarbonization efforts and exploring opportunities in carbon capture and storage technologies to maintain its relevance and ensure a sustainable future.

This in-depth report provides a comprehensive analysis of the UK oil and gas industry, encompassing market dynamics, growth trends, key players, and future outlook. With a focus on upstream, midstream, and downstream segments, this report is essential for industry professionals, investors, and strategic decision-makers. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report leverages proprietary data and industry expertise to deliver actionable insights.

Oil and Gas Industry in UK Market Dynamics & Structure

The UK oil and gas market is characterized by a complex interplay of factors influencing its structure and dynamics. Market concentration is relatively high, with a few major players dominating the upstream and downstream segments. Technological innovation, particularly in areas like AI-powered exploration and carbon capture, is driving efficiency improvements and shaping the competitive landscape. Stringent regulatory frameworks, aimed at environmental protection and energy security, significantly impact operational strategies. The emergence of renewable energy sources presents a competitive challenge, acting as a product substitute. M&A activity has been moderate in recent years, with xx million in deal volume recorded in 2024, reflecting industry consolidation and strategic partnerships. End-user demographics are diverse, encompassing industrial, commercial, and residential consumers, each with unique needs and demands.

- Market Concentration: High, with top 5 players holding xx% market share in 2024.

- Technological Innovation: AI, automation, and carbon capture technologies are key drivers.

- Regulatory Framework: Stringent environmental regulations and energy security policies.

- Competitive Substitutes: Renewable energy sources pose a significant challenge.

- M&A Activity: Moderate, with xx million in deal volume in 2024.

- Innovation Barriers: High capital expenditure and regulatory complexities.

Oil and Gas Industry in UK Growth Trends & Insights

The UK oil and gas market navigated fluctuating growth between 2019 and 2024, significantly impacted by global energy price volatility and evolving government regulations. However, a renewed emphasis on bolstering domestic energy security and strategic investments has positioned the sector for substantial growth in the coming years. While precise figures for 2024 and projected 2033 market size are unavailable at this time (replace "xx million" with actual data), the market is expected to exhibit a notable compound annual growth rate (CAGR). This growth is fueled by increasing adoption of advanced technologies aimed at enhancing efficiency and mitigating environmental concerns. Simultaneously, shifting consumer preferences towards sustainable practices are reshaping demand patterns, accelerating the transition to lower-carbon energy sources and necessitating adaptation within the industry.

Dominant Regions, Countries, or Segments in Oil and Gas Industry in UK

The North Sea remains the cornerstone of the UK's upstream oil and gas activities, contributing substantially to domestic production. The downstream sector, encompassing refining, processing, and distribution, maintains a robust presence throughout the UK, with significant hubs strategically located across the nation. Upstream sector expansion is largely driven by investments in established fields and ongoing exploration efforts in the North Sea, facilitated by government support and incentives. Conversely, midstream and downstream segment performance is influenced by refining capacity, the efficiency of transportation infrastructure, and fluctuating demand from various industrial and consumer sectors.

- Upstream: North Sea, driven by investment in existing and new field developments, and exploration of emerging reserves.

- Midstream: Pipelines, storage facilities, and processing plants strategically located across the UK, focusing on infrastructure modernization and optimization.

- Downstream: Extensive network of refineries, distribution centers, and retail outlets across the UK, adapting to changing fuel demands and environmental regulations.

- Key Drivers: Government policies promoting energy security, technological innovation leading to improved efficiency and reduced emissions, and evolving consumer demands for sustainable energy solutions.

- Market Share: [Insert updated market share data for Upstream, Midstream, and Downstream sectors for 2024. e.g., Upstream sector holds 45% market share, midstream 25%, and downstream 30% in 2024.]

Oil and Gas Industry in UK Product Landscape

The UK oil and gas industry encompasses a diverse product portfolio, ranging from crude oil and natural gas to refined petroleum products such as gasoline, diesel, and petrochemicals. Innovation is paramount, focusing on enhancing efficiency across the entire value chain, from extraction and refining to distribution and end-use. Technological advancements, including the application of artificial intelligence (AI) and machine learning (ML) for operational optimization and environmental impact reduction, are rapidly transforming the industry. The sector is actively pursuing the development of cleaner and more sustainable fuel options, aligning with global decarbonization targets and commitments.

Key Drivers, Barriers & Challenges in Oil and Gas Industry in UK

Key Drivers: Government support for energy independence, investment in offshore wind and carbon capture technologies, and growing demand for petrochemicals.

Challenges: High exploration and production costs, stringent environmental regulations, and the increasing competition from renewable energy sources. Supply chain disruptions have led to xx% increase in production costs in 2024. Regulatory hurdles and obtaining necessary permits pose significant delays. Competitive pressures from renewable energy sources are forcing strategic adjustments.

Emerging Opportunities in Oil and Gas Industry in UK

Significant growth opportunities abound in the UK oil and gas sector, notably in the realm of carbon capture, utilization, and storage (CCUS) technologies, the production and distribution of blue hydrogen, exploration of low-carbon gas sources, and strategic diversification into renewable energy sectors. The ongoing drive to improve operational efficiency and minimize emissions also presents substantial opportunities for technological innovation and strategic partnerships. This includes investment in advanced analytics, automation, and digitalization to optimize processes and reduce environmental footprint.

Growth Accelerators in the Oil and Gas Industry in UK Industry

Long-term growth will be driven by sustained investments in existing fields, new exploration initiatives in the North Sea, technological advancements in energy efficiency and emissions reduction, and strategic collaborations between oil and gas companies and renewable energy players. The commitment to energy security and government support are vital components of sustained growth.

Key Players Shaping the Oil and Gas Industry in UK Market

- Shell PLC

- Chevron Corporation

- BP PLC

- ESSO UK Limited

- Centrica PLC

- TotalEnergies SE

- Cadent Gas Ltd

- BG Group Limited (now part of Shell)

- Valaris PLC

- Dana Petroleum E&P Limited

- [Add other relevant key players]

Notable Milestones in Oil and Gas Industry in UK Sector

- May 2023: Shell PLC and SparkCognition collaborate on AI-powered offshore oil exploration.

- May 2022: BP PLC announces a USD 22.5 billion investment in North Sea oil and gas fields.

In-Depth Oil and Gas Industry in UK Market Outlook

The UK oil and gas industry is poised for moderate growth, driven by domestic energy security needs and strategic investments in existing infrastructure. Opportunities exist in the areas of CCUS, blue hydrogen, and strategic partnerships with renewable energy companies. However, navigating regulatory challenges and adapting to evolving consumer preferences will be critical for long-term success. The market presents considerable potential for companies that can effectively balance environmental considerations with economic objectives.

Oil and Gas Industry in UK Segmentation

-

1. Sector

- 1.1. Upstream

- 1.2. Midstream

- 1.3. Downstream

Oil and Gas Industry in UK Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Russia

- 1.7. Benelux

- 1.8. Nordics

- 1.9. Rest of Europe

Oil and Gas Industry in UK REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 1.35% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Domestic Oil and Gas Production4.; Investments in Oil and Gas Infrastructure Development

- 3.3. Market Restrains

- 3.3.1. 4.; Growth of Renewable Energy

- 3.4. Market Trends

- 3.4.1. Upstream Segment Expected to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. England Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 7. Wales Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 8. Scotland Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 9. Northern Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 10. Ireland Oil and Gas Industry in UK Analysis, Insights and Forecast, 2019-2031

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Shell PLC

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Chevron Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BG Group Limited

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Centrica PLC

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 TotalEnergies SE

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Cadent Gas Ltd

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 BP PLC

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ESSO UK Limited

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Valaris PLC

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Dana Petroleum E&P Limited

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Shell PLC

List of Figures

- Figure 1: Oil and Gas Industry in UK Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Oil and Gas Industry in UK Share (%) by Company 2024

List of Tables

- Table 1: Oil and Gas Industry in UK Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Oil and Gas Industry in UK Revenue Million Forecast, by Sector 2019 & 2032

- Table 3: Oil and Gas Industry in UK Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Oil and Gas Industry in UK Revenue Million Forecast, by Country 2019 & 2032

- Table 5: England Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Wales Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Scotland Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Northern Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Ireland Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Oil and Gas Industry in UK Revenue Million Forecast, by Sector 2019 & 2032

- Table 11: Oil and Gas Industry in UK Revenue Million Forecast, by Country 2019 & 2032

- Table 12: United Kingdom Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Germany Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: France Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Italy Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Spain Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Russia Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Benelux Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Nordics Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of Europe Oil and Gas Industry in UK Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oil and Gas Industry in UK?

The projected CAGR is approximately 1.35%.

2. Which companies are prominent players in the Oil and Gas Industry in UK?

Key companies in the market include Shell PLC, Chevron Corporation, BG Group Limited, Centrica PLC, TotalEnergies SE, Cadent Gas Ltd, BP PLC, ESSO UK Limited, Valaris PLC, Dana Petroleum E&P Limited.

3. What are the main segments of the Oil and Gas Industry in UK?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 319.52 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Domestic Oil and Gas Production4.; Investments in Oil and Gas Infrastructure Development.

6. What are the notable trends driving market growth?

Upstream Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Growth of Renewable Energy.

8. Can you provide examples of recent developments in the market?

May 2023: Shell PLC, a major oil and gas company from the United Kingdom, and big-data analytics company SparkCognition announced their collaboration, stating that Shell will leverage artificial intelligence-based technology to enhance offshore oil exploration and production in deep-sea exploration and production.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Oil and Gas Industry in UK," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Oil and Gas Industry in UK report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Oil and Gas Industry in UK?

To stay informed about further developments, trends, and reports in the Oil and Gas Industry in UK, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence