Key Insights

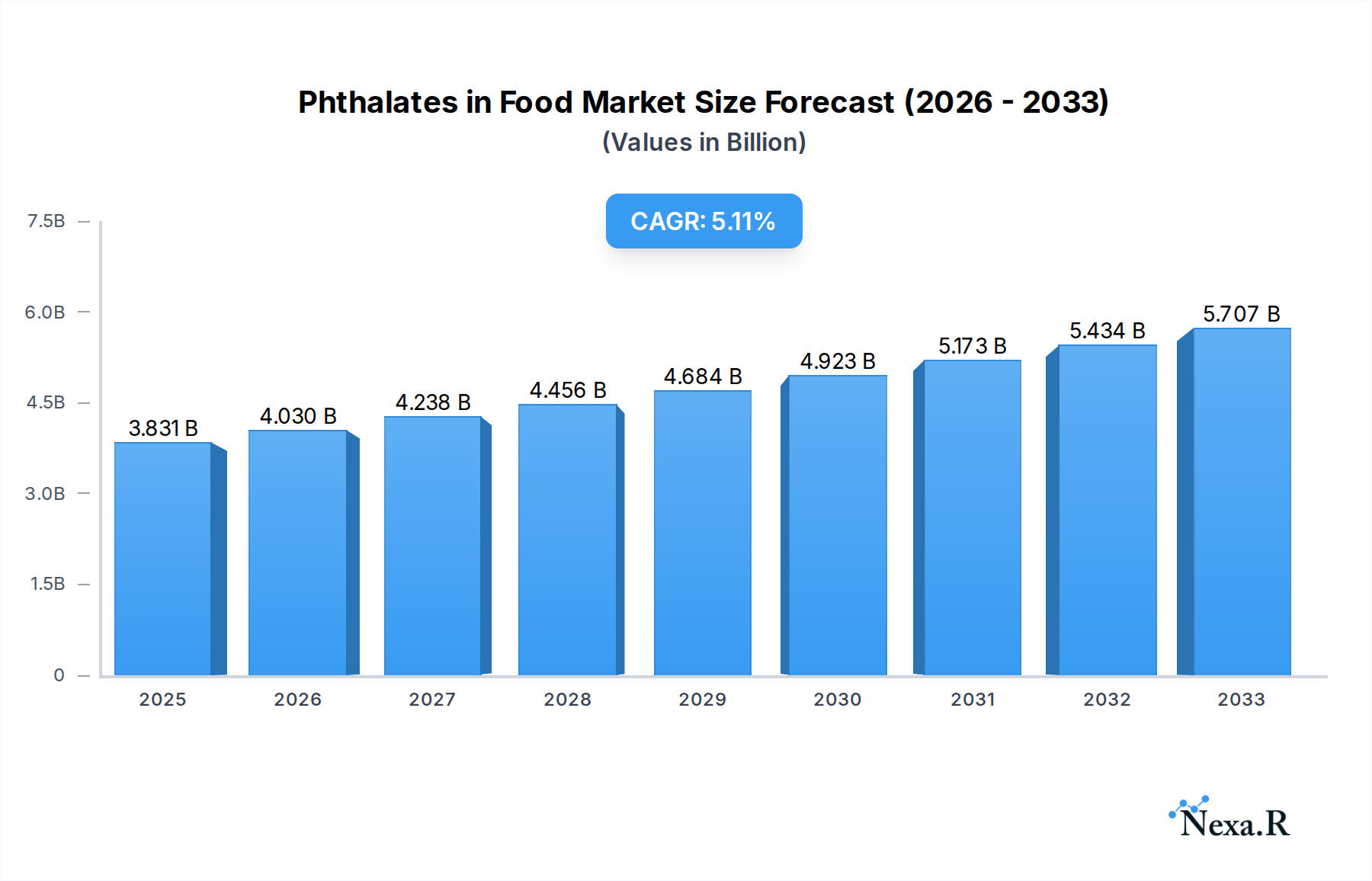

The global market for Phthalates in Food is poised for robust expansion, projected to reach a valuation of $3831 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 5.2% anticipated to sustain through 2033. This growth trajectory is underpinned by a confluence of escalating consumer demand for convenient food options, particularly in the fast-food sector, and a parallel rise in the consumption of fresh produce like fruits and vegetables, both of which increasingly rely on phthalate-containing packaging for preservation and presentation. The versatility of phthalates in enhancing the flexibility and durability of food packaging materials, coupled with their cost-effectiveness, makes them an indispensable component in the modern food supply chain. Innovations in plasticizer technology also contribute to this positive outlook, addressing some of the historical concerns associated with their use.

Phthalates in Food Market Size (In Billion)

However, the market is not without its headwinds. Heightened regulatory scrutiny and growing consumer awareness regarding the potential health implications of certain phthalates are prompting a shift towards phthalate-free alternatives, especially for direct food contact applications. The "Other" application segment, encompassing less prominent yet significant uses, is expected to witness moderate growth, influenced by niche market demands and emerging applications. Similarly, the "Other" phthalate types, excluding prominent ones like Di(2-ethylhexyl) Phthalate (DEHP) and Di-n-butyl Phthalate (DBP), will see nuanced performance driven by specialized industrial requirements and the development of novel plasticizers. Geographically, Asia Pacific, led by China and India, is anticipated to emerge as a dominant region due to its burgeoning population, rapid urbanization, and expanding food processing industry, thereby driving significant demand for phthalate-containing food packaging solutions.

Phthalates in Food Company Market Share

Unlock critical insights into the global Phthalates in Food market with this comprehensive industry report. This in-depth analysis provides a detailed examination of market dynamics, growth trends, regional dominance, product landscape, and future outlook, crucial for stakeholders navigating this evolving sector. Our report leverages extensive data and expert analysis to deliver actionable intelligence for chemical manufacturers, food packaging companies, regulatory bodies, and investors.

Phthalates in Food Market Dynamics & Structure

The global phthalates in food market is characterized by a moderately concentrated structure, with a few key players holding significant market share, alongside a growing number of regional and specialized manufacturers. Technological innovation is a primary driver, focusing on developing safer and more effective plasticizers that minimize migration into food products. Regulatory frameworks, particularly in developed economies, are increasingly stringent, pushing for the adoption of phthalate alternatives and stricter migration limits. Competitive product substitutes, such as alternative plasticizers and migration-resistant packaging materials, are gaining traction, posing a significant challenge to traditional phthalate usage. End-user demographics, driven by increasing consumer awareness of food safety and health concerns, are shifting demand towards products with reduced chemical exposure. Mergers and acquisitions (M&A) activity has been observed, as larger companies seek to consolidate their market position, expand their product portfolios, and acquire innovative technologies. For instance, recent M&A trends indicate a strategic focus on companies developing bio-based or non-phthalate plasticizers. The estimated market share of leading players in the historical period (2019-2024) averaged around 65% for the top five entities. Barriers to innovation include high R&D costs associated with developing novel plasticizers and navigating complex regulatory approval processes.

- Market Concentration: Moderately concentrated, with leading players like Covestro AG, Exxon Mobil Corporation, and BASF SE dominating.

- Technological Innovation: Focus on low-migration and non-phthalate alternatives, driven by health concerns and regulatory pressures.

- Regulatory Frameworks: Increasingly stringent regulations in North America and Europe are shaping product development and market access.

- Competitive Substitutes: Rise of alternative plasticizers and advanced packaging solutions impacting traditional phthalate demand.

- End-User Demographics: Growing consumer demand for safe and clean food products, influencing purchasing decisions.

- M&A Trends: Strategic acquisitions aimed at strengthening market presence and acquiring innovative technologies in the plasticizer segment. Estimated M&A deal volume in the historical period was approximately 15 transactions, valued at over $500 million.

Phthalates in Food Growth Trends & Insights

The phthalates in food market is projected to witness steady growth, influenced by evolving global food packaging standards and the persistent use of phthalates in various food contact materials, particularly in emerging economies. The market size for phthalates in food packaging is estimated to have reached approximately $1.2 billion in 2024 and is forecast to expand at a Compound Annual Growth Rate (CAGR) of 4.2% from 2025 to 2033. This growth is underpinned by the demand for flexible and durable food packaging solutions where phthalates have traditionally offered cost-effectiveness and performance benefits. Adoption rates of specific phthalate types are influenced by regional regulations and industry standards; for instance, the use of Di(2-ethylhexyl) Phthalate (DEHP) is declining in many developed regions due to health concerns, leading to a gradual shift towards alternatives like Di-n-butyl Phthalate (DBP) and other specialized plasticizers. Technological disruptions are primarily centered around the development of low-migration plasticizers and advanced barrier technologies within food packaging to minimize phthalate ingress. Consumer behavior shifts are critical, with a growing segment of the population actively seeking products with transparent ingredient lists and assurances of food safety, thereby indirectly influencing the demand for phthalate-free or low-phthalate packaging options. This conscious consumerism is compelling manufacturers to invest in research and development for compliant and safe plasticizers. The market penetration of alternative plasticizers is gradually increasing, albeit at a slower pace than anticipated due to cost considerations and established infrastructure for conventional phthalates. The estimated market size for alternative plasticizers in food contact applications is expected to reach $0.8 billion by 2025, growing at a CAGR of 5.5%. The market's resilience is also linked to its application in processed foods and convenience items where cost-effectiveness remains a significant factor for widespread adoption. Furthermore, the increasing global population and its demand for convenient and preserved food products will continue to drive the need for effective food packaging solutions. Innovations in polymer science are also playing a crucial role, enabling the development of packaging materials with enhanced properties that can reduce the necessity for high concentrations of plasticizers. The forecast period is expected to see a more pronounced divergence in growth between regions with stringent regulations and those with more lenient standards, creating distinct market dynamics. The estimated market share of DEHP in food applications is projected to decrease from 35% in 2024 to 28% by 2033, while other phthalates and non-phthalate alternatives will see an increase in their respective shares. The CAGR for the overall phthalates in food market is projected at 4.2% for the forecast period.

Dominant Regions, Countries, or Segments in Phthalates in Food

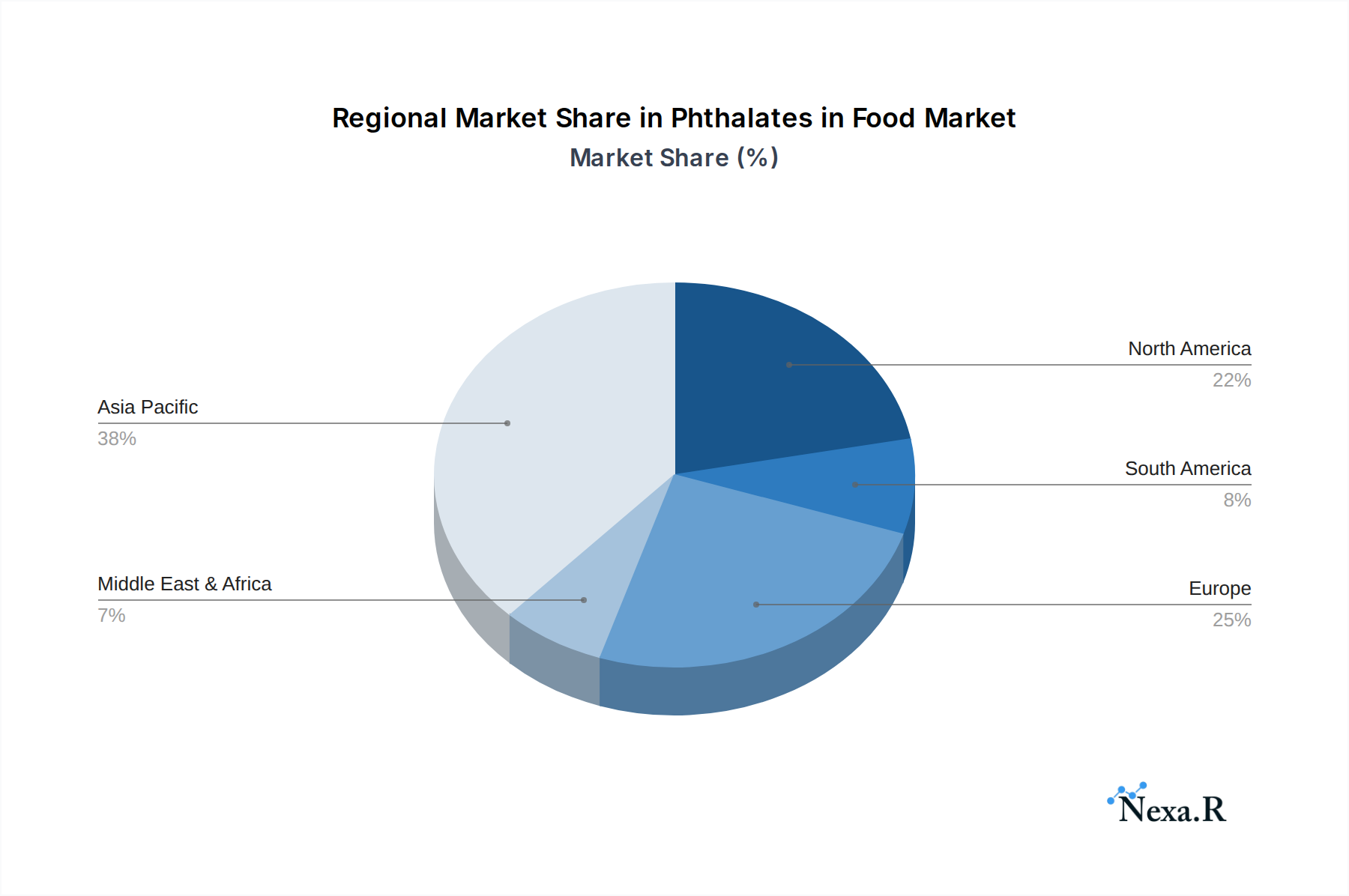

The Asia-Pacific region is emerging as the dominant force in the phthalates in food market, driven by a confluence of rapid economic growth, expanding food processing industries, and a large, growing population with increasing disposable incomes. Within this region, China stands out as a key country, boasting a robust manufacturing base for both phthalates and food packaging materials, alongside a substantial domestic market. The application segment of Fast Food is a significant growth driver, fueled by changing lifestyles and the convenience food trend, which necessitates durable and cost-effective packaging solutions. Di(2-ethylhexyl) Phthalate (DEHP) continues to hold a substantial market share in this region due to its cost-effectiveness and versatility, despite global regulatory pressures. However, Di-n-butyl Phthalate (DBP) and other phthalate types are gaining traction, especially in higher-value food segments and export-oriented markets.

Key drivers for Asia-Pacific's dominance include favorable government policies supporting industrial development, significant investments in food processing infrastructure, and the vast consumer base that drives demand for packaged foods. The market share of the Asia-Pacific region in the global phthalates in food market is estimated to be around 45% in 2025, with a projected growth rate of 5.1% CAGR during the forecast period. Within the fast-food segment, market penetration of phthalate-containing packaging is estimated at 70%, highlighting its integral role.

- Dominant Region: Asia-Pacific, with China as a leading country.

- Key Application Driver: Fast Food sector, owing to convenience and cost-effectiveness in packaging.

- Dominant Phthalate Type (Regional): DEHP, due to its established use and cost advantages, particularly in emerging economies.

- Growth Potential: High, driven by industrial expansion, rising disposable incomes, and increasing food processing capabilities.

- Economic Policies: Government initiatives supporting manufacturing and trade in food packaging contribute to market growth.

- Infrastructure Development: Investments in logistics and cold chain facilities for food products enhance demand for appropriate packaging.

- Market Share (Asia-Pacific): Estimated at 45% in 2025, projected to reach 50% by 2033.

- CAGR (Asia-Pacific): Projected at 5.1% for the forecast period.

Phthalates in Food Product Landscape

The phthalates in food product landscape is characterized by a focus on optimizing performance metrics for food contact applications, primarily in flexible packaging. Companies are innovating to develop phthalate formulations that offer superior flexibility, durability, and resistance to temperature fluctuations, crucial for preserving food quality during storage and transport. Unique selling propositions often revolve around cost-effectiveness and established performance, making certain phthalates like DEHP and DBP perennial choices in specific food segments, especially in regions with less stringent regulations. Technological advancements are geared towards enhancing the plasticizing efficiency of phthalates and minimizing their potential for migration. This includes developing specialized grades of phthalates and exploring novel additive packages that can improve their compatibility with various polymer matrices used in food packaging. The estimated market share for DEHP in flexible food packaging applications remains significant, around 38% in 2025, due to its balanced property profile and widespread adoption.

Key Drivers, Barriers & Challenges in Phthalates in Food

Key Drivers: The phthalates in food market is propelled by robust demand for flexible and cost-effective food packaging solutions, particularly in the expanding processed and convenience food sectors globally. Technological advancements in plasticizer production continue to offer performance benefits in terms of durability and flexibility. Furthermore, regulatory requirements in certain regions still permit the use of specific phthalates, supporting continued market demand. The growth of the fast-food industry and the increasing adoption of ready-to-eat meals are major demand catalysts.

Barriers & Challenges: Significant challenges include increasing global regulatory scrutiny and growing consumer concern regarding the health implications of phthalates, leading to a demand for safer alternatives. Stringent migration limits imposed by regulatory bodies necessitate significant R&D investment for compliance and product reformulation. Supply chain disruptions and volatility in raw material prices for phthalate production can impact manufacturing costs and availability. Competitive pressures from non-phthalate plasticizers and advanced barrier packaging materials are also key restraints. The estimated impact of regulatory restrictions on DEHP usage in North America and Europe is a projected market share decline of approximately 15% by 2033.

Emerging Opportunities in Phthalates in Food

Emerging opportunities lie in the development and adoption of novel, low-migration phthalates and bio-based plasticizers for food contact applications. The increasing consumer preference for transparent labeling and "phthalate-free" products presents a significant market for alternative solutions. Untapped markets in developing economies, where regulatory frameworks are evolving, offer potential for growth in food packaging. Innovative applications in specialized food packaging, such as active and intelligent packaging that requires specific material properties, also present new avenues for phthalate-based or alternative plasticizer solutions.

Growth Accelerators in the Phthalates in Food Industry

Long-term growth in the phthalates in food industry will be accelerated by strategic partnerships between chemical manufacturers and food packaging companies to co-develop compliant and high-performance materials. Technological breakthroughs in polymerization and extrusion processes that enhance plasticizer integration and reduce migration will be crucial. Market expansion strategies in underserved emerging economies, coupled with targeted product development for specific food categories, will further drive growth. The ongoing focus on sustainability and circular economy principles is also pushing innovation towards recyclable and biodegradable plasticizers, which could represent a significant growth area.

Key Players Shaping the Phthalates in Food Market

- Covestro AG

- Exxon Mobil Corporation

- UPC Technology Corporation

- Shandong Qilu Plasticizer Co.,Ltd

- BASF SE

- DIC CORPORATION

- LG Chem Ltd.

- Mitsui Chemicals

- Evonik Industries AG

- SABIC

Notable Milestones in Phthalates in Food Sector

- 2019: Increased regulatory focus on DEHP migration limits in the EU, leading to reformulation efforts.

- 2020: Launch of new research initiatives on alternative plasticizers by major chemical companies.

- 2021: Several food packaging manufacturers announce voluntary phase-out of certain phthalates for specific product lines.

- 2022: Adoption of updated food contact material regulations in several key Asian countries, impacting phthalate usage.

- 2023: Significant investment in R&D for bio-based plasticizers by leading industry players.

- 2024: Anticipated expansion of testing protocols for phthalate migration in various food matrices.

In-Depth Phthalates in Food Market Outlook

The future market for phthalates in food is characterized by a dual trajectory: continued reliance on established phthalates in cost-sensitive markets and rapid innovation towards safer, compliant alternatives in developed regions. Growth accelerators will stem from ongoing technological advancements in plasticizer efficacy and reduced migration, alongside strategic market expansion into emerging economies. The increasing emphasis on food safety and consumer well-being will continue to shape product development, creating significant opportunities for companies that can offer effective, compliant, and sustainable solutions. The estimated market value for phthalates in food is projected to reach $1.5 billion by 2033, with a CAGR of 4.2%.

Phthalates in Food Segmentation

-

1. Application

- 1.1. Fast Food

- 1.2. Fresh Fruits

- 1.3. Vegetables

- 1.4. Other

-

2. Types

- 2.1. Di(2-ethylhexyl) Phthalate (DEHP)

- 2.2. Di-n-butyl Phthalate (DBP)

- 2.3. Other

Phthalates in Food Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Phthalates in Food Regional Market Share

Geographic Coverage of Phthalates in Food

Phthalates in Food REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Phthalates in Food Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Fast Food

- 5.1.2. Fresh Fruits

- 5.1.3. Vegetables

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Di(2-ethylhexyl) Phthalate (DEHP)

- 5.2.2. Di-n-butyl Phthalate (DBP)

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Phthalates in Food Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Fast Food

- 6.1.2. Fresh Fruits

- 6.1.3. Vegetables

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Di(2-ethylhexyl) Phthalate (DEHP)

- 6.2.2. Di-n-butyl Phthalate (DBP)

- 6.2.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Phthalates in Food Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Fast Food

- 7.1.2. Fresh Fruits

- 7.1.3. Vegetables

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Di(2-ethylhexyl) Phthalate (DEHP)

- 7.2.2. Di-n-butyl Phthalate (DBP)

- 7.2.3. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Phthalates in Food Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Fast Food

- 8.1.2. Fresh Fruits

- 8.1.3. Vegetables

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Di(2-ethylhexyl) Phthalate (DEHP)

- 8.2.2. Di-n-butyl Phthalate (DBP)

- 8.2.3. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Phthalates in Food Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Fast Food

- 9.1.2. Fresh Fruits

- 9.1.3. Vegetables

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Di(2-ethylhexyl) Phthalate (DEHP)

- 9.2.2. Di-n-butyl Phthalate (DBP)

- 9.2.3. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Phthalates in Food Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Fast Food

- 10.1.2. Fresh Fruits

- 10.1.3. Vegetables

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Di(2-ethylhexyl) Phthalate (DEHP)

- 10.2.2. Di-n-butyl Phthalate (DBP)

- 10.2.3. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Covestro AG

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Exxon Mobil Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 UPC Technology Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Shandong Qilu Plasticizer Co.

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Ltd

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 BASF SE

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 DIC CORPORATION

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 LG Chem Ltd.

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Mitsui Chemicals

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Evonik Industries AG

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 SABIC

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Covestro AG

List of Figures

- Figure 1: Global Phthalates in Food Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Phthalates in Food Revenue (million), by Application 2025 & 2033

- Figure 3: North America Phthalates in Food Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Phthalates in Food Revenue (million), by Types 2025 & 2033

- Figure 5: North America Phthalates in Food Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Phthalates in Food Revenue (million), by Country 2025 & 2033

- Figure 7: North America Phthalates in Food Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Phthalates in Food Revenue (million), by Application 2025 & 2033

- Figure 9: South America Phthalates in Food Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Phthalates in Food Revenue (million), by Types 2025 & 2033

- Figure 11: South America Phthalates in Food Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Phthalates in Food Revenue (million), by Country 2025 & 2033

- Figure 13: South America Phthalates in Food Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Phthalates in Food Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Phthalates in Food Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Phthalates in Food Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Phthalates in Food Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Phthalates in Food Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Phthalates in Food Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Phthalates in Food Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Phthalates in Food Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Phthalates in Food Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Phthalates in Food Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Phthalates in Food Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Phthalates in Food Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Phthalates in Food Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Phthalates in Food Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Phthalates in Food Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Phthalates in Food Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Phthalates in Food Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Phthalates in Food Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Phthalates in Food Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Phthalates in Food Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Phthalates in Food Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Phthalates in Food Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Phthalates in Food Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Phthalates in Food Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Phthalates in Food Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Phthalates in Food Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Phthalates in Food Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Phthalates in Food Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Phthalates in Food Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Phthalates in Food Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Phthalates in Food Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Phthalates in Food Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Phthalates in Food Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Phthalates in Food Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Phthalates in Food Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Phthalates in Food Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Phthalates in Food Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Phthalates in Food?

The projected CAGR is approximately 5.2%.

2. Which companies are prominent players in the Phthalates in Food?

Key companies in the market include Covestro AG, Exxon Mobil Corporation, UPC Technology Corporation, Shandong Qilu Plasticizer Co., Ltd, BASF SE, DIC CORPORATION, LG Chem Ltd., Mitsui Chemicals, Evonik Industries AG, SABIC.

3. What are the main segments of the Phthalates in Food?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 3831 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Phthalates in Food," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Phthalates in Food report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Phthalates in Food?

To stay informed about further developments, trends, and reports in the Phthalates in Food, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence