Key Insights

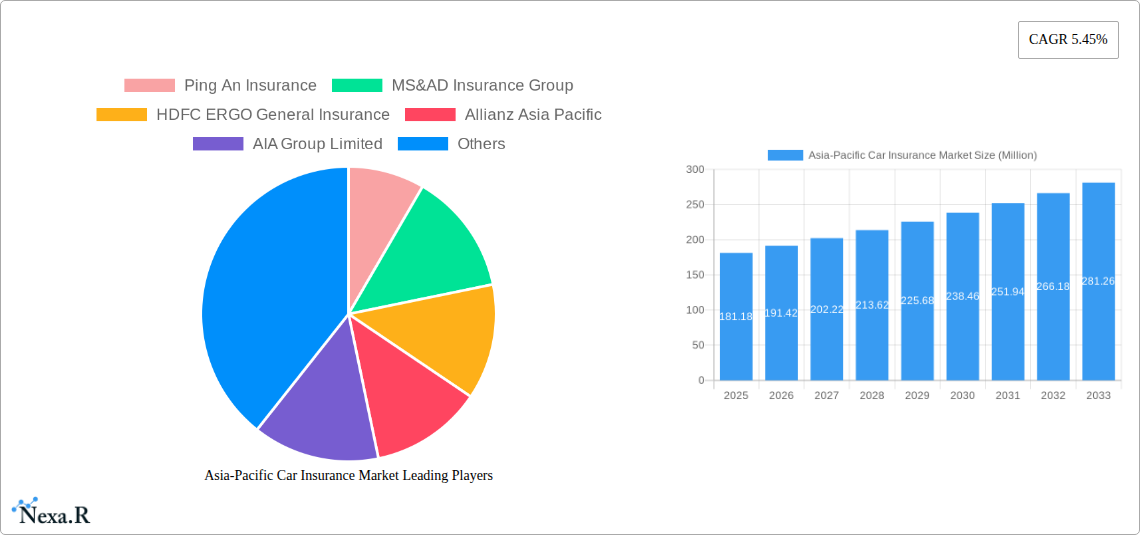

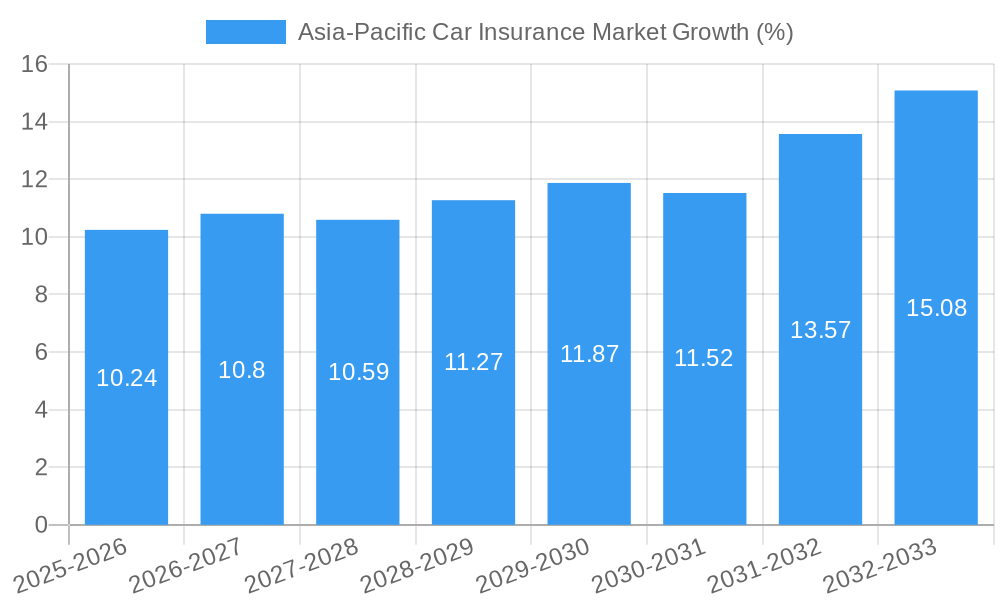

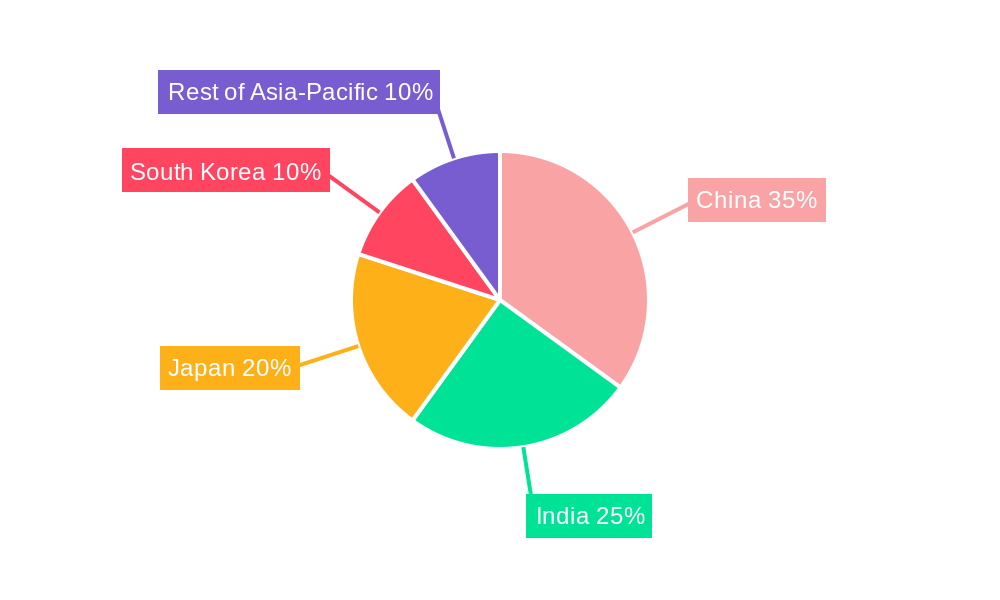

The Asia-Pacific car insurance market, valued at $181.18 million in 2025, is projected to experience robust growth, driven by a rising number of vehicle owners, increasing urbanization, and stricter government regulations mandating insurance coverage. The market's Compound Annual Growth Rate (CAGR) of 5.45% from 2025 to 2033 indicates a substantial expansion over the forecast period. Key growth drivers include the burgeoning middle class in countries like China and India, leading to increased disposable income and car purchases. Furthermore, a growing awareness of the financial risks associated with accidents and the increasing availability of online insurance platforms are fueling market expansion. The market is segmented by application (personal and commercial vehicles), distribution channel (direct sales, agents, brokers, banks, online), coverage type (third-party liability, collision/comprehensive), and country (China, Japan, India, South Korea, and the Rest of Asia-Pacific). China and India are expected to dominate the market due to their large populations and rapidly growing automotive sectors. However, challenges remain, including fluctuating fuel prices, economic uncertainties in some regions, and the need for greater insurance penetration in certain markets. Competitive landscape analysis reveals key players such as Ping An Insurance, MS&AD Insurance Group, and HDFC ERGO General Insurance vying for market share through strategic partnerships, product diversification, and technological advancements. The increasing adoption of telematics and data analytics is further transforming the industry, enabling more personalized pricing and risk assessment.

The market's segmentation offers various opportunities for growth. The personal vehicle segment is currently the largest, but the commercial vehicle segment is poised for significant expansion due to the growth of e-commerce and logistics industries. Online distribution channels are witnessing rapid growth, leveraging digital technologies to reach a wider customer base and streamline operations. Insurers are increasingly focusing on offering comprehensive coverage options to cater to the rising demand for enhanced protection. The competitive landscape is characterized by a mix of global and regional players, with established insurers seeking to consolidate their market positions and new entrants focusing on niche markets and innovative product offerings. The future of the Asia-Pacific car insurance market hinges on adapting to evolving consumer preferences, technological disruptions, and regulatory changes, ensuring continued growth and sustainability.

Asia-Pacific Car Insurance Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Asia-Pacific car insurance market, encompassing market dynamics, growth trends, regional dominance, product landscape, and future outlook. The study period covers 2019-2033, with 2025 as the base year and a forecast period of 2025-2033. The report leverages extensive data analysis to offer valuable insights for industry professionals, investors, and strategic decision-makers. The total market size is projected to reach xx Million by 2033.

Asia-Pacific Car Insurance Market Dynamics & Structure

This section delves into the intricate structure of the Asia-Pacific car insurance market, analyzing its concentration, innovation drivers, regulatory landscape, competitive dynamics, and evolving demographics. We explore the influence of mergers and acquisitions (M&A) activity, providing both quantitative (market share, M&A deal volumes) and qualitative (innovation barriers) insights.

Market Concentration: The Asia-Pacific car insurance market exhibits a moderately concentrated structure, with key players like Ping An Insurance, MS&AD Insurance Group, and Allianz Asia Pacific holding significant market shares. However, the presence of numerous regional and smaller insurers indicates a competitive landscape. The combined market share of the top 5 players is estimated at xx%.

Technological Innovation: The market is experiencing rapid technological advancements, driven by the integration of telematics, AI, and big data analytics. These innovations are enabling personalized pricing, risk assessment, and fraud detection, shaping the future of car insurance. However, challenges remain in data security and the cost of implementing new technologies.

Regulatory Framework: Varying regulatory frameworks across the Asia-Pacific region influence market dynamics. Stringent regulations in certain countries create barriers to entry for new players, while others offer more flexible environments. Compliance costs and differing regulatory requirements across jurisdictions pose significant challenges.

Competitive Product Substitutes: The emergence of alternative risk-sharing models and peer-to-peer insurance platforms poses a growing threat to traditional car insurers. The impact of these innovative solutions on market share is expected to increase to xx% by 2033.

End-User Demographics: The expanding middle class and rising vehicle ownership in several Asia-Pacific countries are major growth drivers. Changing consumer preferences, particularly among younger demographics who favor digital channels, are reshaping distribution strategies.

M&A Trends: Consolidation through mergers and acquisitions remains a significant trend, with a projected xx M&A deals anticipated in the forecast period. These deals are aimed at expanding market reach, enhancing technological capabilities, and optimizing operational efficiency.

Asia-Pacific Car Insurance Market Growth Trends & Insights

This section analyzes the evolution of the Asia-Pacific car insurance market size, adoption rates, technological disruptions, and shifts in consumer behavior from 2019 to 2033. Utilizing comprehensive data, this analysis reveals key trends and provides valuable insights into future market potential. The market is projected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period, driven primarily by factors such as rising vehicle ownership, increasing urbanization, and the growing adoption of insurance products.

Dominant Regions, Countries, or Segments in Asia-Pacific Car Insurance Market

This section identifies the leading regions, countries, and segments (by application, distribution channel, and coverage type) within the Asia-Pacific car insurance market. We analyze the factors driving their dominance, including market share, growth potential, and underlying economic and infrastructural drivers.

By Country: China, India, and Japan are the leading markets, accounting for xx% of the total market size in 2025. China's robust economic growth and increasing vehicle ownership significantly contribute to its dominance. India's expanding middle class and rising insurance penetration are other factors. Japan maintains a significant market presence due to its mature automotive industry and high insurance penetration rates.

By Application: The Personal Vehicles segment dominates the market, with a projected market share of xx% in 2025, driven by the rise in private car ownership across the region. The Commercial Vehicles segment is experiencing steady growth, fueled by increasing logistics and transportation activities.

By Distribution Channel: Online and individual agents are the primary distribution channels, each holding approximately xx% and xx% of the market share respectively in 2025. The increasing adoption of digital platforms and the reach of individual agents contribute to their significant market share.

By Coverage: Third-Party Liability Coverage represents a significant portion of the market, however the Collision/Comprehensive/Other Optional Coverage segment is experiencing faster growth, reflecting the increasing awareness of comprehensive protection among consumers.

Asia-Pacific Car Insurance Market Product Landscape

The Asia-Pacific car insurance market is witnessing a surge in product innovation, driven by technological advancements and evolving customer needs. Insurers are developing innovative products featuring telematics, usage-based insurance, and AI-powered risk assessment. These products offer customized pricing, real-time monitoring, and enhanced customer experience. The unique selling propositions of these new products include lower premiums for safer drivers, personalized risk assessment and more transparent pricing.

Key Drivers, Barriers & Challenges in Asia-Pacific Car Insurance Market

Key Drivers:

- Rising vehicle ownership and increasing urbanization.

- Growing awareness of the importance of car insurance.

- Favorable government policies and regulations.

- Technological advancements such as telematics and AI.

Key Barriers and Challenges:

- Intense competition among established players.

- High operating costs, especially in emerging markets.

- Regulatory hurdles and compliance requirements.

- Fraudulent claims.

Emerging Opportunities in Asia-Pacific Car Insurance Market

Several emerging opportunities exist in the Asia-Pacific car insurance market, including:

- Expanding into untapped rural markets.

- Leveraging innovative technologies like blockchain and IoT.

- Developing tailored products for specific customer segments.

- Capitalizing on the growth of ride-hailing services.

Growth Accelerators in the Asia-Pacific Car Insurance Market Industry

Long-term growth in the Asia-Pacific car insurance market will be fueled by technological breakthroughs in AI and predictive analytics, strategic partnerships between insurers and technology providers, and expansion into new markets with high growth potential. The development of comprehensive, data-driven insurance solutions will drive market penetration.

Key Players Shaping the Asia-Pacific Car Insurance Market Market

- Ping An Insurance

- MS&AD Insurance Group

- HDFC ERGO General Insurance

- Allianz Asia Pacific

- AIA Group Limited

- Zurich Insurance Group

- PICC

- Tokio Marine

- Sompo Japan Nipponkoa Insurance

- National Insurance Company

- TATA AIG General Insurance

- Bajaj Allianz General Insurance

- SBI General Insurance

- IAG (Insurance Australia Group)

Notable Milestones in Asia-Pacific Car Insurance Market Sector

- July 2022: Edelweiss General Insurance launched 'Switch,' a fully digital, telematics-based motor insurance policy, expanding the use of real-time driving scores for dynamic premium calculations.

- July 2023: Lexasure Financial Group partnered with My Car Consultant Pte. Ltd. to offer data-driven, self-insured car insurance in South and Southeast Asia.

In-Depth Asia-Pacific Car Insurance Market Market Outlook

The Asia-Pacific car insurance market presents significant long-term growth potential, driven by the confluence of factors discussed in this report. Strategic partnerships, technological innovation, and expansion into untapped markets will be crucial for success. The market is poised for significant expansion, presenting substantial opportunities for both established players and new entrants.

Asia-Pacific Car Insurance Market Segmentation

-

1. Coverage

- 1.1. Third-Party Liability Coverage

- 1.2. Collision/Comprehensive/Other Optional Coverage

-

2. Application

- 2.1. Personal Vehicles

- 2.2. Commercial Vehicles

-

3. Distribution Channel

- 3.1. Direct Sales

- 3.2. Individual Agents

- 3.3. Brokers

- 3.4. Banks

- 3.5. Online

- 3.6. Other Distribution Channels

Asia-Pacific Car Insurance Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia-Pacific Car Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.45% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Sales of Cars in the Region; China and India Driving the Market with Higher Car Accident Events

- 3.3. Market Restrains

- 3.3.1. Lower Value of Non Life Insurance Penetration in the Region; Decline in Car Insurance Premium Rates with Government Regulations

- 3.4. Market Trends

- 3.4.1. China Leading the Asia Pacific Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Asia-Pacific Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 5.1.1. Third-Party Liability Coverage

- 5.1.2. Collision/Comprehensive/Other Optional Coverage

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Personal Vehicles

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Direct Sales

- 5.3.2. Individual Agents

- 5.3.3. Brokers

- 5.3.4. Banks

- 5.3.5. Online

- 5.3.6. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 6. China Asia-Pacific Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 7. Japan Asia-Pacific Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 8. India Asia-Pacific Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 9. South Korea Asia-Pacific Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 10. Taiwan Asia-Pacific Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 11. Australia Asia-Pacific Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Asia-Pacific Asia-Pacific Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Ping An Insurance

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 MS&AD Insurance Group

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 HDFC ERGO General Insurance

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Allianz Asia Pacific

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 AIA Group Limited

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Zurich Insurance Group

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 PICC

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Tokio Marine

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Sompo Japan Nipponkoa Insurance

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 National Insurance Company

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 TATA AIG General Insurance**List Not Exhaustive

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Bajaj Allianz General Insurance

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.13 SBI General Insurance

- 13.2.13.1. Overview

- 13.2.13.2. Products

- 13.2.13.3. SWOT Analysis

- 13.2.13.4. Recent Developments

- 13.2.13.5. Financials (Based on Availability)

- 13.2.14 IAG (Insurance Australia Group)

- 13.2.14.1. Overview

- 13.2.14.2. Products

- 13.2.14.3. SWOT Analysis

- 13.2.14.4. Recent Developments

- 13.2.14.5. Financials (Based on Availability)

- 13.2.1 Ping An Insurance

List of Figures

- Figure 1: Asia-Pacific Car Insurance Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Asia-Pacific Car Insurance Market Share (%) by Company 2024

List of Tables

- Table 1: Asia-Pacific Car Insurance Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Asia-Pacific Car Insurance Market Revenue Million Forecast, by Coverage 2019 & 2032

- Table 3: Asia-Pacific Car Insurance Market Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Asia-Pacific Car Insurance Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 5: Asia-Pacific Car Insurance Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Asia-Pacific Car Insurance Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: China Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Japan Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: India Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: South Korea Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Taiwan Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Australia Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Asia-Pacific Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Asia-Pacific Car Insurance Market Revenue Million Forecast, by Coverage 2019 & 2032

- Table 15: Asia-Pacific Car Insurance Market Revenue Million Forecast, by Application 2019 & 2032

- Table 16: Asia-Pacific Car Insurance Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 17: Asia-Pacific Car Insurance Market Revenue Million Forecast, by Country 2019 & 2032

- Table 18: China Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Japan Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: South Korea Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: India Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Australia Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: New Zealand Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Indonesia Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Malaysia Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Singapore Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Thailand Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Vietnam Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Philippines Asia-Pacific Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Car Insurance Market?

The projected CAGR is approximately 5.45%.

2. Which companies are prominent players in the Asia-Pacific Car Insurance Market?

Key companies in the market include Ping An Insurance, MS&AD Insurance Group, HDFC ERGO General Insurance, Allianz Asia Pacific, AIA Group Limited, Zurich Insurance Group, PICC, Tokio Marine, Sompo Japan Nipponkoa Insurance, National Insurance Company, TATA AIG General Insurance**List Not Exhaustive, Bajaj Allianz General Insurance, SBI General Insurance, IAG (Insurance Australia Group).

3. What are the main segments of the Asia-Pacific Car Insurance Market?

The market segments include Coverage, Application , Distribution Channel .

4. Can you provide details about the market size?

The market size is estimated to be USD 181.18 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Sales of Cars in the Region; China and India Driving the Market with Higher Car Accident Events.

6. What are the notable trends driving market growth?

China Leading the Asia Pacific Market.

7. Are there any restraints impacting market growth?

Lower Value of Non Life Insurance Penetration in the Region; Decline in Car Insurance Premium Rates with Government Regulations.

8. Can you provide examples of recent developments in the market?

July 2022: Edelweiss General Insurance launched a comprehensive motor insurance product named 'Switch' which exists as a fully digital, mobile telematics-based motor policy that detects motion and automatically activates insurance when the vehicle is driven. This resulted in further expansion toward real-time driving scores and dynamically calculated premium-based car insurance services.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Car Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Car Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Car Insurance Market?

To stay informed about further developments, trends, and reports in the Asia-Pacific Car Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence