Key Insights

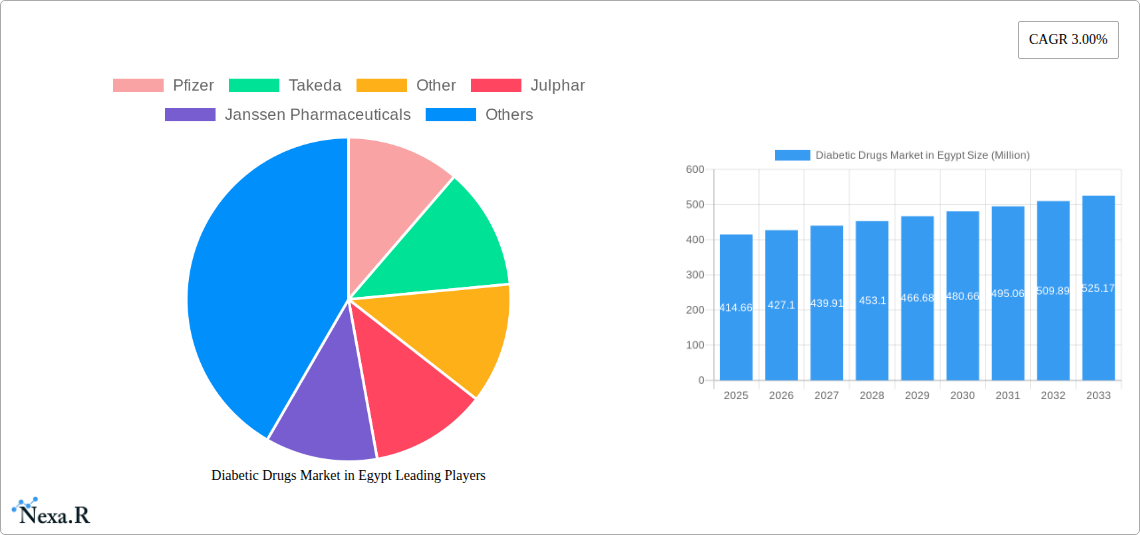

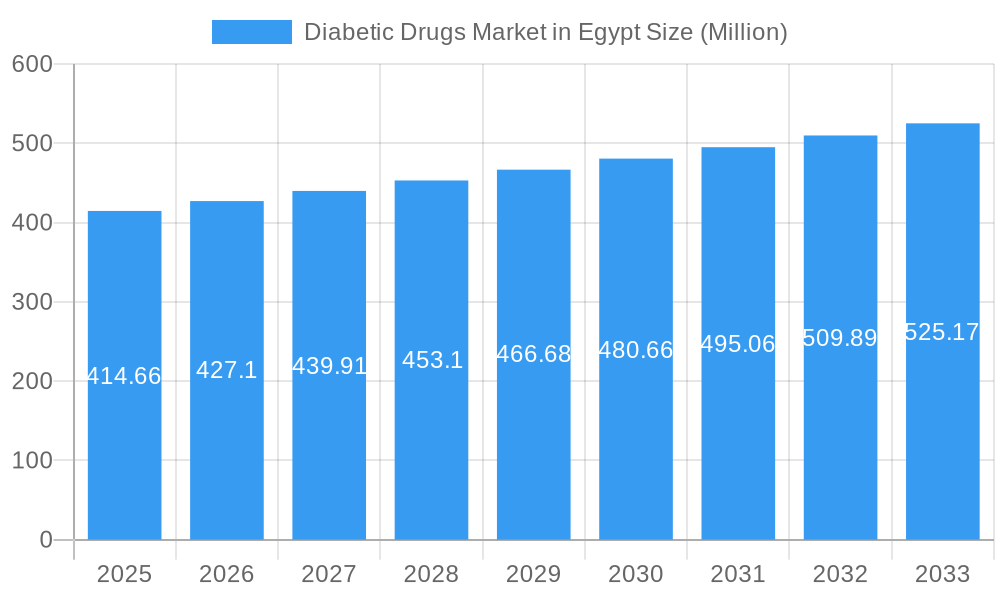

The Egyptian diabetic drugs market is poised for steady growth, projected to reach approximately USD 414.66 million by 2025 with a Compound Annual Growth Rate (CAGR) of 3.00% through 2033. This expansion is primarily driven by the escalating prevalence of diabetes, particularly Type 2 diabetes, within the nation. The increasing adoption of advanced therapeutic options such as non-insulin injectables and oral antidiabetic drugs (OADs) is also a significant catalyst. Furthermore, evolving treatment guidelines and a growing awareness among healthcare professionals and patients regarding the benefits of timely and effective diabetes management contribute to market dynamism. The distribution channels are also evolving, with a notable increase in demand through online retailers alongside established hospital and pharmacy networks. This shift reflects changing consumer behavior and the increasing accessibility of healthcare products.

Diabetic Drugs Market in Egypt Market Size (In Million)

The market's growth, however, faces certain restraints. These include the high cost of some advanced diabetic medications, which can limit accessibility for a segment of the population, and potential reimbursement challenges within the healthcare system. Nonetheless, the robust pipeline of new drug developments and the continuous innovation in diabetes care are expected to mitigate these restraints. Key players like Novo Nordisk A/S, Sanofi Aventis, and Eli Lilly are actively engaged in the Egyptian market, offering a diverse portfolio of insulins, OADs, and non-insulin injectables to address the varied needs of diabetic patients across different therapeutic areas. The focus on improving patient outcomes and managing the long-term complications of diabetes will continue to shape market strategies and product offerings in Egypt.

Diabetic Drugs Market in Egypt Company Market Share

Here is a comprehensive, SEO-optimized report description for the Diabetic Drugs Market in Egypt, designed for maximum visibility and engagement:

Gain unparalleled insights into Egypt's burgeoning diabetic drugs market with this in-depth report. Analyzing the landscape from 2019 to 2033, with a base and estimated year of 2025, this report dissects market dynamics, growth trends, product segmentation, and key players. Uncover the impact of insulins, oral antidiabetics (OADs), and non-insulin injectables across Type 1 and Type 2 diabetes treatment. Explore distribution channels, from hospitals to online retailers, and understand the strategic moves of industry giants like Novo Nordisk, Pfizer, and Takeda. This report provides a critical roadmap for manufacturers, distributors, investors, and policymakers navigating the Egyptian pharmaceutical sector, focusing on high-traffic keywords such as "Egypt diabetes treatment," "Egyptian pharmaceutical market," "insulin Egypt," "diabetes medication Egypt," and "pharmaceutical industry Egypt."

Diabetic Drugs Market in Egypt Market Dynamics & Structure

The diabetic drugs market in Egypt is characterized by a moderate to high market concentration, with a few key global players holding significant shares, alongside a growing presence of local manufacturers. Technological innovation is a primary driver, with continuous research and development focused on more effective and patient-friendly drug formulations, including novel oral agents and advanced insulin delivery systems. Regulatory frameworks, overseen by the Egyptian Drug Authority (EDA), play a crucial role in approving new drugs and ensuring quality standards, impacting market access and competition. Competitive product substitutes are abundant, ranging from traditional OADs to newer biological therapies. End-user demographics are shifting towards an aging population and an increasing prevalence of lifestyle-related chronic diseases, expanding the patient pool. Merger and acquisition (M&A) trends are present, albeit less frequent than in more mature markets, often involving strategic partnerships or acquisitions by larger entities seeking to expand their therapeutic portfolios or market reach within Egypt.

- Market Concentration: Dominated by global pharmaceutical giants alongside emerging local players.

- Technological Innovation: Driven by R&D in novel formulations, delivery systems, and personalized medicine.

- Regulatory Influence: EDA's oversight crucial for drug approval, pricing, and market entry.

- Competitive Landscape: Diverse range of OADs, insulins, and non-insulin injectables offering significant choice.

- End-User Demographics: Growing demand driven by an aging population and rising incidence of diabetes.

- M&A Trends: Strategic partnerships and consolidations aimed at portfolio expansion and market penetration.

Diabetic Drugs Market in Egypt Growth Trends & Insights

The Egyptian diabetic drugs market is poised for robust growth, driven by a confluence of factors including increasing diabetes prevalence, rising healthcare expenditure, and a growing awareness among the population about diabetes management. The market size is projected to expand significantly from an estimated value of $XXX million units in 2025, with a projected Compound Annual Growth Rate (CAGR) of XX% over the forecast period of 2025–2033. Adoption rates for advanced therapies, such as GLP-1 receptor agonists and SGLT2 inhibitors, are steadily increasing as physicians and patients become more aware of their efficacy in glycemic control and cardiovascular benefits. Technological disruptions, including the development of biosimilars for blockbuster biologics and the increasing accessibility of digital health platforms for diabetes management, are further shaping the market landscape. Consumer behavior is shifting towards a greater demand for convenience, personalized treatment plans, and drugs with fewer side effects. The historical period of 2019–2024 saw steady growth, laying the foundation for accelerated expansion. Factors such as government initiatives to improve healthcare infrastructure and affordability are also contributing to increased market penetration. The focus on early diagnosis and proactive management of diabetes is leading to a higher demand for a wider range of therapeutic options, from basic insulins to more complex treatment regimens. The rising disposable income in certain segments of the Egyptian population also allows for greater expenditure on advanced and potentially more expensive diabetes medications.

Dominant Regions, Countries, or Segments in Diabetic Drugs Market in Egypt

The Type 2 diabetes segment is the undisputed leader within the Egyptian diabetic drugs market, mirroring global trends in the prevalence of this chronic condition. This dominance is driven by a combination of lifestyle factors, including changing dietary habits and sedentary lifestyles, coupled with an aging population. The market share for Type 2 diabetes treatments is estimated to be approximately XX% of the overall diabetic drugs market in Egypt. Within the Product Type segmentation, Oral Antidiabetics (OADs) command a significant portion due to their established efficacy, affordability, and ease of administration for a vast majority of Type 2 diabetes patients. Insulins, while crucial, cater to a more specific patient population within Type 2 diabetes and the entirety of Type 1 diabetes. Non-insulin injectables are gaining traction, especially among patients requiring more advanced glycemic control or those benefiting from the added advantages of certain drug classes like GLP-1 RAs.

The pharmacies distribution channel currently holds the largest market share, providing accessible and convenient access to a wide range of diabetic medications for the general population. However, the hospitals segment plays a vital role in managing complex diabetes cases, administering specialized treatments, and providing patient education. The online retailers segment is an emerging force, experiencing rapid growth due to the increasing adoption of e-commerce and a growing demand for home delivery services, particularly in urban centers. Economic policies promoting domestic pharmaceutical manufacturing and import substitution are indirectly influencing the market by potentially increasing the availability and affordability of certain drug classes. Infrastructure development, particularly in healthcare facilities and logistics, further supports the growth and accessibility of diabetic drugs across different regions of Egypt. The expanding middle class with higher disposable incomes is also a key driver for the increased consumption of both traditional and novel diabetic medications, further solidifying the dominance of Type 2 diabetes treatments and OADs.

Diabetic Drugs Market in Egypt Product Landscape

The product landscape of the diabetic drugs market in Egypt is characterized by a robust offering of both generic and branded medications. Insulins, ranging from rapid-acting to long-acting formulations, are a cornerstone of treatment for a significant portion of the diabetic population. Oral antidiabetics (OADs) encompass a broad spectrum of drug classes, including biguanides (e.g., Metformin), sulfonylureas, DPP-4 inhibitors, and SGLT2 inhibitors, each offering distinct mechanisms of action and therapeutic benefits. Non-insulin injectables, particularly GLP-1 receptor agonists, are witnessing increased adoption due to their potent glucose-lowering effects and weight management benefits. Innovations are geared towards improving patient convenience, reducing side effects, and offering combination therapies. The market is seeing a steady introduction of biosimilars, providing more affordable alternatives to biologic drugs.

Key Drivers, Barriers & Challenges in Diabetic Drugs Market in Egypt

Key Drivers:

- Rising Diabetes Prevalence: Egypt faces a growing burden of diabetes, fueled by lifestyle changes and an aging population, creating a consistent demand for diabetic medications.

- Increasing Healthcare Expenditure: Government and private sector investments in healthcare infrastructure and public health initiatives are expanding access to treatments.

- Technological Advancements: Development of novel drug formulations, improved delivery systems, and personalized treatment approaches are driving market growth.

- Awareness and Education: Growing public and professional awareness regarding diabetes management and the benefits of newer therapies.

Barriers & Challenges:

- Affordability and Accessibility: The cost of advanced diabetic drugs can be a significant barrier for a large segment of the population, impacting access.

- Regulatory Hurdles: Stringent drug approval processes and pricing regulations can slow down market entry for new products.

- Supply Chain Complexities: Ensuring consistent availability and efficient distribution of drugs across a large and diverse geographic area presents logistical challenges.

- Competition from Counterfeit Products: The presence of counterfeit or substandard drugs can undermine market trust and patient safety, impacting legitimate manufacturers.

Emerging Opportunities in Diabetic Drugs Market in Egypt

Emerging opportunities in the Egyptian diabetic drugs market lie in the increasing demand for combination therapies that offer improved efficacy and patient compliance. The growing interest in preventive medicine and early intervention presents a fertile ground for drugs that target pre-diabetes or offer robust cardiovascular protection. Furthermore, the rise of digital health platforms and telemedicine opens avenues for innovative drug delivery and patient monitoring solutions. There is also an untapped market for specialized diabetic medications catering to specific patient sub-groups with co-morbidities. The increasing focus on patient-centric care and the development of patient support programs can also create a competitive advantage for pharmaceutical companies.

Growth Accelerators in the Diabetic Drugs Market in Egypt Industry

Several catalysts are accelerating the long-term growth of the diabetic drugs market in Egypt. Technological breakthroughs in pharmaceutical R&D, leading to the development of more effective and safer medications, are paramount. Strategic partnerships between global pharmaceutical giants and local Egyptian companies can foster knowledge transfer, enhance manufacturing capabilities, and improve market access. Government initiatives focused on improving public health infrastructure, promoting domestic production, and increasing drug affordability will significantly boost market expansion. The continuous rise in the prevalence of diabetes, both Type 1 and Type 2, ensures sustained demand for a broad range of therapeutic interventions. Furthermore, the increasing adoption of advanced treatment modalities and a growing emphasis on diabetes prevention programs are key accelerators.

Key Players Shaping the Diabetic Drugs Market in Egypt Market

- Pfizer

- Takeda

- Julphar

- Janssen Pharmaceuticals

- Eli Lilly

- Novartis

- Merck and Co

- AstraZeneca

- Sanofi Aventis

- Bristol Myers Squibb

- Novo Nordisk A/S

- Boehringer Ingelheim

- Astellas

Notable Milestones in Diabetic Drugs Market in Egypt Sector

- November 2023: Novo Nordisk initiated a Phase III comparative trial for their pipeline drug CagriSema against the recently approved Zepbound, indicating potential direct competition in the future market.

- October 2022: Memoranda of Understanding worth AED 260 million (USD 70.8 million) were signed between major pharmaceutical and medical device companies in the UAE, aligning with national strategies to attract investors and manufacturers to the pharmaceutical and medical equipment sectors. Under a separate MoU, PureHealth and Gulf Pharmaceutical Industries Company will establish the first factory in the Middle East to produce Glargine to treat diabetes.

In-Depth Diabetic Drugs Market in Egypt Market Outlook

The future outlook for the diabetic drugs market in Egypt is exceptionally promising, driven by sustained demand and ongoing innovation. Growth accelerators such as advancements in personalized medicine and the increasing adoption of biosimilars will further enhance treatment efficacy and affordability. Strategic collaborations and government support for local manufacturing are expected to bolster the market's resilience and competitive edge. The persistent rise in diabetes prevalence, coupled with a growing focus on integrated healthcare solutions, positions Egypt as a key market for pharmaceutical companies looking to address the unmet needs of diabetic patients. The market is anticipated to witness continued expansion, offering significant opportunities for stakeholders to contribute to improving diabetes care outcomes.

Diabetic Drugs Market in Egypt Segmentation

-

1. Product Type

- 1.1. Insulins

- 1.2. OADs

- 1.3. non-insulin injectables

-

2. Therapeutic Area

- 2.1. Type 1 diabetes

- 2.2. Type 2 diabetes

-

3. Distribution Channel

- 3.1. Hospitals

- 3.2. pharmacies

- 3.3. online retailers

Diabetic Drugs Market in Egypt Segmentation By Geography

- 1. Egypt

Diabetic Drugs Market in Egypt Regional Market Share

Geographic Coverage of Diabetic Drugs Market in Egypt

Diabetic Drugs Market in Egypt REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Insulins

- 5.1.2. OADs

- 5.1.3. non-insulin injectables

- 5.2. Market Analysis, Insights and Forecast - by Therapeutic Area

- 5.2.1. Type 1 diabetes

- 5.2.2. Type 2 diabetes

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Hospitals

- 5.3.2. pharmacies

- 5.3.3. online retailers

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Egypt

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Diabetic Drugs Market in Egypt Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Insulins

- 6.1.2. OADs

- 6.1.3. non-insulin injectables

- 6.2. Market Analysis, Insights and Forecast - by Therapeutic Area

- 6.2.1. Type 1 diabetes

- 6.2.2. Type 2 diabetes

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Hospitals

- 6.3.2. pharmacies

- 6.3.3. online retailers

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Pfizer

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Takeda

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Other

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Julphar

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Janssen Pharmaceuticals

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Eli Lilly

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Novartis

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Merck and Co

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AstraZeneca

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Sanofi Aventis

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Bristol Myers Squibb

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Novo Nordisk A/S

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Boehringer Ingelheim

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Sanofi Aventis

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Astellas

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 Pfizer

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Global Diabetic Drugs Market in Egypt Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Diabetic Drugs Market in Egypt Volume Breakdown (Egypt, %) by Region 2025 & 2033

- Figure 3: Egypt Diabetic Drugs Market in Egypt Revenue (Million), by Product Type 2025 & 2033

- Figure 4: Egypt Diabetic Drugs Market in Egypt Volume (Egypt), by Product Type 2025 & 2033

- Figure 5: Egypt Diabetic Drugs Market in Egypt Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: Egypt Diabetic Drugs Market in Egypt Volume Share (%), by Product Type 2025 & 2033

- Figure 7: Egypt Diabetic Drugs Market in Egypt Revenue (Million), by Therapeutic Area 2025 & 2033

- Figure 8: Egypt Diabetic Drugs Market in Egypt Volume (Egypt), by Therapeutic Area 2025 & 2033

- Figure 9: Egypt Diabetic Drugs Market in Egypt Revenue Share (%), by Therapeutic Area 2025 & 2033

- Figure 10: Egypt Diabetic Drugs Market in Egypt Volume Share (%), by Therapeutic Area 2025 & 2033

- Figure 11: Egypt Diabetic Drugs Market in Egypt Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 12: Egypt Diabetic Drugs Market in Egypt Volume (Egypt), by Distribution Channel 2025 & 2033

- Figure 13: Egypt Diabetic Drugs Market in Egypt Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 14: Egypt Diabetic Drugs Market in Egypt Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 15: Egypt Diabetic Drugs Market in Egypt Revenue (Million), by Country 2025 & 2033

- Figure 16: Egypt Diabetic Drugs Market in Egypt Volume (Egypt), by Country 2025 & 2033

- Figure 17: Egypt Diabetic Drugs Market in Egypt Revenue Share (%), by Country 2025 & 2033

- Figure 18: Egypt Diabetic Drugs Market in Egypt Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Product Type 2020 & 2033

- Table 3: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Therapeutic Area 2020 & 2033

- Table 4: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Therapeutic Area 2020 & 2033

- Table 5: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Distribution Channel 2020 & 2033

- Table 7: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Region 2020 & 2033

- Table 9: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Product Type 2020 & 2033

- Table 10: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Product Type 2020 & 2033

- Table 11: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Therapeutic Area 2020 & 2033

- Table 12: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Therapeutic Area 2020 & 2033

- Table 13: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 14: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Distribution Channel 2020 & 2033

- Table 15: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diabetic Drugs Market in Egypt?

The projected CAGR is approximately 3.00%.

2. Which companies are prominent players in the Diabetic Drugs Market in Egypt?

Key companies in the market include Pfizer, Takeda, Other, Julphar, Janssen Pharmaceuticals, Eli Lilly, Novartis, Merck and Co, AstraZeneca, Sanofi Aventis, Bristol Myers Squibb, Novo Nordisk A/S, Boehringer Ingelheim, Sanofi Aventis, Astellas.

3. What are the main segments of the Diabetic Drugs Market in Egypt?

The market segments include Product Type, Therapeutic Area, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 414.66 Million as of 2022.

5. What are some drivers contributing to market growth?

; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies.

6. What are the notable trends driving market growth?

The oral anti-diabetic drugs segment holds the highest market share in the Egypt Diabetes Drugs Market in the current year.

7. Are there any restraints impacting market growth?

; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures. Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products.

8. Can you provide examples of recent developments in the market?

Novmber 2023: Novo Nordisk's initiation of a Phase III comparative trial for their pipeline drug CagriSema against the recently approved Zepbound suggests the potential for direct competition between the two drugs upon Novo Nordisk's candidate entering the market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Egypt.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Diabetic Drugs Market in Egypt," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Diabetic Drugs Market in Egypt report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Diabetic Drugs Market in Egypt?

To stay informed about further developments, trends, and reports in the Diabetic Drugs Market in Egypt, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence