Key Insights

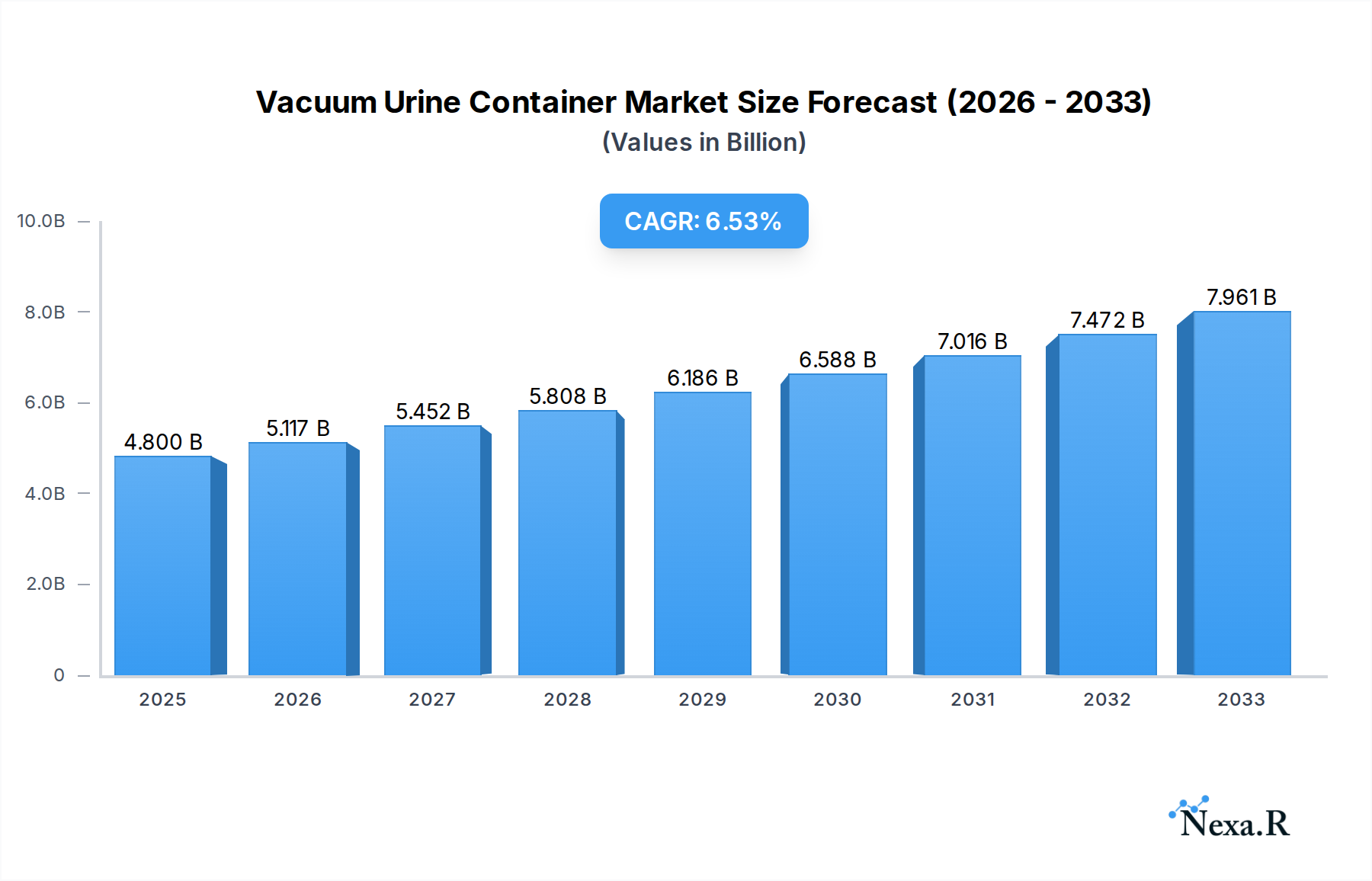

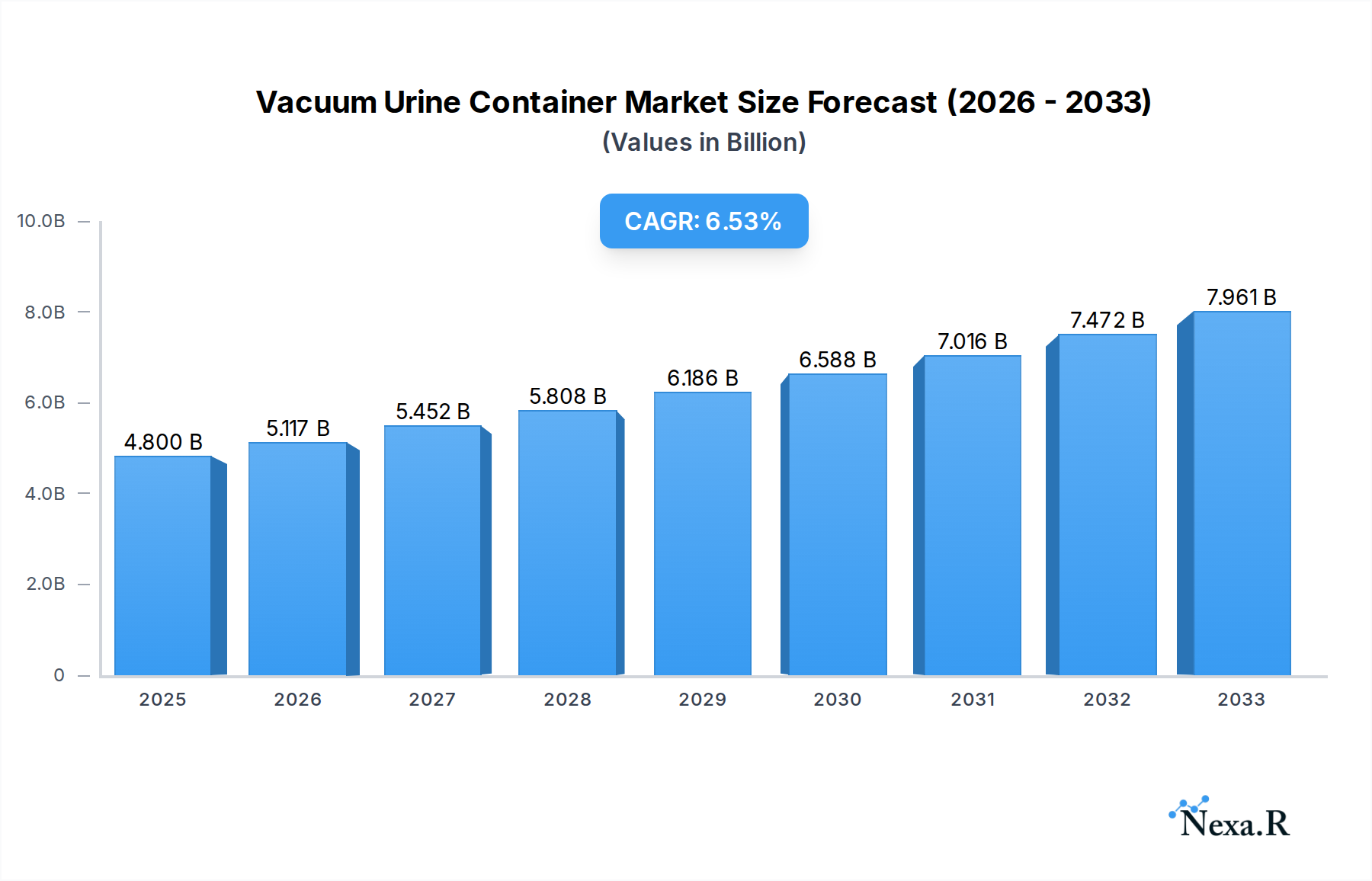

The global Vacuum Urine Container market is projected to reach an estimated $4.8 billion in 2025, experiencing robust growth at a Compound Annual Growth Rate (CAGR) of 6.5% over the forecast period of 2025-2033. This expansion is primarily fueled by several key drivers, including the increasing prevalence of diagnostic testing for various urinary tract infections and chronic diseases, a growing emphasis on patient convenience and sample integrity in healthcare settings, and advancements in material science leading to more reliable and sterile collection devices. The market's trajectory is further bolstered by a rising awareness of public health and the continuous need for accurate laboratory diagnostics. Hospitals and medical examination centers represent the largest application segments, reflecting the high volume of urine sample collections in these facilities for routine check-ups, disease diagnosis, and treatment monitoring.

Vacuum Urine Container Market Size (In Billion)

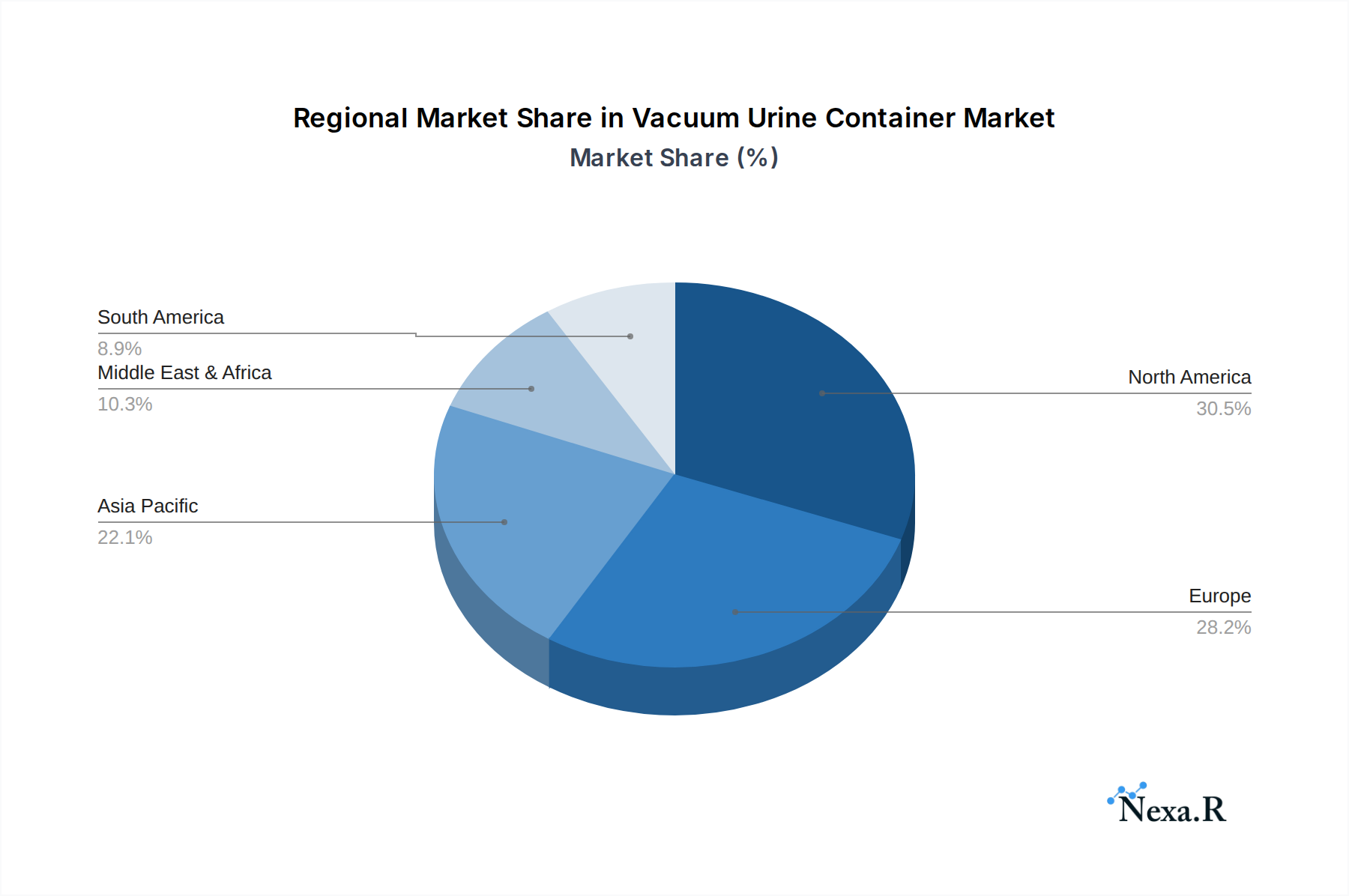

Emerging trends such as the development of specialized vacuum urine containers with integrated features for enhanced safety and ease of use, alongside the increasing adoption of these containers in home-based diagnostic kits, are shaping the market landscape. The growing demand for enhanced patient experience and reduced risk of contamination during sample collection are driving innovation and adoption. Geographically, North America and Europe currently dominate the market due to advanced healthcare infrastructure and high diagnostic test volumes. However, the Asia Pacific region is anticipated to exhibit the fastest growth, driven by an expanding healthcare sector, increasing disposable incomes, and a growing focus on preventive healthcare. While the market demonstrates strong growth potential, restraints such as stringent regulatory approvals for medical devices and the potential for price sensitivity in certain emerging economies could pose challenges. Nevertheless, the overall outlook for the vacuum urine container market remains highly positive, supported by ongoing advancements and increasing healthcare expenditure worldwide.

Vacuum Urine Container Company Market Share

Vacuum Urine Container Market Analysis: 2019-2033

This comprehensive report delves into the global vacuum urine container market, a critical component of modern diagnostics and healthcare. We provide an in-depth analysis of market dynamics, growth trends, regional dominance, product innovations, and key player strategies from 2019 to 2033, with a base year of 2025. This report is tailored for industry professionals, researchers, and investors seeking actionable insights into this rapidly evolving sector.

Vacuum Urine Container Market Dynamics & Structure

The vacuum urine container market exhibits a moderately consolidated structure, characterized by the presence of both established global players and niche manufacturers. Technological innovation remains a primary driver, with advancements focusing on enhanced sterility, user-friendliness, and integrated testing capabilities. Regulatory frameworks, particularly those surrounding medical device safety and hygiene, significantly influence product development and market entry. Competitive product substitutes, while present in the form of traditional urine collection cups, are increasingly being supplanted by vacuum-sealed options due to their superior contamination prevention. End-user demographics span across healthcare professionals in hospitals and diagnostic centers, as well as researchers in academic and pharmaceutical institutions. Mergers and acquisitions (M&A) trends are observed, indicating a strategic push for market expansion and portfolio diversification. For instance, a notable trend involves acquisitions aimed at integrating vacuum urine collection systems with point-of-care diagnostic platforms. The market concentration is estimated to be around 55% held by the top five players. M&A deal volumes are projected to average 3 deals per year during the forecast period, with an average deal value of $XX billion. Barriers to innovation include stringent regulatory approvals and the high cost of research and development for advanced features.

Vacuum Urine Container Growth Trends & Insights

The global vacuum urine container market is poised for robust expansion, driven by a confluence of factors including an increasing global healthcare expenditure, a rising prevalence of chronic diseases requiring regular diagnostic testing, and a growing emphasis on infection control in clinical settings. The adoption rates for vacuum urine containers are steadily increasing across hospitals, medical examination centers, and research institutes, moving away from traditional, less sterile collection methods. Technological disruptions, such as the integration of smart features for sample tracking and automated analysis, are further accelerating market penetration. Consumer behavior shifts are also playing a significant role, with healthcare providers and patients alike prioritizing convenience, safety, and accuracy in diagnostic procedures. The market size for vacuum urine containers is projected to grow from approximately $2.5 billion in 2024 to an estimated $4.1 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period. Market penetration is expected to rise from 60% in 2024 to over 75% by 2033, indicating a substantial shift towards advanced collection systems. The increasing demand for diagnostic tests for conditions like urinary tract infections, kidney diseases, and diabetes, coupled with a growing awareness of the importance of precise sample integrity, will continue to fuel this upward trajectory. Furthermore, the expansion of healthcare infrastructure in emerging economies is opening up new avenues for market growth.

Dominant Regions, Countries, or Segments in Vacuum Urine Container

The North America region currently holds a dominant position in the global vacuum urine container market, driven by a well-established healthcare infrastructure, high healthcare spending, and a proactive approach to adopting advanced medical technologies. The United States, in particular, contributes significantly to this regional dominance due to the high volume of diagnostic tests performed annually and the stringent quality standards mandated for medical devices. Within the application segment, Hospitals are the leading segment, accounting for an estimated 45% of the total market share in 2025. This is attributed to the continuous need for sterile and reliable urine sample collection for patient diagnosis, treatment monitoring, and pre-surgical assessments. The Capacity: 90ml segment is also a major contributor to market growth, offering a versatile capacity suitable for a wide range of routine diagnostic tests.

- Key Drivers in North America:

- Advanced healthcare reimbursement policies supporting diagnostic procedures.

- High concentration of leading pharmaceutical and biotechnology companies driving research and development.

- Robust regulatory framework ensuring product safety and efficacy.

- Significant investment in healthcare infrastructure and technology adoption.

- Dominance Factors for Hospitals:

- High patient throughput and demand for accurate, sterile sample collection.

- Integration of vacuum urine containers into existing laboratory workflows.

- Reduced risk of sample contamination and improved turnaround times.

- Growth Potential for 90ml Capacity:

- Optimal volume for most routine urinalysis, balancing sample adequacy with waste reduction.

- Cost-effectiveness for high-volume diagnostic laboratories.

- Versatility for various types of urine tests, including culture and sensitivity.

The Asia-Pacific region is emerging as a significant growth engine, propelled by increasing healthcare investments, a burgeoning middle class with improved access to healthcare services, and a rising prevalence of lifestyle-related diseases. Within the application segment, Medical Examination Centres are witnessing rapid growth in market share, driven by their increasing role in primary healthcare and preventive diagnostics. Furthermore, the Capacity: 120ml segment is expected to gain traction due to the evolving requirements for specialized urine tests and the growing demand for comprehensive diagnostic panels.

- Key Drivers in Asia-Pacific:

- Government initiatives to expand healthcare access and affordability.

- Growing awareness of preventive healthcare and early disease detection.

- Increasing foreign direct investment in the healthcare sector.

- Rapid urbanization and a growing demand for advanced medical diagnostics.

- Growth Drivers for Medical Examination Centres:

- Focus on routine health check-ups and early detection of diseases.

- Efficient workflow and higher patient turnover necessitate reliable collection tools.

- Increasing outsourcing of diagnostic services by hospitals.

- Potential for 120ml Capacity:

- Suitability for quantitative urine analysis and specialized toxicology testing.

- Demand for larger sample volumes for comprehensive research studies.

- Growing trend of integrated diagnostic panels requiring more sample material.

Vacuum Urine Container Product Landscape

The vacuum urine container market is characterized by continuous product innovation aimed at enhancing user safety, sample integrity, and diagnostic efficiency. Leading manufacturers are focusing on developing containers with advanced features such as integrated needles for direct venipuncture into the container, tamper-evident seals for enhanced security, and material advancements to prevent sample degradation. These innovations ensure superior sterility, minimize the risk of aerosol generation during collection, and provide a reliable medium for various laboratory analyses, including urine culture, toxicology screening, and routine urinalysis. Unique selling propositions include improved ergonomic designs for easier handling and the availability of different anticoagulants or preservatives tailored for specific diagnostic needs. Technological advancements are also leaning towards smart containers with embedded RFID tags for seamless tracking within laboratory information systems.

Key Drivers, Barriers & Challenges in Vacuum Urine Container

Key Drivers:

- Increasing prevalence of infectious diseases and chronic conditions: Driving demand for routine and specialized urine diagnostics.

- Growing emphasis on infection control and patient safety: Favoring sterile, closed-loop collection systems like vacuum urine containers.

- Technological advancements in diagnostic testing: Requiring accurate and contamination-free sample collection.

- Expansion of healthcare infrastructure in emerging economies: Creating new market opportunities.

Barriers & Challenges:

- High manufacturing costs and price sensitivity: Particularly in price-sensitive markets.

- Stringent regulatory compliance: Requiring significant investment and time for product approvals.

- Availability of cheaper, traditional urine collection cups: Posing a competitive threat in some segments.

- Supply chain disruptions and raw material price volatility: Affecting production costs and availability. For instance, a 10% increase in plastic resin prices can impact manufacturing costs by 3-5%.

- Disposal of biohazardous waste: Requiring specialized handling protocols and infrastructure.

Emerging Opportunities in Vacuum Urine Container

Emerging opportunities in the vacuum urine container market lie in the development of specialized containers for point-of-care testing (POCT) devices, enabling rapid diagnostics at the patient's bedside or in remote locations. The growing trend of personalized medicine also presents an opportunity for containers with integrated molecular diagnostic capabilities for DNA or RNA analysis from urine samples. Furthermore, untapped markets in developing nations with rapidly expanding healthcare sectors offer significant growth potential, requiring cost-effective yet reliable vacuum urine collection solutions. The increasing use of telemedicine and remote patient monitoring also drives the need for secure and well-preserved urine samples for at-home collection and subsequent laboratory analysis.

Growth Accelerators in the Vacuum Urine Container Industry

Growth in the vacuum urine container industry is being significantly accelerated by strategic partnerships between container manufacturers and diagnostic equipment providers. These collaborations aim to create integrated solutions, streamlining the entire diagnostic workflow from sample collection to analysis. Technological breakthroughs in material science, leading to lighter, more durable, and environmentally friendly containers, are also acting as growth catalysts. Moreover, the increasing adoption of automated laboratory systems necessitates the use of standardized and reliable collection devices, further propelling the demand for vacuum urine containers. Market expansion strategies, including targeted marketing campaigns and distribution network development in emerging economies, are also crucial growth accelerators.

Key Players Shaping the Vacuum Urine Container Market

- Deltalab

- NOKE LAB

- BD

- VWR

- BIOSIGMA

- Sarstedt

- Greiner Bio-One

- Thermo Fisher Scientific

- Cardinal Health

- Medline Industries

- FL Medical

- Pioneer Impex

Notable Milestones in Vacuum Urine Container Sector

- 2019: Launch of advanced vacuum urine containers with enhanced tamper-evident seals, improving sample security.

- 2020: Introduction of biohazard-resistant materials in vacuum urine containers, enhancing safety for healthcare workers.

- 2021: Development of vacuum urine containers with integrated preservatives for extended sample stability.

- 2022: Increased regulatory focus on closed-system urine collection devices, boosting market adoption.

- 2023: Key player acquisition focusing on expanding product portfolios for integrated diagnostic solutions.

- 2024: Growing adoption of vacuum urine containers in point-of-care testing settings.

In-Depth Vacuum Urine Container Market Outlook

The future outlook for the vacuum urine container market is exceptionally positive, driven by sustained demand for accurate and sterile diagnostic samples across diverse healthcare settings. The convergence of technological advancements, such as the integration of smart features and novel materials, with the expanding global healthcare infrastructure will continue to fuel market growth. Strategic collaborations and a focus on emerging markets will be critical for unlocking the full potential of this sector. The market is expected to witness a CAGR of 5.5% from 2025 to 2033, reaching an estimated $4.1 billion, signifying robust growth opportunities and sustained innovation.

Vacuum Urine Container Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Medical Examination Centre

- 1.3. Research Institutes

- 1.4. Others

-

2. Types

- 2.1. Capacity: 60ml

- 2.2. Capacity: 90ml

- 2.3. Capacity: 120ml

- 2.4. Others

Vacuum Urine Container Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Vacuum Urine Container Regional Market Share

Geographic Coverage of Vacuum Urine Container

Vacuum Urine Container REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Vacuum Urine Container Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Medical Examination Centre

- 5.1.3. Research Institutes

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Capacity: 60ml

- 5.2.2. Capacity: 90ml

- 5.2.3. Capacity: 120ml

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Vacuum Urine Container Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Medical Examination Centre

- 6.1.3. Research Institutes

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Capacity: 60ml

- 6.2.2. Capacity: 90ml

- 6.2.3. Capacity: 120ml

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Vacuum Urine Container Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Medical Examination Centre

- 7.1.3. Research Institutes

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Capacity: 60ml

- 7.2.2. Capacity: 90ml

- 7.2.3. Capacity: 120ml

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Vacuum Urine Container Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Medical Examination Centre

- 8.1.3. Research Institutes

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Capacity: 60ml

- 8.2.2. Capacity: 90ml

- 8.2.3. Capacity: 120ml

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Vacuum Urine Container Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Medical Examination Centre

- 9.1.3. Research Institutes

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Capacity: 60ml

- 9.2.2. Capacity: 90ml

- 9.2.3. Capacity: 120ml

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Vacuum Urine Container Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Medical Examination Centre

- 10.1.3. Research Institutes

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Capacity: 60ml

- 10.2.2. Capacity: 90ml

- 10.2.3. Capacity: 120ml

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Deltalab

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 NOKE LAB

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BD

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 VWR

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 BIOSIGMA

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Sarstedt

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Greiner Bio-One

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Thermo Fisher Scientific

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Cardinal Health

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Medline Industries

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 FL Medical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Pioneer Impex

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Deltalab

List of Figures

- Figure 1: Global Vacuum Urine Container Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Vacuum Urine Container Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Vacuum Urine Container Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Vacuum Urine Container Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Vacuum Urine Container Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Vacuum Urine Container Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Vacuum Urine Container Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Vacuum Urine Container Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Vacuum Urine Container Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Vacuum Urine Container Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Vacuum Urine Container Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Vacuum Urine Container Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Vacuum Urine Container Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Vacuum Urine Container Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Vacuum Urine Container Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Vacuum Urine Container Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Vacuum Urine Container Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Vacuum Urine Container Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Vacuum Urine Container Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Vacuum Urine Container Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Vacuum Urine Container Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Vacuum Urine Container Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Vacuum Urine Container Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Vacuum Urine Container Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Vacuum Urine Container Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Vacuum Urine Container Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Vacuum Urine Container Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Vacuum Urine Container Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Vacuum Urine Container Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Vacuum Urine Container Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Vacuum Urine Container Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Vacuum Urine Container Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Vacuum Urine Container Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Vacuum Urine Container Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Vacuum Urine Container Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Vacuum Urine Container Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Vacuum Urine Container Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Vacuum Urine Container Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Vacuum Urine Container Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Vacuum Urine Container Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Vacuum Urine Container Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Vacuum Urine Container Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Vacuum Urine Container Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Vacuum Urine Container Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Vacuum Urine Container Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Vacuum Urine Container Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Vacuum Urine Container Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Vacuum Urine Container Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Vacuum Urine Container Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Vacuum Urine Container Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vacuum Urine Container?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the Vacuum Urine Container?

Key companies in the market include Deltalab, NOKE LAB, BD, VWR, BIOSIGMA, Sarstedt, Greiner Bio-One, Thermo Fisher Scientific, Cardinal Health, Medline Industries, FL Medical, Pioneer Impex.

3. What are the main segments of the Vacuum Urine Container?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vacuum Urine Container," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vacuum Urine Container report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vacuum Urine Container?

To stay informed about further developments, trends, and reports in the Vacuum Urine Container, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence