Key Insights

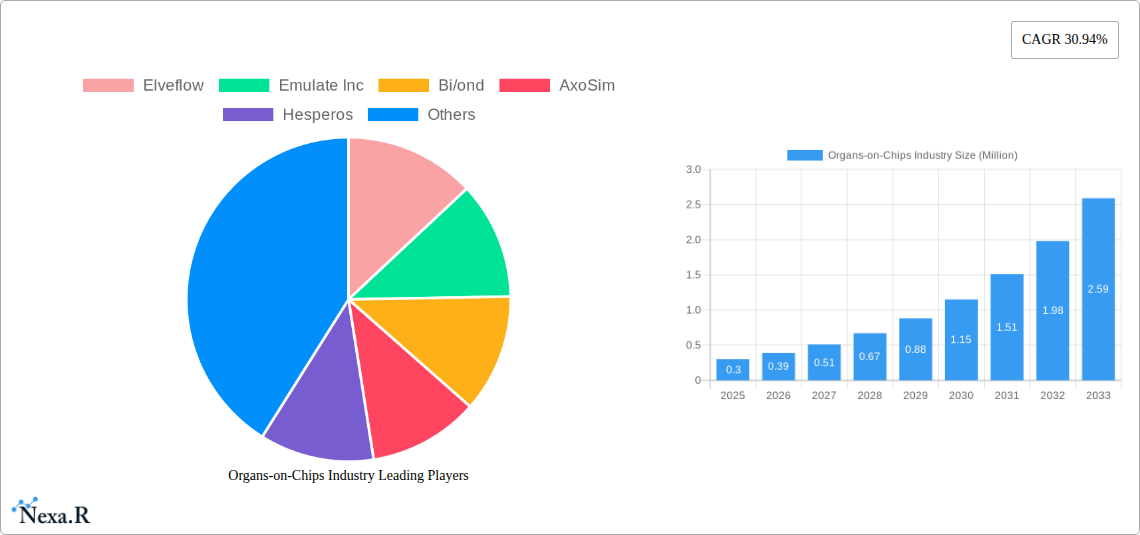

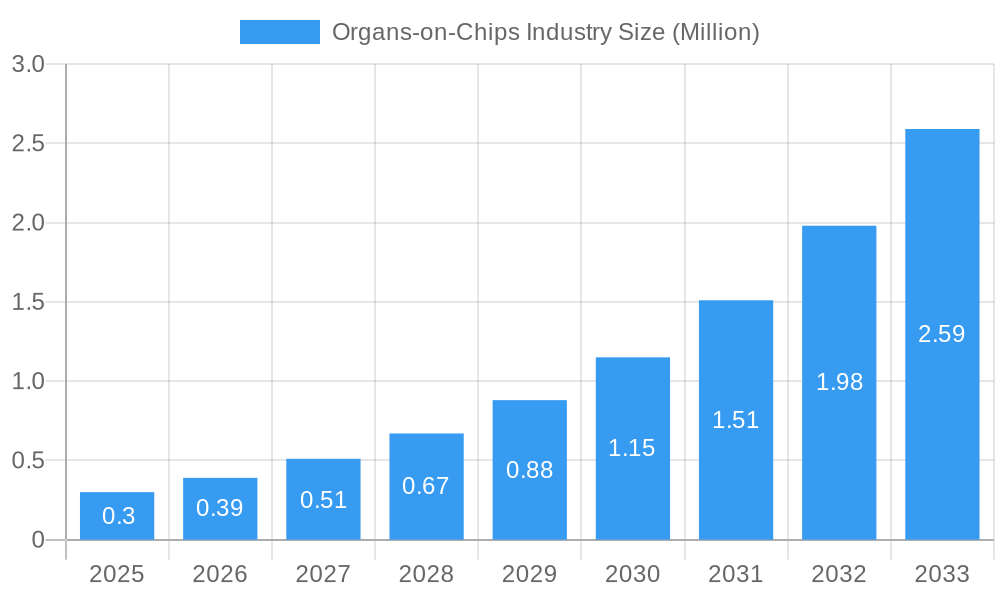

The Organs-on-Chips market is poised for explosive growth, currently valued at $0.3 million in 2025 and projected to surge at an impressive Compound Annual Growth Rate (CAGR) of 30.94% through 2033. This remarkable expansion is primarily fueled by the increasing demand for more accurate and predictive preclinical testing models that can reduce the reliance on traditional animal testing. Key drivers include the rising prevalence of chronic diseases, necessitating advanced research and development for novel therapeutics, and the growing ethical concerns surrounding animal welfare in scientific experimentation. Furthermore, significant advancements in microfluidics, cell culture technologies, and biosensor integration are enabling the creation of highly sophisticated and physiologically relevant organ models. This technological evolution is critical in enhancing the predictive power of these in-vitro systems, making them indispensable tools for drug discovery, toxicology research, and personalized medicine. The industry's ability to accurately recapitulate human organ functions offers a transformative approach to understanding disease mechanisms and evaluating drug efficacy and safety.

Organs-on-Chips Industry Market Size (In Million)

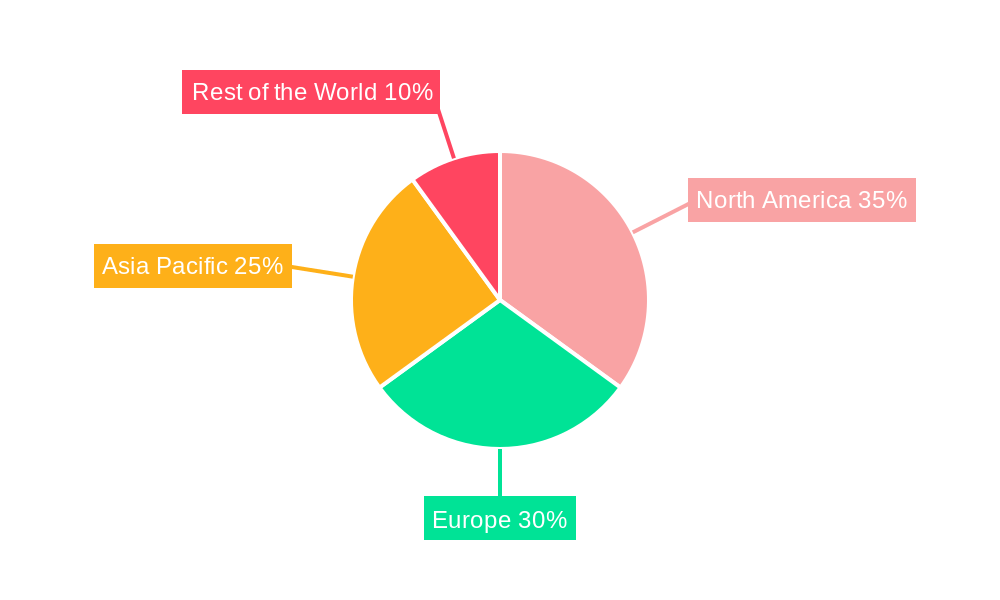

The market is segmented across various organ types, including Liver, Heart, and Lung, each catering to specific research needs, with "Other Organ Types" also representing significant development. Applications are broadly categorized into Drug Discovery, Toxicology Research, and Other Applications, underscoring the versatility of this technology. The end-user landscape is dominated by Pharmaceutical and Biotechnology Companies and Academic and Research Institutes, who are actively investing in and adopting these advanced research tools. Geographically, North America is expected to lead the market, driven by substantial R&D investments and a strong presence of leading biopharmaceutical firms. Asia Pacific, with its rapidly expanding healthcare infrastructure and increasing research collaborations, is anticipated to exhibit the fastest growth. Emerging trends include the development of multi-organ chips for simulating systemic effects, increased automation and miniaturization for high-throughput screening, and integration with artificial intelligence for data analysis. However, challenges such as the high initial cost of development and the need for standardization and regulatory acceptance may present some restraints to market penetration.

Organs-on-Chips Industry Company Market Share

This comprehensive report provides an in-depth analysis of the global Organs-on-Chips (OoC) industry, forecasting market evolution from 2019–2033, with a base and estimated year of 2025, and a forecast period of 2025–2033, built upon historical data from 2019–2024. We explore the intricate dynamics of this transformative technology, covering market size, growth trends, regional dominance, product landscape, key drivers, barriers, emerging opportunities, growth accelerators, and the influential companies shaping its future. This report is essential for pharmaceutical and biotechnology companies, academic and research institutes, and investors seeking to understand the burgeoning potential of organoids, microfluidic devices, and advanced biological models in preclinical research.

Organs-on-Chips Industry Market Dynamics & Structure

The Organs-on-Chips (OoC) industry is characterized by a moderately concentrated market structure, driven by rapid technological advancements and increasing demand for more predictive preclinical models. Key players are investing heavily in research and development to enhance the complexity and functionality of OoC systems, aiming to replicate human physiology with greater fidelity. Technological innovation is the primary driver, with advancements in microfluidics, 3D bioprinting, and cell culture techniques continuously pushing the boundaries of OoC capabilities. Regulatory frameworks are slowly evolving to recognize the potential of OoC as valid alternatives to animal testing, particularly in drug discovery and toxicology. Competitive product substitutes include traditional animal models and 2D cell cultures, but OoC offer significant advantages in terms of human relevance and reduced animal use. End-user demographics are predominantly concentrated within pharmaceutical and biotechnology companies, followed by academic and research institutes, all seeking to de-risk drug development and accelerate time-to-market. Mergers and acquisitions (M&A) are a growing trend, as larger entities aim to integrate OoC technologies into their existing R&D pipelines. For instance, the acquisition of TARA Biosystems by Valo Health in April 2022 exemplifies this consolidation, integrating advanced heart tissue modeling into a broader drug development platform.

- Market Concentration: Moderate, with increasing M&A activity.

- Technological Innovation Drivers: Microfluidics, 3D bioprinting, advanced cell culture.

- Regulatory Frameworks: Evolving, with increasing acceptance for preclinical applications.

- Competitive Product Substitutes: Animal models, 2D cell cultures.

- End-User Demographics: Primarily Pharmaceutical & Biotechnology Companies, Academic & Research Institutes.

- M&A Trends: Increasing, driven by strategic integration of OoC capabilities.

Organs-on-Chips Industry Growth Trends & Insights

The global Organs-on-Chips (OoC) market is poised for substantial growth, projected to reach an estimated value of $3,500 million by 2025. This expansion is fueled by an escalating need for more accurate and human-relevant preclinical models, driven by the inherent limitations of traditional animal testing and 2D cell cultures. The adoption rates of OoC technologies are steadily increasing across pharmaceutical, biotechnology, and academic research sectors, as scientists recognize their ability to predict drug efficacy and toxicity with greater precision. Technological disruptions, such as the development of multi-organ chips and more sophisticated perfusion systems, are further enhancing the predictive power of these platforms. Consumer behavior shifts, particularly the growing ethical concern around animal testing and a demand for faster, more cost-effective drug development, are also contributing to market momentum. The market penetration of OoC, while still in its nascent stages compared to established methodologies, is accelerating rapidly. The Compound Annual Growth Rate (CAGR) for the forecast period 2025–2033 is estimated at an impressive 22.5%, signifying a robust upward trajectory. This growth is underpinned by increasing investments in R&D and a burgeoning understanding of the complex biological interactions that OoC can replicate. The evolution of OoC from single-organ to multi-organ systems, coupled with advanced data analytics, promises to revolutionize how new therapeutics are discovered and validated.

Dominant Regions, Countries, or Segments in Organs-on-Chips Industry

The North America region currently dominates the Organs-on-Chips (OoC) market, driven by a robust pharmaceutical and biotechnology ecosystem, significant government funding for life sciences research, and a proactive regulatory environment that encourages innovation. Within North America, the United States stands out as the leading country, home to numerous pioneering OoC companies and major research institutions. The dominant segment driving this growth is Drug Discovery, where OoC are instrumental in identifying lead compounds, evaluating drug efficacy, and predicting potential adverse effects, thereby reducing the high attrition rates seen in traditional drug development pipelines.

Leading Region: North America

- Key Country: United States

- Dominant Application Segment: Drug Discovery

- Market Share Contribution: Estimated at 45% in 2025.

- Growth Potential: Driven by the increasing demand for personalized medicine and novel therapeutic approaches.

- Key Drivers: High R&D expenditure by pharmaceutical giants, presence of leading OoC developers, and strong academic-biotech collaborations.

- Economic Policies: Favorable venture capital funding and government grants supporting life science innovation.

- Infrastructure: Advanced research facilities and a skilled scientific workforce.

Dominant Organ Type: Liver organ-on-a-chip models are particularly prevalent due to the liver's central role in drug metabolism and toxicity.

- Market Share Contribution: Estimated at 30% of the organ type segment in 2025.

- Growth Potential: Crucial for predicting hepatotoxicity of drug candidates.

Dominant End User: Pharmaceutical and Biotechnology Companies represent the largest end-user segment.

- Market Share Contribution: Estimated at 60% in 2025.

- Growth Potential: Their continuous need to streamline drug development pipelines and reduce costs fuels the adoption of OoC.

The European market, particularly Germany and the UK, is also a significant contributor, bolstered by strong academic research and a growing number of OoC startups. Asia-Pacific is emerging as a key growth area, driven by increasing investments in biopharmaceutical R&D and a growing emphasis on reducing animal testing.

Organs-on-Chips Industry Product Landscape

The Organs-on-Chips (OoC) product landscape is rapidly evolving with innovations focused on increasing biological complexity and predictive power. Companies are developing advanced microfluidic devices that precisely control cellular microenvironments, mimicking physiological conditions for various organs including Liver, Heart, and Lung, as well as Other Organ Types. These products offer unique selling propositions such as high throughput screening capabilities, integration with advanced imaging technologies, and the ability to create multi-organ systems. For example, Mimetic BV's Mimetas OrganoPlate® platform allows for the parallel testing of multiple compounds on various organ models, significantly accelerating Drug Discovery and Toxicology Research. Valo Health's acquisition of TARA Biosystems underscores the trend of integrating sophisticated 3D heart tissue models into comprehensive drug development solutions. These advancements are crucial for generating more translatable data compared to traditional methods.

Key Drivers, Barriers & Challenges in Organs-on-Chips Industry

Key Drivers:

- Enhanced Predictive Power: OoC models offer superior human relevance for predicting drug efficacy and toxicity compared to animal models and 2D cell cultures.

- Reduced R&D Costs & Timelines: By de-risking drug development earlier in the pipeline, OoC can significantly lower overall costs and accelerate time-to-market.

- Ethical Considerations & Reduced Animal Testing: Growing societal and regulatory pressure to reduce, refine, and replace animal testing is a major impetus for OoC adoption.

- Technological Advancements: Continuous innovation in microfluidics, 3D bioprinting, and cell culture techniques are expanding the capabilities and applications of OoC.

- Increasing Demand for Personalized Medicine: OoC can be used to develop patient-specific models for tailored drug development.

Barriers & Challenges:

- Standardization and Validation: A lack of universally accepted standardization and regulatory validation pathways can hinder widespread adoption.

- Complexity and Cost of Implementation: Developing and operating complex OoC systems can be expensive and require specialized expertise.

- Scalability for High-Throughput Screening: While improving, scaling OoC for large-scale, high-throughput screening remains a challenge for some applications.

- Integration with Existing Workflows: Integrating OoC technology seamlessly into established R&D workflows of pharmaceutical companies can be complex.

- Data Interpretation and Standardization: Standardizing data analysis and interpretation across different OoC platforms is crucial for reliable comparisons.

Emerging Opportunities in Organs-on-Chips Industry

Emerging opportunities in the Organs-on-Chips (OoC) industry lie in the development of more complex, interconnected multi-organ systems to better model systemic drug effects and disease progression. The expansion into novel therapeutic areas, such as neurodegenerative diseases and rare genetic disorders, presents significant untapped markets. Furthermore, the application of OoC in Toxicology Research for environmental impact assessments and cosmetic ingredient testing is gaining traction. The increasing interest in personalized medicine is driving opportunities for patient-derived OoC models, enabling bespoke drug efficacy and safety testing. The integration of AI and machine learning with OoC data is also a burgeoning area, promising to unlock deeper insights and predictive capabilities.

Growth Accelerators in the Organs-on-Chips Industry Industry

Long-term growth in the Organs-on-Chips (OoC) industry will be propelled by a combination of technological breakthroughs, strategic partnerships, and market expansion strategies. Continued advancements in engineering complex vascular networks and immune cell interactions within OoC will significantly enhance their physiological relevance. Strategic partnerships between OoC developers and major pharmaceutical companies, as seen with the acquisition of TARA Biosystems by Valo Health, will accelerate the integration of OoC into mainstream drug discovery pipelines. Market expansion into emerging economies with growing biopharmaceutical sectors will also contribute significantly to overall growth. The development of user-friendly, automated OoC platforms will further broaden their accessibility to a wider range of researchers.

Key Players Shaping the Organs-on-Chips Industry Market

- Elveflow

- Emulate Inc

- Bi/ond

- AxoSim

- Hesperos

- MIMETAS BV

- Altis Biosystems

- BiomimX SRL

- Valo Health (Tara Biosystems Inc)

- Netri

- Nortis Inc

- TissUse GmbH

- Allevi Inc

- InSphero

Notable Milestones in Organs-on-Chips Industry Sector

- May 2022: Emulate upgraded its intestinal organ-on-a-chip for researchers studying inflammatory bowel disease.

- April 2022: Valo Health acquired TARA Biosystems, makers of a 3D heart tissue modeling platform. Valo planned to incorporate TARA's heart tissue chips into an end-to-end drug development offering aimed at cardiovascular disease, driven by its Opal data platform.

In-Depth Organs-on-Chips Industry Market Outlook

The future outlook for the Organs-on-Chips (OoC) industry is exceptionally promising, with continued expansion driven by unmet needs in preclinical research and development. Growth accelerators include the ongoing refinement of multi-organ chip technology, enabling the study of complex systemic interactions and disease pathologies with unprecedented accuracy. Strategic collaborations and acquisitions, such as Valo Health's integration of TARA Biosystems, are consolidating the market and accelerating the translation of OoC capabilities into commercial drug development pipelines. The increasing adoption of OoC for personalized medicine, allowing for patient-specific drug testing, represents a significant untapped opportunity. As regulatory bodies increasingly recognize and accept OoC data, the market is poised for sustained high growth, revolutionizing how new therapies are discovered, developed, and brought to patients globally.

Organs-on-Chips Industry Segmentation

-

1. Organ Type

- 1.1. Liver

- 1.2. Heart

- 1.3. Lung

- 1.4. Other Organ Types

-

2. Application

- 2.1. Drug Discovery

- 2.2. Toxicology Research

- 2.3. Other Applications

-

3. End User

- 3.1. Pharmaceutical and Biotechnology Companies

- 3.2. Academic and Research Institutes

- 3.3. Other End Users

Organs-on-Chips Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

- 4. Rest of the World

Organs-on-Chips Industry Regional Market Share

Geographic Coverage of Organs-on-Chips Industry

Organs-on-Chips Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 30.94% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Organ Type

- 5.1.1. Liver

- 5.1.2. Heart

- 5.1.3. Lung

- 5.1.4. Other Organ Types

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Drug Discovery

- 5.2.2. Toxicology Research

- 5.2.3. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Pharmaceutical and Biotechnology Companies

- 5.3.2. Academic and Research Institutes

- 5.3.3. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Organ Type

- 6. Global Organs-on-Chips Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Organ Type

- 6.1.1. Liver

- 6.1.2. Heart

- 6.1.3. Lung

- 6.1.4. Other Organ Types

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Drug Discovery

- 6.2.2. Toxicology Research

- 6.2.3. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Pharmaceutical and Biotechnology Companies

- 6.3.2. Academic and Research Institutes

- 6.3.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Organ Type

- 7. North America Organs-on-Chips Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Organ Type

- 7.1.1. Liver

- 7.1.2. Heart

- 7.1.3. Lung

- 7.1.4. Other Organ Types

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Drug Discovery

- 7.2.2. Toxicology Research

- 7.2.3. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Pharmaceutical and Biotechnology Companies

- 7.3.2. Academic and Research Institutes

- 7.3.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Organ Type

- 8. Europe Organs-on-Chips Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Organ Type

- 8.1.1. Liver

- 8.1.2. Heart

- 8.1.3. Lung

- 8.1.4. Other Organ Types

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Drug Discovery

- 8.2.2. Toxicology Research

- 8.2.3. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Pharmaceutical and Biotechnology Companies

- 8.3.2. Academic and Research Institutes

- 8.3.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Organ Type

- 9. Asia Pacific Organs-on-Chips Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Organ Type

- 9.1.1. Liver

- 9.1.2. Heart

- 9.1.3. Lung

- 9.1.4. Other Organ Types

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Drug Discovery

- 9.2.2. Toxicology Research

- 9.2.3. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Pharmaceutical and Biotechnology Companies

- 9.3.2. Academic and Research Institutes

- 9.3.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Organ Type

- 10. Rest of the World Organs-on-Chips Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Organ Type

- 10.1.1. Liver

- 10.1.2. Heart

- 10.1.3. Lung

- 10.1.4. Other Organ Types

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Drug Discovery

- 10.2.2. Toxicology Research

- 10.2.3. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Pharmaceutical and Biotechnology Companies

- 10.3.2. Academic and Research Institutes

- 10.3.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Organ Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Elveflow

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Emulate Inc

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Bi/ond

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 AxoSim

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Hesperos

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 MIMETAS BV

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Altis Biosystems

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 BiomimX SRL

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Valo Health (Tara Biosystems Inc )

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Netri

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Nortis Inc

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 TissUse GmbH

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Allevi Inc

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 InSphero

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.1 Elveflow

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Organs-on-Chips Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Organs-on-Chips Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Organs-on-Chips Industry Revenue (Million), by Organ Type 2025 & 2033

- Figure 4: North America Organs-on-Chips Industry Volume (K Unit), by Organ Type 2025 & 2033

- Figure 5: North America Organs-on-Chips Industry Revenue Share (%), by Organ Type 2025 & 2033

- Figure 6: North America Organs-on-Chips Industry Volume Share (%), by Organ Type 2025 & 2033

- Figure 7: North America Organs-on-Chips Industry Revenue (Million), by Application 2025 & 2033

- Figure 8: North America Organs-on-Chips Industry Volume (K Unit), by Application 2025 & 2033

- Figure 9: North America Organs-on-Chips Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Organs-on-Chips Industry Volume Share (%), by Application 2025 & 2033

- Figure 11: North America Organs-on-Chips Industry Revenue (Million), by End User 2025 & 2033

- Figure 12: North America Organs-on-Chips Industry Volume (K Unit), by End User 2025 & 2033

- Figure 13: North America Organs-on-Chips Industry Revenue Share (%), by End User 2025 & 2033

- Figure 14: North America Organs-on-Chips Industry Volume Share (%), by End User 2025 & 2033

- Figure 15: North America Organs-on-Chips Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Organs-on-Chips Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Organs-on-Chips Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Organs-on-Chips Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Organs-on-Chips Industry Revenue (Million), by Organ Type 2025 & 2033

- Figure 20: Europe Organs-on-Chips Industry Volume (K Unit), by Organ Type 2025 & 2033

- Figure 21: Europe Organs-on-Chips Industry Revenue Share (%), by Organ Type 2025 & 2033

- Figure 22: Europe Organs-on-Chips Industry Volume Share (%), by Organ Type 2025 & 2033

- Figure 23: Europe Organs-on-Chips Industry Revenue (Million), by Application 2025 & 2033

- Figure 24: Europe Organs-on-Chips Industry Volume (K Unit), by Application 2025 & 2033

- Figure 25: Europe Organs-on-Chips Industry Revenue Share (%), by Application 2025 & 2033

- Figure 26: Europe Organs-on-Chips Industry Volume Share (%), by Application 2025 & 2033

- Figure 27: Europe Organs-on-Chips Industry Revenue (Million), by End User 2025 & 2033

- Figure 28: Europe Organs-on-Chips Industry Volume (K Unit), by End User 2025 & 2033

- Figure 29: Europe Organs-on-Chips Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Europe Organs-on-Chips Industry Volume Share (%), by End User 2025 & 2033

- Figure 31: Europe Organs-on-Chips Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Organs-on-Chips Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Organs-on-Chips Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Organs-on-Chips Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Organs-on-Chips Industry Revenue (Million), by Organ Type 2025 & 2033

- Figure 36: Asia Pacific Organs-on-Chips Industry Volume (K Unit), by Organ Type 2025 & 2033

- Figure 37: Asia Pacific Organs-on-Chips Industry Revenue Share (%), by Organ Type 2025 & 2033

- Figure 38: Asia Pacific Organs-on-Chips Industry Volume Share (%), by Organ Type 2025 & 2033

- Figure 39: Asia Pacific Organs-on-Chips Industry Revenue (Million), by Application 2025 & 2033

- Figure 40: Asia Pacific Organs-on-Chips Industry Volume (K Unit), by Application 2025 & 2033

- Figure 41: Asia Pacific Organs-on-Chips Industry Revenue Share (%), by Application 2025 & 2033

- Figure 42: Asia Pacific Organs-on-Chips Industry Volume Share (%), by Application 2025 & 2033

- Figure 43: Asia Pacific Organs-on-Chips Industry Revenue (Million), by End User 2025 & 2033

- Figure 44: Asia Pacific Organs-on-Chips Industry Volume (K Unit), by End User 2025 & 2033

- Figure 45: Asia Pacific Organs-on-Chips Industry Revenue Share (%), by End User 2025 & 2033

- Figure 46: Asia Pacific Organs-on-Chips Industry Volume Share (%), by End User 2025 & 2033

- Figure 47: Asia Pacific Organs-on-Chips Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Organs-on-Chips Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Organs-on-Chips Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Organs-on-Chips Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Rest of the World Organs-on-Chips Industry Revenue (Million), by Organ Type 2025 & 2033

- Figure 52: Rest of the World Organs-on-Chips Industry Volume (K Unit), by Organ Type 2025 & 2033

- Figure 53: Rest of the World Organs-on-Chips Industry Revenue Share (%), by Organ Type 2025 & 2033

- Figure 54: Rest of the World Organs-on-Chips Industry Volume Share (%), by Organ Type 2025 & 2033

- Figure 55: Rest of the World Organs-on-Chips Industry Revenue (Million), by Application 2025 & 2033

- Figure 56: Rest of the World Organs-on-Chips Industry Volume (K Unit), by Application 2025 & 2033

- Figure 57: Rest of the World Organs-on-Chips Industry Revenue Share (%), by Application 2025 & 2033

- Figure 58: Rest of the World Organs-on-Chips Industry Volume Share (%), by Application 2025 & 2033

- Figure 59: Rest of the World Organs-on-Chips Industry Revenue (Million), by End User 2025 & 2033

- Figure 60: Rest of the World Organs-on-Chips Industry Volume (K Unit), by End User 2025 & 2033

- Figure 61: Rest of the World Organs-on-Chips Industry Revenue Share (%), by End User 2025 & 2033

- Figure 62: Rest of the World Organs-on-Chips Industry Volume Share (%), by End User 2025 & 2033

- Figure 63: Rest of the World Organs-on-Chips Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: Rest of the World Organs-on-Chips Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Rest of the World Organs-on-Chips Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Rest of the World Organs-on-Chips Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Organs-on-Chips Industry Revenue Million Forecast, by Organ Type 2020 & 2033

- Table 2: Global Organs-on-Chips Industry Volume K Unit Forecast, by Organ Type 2020 & 2033

- Table 3: Global Organs-on-Chips Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Organs-on-Chips Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Global Organs-on-Chips Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Global Organs-on-Chips Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 7: Global Organs-on-Chips Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Organs-on-Chips Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Organs-on-Chips Industry Revenue Million Forecast, by Organ Type 2020 & 2033

- Table 10: Global Organs-on-Chips Industry Volume K Unit Forecast, by Organ Type 2020 & 2033

- Table 11: Global Organs-on-Chips Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Global Organs-on-Chips Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 13: Global Organs-on-Chips Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 14: Global Organs-on-Chips Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 15: Global Organs-on-Chips Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Organs-on-Chips Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Organs-on-Chips Industry Revenue Million Forecast, by Organ Type 2020 & 2033

- Table 24: Global Organs-on-Chips Industry Volume K Unit Forecast, by Organ Type 2020 & 2033

- Table 25: Global Organs-on-Chips Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 26: Global Organs-on-Chips Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 27: Global Organs-on-Chips Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 28: Global Organs-on-Chips Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 29: Global Organs-on-Chips Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Organs-on-Chips Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Germany Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: France Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Italy Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Spain Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Organs-on-Chips Industry Revenue Million Forecast, by Organ Type 2020 & 2033

- Table 44: Global Organs-on-Chips Industry Volume K Unit Forecast, by Organ Type 2020 & 2033

- Table 45: Global Organs-on-Chips Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 46: Global Organs-on-Chips Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 47: Global Organs-on-Chips Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 48: Global Organs-on-Chips Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 49: Global Organs-on-Chips Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Organs-on-Chips Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: China Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Japan Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: India Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Australia Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: South Korea Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Organs-on-Chips Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Organs-on-Chips Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Organs-on-Chips Industry Revenue Million Forecast, by Organ Type 2020 & 2033

- Table 64: Global Organs-on-Chips Industry Volume K Unit Forecast, by Organ Type 2020 & 2033

- Table 65: Global Organs-on-Chips Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 66: Global Organs-on-Chips Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 67: Global Organs-on-Chips Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 68: Global Organs-on-Chips Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 69: Global Organs-on-Chips Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Organs-on-Chips Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Organs-on-Chips Industry?

The projected CAGR is approximately 30.94%.

2. Which companies are prominent players in the Organs-on-Chips Industry?

Key companies in the market include Elveflow, Emulate Inc, Bi/ond, AxoSim, Hesperos, MIMETAS BV, Altis Biosystems, BiomimX SRL, Valo Health (Tara Biosystems Inc ), Netri, Nortis Inc, TissUse GmbH, Allevi Inc, InSphero.

3. What are the main segments of the Organs-on-Chips Industry?

The market segments include Organ Type, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.3 Million as of 2022.

5. What are some drivers contributing to market growth?

Requirement of Alternative for Animal Testing; Need for Early Detection of Drug Toxicity and New Products Launches.

6. What are the notable trends driving market growth?

Lung-related Application is Expected to Exhibit a Significant Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Complexity of Organ-on-chip Models.

8. Can you provide examples of recent developments in the market?

May 2022 : Emulate upgraded its intestinal organ-on-a-chip for researchers studying inflammatory bowel disease.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Organs-on-Chips Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Organs-on-Chips Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Organs-on-Chips Industry?

To stay informed about further developments, trends, and reports in the Organs-on-Chips Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence