Key Insights

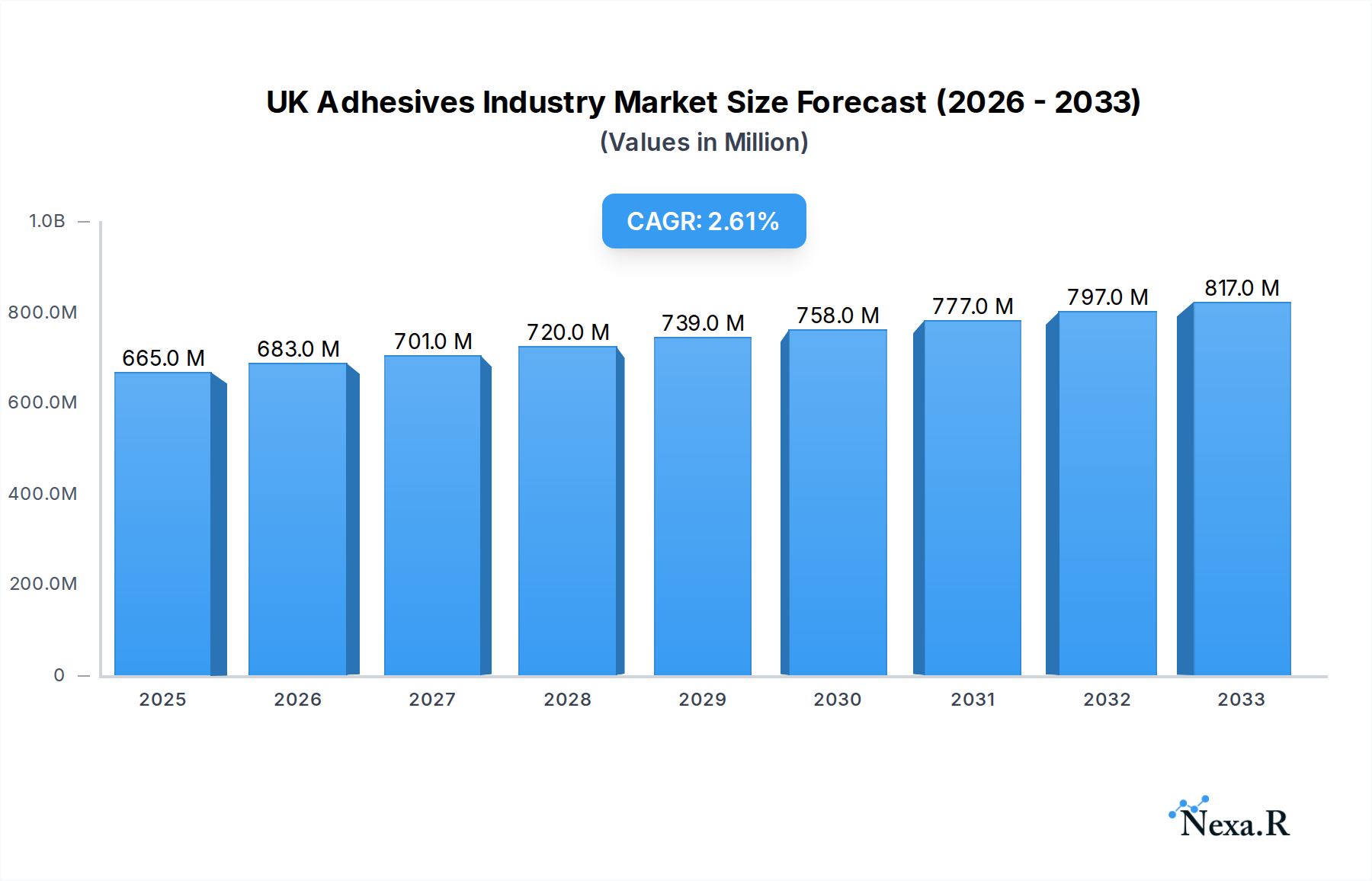

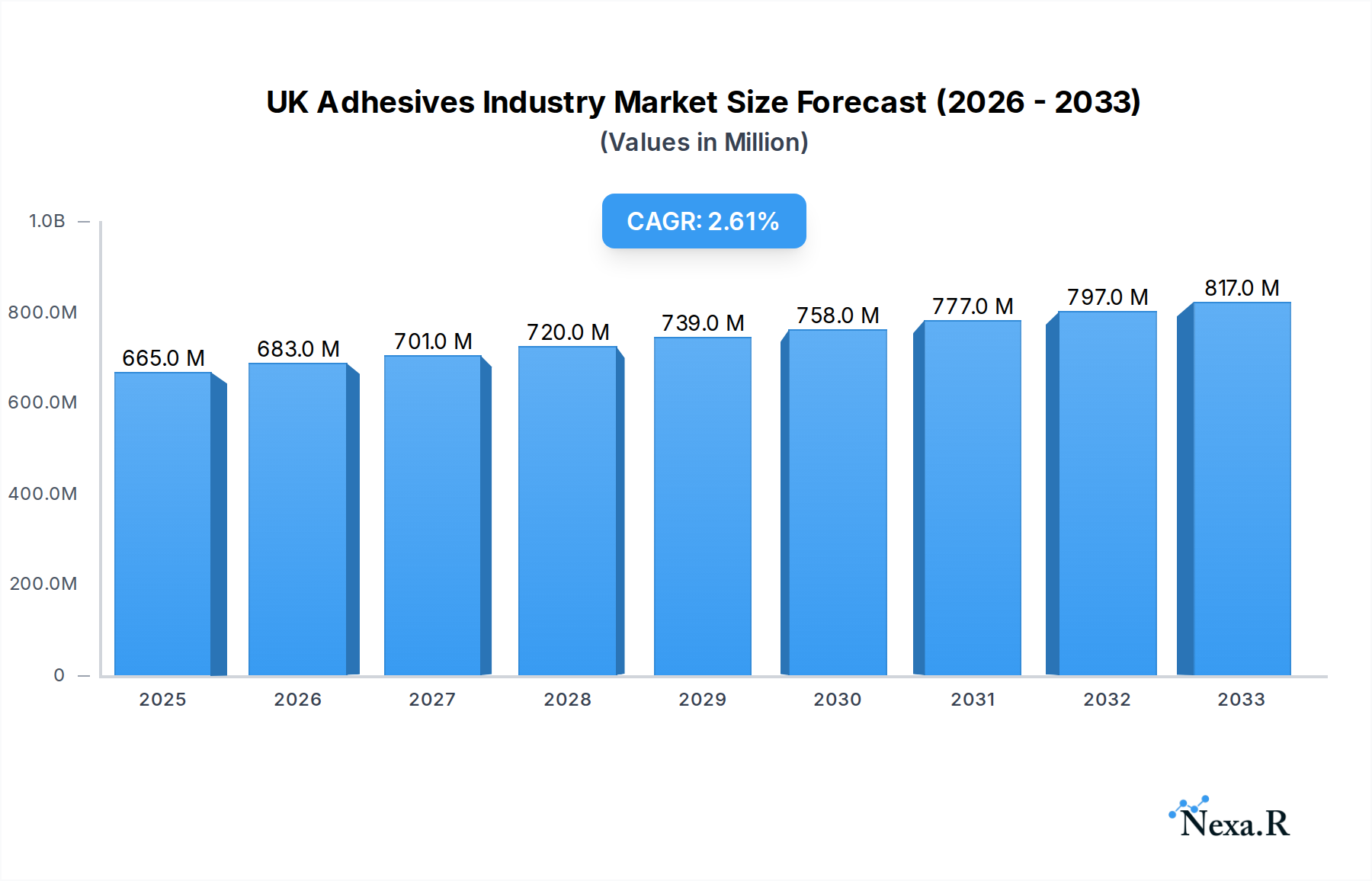

The UK adhesives market is poised for steady growth, projected to reach approximately £665 million by 2025, driven by a consistent CAGR of 2.6% over the forecast period. This expansion is underpinned by robust demand across a diverse range of end-user industries, most notably automotive and building & construction, which continue to benefit from infrastructure development and a revitalized manufacturing sector. The increasing adoption of advanced adhesive technologies, such as reactive and UV-cured systems, is further fueling market penetration due to their superior performance characteristics and environmental advantages. Furthermore, the growing emphasis on sustainable solutions is spurring innovation in water-borne and solvent-borne adhesives with reduced VOC emissions, aligning with stringent regulatory frameworks and consumer preferences.

UK Adhesives Industry Market Size (In Million)

The market's trajectory is further shaped by key players like Henkel AG & Co KGaA, 3M, and Arkema Group, whose continuous investment in research and development is crucial for introducing novel formulations and expanding their product portfolios. While the market presents significant opportunities, potential restraints include fluctuating raw material costs, particularly for key resins like acrylic and epoxy, and the ongoing challenges associated with supply chain disruptions. However, the inherent versatility of adhesives, their ability to replace traditional joining methods like welding and riveting, and their critical role in lightweighting initiatives within the automotive and aerospace sectors are expected to offset these challenges, ensuring sustained market vitality and an estimated 2.8% growth rate between 2025 and 2026.

UK Adhesives Industry Company Market Share

This comprehensive report provides an in-depth analysis of the UK adhesives industry, offering critical insights into market dynamics, growth trajectories, and emerging opportunities. Covering the period from 2019 to 2033, with a base year of 2025, this report delves into the intricate landscape of the UK adhesives market, examining its structure, key drivers, challenges, and future outlook. We explore parent and child markets, providing a granular view of market segmentation by end-user industry, technology, and resin type.

UK Adhesives Industry Market Dynamics & Structure

The UK adhesives industry exhibits a moderately concentrated market structure, with a blend of global chemical giants and specialized domestic manufacturers. Key players like Henkel AG & Co KGaA, 3M, Arkema Group, and Huntsman International LLC dominate market share through extensive product portfolios and significant R&D investments. Technological innovation, particularly in sustainable and high-performance adhesives, acts as a primary driver. Regulatory frameworks, such as REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), influence product development and market entry. Competitive product substitutes, including mechanical fasteners and welding, present a constant challenge, requiring adhesive manufacturers to emphasize performance, cost-effectiveness, and ease of application. End-user demographics, driven by growth in construction, automotive, and packaging sectors, significantly shape demand. Mergers and acquisitions (M&A) are prevalent, with companies like H.B. Fuller strategically acquiring businesses to expand their market reach and product offerings, reinforcing market consolidation.

- Market Concentration: Moderately concentrated, with key global players holding substantial market share.

- Innovation Drivers: Demand for sustainable, eco-friendly, and high-performance adhesives for diverse applications.

- Regulatory Influence: REACH compliance and environmental regulations shaping product formulations.

- Competitive Landscape: Competition from mechanical fasteners and alternative joining methods.

- M&A Activity: Strategic acquisitions to enhance market position and product portfolios.

UK Adhesives Industry Growth Trends & Insights

The UK adhesives market is poised for robust growth, propelled by evolving industrial demands and technological advancements. Over the forecast period (2025–2033), the market is expected to witness a healthy Compound Annual Growth Rate (CAGR), indicating sustained expansion. This growth is fueled by increasing adoption rates of advanced adhesive technologies across various end-user industries, such as automotive (lightweighting and electric vehicle manufacturing), building and construction (energy-efficient building solutions), and packaging (sustainable and high-barrier packaging). Technological disruptions, including the development of bio-based and recyclable adhesives, are redefining market offerings and consumer preferences. Shifts in consumer behavior, prioritizing sustainability and product longevity, are further accelerating the demand for innovative adhesive solutions. Market penetration is expected to deepen as new applications emerge and existing ones are optimized with next-generation adhesives.

The market size evolution is intrinsically linked to the performance of key sectors within the UK economy. For instance, the burgeoning demand for advanced materials in the automotive sector, driven by the transition to electric vehicles, necessitates specialized adhesives for battery assembly, structural bonding, and interior components. Similarly, the construction industry's focus on energy efficiency and modular building techniques creates a sustained need for high-performance sealants and adhesives that offer excellent thermal insulation and structural integrity. The packaging industry, under increasing pressure to adopt sustainable practices, is witnessing a surge in demand for adhesives that facilitate recyclability and reduce material usage, such as primer-free laminating adhesives and hot melts with enhanced debonding capabilities. The healthcare sector, with its stringent regulatory requirements and demand for biocompatible materials, represents a niche but high-value growth segment for specialized adhesives. The report details these trends, providing quantitative metrics such as projected market size in million units and CAGR projections for the forecast period, alongside qualitative analyses of the factors influencing adoption rates and consumer preferences.

Dominant Regions, Countries, or Segments in UK Adhesives Industry

Within the UK adhesives industry, the Building and Construction end-user industry stands out as a dominant segment, consistently driving market growth. This dominance is attributed to several interconnected factors, including ongoing infrastructure development, a strong focus on energy-efficient building practices, and the increasing use of prefabricated and modular construction techniques. The Automotive sector also represents a significant and growing segment, particularly with the UK's commitment to electric vehicle production, requiring advanced bonding solutions for lightweighting and battery integration.

- Building and Construction: This segment is propelled by government initiatives for sustainable infrastructure, renovation projects, and new housing development. The demand for adhesives in flooring, roofing, insulation, and window/door sealing remains robust.

- Automotive: The shift towards electric vehicles, lightweighting initiatives, and stringent safety standards are driving demand for structural adhesives, sealants, and specialty adhesives for battery packs and interior components.

- Packaging: The growth in e-commerce and the increasing demand for sustainable packaging solutions are key drivers for hot melt adhesives and other specialized formulations that enhance recyclability and product protection.

Technologically, Hot Melt adhesives continue to hold a significant market share due to their fast setting times and versatility across numerous applications, especially in packaging and woodworking. However, Reactive adhesives, including epoxies and polyurethanes, are witnessing strong growth due to their superior bonding strength and durability required in demanding applications like automotive and aerospace. In terms of resin types, Acrylic and Polyurethane resins are increasingly favored for their excellent performance characteristics and growing adoption in high-performance applications. The Water-borne adhesive technology segment is also expanding, driven by increasing environmental regulations and a preference for low-VOC (Volatile Organic Compound) products, particularly in the building and construction and woodworking sectors. Market share analysis within these segments reveals a dynamic interplay between established technologies and emerging innovations, with a clear trend towards higher performance, greater sustainability, and specialized application-specific solutions.

UK Adhesives Industry Product Landscape

The UK adhesives industry is characterized by continuous product innovation focused on enhanced performance, sustainability, and application-specific solutions. Key developments include the introduction of bio-based and solvent-free adhesives, addressing growing environmental concerns. High-strength structural adhesives for lightweighting in automotive and aerospace remain a significant focus, offering superior mechanical properties and durability. Furthermore, advancements in UV-cured adhesives are providing faster curing times and improved process efficiency. The product landscape is increasingly driven by demands for recyclability, with new formulations designed for easier debonding or compatibility with recycling streams, particularly in the packaging sector. Unique selling propositions often revolve around achieving faster assembly times, greater product lifespan, and reduced environmental impact through innovative adhesive technologies.

Key Drivers, Barriers & Challenges in UK Adhesives Industry

Key Drivers:

- Technological Advancements: Development of high-performance, sustainable, and application-specific adhesives.

- Growth in End-User Industries: Expansion in automotive, construction, packaging, and healthcare sectors.

- Sustainability Initiatives: Increasing demand for eco-friendly and recyclable adhesive solutions.

- Government Support: Favorable policies and investments in key industrial sectors.

Barriers & Challenges:

- Supply Chain Disruptions: Volatility in raw material prices and availability impacting production costs.

- Regulatory Hurdles: Stringent environmental and safety regulations requiring continuous product reformulation and compliance.

- Competitive Pressures: Intense competition from both established players and emerging low-cost alternatives.

- Skilled Workforce Shortage: Difficulty in finding and retaining skilled personnel for manufacturing and R&D.

- Economic Volatility: Fluctuations in the UK economy impacting demand from key end-user industries.

Emerging Opportunities in UK Adhesives Industry

Emerging opportunities in the UK adhesives industry lie in the growing demand for advanced bonding solutions in sectors like renewable energy (e.g., wind turbine manufacturing and solar panel assembly), where specialized adhesives are crucial for durability and performance. The increasing adoption of smart manufacturing and Industry 4.0 principles presents opportunities for adhesives that enable automated application processes and in-line quality control. Furthermore, the circular economy drive is creating a strong demand for adhesives that facilitate product disassembly and material recovery, opening avenues for innovative debonding technologies. The healthcare sector's continuous need for biocompatible and sterilizable adhesives for medical devices and diagnostics also represents a high-value growth area.

Growth Accelerators in the UK Adhesives Industry Industry

Several catalysts are accelerating long-term growth within the UK adhesives industry. Technological breakthroughs in material science are enabling the development of adhesives with unprecedented strength-to-weight ratios, thermal resistance, and conductivity, catering to advanced applications. Strategic partnerships between adhesive manufacturers, material suppliers, and end-users are fostering collaborative innovation and accelerating the adoption of new solutions. Market expansion strategies, both domestically and internationally, are crucial, with companies actively seeking to penetrate new geographical regions and application areas. Furthermore, a continued focus on sustainability and the development of bio-based and biodegradable adhesives will be a significant growth accelerator, aligning with global environmental agendas and consumer preferences.

Key Players Shaping the UK Adhesives Industry Market

- Henkel AG & Co KGaA

- 3M

- Arkema Group

- Huntsman International LLC

- Beardow Adams

- Dow

- H B Fuller Company

- Sika AG

- AVERY DENNISON CORPORATION

- Follmann Chemie GmbH

Notable Milestones in UK Adhesives Industry Sector

- May 2022: Henkel introduced new products, such as Loctite Liofol LA 7818 RE / 6231 RE and Loctite Liofol LA 7102 RE / 6902 RE, to promote recyclability in the packaging industry.

- March 2022: Bostik signed an agreement with DGE for distribution throughout Europe, Middle East & Africa. The agreement includes Born2BondTM engineering adhesives developed for 'by-the-dot' bonding applications in specific industries, such as automotive, electronics, luxury packaging, medical devices, and MRO.

- February 2022: H.B. Fuller announced the acquisition of Fourny NV to strengthen its Construction Adhesives business in Europe.

In-Depth UK Adhesives Industry Market Outlook

The future outlook for the UK adhesives industry is exceptionally promising, driven by a convergence of technological innovation and evolving market demands. Growth accelerators include the relentless pursuit of advanced, sustainable adhesive solutions that meet stringent environmental regulations and consumer preferences for eco-friendly products. Strategic partnerships between industry players and research institutions will continue to foster groundbreaking developments in material science. Furthermore, the expansion of key end-user industries, particularly in areas like electric vehicles, renewable energy, and advanced manufacturing, will create sustained demand for high-performance bonding agents. The UK's commitment to innovation and its strong industrial base position it favorably to capitalize on these evolving market dynamics, ensuring robust growth and significant opportunities for market leaders.

UK Adhesives Industry Segmentation

-

1. End User Industry

- 1.1. Aerospace

- 1.2. Automotive

- 1.3. Building and Construction

- 1.4. Footwear and Leather

- 1.5. Healthcare

- 1.6. Packaging

- 1.7. Woodworking and Joinery

- 1.8. Other End-user Industries

-

2. Technology

- 2.1. Hot Melt

- 2.2. Reactive

- 2.3. Solvent-borne

- 2.4. UV Cured Adhesives

- 2.5. Water-borne

-

3. Resin

- 3.1. Acrylic

- 3.2. Cyanoacrylate

- 3.3. Epoxy

- 3.4. Polyurethane

- 3.5. Silicone

- 3.6. VAE/EVA

- 3.7. Other Resins

UK Adhesives Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

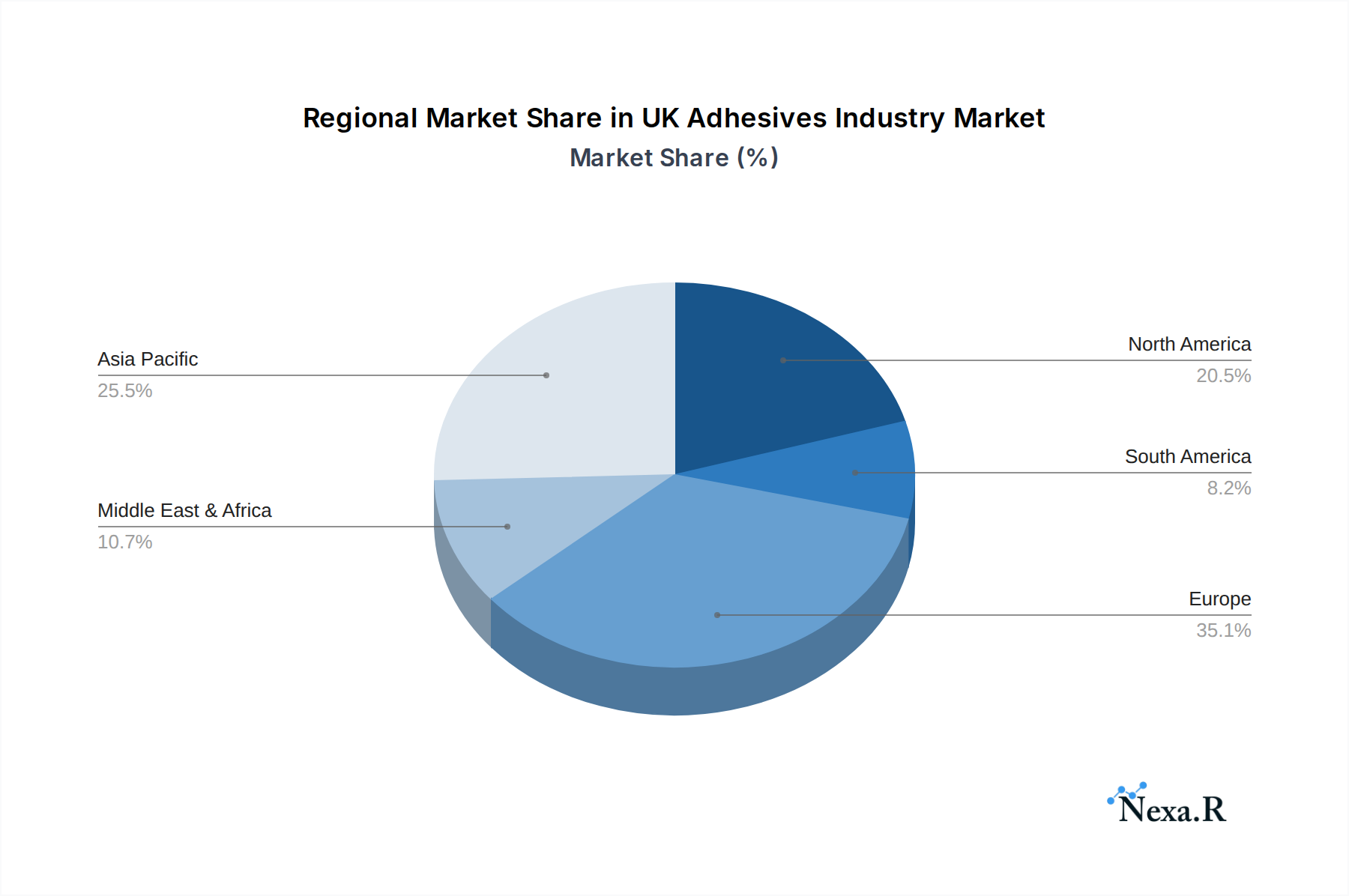

UK Adhesives Industry Regional Market Share

Geographic Coverage of UK Adhesives Industry

UK Adhesives Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Aerospace

- 5.1.2. Automotive

- 5.1.3. Building and Construction

- 5.1.4. Footwear and Leather

- 5.1.5. Healthcare

- 5.1.6. Packaging

- 5.1.7. Woodworking and Joinery

- 5.1.8. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Hot Melt

- 5.2.2. Reactive

- 5.2.3. Solvent-borne

- 5.2.4. UV Cured Adhesives

- 5.2.5. Water-borne

- 5.3. Market Analysis, Insights and Forecast - by Resin

- 5.3.1. Acrylic

- 5.3.2. Cyanoacrylate

- 5.3.3. Epoxy

- 5.3.4. Polyurethane

- 5.3.5. Silicone

- 5.3.6. VAE/EVA

- 5.3.7. Other Resins

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. South America

- 5.4.3. Europe

- 5.4.4. Middle East & Africa

- 5.4.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Global UK Adhesives Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 6.1.1. Aerospace

- 6.1.2. Automotive

- 6.1.3. Building and Construction

- 6.1.4. Footwear and Leather

- 6.1.5. Healthcare

- 6.1.6. Packaging

- 6.1.7. Woodworking and Joinery

- 6.1.8. Other End-user Industries

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Hot Melt

- 6.2.2. Reactive

- 6.2.3. Solvent-borne

- 6.2.4. UV Cured Adhesives

- 6.2.5. Water-borne

- 6.3. Market Analysis, Insights and Forecast - by Resin

- 6.3.1. Acrylic

- 6.3.2. Cyanoacrylate

- 6.3.3. Epoxy

- 6.3.4. Polyurethane

- 6.3.5. Silicone

- 6.3.6. VAE/EVA

- 6.3.7. Other Resins

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 7. North America UK Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by End User Industry

- 7.1.1. Aerospace

- 7.1.2. Automotive

- 7.1.3. Building and Construction

- 7.1.4. Footwear and Leather

- 7.1.5. Healthcare

- 7.1.6. Packaging

- 7.1.7. Woodworking and Joinery

- 7.1.8. Other End-user Industries

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Hot Melt

- 7.2.2. Reactive

- 7.2.3. Solvent-borne

- 7.2.4. UV Cured Adhesives

- 7.2.5. Water-borne

- 7.3. Market Analysis, Insights and Forecast - by Resin

- 7.3.1. Acrylic

- 7.3.2. Cyanoacrylate

- 7.3.3. Epoxy

- 7.3.4. Polyurethane

- 7.3.5. Silicone

- 7.3.6. VAE/EVA

- 7.3.7. Other Resins

- 7.1. Market Analysis, Insights and Forecast - by End User Industry

- 8. South America UK Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by End User Industry

- 8.1.1. Aerospace

- 8.1.2. Automotive

- 8.1.3. Building and Construction

- 8.1.4. Footwear and Leather

- 8.1.5. Healthcare

- 8.1.6. Packaging

- 8.1.7. Woodworking and Joinery

- 8.1.8. Other End-user Industries

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Hot Melt

- 8.2.2. Reactive

- 8.2.3. Solvent-borne

- 8.2.4. UV Cured Adhesives

- 8.2.5. Water-borne

- 8.3. Market Analysis, Insights and Forecast - by Resin

- 8.3.1. Acrylic

- 8.3.2. Cyanoacrylate

- 8.3.3. Epoxy

- 8.3.4. Polyurethane

- 8.3.5. Silicone

- 8.3.6. VAE/EVA

- 8.3.7. Other Resins

- 8.1. Market Analysis, Insights and Forecast - by End User Industry

- 9. Europe UK Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by End User Industry

- 9.1.1. Aerospace

- 9.1.2. Automotive

- 9.1.3. Building and Construction

- 9.1.4. Footwear and Leather

- 9.1.5. Healthcare

- 9.1.6. Packaging

- 9.1.7. Woodworking and Joinery

- 9.1.8. Other End-user Industries

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Hot Melt

- 9.2.2. Reactive

- 9.2.3. Solvent-borne

- 9.2.4. UV Cured Adhesives

- 9.2.5. Water-borne

- 9.3. Market Analysis, Insights and Forecast - by Resin

- 9.3.1. Acrylic

- 9.3.2. Cyanoacrylate

- 9.3.3. Epoxy

- 9.3.4. Polyurethane

- 9.3.5. Silicone

- 9.3.6. VAE/EVA

- 9.3.7. Other Resins

- 9.1. Market Analysis, Insights and Forecast - by End User Industry

- 10. Middle East & Africa UK Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by End User Industry

- 10.1.1. Aerospace

- 10.1.2. Automotive

- 10.1.3. Building and Construction

- 10.1.4. Footwear and Leather

- 10.1.5. Healthcare

- 10.1.6. Packaging

- 10.1.7. Woodworking and Joinery

- 10.1.8. Other End-user Industries

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. Hot Melt

- 10.2.2. Reactive

- 10.2.3. Solvent-borne

- 10.2.4. UV Cured Adhesives

- 10.2.5. Water-borne

- 10.3. Market Analysis, Insights and Forecast - by Resin

- 10.3.1. Acrylic

- 10.3.2. Cyanoacrylate

- 10.3.3. Epoxy

- 10.3.4. Polyurethane

- 10.3.5. Silicone

- 10.3.6. VAE/EVA

- 10.3.7. Other Resins

- 10.1. Market Analysis, Insights and Forecast - by End User Industry

- 11. Asia Pacific UK Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by End User Industry

- 11.1.1. Aerospace

- 11.1.2. Automotive

- 11.1.3. Building and Construction

- 11.1.4. Footwear and Leather

- 11.1.5. Healthcare

- 11.1.6. Packaging

- 11.1.7. Woodworking and Joinery

- 11.1.8. Other End-user Industries

- 11.2. Market Analysis, Insights and Forecast - by Technology

- 11.2.1. Hot Melt

- 11.2.2. Reactive

- 11.2.3. Solvent-borne

- 11.2.4. UV Cured Adhesives

- 11.2.5. Water-borne

- 11.3. Market Analysis, Insights and Forecast - by Resin

- 11.3.1. Acrylic

- 11.3.2. Cyanoacrylate

- 11.3.3. Epoxy

- 11.3.4. Polyurethane

- 11.3.5. Silicone

- 11.3.6. VAE/EVA

- 11.3.7. Other Resins

- 11.1. Market Analysis, Insights and Forecast - by End User Industry

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Henkel AG & Co KGaA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 3M

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Arkema Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Huntsman International LLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Beardow Adams

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Dow

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 H B Fuller Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Sika A

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 AVERY DENNISON CORPORATION

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Follmann Chemie GmbH

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Henkel AG & Co KGaA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global UK Adhesives Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America UK Adhesives Industry Revenue (million), by End User Industry 2025 & 2033

- Figure 3: North America UK Adhesives Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 4: North America UK Adhesives Industry Revenue (million), by Technology 2025 & 2033

- Figure 5: North America UK Adhesives Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 6: North America UK Adhesives Industry Revenue (million), by Resin 2025 & 2033

- Figure 7: North America UK Adhesives Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 8: North America UK Adhesives Industry Revenue (million), by Country 2025 & 2033

- Figure 9: North America UK Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: South America UK Adhesives Industry Revenue (million), by End User Industry 2025 & 2033

- Figure 11: South America UK Adhesives Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 12: South America UK Adhesives Industry Revenue (million), by Technology 2025 & 2033

- Figure 13: South America UK Adhesives Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 14: South America UK Adhesives Industry Revenue (million), by Resin 2025 & 2033

- Figure 15: South America UK Adhesives Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 16: South America UK Adhesives Industry Revenue (million), by Country 2025 & 2033

- Figure 17: South America UK Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe UK Adhesives Industry Revenue (million), by End User Industry 2025 & 2033

- Figure 19: Europe UK Adhesives Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 20: Europe UK Adhesives Industry Revenue (million), by Technology 2025 & 2033

- Figure 21: Europe UK Adhesives Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: Europe UK Adhesives Industry Revenue (million), by Resin 2025 & 2033

- Figure 23: Europe UK Adhesives Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 24: Europe UK Adhesives Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Europe UK Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East & Africa UK Adhesives Industry Revenue (million), by End User Industry 2025 & 2033

- Figure 27: Middle East & Africa UK Adhesives Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 28: Middle East & Africa UK Adhesives Industry Revenue (million), by Technology 2025 & 2033

- Figure 29: Middle East & Africa UK Adhesives Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 30: Middle East & Africa UK Adhesives Industry Revenue (million), by Resin 2025 & 2033

- Figure 31: Middle East & Africa UK Adhesives Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 32: Middle East & Africa UK Adhesives Industry Revenue (million), by Country 2025 & 2033

- Figure 33: Middle East & Africa UK Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Asia Pacific UK Adhesives Industry Revenue (million), by End User Industry 2025 & 2033

- Figure 35: Asia Pacific UK Adhesives Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 36: Asia Pacific UK Adhesives Industry Revenue (million), by Technology 2025 & 2033

- Figure 37: Asia Pacific UK Adhesives Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 38: Asia Pacific UK Adhesives Industry Revenue (million), by Resin 2025 & 2033

- Figure 39: Asia Pacific UK Adhesives Industry Revenue Share (%), by Resin 2025 & 2033

- Figure 40: Asia Pacific UK Adhesives Industry Revenue (million), by Country 2025 & 2033

- Figure 41: Asia Pacific UK Adhesives Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global UK Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 2: Global UK Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 3: Global UK Adhesives Industry Revenue million Forecast, by Resin 2020 & 2033

- Table 4: Global UK Adhesives Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: Global UK Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 6: Global UK Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 7: Global UK Adhesives Industry Revenue million Forecast, by Resin 2020 & 2033

- Table 8: Global UK Adhesives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: United States UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Canada UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Mexico UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: Global UK Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 13: Global UK Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 14: Global UK Adhesives Industry Revenue million Forecast, by Resin 2020 & 2033

- Table 15: Global UK Adhesives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 16: Brazil UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: Argentina UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Rest of South America UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 19: Global UK Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 20: Global UK Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 21: Global UK Adhesives Industry Revenue million Forecast, by Resin 2020 & 2033

- Table 22: Global UK Adhesives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 23: United Kingdom UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Germany UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: France UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Italy UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Spain UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Russia UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 29: Benelux UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Nordics UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Europe UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Global UK Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 33: Global UK Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 34: Global UK Adhesives Industry Revenue million Forecast, by Resin 2020 & 2033

- Table 35: Global UK Adhesives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 36: Turkey UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Israel UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: GCC UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 39: North Africa UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: South Africa UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: Rest of Middle East & Africa UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Global UK Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 43: Global UK Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 44: Global UK Adhesives Industry Revenue million Forecast, by Resin 2020 & 2033

- Table 45: Global UK Adhesives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 46: China UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 47: India UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Japan UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 49: South Korea UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: ASEAN UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 51: Oceania UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Rest of Asia Pacific UK Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Adhesives Industry?

The projected CAGR is approximately 2.6%.

2. Which companies are prominent players in the UK Adhesives Industry?

Key companies in the market include Henkel AG & Co KGaA, 3M, Arkema Group, Huntsman International LLC, Beardow Adams, Dow, H B Fuller Company, Sika A, AVERY DENNISON CORPORATION, Follmann Chemie GmbH.

3. What are the main segments of the UK Adhesives Industry?

The market segments include End User Industry, Technology, Resin.

4. Can you provide details about the market size?

The market size is estimated to be USD 644.3 million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand from the Construction Industry in Germany; Growing Usage in the Healthcare Industry.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

The Rising Environmental Concerns; Other Restrains.

8. Can you provide examples of recent developments in the market?

May 2022: Henkel introduced new products, such as Loctite Liofol LA 7818 RE / 6231 RE and Loctite Liofol LA 7102 RE / 6902 RE, to promote recyclability in the packaging industry.March 2022: Bostik signed an agreement with DGE for distribution throughout Europe, Middle East & Africa. The agreement includes Born2BondTM engineering adhesives developed for 'by-the-dot' bonding applications in specific industries, such as automotive, electronics, luxury packaging, medical devices, and MRO.February 2022: H.B. Fuller announced the acquisition of Fourny NV to strengthen its Construction Adhesives business in Europe.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Adhesives Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Adhesives Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Adhesives Industry?

To stay informed about further developments, trends, and reports in the UK Adhesives Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence