Key Insights

The US veterinary healthcare market is poised for significant expansion, driven by escalating pet ownership, increasing pet humanization, and innovations in veterinary diagnostics and therapeutics. The market, currently valued at $65.45 billion in 2025, is projected to achieve a Compound Annual Growth Rate (CAGR) of 7.8% through 2033. This robust growth is underpinned by several key drivers. Firstly, a growing preference for companion animals, predominantly dogs and cats, combined with rising disposable incomes, fuels increased expenditure on pet healthcare. Secondly, heightened awareness of preventative care and the availability of advanced diagnostic tools, such as sophisticated imaging and genetic testing, are driving demand for specialized veterinary services. This trend is further amplified by the development of novel therapeutics, including targeted treatments for specific animal diseases. The market is segmented by product categories, including therapeutics, diagnostics, and other related products, and by animal types, such as dogs and cats, horses, ruminants, swine, poultry, and other animals. Dogs and cats represent the dominant segment, reflecting their widespread status as companion animals. Geographically, the market exhibits its strongest presence in the densely populated regions of the Northeast and West, with substantial growth opportunities identified across all US regions.

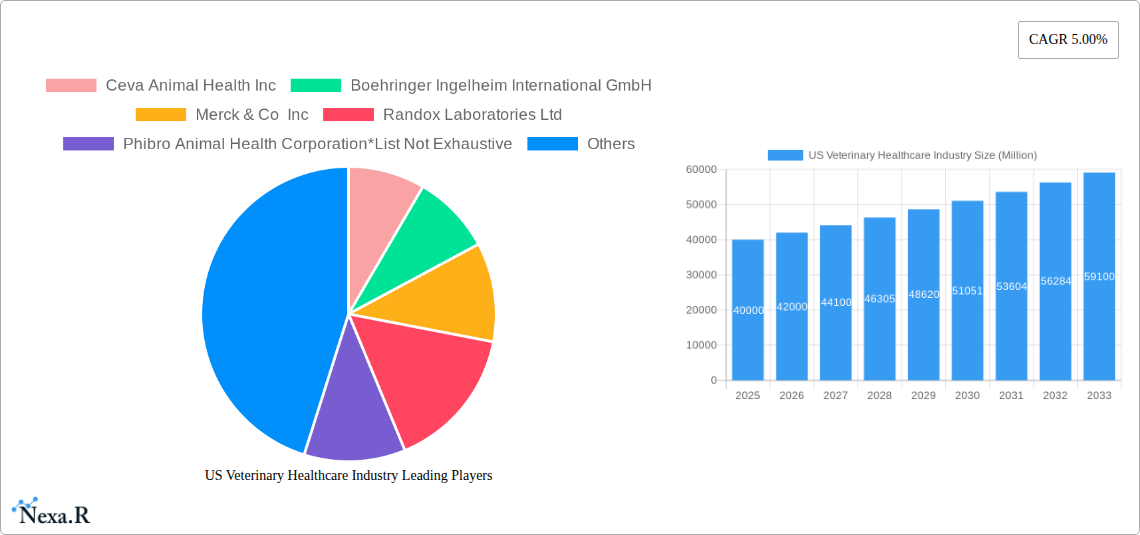

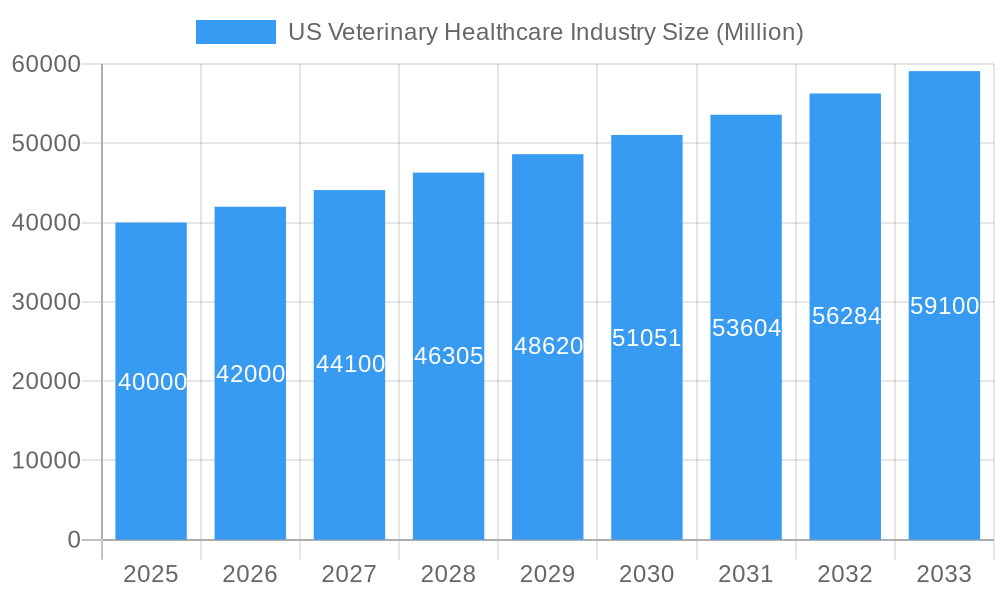

US Veterinary Healthcare Industry Market Size (In Billion)

Despite the positive outlook, the industry encounters challenges, including rising costs for veterinary services and medications, which may impact accessibility to care for certain pet owners. Furthermore, veterinary insurance penetration, while increasing, remains comparatively lower than in human healthcare, presenting a potential barrier for pet owners seeking advanced or extensive treatment options. The competitive landscape among established players, including Zoetis, Merck, and Boehringer Ingelheim, is intense. Consequently, market participants are prioritizing innovation, strategic alliances, and portfolio expansion to strengthen their market positions. Future growth trajectories will be contingent upon sustained consumer demand, technological advancements, and effective management of costs and access to care. A strong emphasis on preventative health strategies and the continued integration of technology within veterinary practices will be vital for enduring industry expansion in the forthcoming years.

US Veterinary Healthcare Industry Company Market Share

This comprehensive market research report offers an in-depth analysis of the US Veterinary Healthcare industry, delivering critical insights for investors, industry professionals, and strategic decision-makers. Through a detailed examination of market dynamics, growth trajectories, and key stakeholders, this report provides a holistic view of this rapidly evolving sector. The analysis covers the period from 2019 to 2033, with 2025 serving as the base year and the forecast period extending from 2025 to 2033. Market valuations are presented in billions of US dollars.

US Veterinary Healthcare Industry Market Dynamics & Structure

The US veterinary healthcare market is a dynamic landscape shaped by several interconnected factors. Market concentration is moderate, with a few large multinational corporations holding significant market share, alongside numerous smaller, specialized players. Technological innovation, particularly in diagnostics and therapeutics, is a key growth driver, constantly pushing the boundaries of animal health management. Stringent regulatory frameworks, overseen by agencies like the FDA, influence product development and market entry. The market also witnesses competitive pressure from the emergence of product substitutes and the increasing availability of generic medications. End-user demographics, characterized by rising pet ownership and an increasing humanization of pets, fuel market expansion. Finally, the industry experiences considerable M&A activity, with larger companies strategically acquiring smaller firms to bolster their portfolios and technological capabilities.

- Market Concentration: Moderate, with top players holding approximately xx% market share in 2024.

- Technological Innovation: Driven by advancements in diagnostics, therapeutics, and data analytics.

- Regulatory Landscape: Stringent regulations by the FDA and other agencies impact product approvals and market entry.

- Competitive Substitutes: Emergence of generic drugs and alternative therapies creates competitive pressure.

- End-User Demographics: Increasing pet ownership and humanization of pets drive market demand.

- M&A Activity: Significant M&A activity observed, with approximately xx deals recorded in the past five years.

US Veterinary Healthcare Industry Growth Trends & Insights

The US veterinary healthcare market experienced robust growth during the historical period (2019-2024), driven by factors such as increased pet ownership, rising pet healthcare expenditure, and advancements in veterinary medicine. The market is expected to continue its expansion throughout the forecast period (2025-2033), albeit at a slightly moderated pace due to economic factors and potential inflationary pressures. The adoption of new technologies, such as telemedicine and advanced diagnostic tools, is accelerating. Consumer behavior shifts towards preventative care and premium pet products contribute to growth. The market size is projected to reach xx Million by 2033, exhibiting a compound annual growth rate (CAGR) of xx% during the forecast period. Market penetration of advanced diagnostics and therapeutics is also expected to increase significantly. This growth is further fueled by the increasing awareness among pet owners about animal health and a willingness to invest in advanced treatments.

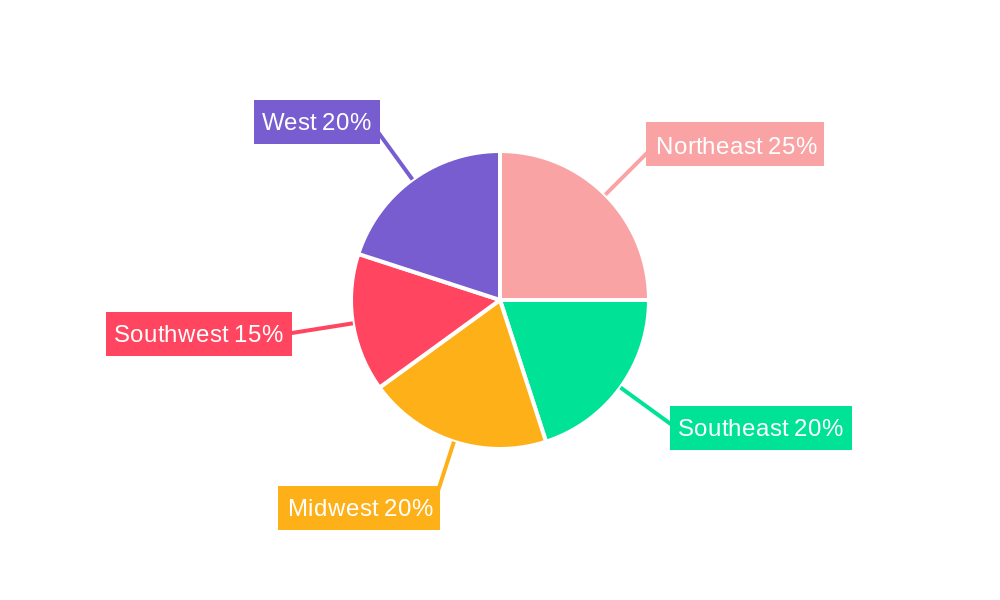

Dominant Regions, Countries, or Segments in US Veterinary Healthcare Industry

The US veterinary healthcare market shows significant regional variations in growth. The highest growth is observed in the companion animal segment (dogs and cats), largely driven by increased pet ownership and the willingness to invest in their health. Within this segment, therapeutic products dominate, with a substantial share in the market. Geographically, states with higher pet ownership density and higher disposable incomes, such as California, Florida, and Texas, show the highest market value and growth.

- Dominant Segment: Companion Animals (Dogs & Cats) – Therapeutic Products.

- Key Growth Drivers: High pet ownership rates, increasing disposable incomes, and humanization of pets.

- Regional Dominance: California, Florida, and Texas contribute significantly to the market size.

- Market Share: Companion animals segment holds approximately xx% of the total market.

- Growth Potential: Continued growth is expected driven by premium pet food and services.

US Veterinary Healthcare Industry Product Landscape

The US veterinary healthcare product landscape is characterized by a wide range of therapeutic drugs, diagnostic tools, and other ancillary products. Innovation focuses on developing more targeted and effective treatments, improved diagnostic accuracy, and user-friendly technologies. Products such as advanced imaging systems, rapid diagnostic tests, and personalized medicine solutions are gaining traction. Unique selling propositions include improved efficacy, reduced side effects, and enhanced convenience.

Key Drivers, Barriers & Challenges in US Veterinary Healthcare Industry

Key Drivers:

- Rising pet ownership and increasing humanization of pets.

- Technological advancements in diagnostics and therapeutics.

- Growing awareness of animal health and preventative care.

- Increased veterinary clinic visits and specialized services.

Challenges & Restraints:

- High cost of veterinary care creating access barriers for some pet owners.

- Supply chain disruptions impacting the availability of certain medications and supplies.

- Stringent regulatory approvals lengthening the time-to-market for new products.

- Competition from both established and emerging companies.

- xx Million annual losses due to supply chain issues.

Emerging Opportunities in US Veterinary Healthcare Industry

- Growing demand for telehealth services and remote animal health monitoring.

- Increasing adoption of personalized medicine approaches.

- Expansion of preventative care services and wellness programs.

- Development of innovative diagnostic tools with improved accuracy and speed.

- Growing interest in alternative and complementary therapies for animals.

Growth Accelerators in the US Veterinary Healthcare Industry

Technological breakthroughs in diagnostics, therapeutics, and data analytics are key growth accelerators. Strategic partnerships between veterinary clinics, pharmaceutical companies, and technology providers enhance service delivery and market access. Expanding into niche markets, such as specialized veterinary care for exotic animals, creates new revenue streams.

Key Players Shaping the US Veterinary Healthcare Industry Market

- Ceva Animal Health Inc

- Boehringer Ingelheim International GmbH

- Merck & Co Inc

- Randox Laboratories Ltd

- Phibro Animal Health Corporation

- Vetoquinol

- Virbac SA

- Elanco Animal Health

- Idexx Laboratories

- Zoetis Inc

Notable Milestones in US Veterinary Healthcare Industry Sector

- March 2022: LexaGene Holdings developed the MiQLab System, a fully automated rapid pathogen testing device.

- January 2022: Covetrus launched Covetrus Pulse, a cloud-based veterinary operating system.

In-Depth US Veterinary Healthcare Industry Market Outlook

The future of the US veterinary healthcare market is bright, driven by sustained growth in pet ownership, technological advancements, and an increasing emphasis on preventative care. Strategic opportunities lie in investing in innovative technologies, expanding service offerings, and establishing strong partnerships. The market is poised for significant expansion, presenting lucrative opportunities for both established and emerging players.

US Veterinary Healthcare Industry Segmentation

-

1. Product

-

1.1. Therapeutics

- 1.1.1. Vaccines

- 1.1.2. Parasiticides

- 1.1.3. Anti-infectives

- 1.1.4. Medical Feed Additives

- 1.1.5. Other Therapeutics

-

1.2. Diagnostics

- 1.2.1. Immunodiagnostic Tests

- 1.2.2. Molecular Diagnostics

- 1.2.3. Diagnostic Imaging

- 1.2.4. Clinical Chemistry

- 1.2.5. Other Diagnostics

-

1.1. Therapeutics

-

2. Animal Type

- 2.1. Dogs and Cats

- 2.2. Horses

- 2.3. Ruminants

- 2.4. Swine

- 2.5. Poultry

- 2.6. Other Animals

US Veterinary Healthcare Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

US Veterinary Healthcare Industry Regional Market Share

Geographic Coverage of US Veterinary Healthcare Industry

US Veterinary Healthcare Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Therapeutics

- 5.1.1.1. Vaccines

- 5.1.1.2. Parasiticides

- 5.1.1.3. Anti-infectives

- 5.1.1.4. Medical Feed Additives

- 5.1.1.5. Other Therapeutics

- 5.1.2. Diagnostics

- 5.1.2.1. Immunodiagnostic Tests

- 5.1.2.2. Molecular Diagnostics

- 5.1.2.3. Diagnostic Imaging

- 5.1.2.4. Clinical Chemistry

- 5.1.2.5. Other Diagnostics

- 5.1.1. Therapeutics

- 5.2. Market Analysis, Insights and Forecast - by Animal Type

- 5.2.1. Dogs and Cats

- 5.2.2. Horses

- 5.2.3. Ruminants

- 5.2.4. Swine

- 5.2.5. Poultry

- 5.2.6. Other Animals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global US Veterinary Healthcare Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Therapeutics

- 6.1.1.1. Vaccines

- 6.1.1.2. Parasiticides

- 6.1.1.3. Anti-infectives

- 6.1.1.4. Medical Feed Additives

- 6.1.1.5. Other Therapeutics

- 6.1.2. Diagnostics

- 6.1.2.1. Immunodiagnostic Tests

- 6.1.2.2. Molecular Diagnostics

- 6.1.2.3. Diagnostic Imaging

- 6.1.2.4. Clinical Chemistry

- 6.1.2.5. Other Diagnostics

- 6.1.1. Therapeutics

- 6.2. Market Analysis, Insights and Forecast - by Animal Type

- 6.2.1. Dogs and Cats

- 6.2.2. Horses

- 6.2.3. Ruminants

- 6.2.4. Swine

- 6.2.5. Poultry

- 6.2.6. Other Animals

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America US Veterinary Healthcare Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Therapeutics

- 7.1.1.1. Vaccines

- 7.1.1.2. Parasiticides

- 7.1.1.3. Anti-infectives

- 7.1.1.4. Medical Feed Additives

- 7.1.1.5. Other Therapeutics

- 7.1.2. Diagnostics

- 7.1.2.1. Immunodiagnostic Tests

- 7.1.2.2. Molecular Diagnostics

- 7.1.2.3. Diagnostic Imaging

- 7.1.2.4. Clinical Chemistry

- 7.1.2.5. Other Diagnostics

- 7.1.1. Therapeutics

- 7.2. Market Analysis, Insights and Forecast - by Animal Type

- 7.2.1. Dogs and Cats

- 7.2.2. Horses

- 7.2.3. Ruminants

- 7.2.4. Swine

- 7.2.5. Poultry

- 7.2.6. Other Animals

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. South America US Veterinary Healthcare Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Therapeutics

- 8.1.1.1. Vaccines

- 8.1.1.2. Parasiticides

- 8.1.1.3. Anti-infectives

- 8.1.1.4. Medical Feed Additives

- 8.1.1.5. Other Therapeutics

- 8.1.2. Diagnostics

- 8.1.2.1. Immunodiagnostic Tests

- 8.1.2.2. Molecular Diagnostics

- 8.1.2.3. Diagnostic Imaging

- 8.1.2.4. Clinical Chemistry

- 8.1.2.5. Other Diagnostics

- 8.1.1. Therapeutics

- 8.2. Market Analysis, Insights and Forecast - by Animal Type

- 8.2.1. Dogs and Cats

- 8.2.2. Horses

- 8.2.3. Ruminants

- 8.2.4. Swine

- 8.2.5. Poultry

- 8.2.6. Other Animals

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Europe US Veterinary Healthcare Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Therapeutics

- 9.1.1.1. Vaccines

- 9.1.1.2. Parasiticides

- 9.1.1.3. Anti-infectives

- 9.1.1.4. Medical Feed Additives

- 9.1.1.5. Other Therapeutics

- 9.1.2. Diagnostics

- 9.1.2.1. Immunodiagnostic Tests

- 9.1.2.2. Molecular Diagnostics

- 9.1.2.3. Diagnostic Imaging

- 9.1.2.4. Clinical Chemistry

- 9.1.2.5. Other Diagnostics

- 9.1.1. Therapeutics

- 9.2. Market Analysis, Insights and Forecast - by Animal Type

- 9.2.1. Dogs and Cats

- 9.2.2. Horses

- 9.2.3. Ruminants

- 9.2.4. Swine

- 9.2.5. Poultry

- 9.2.6. Other Animals

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East & Africa US Veterinary Healthcare Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Therapeutics

- 10.1.1.1. Vaccines

- 10.1.1.2. Parasiticides

- 10.1.1.3. Anti-infectives

- 10.1.1.4. Medical Feed Additives

- 10.1.1.5. Other Therapeutics

- 10.1.2. Diagnostics

- 10.1.2.1. Immunodiagnostic Tests

- 10.1.2.2. Molecular Diagnostics

- 10.1.2.3. Diagnostic Imaging

- 10.1.2.4. Clinical Chemistry

- 10.1.2.5. Other Diagnostics

- 10.1.1. Therapeutics

- 10.2. Market Analysis, Insights and Forecast - by Animal Type

- 10.2.1. Dogs and Cats

- 10.2.2. Horses

- 10.2.3. Ruminants

- 10.2.4. Swine

- 10.2.5. Poultry

- 10.2.6. Other Animals

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Asia Pacific US Veterinary Healthcare Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Therapeutics

- 11.1.1.1. Vaccines

- 11.1.1.2. Parasiticides

- 11.1.1.3. Anti-infectives

- 11.1.1.4. Medical Feed Additives

- 11.1.1.5. Other Therapeutics

- 11.1.2. Diagnostics

- 11.1.2.1. Immunodiagnostic Tests

- 11.1.2.2. Molecular Diagnostics

- 11.1.2.3. Diagnostic Imaging

- 11.1.2.4. Clinical Chemistry

- 11.1.2.5. Other Diagnostics

- 11.1.1. Therapeutics

- 11.2. Market Analysis, Insights and Forecast - by Animal Type

- 11.2.1. Dogs and Cats

- 11.2.2. Horses

- 11.2.3. Ruminants

- 11.2.4. Swine

- 11.2.5. Poultry

- 11.2.6. Other Animals

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ceva Animal Health Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Boehringer Ingelheim International GmbH

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Merck & Co Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Randox Laboratories Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Phibro Animal Health Corporation*List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Vetoquinol

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Virbac SA

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Elanco Animal Health

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Idexx Laboratories

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Zoetis Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Ceva Animal Health Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Veterinary Healthcare Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America US Veterinary Healthcare Industry Revenue (billion), by Product 2025 & 2033

- Figure 3: North America US Veterinary Healthcare Industry Revenue Share (%), by Product 2025 & 2033

- Figure 4: North America US Veterinary Healthcare Industry Revenue (billion), by Animal Type 2025 & 2033

- Figure 5: North America US Veterinary Healthcare Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 6: North America US Veterinary Healthcare Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America US Veterinary Healthcare Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America US Veterinary Healthcare Industry Revenue (billion), by Product 2025 & 2033

- Figure 9: South America US Veterinary Healthcare Industry Revenue Share (%), by Product 2025 & 2033

- Figure 10: South America US Veterinary Healthcare Industry Revenue (billion), by Animal Type 2025 & 2033

- Figure 11: South America US Veterinary Healthcare Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 12: South America US Veterinary Healthcare Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America US Veterinary Healthcare Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe US Veterinary Healthcare Industry Revenue (billion), by Product 2025 & 2033

- Figure 15: Europe US Veterinary Healthcare Industry Revenue Share (%), by Product 2025 & 2033

- Figure 16: Europe US Veterinary Healthcare Industry Revenue (billion), by Animal Type 2025 & 2033

- Figure 17: Europe US Veterinary Healthcare Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 18: Europe US Veterinary Healthcare Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe US Veterinary Healthcare Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa US Veterinary Healthcare Industry Revenue (billion), by Product 2025 & 2033

- Figure 21: Middle East & Africa US Veterinary Healthcare Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Middle East & Africa US Veterinary Healthcare Industry Revenue (billion), by Animal Type 2025 & 2033

- Figure 23: Middle East & Africa US Veterinary Healthcare Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 24: Middle East & Africa US Veterinary Healthcare Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa US Veterinary Healthcare Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific US Veterinary Healthcare Industry Revenue (billion), by Product 2025 & 2033

- Figure 27: Asia Pacific US Veterinary Healthcare Industry Revenue Share (%), by Product 2025 & 2033

- Figure 28: Asia Pacific US Veterinary Healthcare Industry Revenue (billion), by Animal Type 2025 & 2033

- Figure 29: Asia Pacific US Veterinary Healthcare Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 30: Asia Pacific US Veterinary Healthcare Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific US Veterinary Healthcare Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 3: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 5: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 6: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 11: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 12: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 17: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 18: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 29: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 30: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 38: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 39: Global US Veterinary Healthcare Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific US Veterinary Healthcare Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Veterinary Healthcare Industry?

The projected CAGR is approximately 7.8%.

2. Which companies are prominent players in the US Veterinary Healthcare Industry?

Key companies in the market include Ceva Animal Health Inc, Boehringer Ingelheim International GmbH, Merck & Co Inc, Randox Laboratories Ltd, Phibro Animal Health Corporation*List Not Exhaustive, Vetoquinol, Virbac SA, Elanco Animal Health, Idexx Laboratories, Zoetis Inc.

3. What are the main segments of the US Veterinary Healthcare Industry?

The market segments include Product, Animal Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 65.45 billion as of 2022.

5. What are some drivers contributing to market growth?

Advanced Technology Leading to Innovations in Animal Healthcare; Increasing Productivity at the Risk of Emerging Zoonosis; Increasing Initiatives by the Governments and Animal Welfare Associations.

6. What are the notable trends driving market growth?

Medical Feed Additives Segment Expects to Register a High CAGR in the United States Veterinary Healthcare Market Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Costs Related to Animal Testing.

8. Can you provide examples of recent developments in the market?

In March 2022, LexaGeneHoldings developed a fully automated rapid pathogen testing device LexaGenes MiQLab System and announced advancements to its sample preparation cartridge for processing complex samples. This system s designed to process liquid samples from companion animals used in the diagnosis of infections such as urinary tract infections (UTIs) and skin infections.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Veterinary Healthcare Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Veterinary Healthcare Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Veterinary Healthcare Industry?

To stay informed about further developments, trends, and reports in the US Veterinary Healthcare Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence