Key Insights

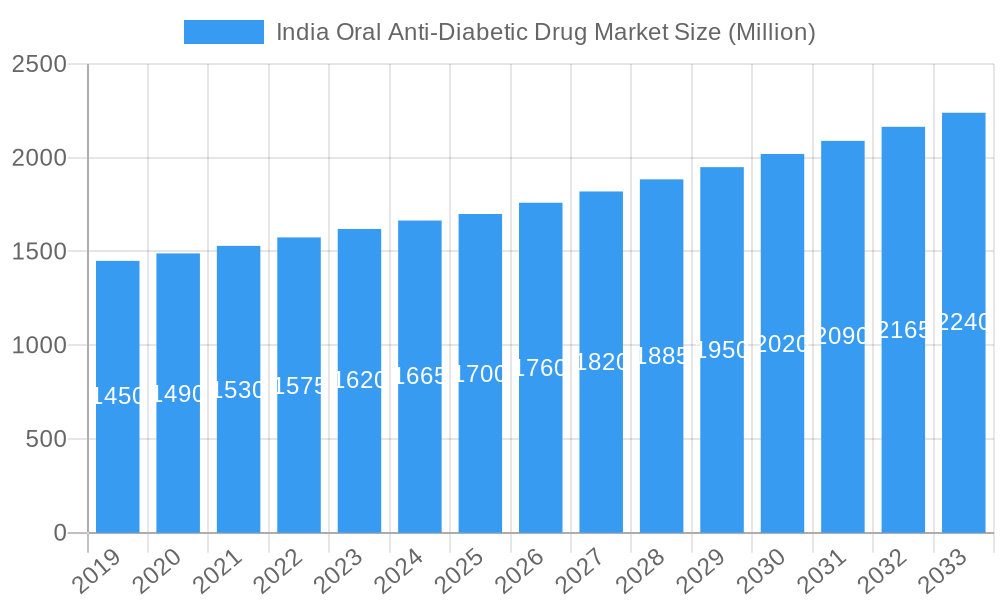

The Indian oral anti-diabetic drug market is poised for robust growth, projected to reach approximately USD 1.7 billion in the base year of 2025, with a compound annual growth rate (CAGR) of 3.50% anticipated through 2033. This expansion is primarily fueled by the escalating prevalence of diabetes in India, driven by evolving lifestyles, sedentary habits, and an increasing aging population susceptible to Type 2 diabetes. The rising awareness among both patients and healthcare providers regarding effective diabetes management through oral medications also acts as a significant growth catalyst. Furthermore, the introduction of novel drug formulations and the growing accessibility of these treatments across urban and semi-urban areas are contributing to market penetration. The market is segmented into various drug classes, including Biguanides (Metformin), DPP-4 inhibitors, Sulfonylureas, and SGLT-2 inhibitors, catering to a broad spectrum of patient needs. While Metformin remains a cornerstone therapy due to its efficacy and affordability, newer classes are gaining traction owing to their improved safety profiles and targeted mechanisms of action.

India Oral Anti-Diabetic Drug Market Market Size (In Billion)

Key trends shaping the Indian oral anti-diabetic drug market include a notable shift towards combination therapies, offering enhanced glycemic control and reduced pill burden for patients. The increasing demand for personalized medicine approaches, where treatment regimens are tailored based on individual patient characteristics, is also gaining momentum. Furthermore, the growing focus on patient adherence and education programs, often supported by pharmaceutical companies, is crucial for long-term disease management. However, certain restraints exist, such as the high cost associated with newer drug classes, potential side effects, and challenges in drug accessibility in remote rural areas. Despite these challenges, the consistent efforts by leading pharmaceutical players like Merck & Co., Pfizer, Takeda, Eli Lilly, and Novo Nordisk to invest in research and development, expand manufacturing capabilities, and strengthen their distribution networks are expected to propel the market forward, ensuring better diabetes management solutions for the Indian population.

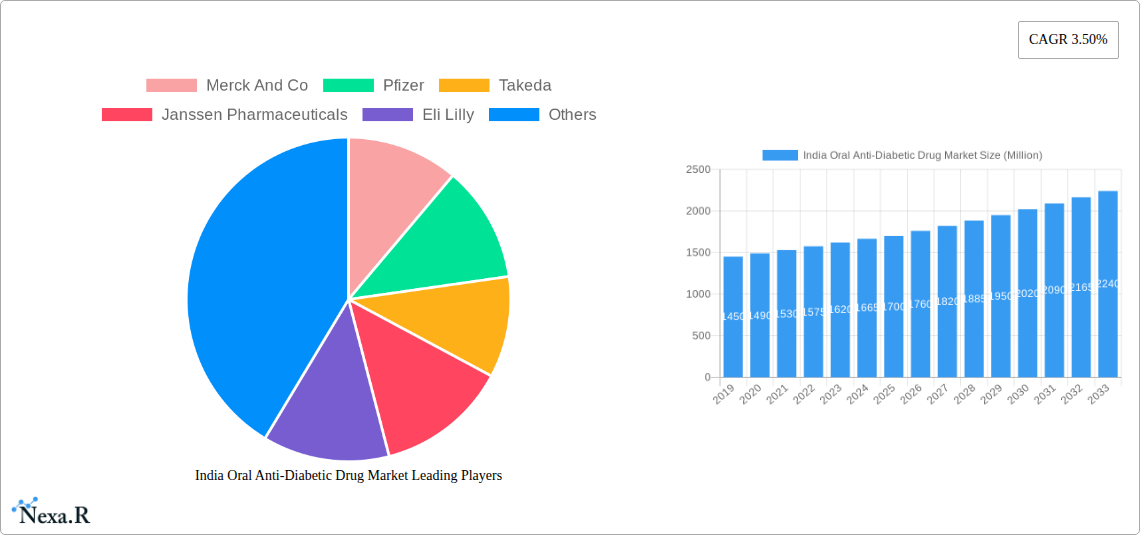

India Oral Anti-Diabetic Drug Market Company Market Share

India Oral Anti-Diabetic Drug Market: Comprehensive Report 2024-2033

This in-depth report offers a detailed analysis of the India Oral Anti-Diabetic Drug Market, forecasting its trajectory from 2024 to 2033. With a base year of 2025, the study delves into historical trends (2019-2024) and projects future growth (2025-2033) at a significant Compound Annual Growth Rate (CAGR). We meticulously examine the market's structure, key growth drivers, dominant segments, competitive landscape, and emerging opportunities, providing actionable insights for stakeholders aiming to capitalize on this rapidly expanding pharmaceutical sector.

The India Oral Anti-Diabetic Drug Market is poised for substantial expansion, driven by an increasing diabetic population, rising healthcare expenditure, and growing awareness of diabetes management. This report provides a granular view of market dynamics, segmentation, and competitive strategies, essential for informed decision-making.

Study Period: 2019–2033 Base Year: 2025 Estimated Year: 2025 Forecast Period: 2025–2033 Historical Period: 2019–2024

India Oral Anti-Diabetic Drug Market Dynamics & Structure

The India Oral Anti-Diabetic Drug Market exhibits a dynamic and evolving structure, characterized by increasing market concentration among leading global and domestic pharmaceutical players. Technological innovation serves as a primary driver, with ongoing research and development focused on novel drug formulations and combination therapies to enhance efficacy and patient adherence. Regulatory frameworks, guided by bodies like the CDCSCO, play a crucial role in approving new drugs and ensuring market quality and safety. The competitive landscape features a robust presence of established players like Merck And Co, Pfizer, Takeda, Janssen Pharmaceuticals, Eli Lilly, Novartis, Sanofi, AstraZeneca, Bristol Myers Squibb, Novo Nordisk, Boehringer Ingelheim, and Astellas, alongside a growing number of agile domestic manufacturers.

- Market Concentration: Dominated by a mix of multinational corporations and large Indian pharmaceutical firms, with significant market share held by a few key players in specific therapeutic classes.

- Technological Innovation Drivers: Focus on Fixed-Dose Combinations (FDCs), combination therapies, and novel drug delivery systems to improve patient outcomes and compliance. The development of drugs targeting specific metabolic pathways remains a key innovation area.

- Regulatory Frameworks: Stringent approval processes by the Central Drugs Standard Control Organization (CDCSCO) ensure drug safety and efficacy. Evolving guidelines for clinical trials and post-market surveillance influence product launches and market access.

- Competitive Product Substitutes: While oral anti-diabetic drugs remain a cornerstone, advancements in injectable therapies and lifestyle interventions present competitive pressures. However, the convenience and cost-effectiveness of oral medications ensure their continued dominance.

- End-User Demographics: The market caters to a vast and growing patient pool, primarily individuals diagnosed with Type 2 Diabetes, followed by a smaller segment of Type 1 Diabetes patients requiring oral adjunct therapies.

- M&A Trends: Mergers, acquisitions, and strategic partnerships are prevalent as companies seek to expand their portfolios, gain access to new markets, and leverage synergistic technologies. The recent surge in FDC launches indicates a strategic focus on simplifying treatment regimens.

India Oral Anti-Diabetic Drug Market Growth Trends & Insights

The India Oral Anti-Diabetic Drug Market is experiencing robust growth, projected to achieve significant market expansion in terms of both volume and value over the forecast period. This growth is intrinsically linked to the escalating prevalence of diabetes in India, driven by lifestyle changes, an aging population, and genetic predispositions. The market size evolution is marked by a steady increase in the adoption of oral anti-diabetic medications, reflecting their efficacy, affordability, and patient preference. Technological disruptions are continuously reshaping the market, with a notable shift towards newer classes of oral anti-diabetics that offer improved glycemic control and reduced side effects.

The adoption rates for various drug classes are evolving, with SGLT-2 inhibitors and DPP-4 inhibitors gaining traction due to their demonstrated cardiovascular and renal benefits, respectively. Biguanides, particularly Metformin, continue to be the first-line therapy due to their established safety profile and cost-effectiveness, representing a significant portion of the market volume. The development of novel triple-fixed-dose combinations (FDCs) is a key trend, simplifying treatment regimens and enhancing patient adherence, thereby contributing to market penetration. For instance, the introduction of Zita, a triple-FDC by Glenmark Pharmaceuticals, exemplifies this trend.

Consumer behavior shifts are also playing a pivotal role. Patients are becoming more informed about their condition and actively seek treatment options that offer comprehensive management, including benefits beyond glycemic control. This has fueled the demand for drugs with demonstrated cardiovascular and nephroprotective properties. The market penetration of these advanced therapies is expected to rise as healthcare professionals increasingly recommend them based on clinical evidence and guidelines. The CAGR of the India Oral Anti-Diabetic Drug Market is estimated to be substantial, driven by these multifaceted factors.

Specific metrics such as market penetration rates for individual drug classes, patient adherence levels influenced by FDCs, and the impact of newer drug launches on overall market value are key indicators of this growth. The increasing disposable income and expanding health insurance coverage in India further facilitate access to these medications, contributing to higher adoption rates. The trend towards personalized medicine, although nascent in the oral anti-diabetic space, is also expected to influence future market dynamics, with a potential for tailored treatment approaches based on individual patient profiles. The overall market size is predicted to reach significant figures, reflecting the immense unmet need and the proactive healthcare initiatives in the country.

Dominant Regions, Countries, or Segments in India Oral Anti-Diabetic Drug Market

Within the India Oral Anti-Diabetic Drug Market, specific segments and regions are poised to drive significant growth and exhibit dominance. The Type 2 Diabetes segment stands out as the primary growth engine, accounting for the overwhelming majority of the diabetic population in India. This segment's dominance is fueled by increasing lifestyle-related risk factors such as obesity, sedentary lifestyles, and unhealthy dietary habits, which are prevalent across the nation. Consequently, oral anti-diabetic drugs are the cornerstone of managing this widespread chronic condition.

Among the various oral anti-diabetic drug classes, Biguanides (Metformin) continue to hold the largest market share by volume. Metformin's established efficacy, extensive safety record, affordability, and its role as a first-line therapy for Type 2 Diabetes solidify its dominant position. However, newer drug classes are exhibiting higher growth rates and increasing market penetration, particularly in specific patient profiles. DPP-4 inhibitors and SGLT-2 inhibitors are emerging as significant growth drivers. DPP-4 inhibitors offer a favorable safety profile and effective glycemic control, while SGLT-2 inhibitors are gaining prominence due to their proven benefits in reducing cardiovascular events and slowing the progression of chronic kidney disease (CKD), as highlighted by AstraZeneca India's approval for Dapagliflozin for diabetes patients with CKD.

Geographically, major metropolitan areas and Tier 1 cities in India, such as Mumbai, Delhi, Bengaluru, Chennai, and Kolkata, are leading the market. These regions benefit from higher population density, greater awareness of diabetes and its complications, better healthcare infrastructure, and a higher concentration of healthcare professionals and specialized diabetes clinics. Economic policies promoting healthcare access and investment in medical facilities further bolster these regions. The presence of major pharmaceutical manufacturers and distributors in these urban centers also facilitates the availability and accessibility of a wide range of oral anti-diabetic drugs.

- Dominant Segment (End-User): Type 2 Diabetes. The sheer prevalence of this condition in India, exacerbated by lifestyle factors, makes it the largest consumer base for oral anti-diabetic medications.

- Dominant Segment (Type): Biguanides (Metformin). Despite the rise of newer classes, Metformin's status as a first-line therapy, coupled with its affordability, ensures its continued market leadership in terms of volume.

- High-Growth Segments (Type):

- SGLT-2 Inhibitors: Driven by their proven cardiovascular and renal benefits, gaining significant traction.

- DPP-4 Inhibitors: Valued for their efficacy and favorable safety profile, experiencing consistent growth.

- Leading Geographic Areas: Major metropolitan cities (e.g., Mumbai, Delhi, Bengaluru) and Tier 1 cities. These urban hubs benefit from:

- Higher diabetic population density.

- Enhanced healthcare infrastructure and specialized diabetes care centers.

- Greater patient awareness and access to advanced treatments.

- Concentration of pharmaceutical market players and distribution networks.

- Favorable economic conditions and higher disposable incomes.

The growth potential in these dominant segments and regions is substantial, driven by increasing diagnosis rates, greater emphasis on proactive diabetes management, and the continuous introduction of improved therapeutic options. The market share of newer drug classes is expected to grow at the expense of older ones, reflecting the industry's focus on innovation and better patient outcomes.

India Oral Anti-Diabetic Drug Market Product Landscape

The India Oral Anti-Diabetic Drug Market product landscape is characterized by a strong presence of established molecules and a burgeoning innovation pipeline focused on enhanced efficacy and patient convenience. Metformin continues to be the foundational product, available in various formulations. The market also features a diverse array of therapeutic classes including Alpha-Glucosidase Inhibitors, Dopamine D2 receptor agonists (like Bromocriptin), DPP-4 inhibitors, Sulfonylureas, and Meglitinides, catering to different patient needs and treatment regimens.

Recent innovations are prominently seen in the development of combination therapies and fixed-dose combinations (FDCs). These products aim to simplify treatment protocols, improve patient adherence, and offer synergistic therapeutic effects. For instance, Glenmark Pharmaceuticals' Zita, a triple-FDC combining Teneligliptin, Dapagliflozin, and Metformin, represents a significant advancement in offering a comprehensive treatment solution in a single pill. Similarly, the introduction of oral semaglutide by Novo Nordisk marks a significant stride in providing more effective oral options for Type 2 diabetes management. The approval of Dapagliflozin by AstraZeneca India for patients with chronic kidney disease further underscores the evolving applications and benefits of oral anti-diabetic drugs, expanding their utility beyond glycemic control. The product landscape is thus dynamic, with a clear trend towards multi-component therapies and drugs with broader therapeutic benefits.

Key Drivers, Barriers & Challenges in India Oral Anti-Diabetic Drug Market

The India Oral Anti-Diabetic Drug Market is propelled by several key drivers, primarily the escalating prevalence of diabetes and pre-diabetes across the nation. This demographic shift, coupled with increasing healthcare expenditure and greater patient awareness regarding diabetes management, fuels demand for effective oral anti-diabetic medications. Technological advancements in drug discovery and formulation, leading to novel and improved therapies such as Fixed-Dose Combinations (FDCs) and drugs with added cardiovascular and renal benefits, act as significant growth catalysts. Government initiatives aimed at improving healthcare accessibility and affordability also contribute positively.

However, the market faces significant barriers and challenges. The sheer cost of newer generation drugs can be a restraint for a large segment of the population, despite their superior efficacy. Regulatory hurdles and the time-consuming approval processes for new drug entities can delay market entry and innovation. Intense competition among a vast number of domestic and international players can lead to price erosion and pressure on profit margins. Furthermore, the challenge of ensuring patient adherence to complex treatment regimens remains a constant concern, despite the introduction of simpler FDC options. Supply chain complexities, particularly in reaching remote areas, and issues related to the quality control of generic drugs also pose challenges.

Emerging Opportunities in India Oral Anti-Diabetic Drug Market

Emerging opportunities within the India Oral Anti-Diabetic Drug Market lie in leveraging the growing awareness of diabetes as a multifaceted condition. The increasing demand for drugs that offer benefits beyond glycemic control, such as cardiovascular protection and renal benefits, presents a significant avenue for growth. The expansion of healthcare infrastructure into Tier 2 and Tier 3 cities, coupled with government-led initiatives for diabetes screening and management, unlocks untapped market potential. The growing preference for simplified treatment regimens is creating a robust demand for innovative Fixed-Dose Combinations (FDCs) and combination therapies, offering a prime opportunity for product development and market penetration.

Furthermore, the evolving consumer preferences towards personalized medicine and proactive health management are creating a niche for advanced oral anti-diabetic agents. Opportunities also exist in developing cost-effective generic versions of recently approved novel drugs, catering to the price-sensitive Indian market. The potential for digital health integration, including patient monitoring apps and telehealth services, can enhance treatment adherence and outcomes, thereby creating new service-based opportunities around oral anti-diabetic therapies.

Growth Accelerators in the India Oral Anti-Diabetic Drug Market Industry

Several catalysts are accelerating the long-term growth of the India Oral Anti-Diabetic Drug Market. Technological breakthroughs in pharmaceutical research are continuously yielding novel drug molecules and improved formulations, such as SGLT-2 inhibitors and DPP-4 inhibitors, which offer enhanced efficacy and better patient outcomes. The strategic partnerships and collaborations between global pharmaceutical giants and domestic Indian companies are vital for market expansion, technology transfer, and efficient product distribution. Furthermore, market expansion strategies, including the penetration into semi-urban and rural areas through robust distribution networks and targeted marketing campaigns, are crucial growth accelerators. The increasing focus on preventative healthcare and early diagnosis of diabetes, supported by government policies and public health programs, is also a significant factor driving sustained demand for oral anti-diabetic drugs.

Key Players Shaping the India Oral Anti-Diabetic Drug Market Market

- Merck And Co

- Pfizer

- Takeda

- Janssen Pharmaceuticals

- Eli Lilly

- Novartis

- Sanofi

- AstraZeneca

- Bristol Myers Squibb

- Novo Nordisk

- Boehringer Ingelheim

- Astellas

Notable Milestones in India Oral Anti-Diabetic Drug Market Sector

- October 2023: Glenmark Pharmaceuticals announced the release of Zita, a new triple-fixed-dose combination (FDC) medication for diabetes treatment, blending Teneligliptin, Dapagliflozin, and Metformin.

- November 2022: AstraZeneca India received approval from the CDCSCO to market Dapagliflozin, an anti-diabetes drug indicated for patients with chronic kidney disease (CKD).

- January 2022: Novo Nordisk launched oral semaglutide in India for the treatment of Type 2 Diabetes.

In-Depth India Oral Anti-Diabetic Drug Market Market Outlook

The India Oral Anti-Diabetic Drug Market is set for a period of sustained and robust growth, driven by an expanding diabetic population and increasing healthcare investments. The market's outlook is characterized by the continued dominance of Metformin, alongside the rapid ascent of newer drug classes like SGLT-2 inhibitors and DPP-4 inhibitors, propelled by their superior clinical benefits and improved patient outcomes. Strategic partnerships, the introduction of innovative fixed-dose combinations, and an expanding distribution network into underserved regions are key growth accelerators. The increasing focus on holistic diabetes management, encompassing cardiovascular and renal health, presents substantial opportunities for pharmaceutical companies to introduce and market drugs with multifaceted therapeutic advantages. The market's future trajectory is strongly indicative of significant value creation and a positive impact on public health in India.

India Oral Anti-Diabetic Drug Market Segmentation

-

1. Type

- 1.1. Oral Ant: Biguanides(Metformin)

- 1.2. Alpha-Glucosidase Inhibitors

- 1.3. Dopamine D2 receptor agonist(Bromocriptin)

- 1.4. SGLT-2 inhibitors

- 1.5. DPP-4 inhibitors

- 1.6. Sulfonylureas

- 1.7. Meglitinides

-

2. End-User

- 2.1. Type 1 Diabetes

- 2.2. Type 2 Diabetes

India Oral Anti-Diabetic Drug Market Segmentation By Geography

- 1. India

India Oral Anti-Diabetic Drug Market Regional Market Share

Geographic Coverage of India Oral Anti-Diabetic Drug Market

India Oral Anti-Diabetic Drug Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Oral Ant: Biguanides(Metformin)

- 5.1.2. Alpha-Glucosidase Inhibitors

- 5.1.3. Dopamine D2 receptor agonist(Bromocriptin)

- 5.1.4. SGLT-2 inhibitors

- 5.1.5. DPP-4 inhibitors

- 5.1.6. Sulfonylureas

- 5.1.7. Meglitinides

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Type 1 Diabetes

- 5.2.2. Type 2 Diabetes

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. India Oral Anti-Diabetic Drug Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Oral Ant: Biguanides(Metformin)

- 6.1.2. Alpha-Glucosidase Inhibitors

- 6.1.3. Dopamine D2 receptor agonist(Bromocriptin)

- 6.1.4. SGLT-2 inhibitors

- 6.1.5. DPP-4 inhibitors

- 6.1.6. Sulfonylureas

- 6.1.7. Meglitinides

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Type 1 Diabetes

- 6.2.2. Type 2 Diabetes

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Merck And Co

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Pfizer

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Takeda

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Janssen Pharmaceuticals

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Eli Lilly

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Novartis

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Sanofi

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 AstraZeneca

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Bristol Myers Squibb

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Novo Nordisk

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Boehringer Ingelheim

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Astellas

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Merck And Co

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Oral Anti-Diabetic Drug Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India Oral Anti-Diabetic Drug Market Share (%) by Company 2025

List of Tables

- Table 1: India Oral Anti-Diabetic Drug Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: India Oral Anti-Diabetic Drug Market Volume K Unit Forecast, by Type 2020 & 2033

- Table 3: India Oral Anti-Diabetic Drug Market Revenue Million Forecast, by End-User 2020 & 2033

- Table 4: India Oral Anti-Diabetic Drug Market Volume K Unit Forecast, by End-User 2020 & 2033

- Table 5: India Oral Anti-Diabetic Drug Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: India Oral Anti-Diabetic Drug Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: India Oral Anti-Diabetic Drug Market Revenue Million Forecast, by Type 2020 & 2033

- Table 8: India Oral Anti-Diabetic Drug Market Volume K Unit Forecast, by Type 2020 & 2033

- Table 9: India Oral Anti-Diabetic Drug Market Revenue Million Forecast, by End-User 2020 & 2033

- Table 10: India Oral Anti-Diabetic Drug Market Volume K Unit Forecast, by End-User 2020 & 2033

- Table 11: India Oral Anti-Diabetic Drug Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: India Oral Anti-Diabetic Drug Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Oral Anti-Diabetic Drug Market?

The projected CAGR is approximately 3.50%.

2. Which companies are prominent players in the India Oral Anti-Diabetic Drug Market?

Key companies in the market include Merck And Co, Pfizer, Takeda, Janssen Pharmaceuticals, Eli Lilly, Novartis, Sanofi, AstraZeneca, Bristol Myers Squibb, Novo Nordisk, Boehringer Ingelheim, Astellas.

3. What are the main segments of the India Oral Anti-Diabetic Drug Market?

The market segments include Type , End-User .

4. Can you provide details about the market size?

The market size is estimated to be USD 1.7 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Geriatric Population and Changing Dietary Habits; High Prevalence of Irritable bowel syndrome with constipation (IBS-C) and Opioid-induced constipation (OIC) and Chronic Constipation; Development of Latest Drugs and Treatment Procedures.

6. What are the notable trends driving market growth?

Sodium-glucose Cotransport-2 (SGLT-2) inhibitor Segment Occupied the Highest Market Share in India Oral Anti-Diabetic Drugs Market in current year.

7. Are there any restraints impacting market growth?

Increasing Dependence on Majority of Over-the-Counter (OTC) Drugs; Lack of Awareness and Reluctance Among Patients due to Adverse Effects of Opioid-Induced Constipation (OIC) Drugs.

8. Can you provide examples of recent developments in the market?

October 2023: Glenmark Pharmaceuticals has announced the release of a new triple-fixed-dose combination (FDC) medication for diabetes treatment. The company, headquartered in Mumbai, has unveiled the blend of Teneligliptin, Dapagliflozin, and Metformin under the brand name Zita.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Oral Anti-Diabetic Drug Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Oral Anti-Diabetic Drug Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Oral Anti-Diabetic Drug Market?

To stay informed about further developments, trends, and reports in the India Oral Anti-Diabetic Drug Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence