Key Insights

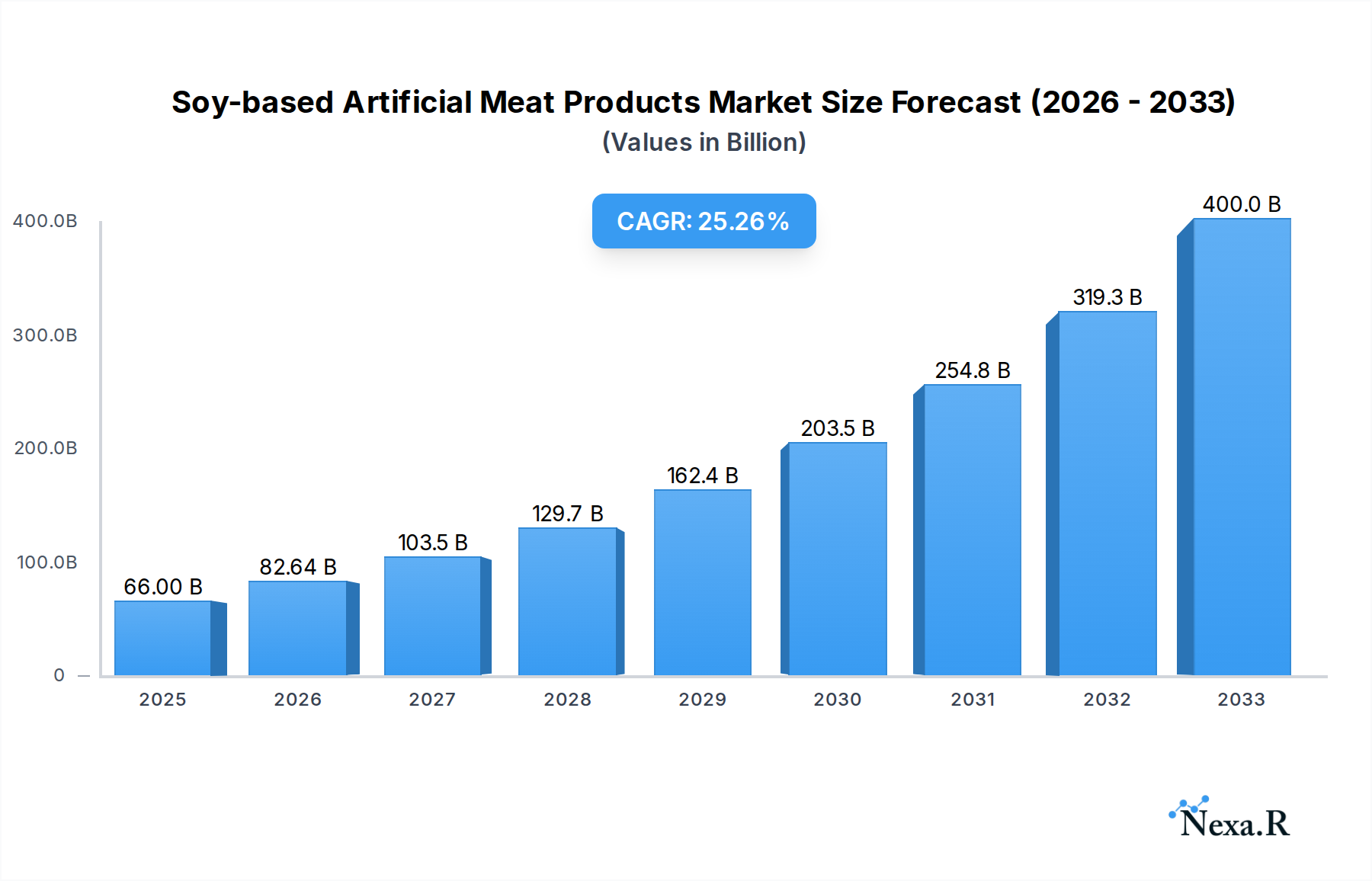

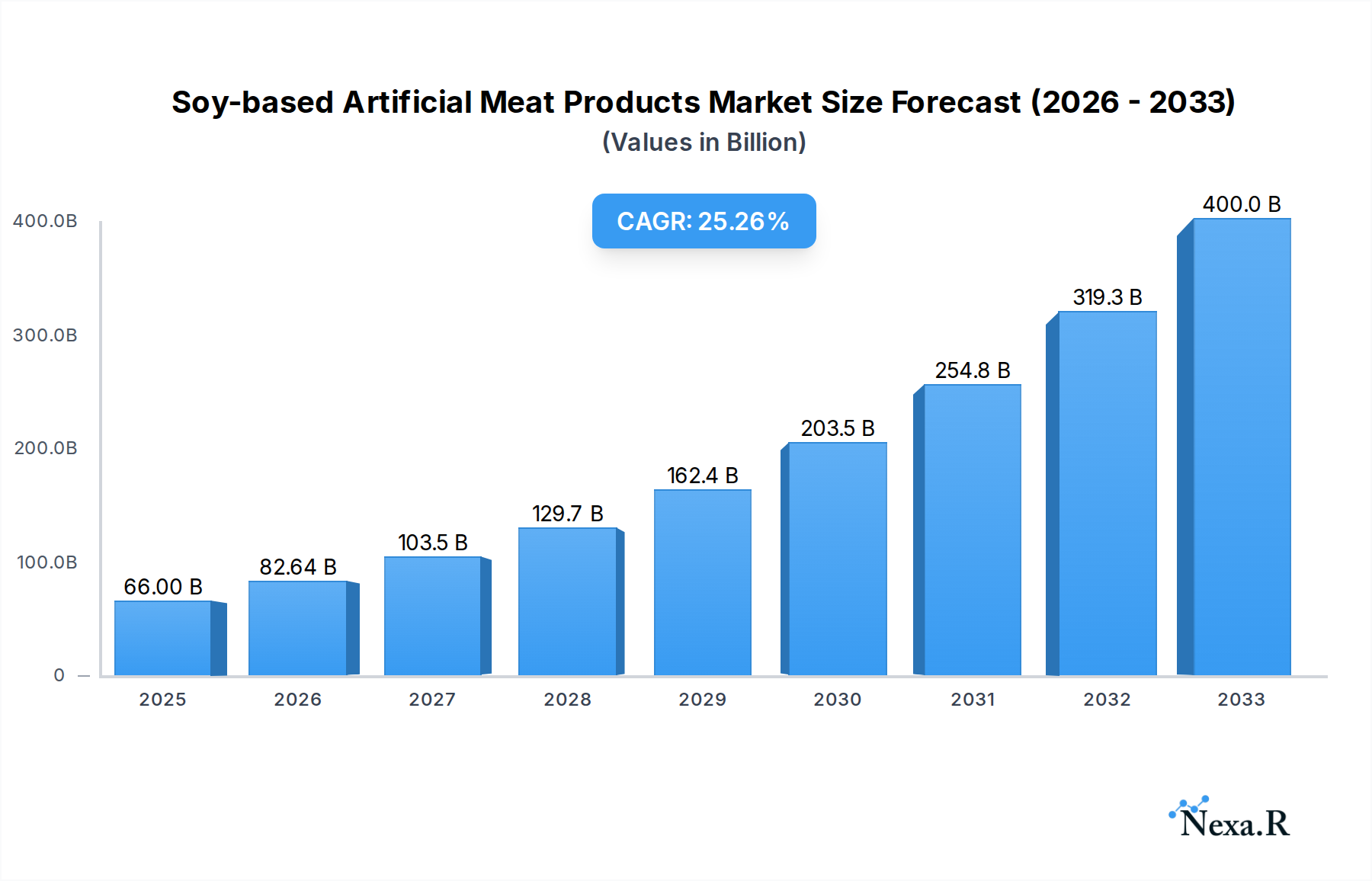

The Soy-based Artificial Meat Products market is poised for remarkable expansion, with a projected market size of $66 billion in 2025. This robust growth is underpinned by an impressive Compound Annual Growth Rate (CAGR) of 25.1%, indicating a dynamic and rapidly evolving sector. The primary drivers fueling this surge include increasing consumer awareness and concern regarding the environmental impact of traditional meat production, coupled with a growing demand for healthier and ethically sourced protein alternatives. The "flexitarian" and vegan diets are gaining significant traction globally, further augmenting the demand for soy-based meat substitutes. Innovations in taste, texture, and nutritional profiles are making these products increasingly indistinguishable from their conventional counterparts, thereby appealing to a broader consumer base. The Food Service and Retail segments are expected to be key beneficiaries, as restaurants and supermarkets increasingly feature these plant-based options to cater to evolving consumer preferences.

Soy-based Artificial Meat Products Market Size (In Billion)

The market is also shaped by several key trends, including the rise of advanced processing technologies that enhance the sensory appeal of soy-based meats, and the strategic collaborations and partnerships between established food giants and innovative startups. Furthermore, the growing emphasis on clean-label products and the demand for non-GMO ingredients are influencing product development and market strategies. However, certain restraints such as the higher initial cost of production compared to traditional meat, and occasional consumer skepticism regarding taste and texture, could pose challenges. Despite these hurdles, the sustained innovation, growing consumer acceptance, and supportive regulatory environments in various regions are expected to propel the Soy-based Artificial Meat Products market to new heights, solidifying its position as a significant player in the global food industry.

Soy-based Artificial Meat Products Company Market Share

Comprehensive Report on Soy-based Artificial Meat Products: Market Dynamics, Growth, and Future Outlook (2019–2033)

This in-depth market intelligence report offers a definitive analysis of the global soy-based artificial meat products market. Spanning from 2019 to 2033, with a base and estimated year of 2025, this research provides critical insights into market size, growth trajectories, key players, and future potential. The report leverages high-traffic keywords such as "plant-based meat," "alternative protein," "soy protein," "meat alternatives," and "vegan meat," ensuring maximum search engine visibility for industry professionals and investors. We dissect the parent and child market structures, offering a granular understanding of market segmentation and regional dominance, with all quantitative data presented in billion units.

Soy-based Artificial Meat Products Market Dynamics & Structure

The global soy-based artificial meat products market is characterized by a dynamic interplay of technological innovation, evolving consumer preferences, and a robust regulatory landscape. Market concentration is moderate, with established players like Beyond Meat and Impossible Foods leading the charge, alongside a growing cohort of regional and emerging companies such as Turtle Island Foods, Maple Leaf, Yves Veggie Cuisine, Nestle, Kellogg's, Omnipork, PFI, Qishan Foods, Hongchang Food, Sulian Food, Fuzhou Sutianxia, Zhen Meat, Vesta food lab, and Starfield, and Segments. Technological innovation drivers are primarily focused on improving taste, texture, and nutritional profiles to achieve parity with conventional meat. Regulatory frameworks are increasingly supportive, with many regions actively promoting plant-based diets for environmental and health reasons. Competitive product substitutes are diverse, ranging from other plant-based proteins like pea and fava bean to cultured meat technologies. End-user demographics are expanding beyond traditional vegan and vegetarian segments to include flexitarians and health-conscious consumers. Mergers and acquisitions (M&A) trends are observed as larger food conglomerates seek to integrate innovative plant-based offerings into their portfolios, indicating consolidation and strategic partnerships.

- Market Concentration: Moderate, with a mix of large multinational corporations and specialized plant-based food companies.

- Technological Innovation Drivers: Enhancing palatability, mimicking animal protein texture, improving protein digestibility, and reducing processing.

- Regulatory Frameworks: Evolving to support food labeling accuracy, promote sustainability claims, and potentially establish novel food regulations.

- Competitive Product Substitutes: Pea protein-based meat, fungal protein (mycoprotein), insect protein, and emerging cultured meat technologies.

- End-User Demographics: Growing adoption by flexitarians, millennials, and Gen Z consumers driven by health, environmental, and ethical concerns.

- M&A Trends: Increased acquisition of smaller, innovative plant-based startups by major food and beverage companies to expand product lines and market reach.

Soy-based Artificial Meat Products Growth Trends & Insights

The soy-based artificial meat products market has witnessed substantial growth and is projected to continue its upward trajectory, driven by a confluence of factors that are reshaping global food consumption patterns. The market size has evolved significantly from its nascent stages, propelled by increasing consumer awareness of the environmental impact of traditional animal agriculture and a growing demand for healthier dietary options. Adoption rates for plant-based meat alternatives, particularly those leveraging the versatility and affordability of soy protein, have surged. Technological disruptions have played a pivotal role, with ongoing advancements in processing techniques, ingredient formulation, and flavor replication enabling soy-based products to achieve a remarkable resemblance to conventional meat in terms of taste, texture, and appearance. These innovations have been instrumental in overcoming initial consumer skepticism and broadening the appeal of plant-based meat beyond niche markets.

Consumer behavior shifts are perhaps the most significant catalyst. A growing segment of consumers, often referred to as flexitarians, are actively reducing their meat consumption without entirely eliminating it, making plant-based alternatives an attractive and accessible choice. This shift is fueled by a multifaceted understanding of sustainability, with consumers increasingly connecting their food choices to climate change, resource depletion, and animal welfare. Furthermore, the perceived health benefits associated with plant-based diets, such as lower saturated fat and cholesterol content, are resonating with a broader audience seeking to improve their well-being. The convenience of these products, readily available in both retail and food service channels, further accelerates their integration into daily diets.

The market penetration of soy-based artificial meat products is steadily increasing across diverse demographics and geographic regions. As investment in research and development continues, product portfolios are expanding to include a wider array of meat analogues, catering to various culinary preferences and cooking methods. This diversification is crucial for sustained market growth, ensuring that soy-based options can effectively compete with and even surpass the appeal of traditional meat in numerous applications. The CAGR for this market is projected to remain robust, reflecting the ongoing transition towards more sustainable and health-conscious food systems. The estimated market size for 2025 is projected to be $XX billion, with a projected CAGR of XX% from 2025 to 2033, reaching an estimated $XX billion by the end of the forecast period. Historical data from 2019–2024 indicates a strong foundational growth phase, setting the stage for accelerated expansion.

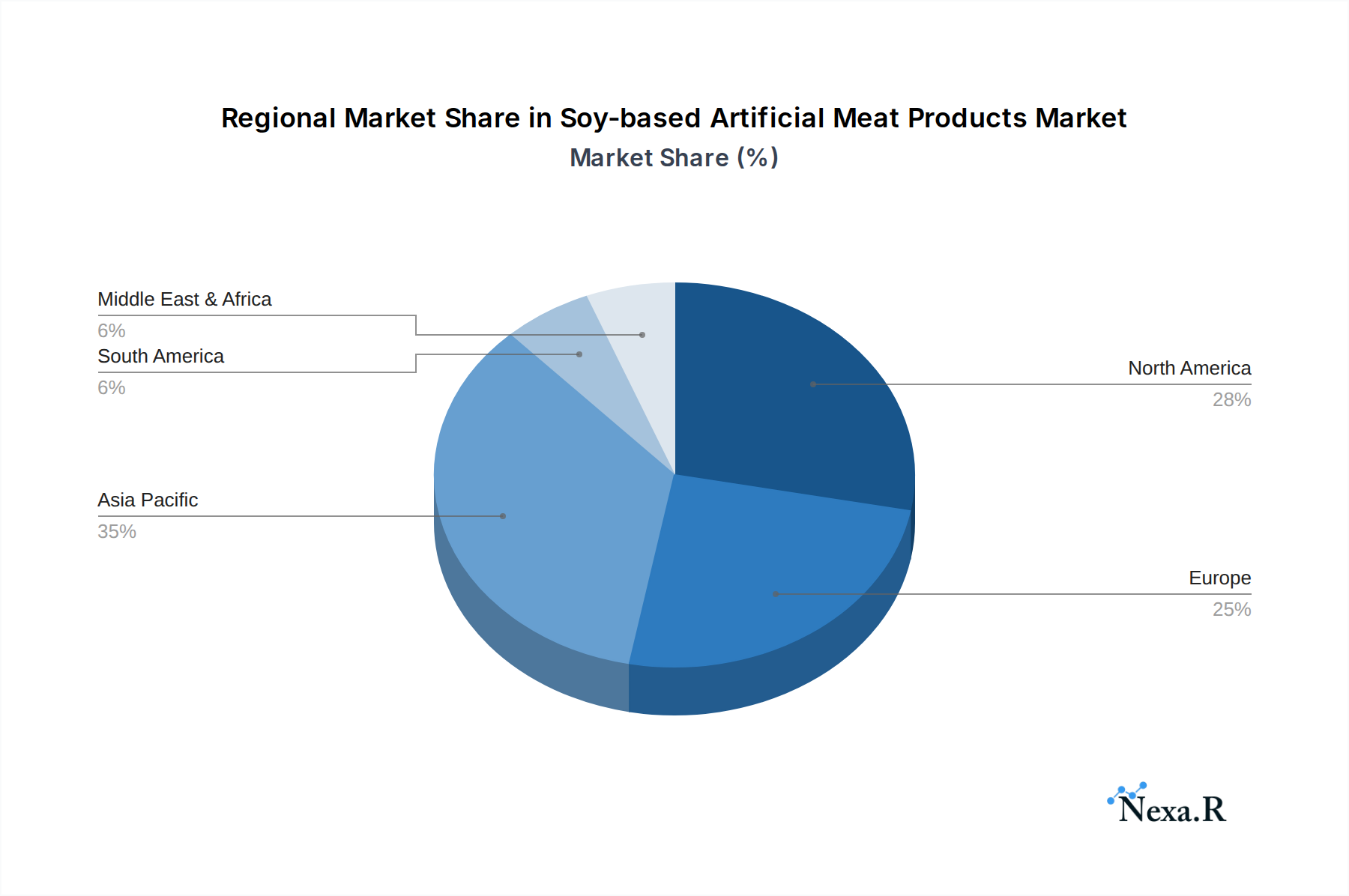

Dominant Regions, Countries, or Segments in Soy-based Artificial Meat Products

The dominance in the soy-based artificial meat products market is a multifaceted phenomenon, influenced by a complex interplay of economic policies, consumer preferences, and infrastructural development. Among the key segments, Retail has emerged as a primary driver of market growth, showcasing a significant market share and robust expansion potential. This dominance is propelled by increasing consumer accessibility, the proliferation of dedicated plant-based aisles in supermarkets, and the growing availability of a wide array of soy-based products for home consumption. The convenience of purchasing these alternatives alongside other grocery items makes the retail channel a crucial touchpoint for both established brands and emerging players.

In terms of geographical influence, North America stands out as a leading region, driven by a well-established consumer base for plant-based diets and proactive market development. The presence of key industry pioneers like Beyond Meat and Impossible Foods, coupled with significant investment in research and development, has cemented North America's position. Furthermore, supportive government initiatives promoting sustainable food systems and a generally health-conscious populace contribute to its leading status. Within North America, the United States, with its large consumer market and advanced retail infrastructure, plays a pivotal role.

Analyzing the Application segment, the Retail channel is projected to hold the largest market share, estimated at $XX billion in 2025, growing at a CAGR of XX% from 2025 to 2033. This growth is attributed to the expanding product variety, increasing supermarket penetration, and the rising popularity of plant-based diets among household consumers. The Food Service segment also presents significant growth opportunities, with an estimated market size of $XX billion in 2025, expected to grow at a CAGR of XX%. This is driven by restaurant chains and food vendors incorporating plant-based options to cater to diverse customer preferences. The Other application segment, encompassing institutional catering and food manufacturing, is anticipated to reach $XX billion in 2025, with a CAGR of XX%.

Within the Types of products, Meat Products (encompassing burgers, sausages, nuggets, and grounds) are expected to dominate, holding an estimated market share of $XX billion in 2025 and a projected CAGR of XX% through 2033. This dominance is fueled by the direct replacement appeal of these products for traditional meat consumption. The broader Meat category, which can include processed items and ingredients derived from soy, is also a significant contributor.

- Dominant Segment (Application): Retail, driven by accessibility and consumer demand for home consumption.

- Dominant Segment (Types): Meat Products (burgers, sausages, nuggets, grounds), offering direct substitutes for traditional meat.

- Leading Region: North America, characterized by early adoption, significant R&D investment, and supportive market trends.

- Key Countries: United States, Canada, and increasingly, European nations like Germany and the UK.

- Drivers of Retail Dominance: Supermarket penetration, product variety, convenience, and growing consumer adoption of plant-based diets for various reasons.

- Drivers of North American Leadership: Pioneer companies, strong venture capital funding, and a culturally receptive consumer base for alternative proteins.

- Growth Potential in Food Service: Increasing inclusion of plant-based options by major restaurant chains and fast-food providers.

Soy-based Artificial Meat Products Product Landscape

The product landscape for soy-based artificial meat products is characterized by continuous innovation aimed at replicating the sensory attributes and nutritional value of conventional meat. Manufacturers are leveraging advanced processing techniques, including extrusion and texturization, to achieve fibrous textures that closely mimic animal muscle. Key product types include burgers, sausages, grounds, nuggets, and deli slices, with ongoing efforts to expand into more complex meat analogues like steaks and chicken breasts. Performance metrics are increasingly being benchmarked against traditional meat, focusing on protein content, flavor profiles, juiciness, and cooking behavior. Unique selling propositions often revolve around health benefits, such as lower saturated fat and cholesterol, alongside environmental sustainability claims. Technological advancements in flavor encapsulation and binding agents are crucial in achieving authentic meat-like experiences.

Key Drivers, Barriers & Challenges in Soy-based Artificial Meat Products

The growth of the soy-based artificial meat products market is propelled by several key drivers:

- Growing Consumer Demand for Healthier Options: Increasing awareness of the health benefits associated with reduced meat consumption, such as lower cholesterol and saturated fat intake.

- Environmental Sustainability Concerns: Consumers are actively seeking food choices that minimize their environmental footprint, driving demand for plant-based alternatives due to the lower resource intensity of soy cultivation compared to livestock farming.

- Ethical Considerations: Rising concerns about animal welfare in conventional farming practices are motivating consumers to opt for cruelty-free protein sources.

- Technological Advancements: Continuous innovation in texture replication, flavor profiles, and nutritional fortification is making soy-based products more appealing and comparable to conventional meat.

- Expanding Retail Availability: Increased presence and variety of soy-based meat alternatives in mainstream supermarkets and grocery stores.

However, the market faces significant barriers and challenges:

- Price Parity: Soy-based artificial meats can still be more expensive than conventional meat, limiting widespread adoption, particularly in price-sensitive markets. The cost of production and ingredient sourcing contributes to this challenge.

- Taste and Texture Perceptions: While improving, achieving a perfect replication of traditional meat's taste and texture remains a challenge for some products, leading to consumer preference shifts.

- Supply Chain Complexities: Ensuring a consistent and high-quality supply of specialized soy ingredients and managing the intricacies of plant-based food manufacturing can be challenging.

- Regulatory Hurdles and Labeling Concerns: Navigating evolving regulations regarding product naming, ingredient disclosure, and health claims can create uncertainty for manufacturers.

- Consumer Education and Misconceptions: Addressing consumer skepticism, educating them about the benefits and production of plant-based meats, and dispelling myths are ongoing efforts.

Emerging Opportunities in Soy-based Artificial Meat Products

Emerging opportunities in the soy-based artificial meat products sector lie in expanding product innovation, tapping into underdeveloped markets, and catering to evolving consumer preferences. The development of whole-cut analogues, such as plant-based steaks and chicken breasts, represents a significant area for growth, offering a more premium and versatile alternative. Geographic expansion into emerging economies in Asia and Latin America, where meat consumption is high and there's a growing interest in healthier and more sustainable options, presents a substantial untapped market. Furthermore, the integration of soy-based proteins into a wider range of convenience foods and ready-to-eat meals can attract time-pressed consumers. Innovations in clean label formulations, reducing the number of artificial ingredients, and enhancing the nutritional profile with added vitamins and minerals also represent key opportunities.

Growth Accelerators in the Soy-based Artificial Meat Products Industry

Several catalysts are accelerating the growth of the soy-based artificial meat products industry. Technological breakthroughs in ingredient functionality, particularly in creating more authentic meat-like textures and flavors without relying on highly processed components, are game-changers. Strategic partnerships between established food companies and innovative plant-based startups are crucial for scaling production, distribution, and marketing efforts. Market expansion strategies, including penetration into new geographic regions and diversification of product offerings beyond traditional patties and sausages, are key to sustained growth. Increased investment in research and development, coupled with supportive government policies and public awareness campaigns promoting sustainable diets, further fuels this expansion.

Key Players Shaping the Soy-based Artificial Meat Products Market

- Beyond Meat

- Impossible Foods

- Turtle Island Foods

- Maple Leaf

- Yves Veggie Cuisine

- Nestle

- Kellogg's

- Omnipork

- PFI

- Qishan Foods

- Hongchang Food

- Sulian Food

- Fuzhou Sutianxia

- Zhen Meat

- Vesta food lab

- Starfield

Notable Milestones in Soy-based Artificial Meat Products Sector

- 2019: Beyond Meat's highly successful IPO, marking a significant milestone for the plant-based meat industry and attracting substantial investor attention.

- 2020: Impossible Foods expands its retail presence, making its plant-based meat products more accessible to consumers beyond foodservice.

- 2021: Nestlé launches its plant-based "Awesome Burger" in various international markets, signaling the growing commitment of traditional food giants.

- 2022: Increased regulatory clarity and labeling initiatives emerge in key markets, providing clearer guidelines for plant-based food products.

- 2023: Significant advancements in texture replication technology reported, enabling the creation of more sophisticated whole-cut plant-based meat analogues.

- 2024: Growing number of food service providers, including fast-food chains and casual dining restaurants, expand their plant-based menu options featuring soy-based alternatives.

In-Depth Soy-based Artificial Meat Products Market Outlook

The future outlook for the soy-based artificial meat products market is exceptionally promising, driven by persistent demand for sustainable and health-conscious food choices. Growth accelerators, including continuous technological innovation, strategic collaborations, and aggressive market expansion strategies, will continue to shape the industry landscape. The projected increase in investment in plant-based food research and development, coupled with favorable government policies promoting alternative proteins, will further bolster market expansion. Strategic opportunities lie in capitalizing on the growing flexitarian movement, developing a wider range of premium and whole-cut plant-based meat analogues, and penetrating underserved emerging markets. The market is poised for significant growth, offering substantial returns for stakeholders invested in the evolving future of food.

Soy-based Artificial Meat Products Segmentation

-

1. Application

- 1.1. Food Service

- 1.2. Retail

- 1.3. Other

-

2. Types

- 2.1. Meat Products

- 2.2. Meat

Soy-based Artificial Meat Products Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Soy-based Artificial Meat Products Regional Market Share

Geographic Coverage of Soy-based Artificial Meat Products

Soy-based Artificial Meat Products REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 25.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Soy-based Artificial Meat Products Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food Service

- 5.1.2. Retail

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Meat Products

- 5.2.2. Meat

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Soy-based Artificial Meat Products Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food Service

- 6.1.2. Retail

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Meat Products

- 6.2.2. Meat

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Soy-based Artificial Meat Products Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food Service

- 7.1.2. Retail

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Meat Products

- 7.2.2. Meat

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Soy-based Artificial Meat Products Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food Service

- 8.1.2. Retail

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Meat Products

- 8.2.2. Meat

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Soy-based Artificial Meat Products Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food Service

- 9.1.2. Retail

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Meat Products

- 9.2.2. Meat

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Soy-based Artificial Meat Products Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food Service

- 10.1.2. Retail

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Meat Products

- 10.2.2. Meat

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Beyond Meat

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Impossible Foods

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Turtle Island Foods

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Maple Leaf

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Yves Veggie Cuisine

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Nestle

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Kellogg's

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Omnipork

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 PFI

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Qishan Foods

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Hongchang Food

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Sulian Food

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Fuzhou Sutianxia

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Zhen Meat

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Vesta food lab

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Starfield

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Beyond Meat

List of Figures

- Figure 1: Global Soy-based Artificial Meat Products Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Soy-based Artificial Meat Products Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Soy-based Artificial Meat Products Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Soy-based Artificial Meat Products Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Soy-based Artificial Meat Products Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Soy-based Artificial Meat Products Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Soy-based Artificial Meat Products Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Soy-based Artificial Meat Products Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Soy-based Artificial Meat Products Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Soy-based Artificial Meat Products Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Soy-based Artificial Meat Products Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Soy-based Artificial Meat Products Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Soy-based Artificial Meat Products Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Soy-based Artificial Meat Products Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Soy-based Artificial Meat Products Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Soy-based Artificial Meat Products Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Soy-based Artificial Meat Products Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Soy-based Artificial Meat Products Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Soy-based Artificial Meat Products Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Soy-based Artificial Meat Products Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Soy-based Artificial Meat Products Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Soy-based Artificial Meat Products Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Soy-based Artificial Meat Products Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Soy-based Artificial Meat Products Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Soy-based Artificial Meat Products Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Soy-based Artificial Meat Products Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Soy-based Artificial Meat Products Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Soy-based Artificial Meat Products Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Soy-based Artificial Meat Products Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Soy-based Artificial Meat Products Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Soy-based Artificial Meat Products Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Soy-based Artificial Meat Products Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Soy-based Artificial Meat Products Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Soy-based Artificial Meat Products?

The projected CAGR is approximately 25.1%.

2. Which companies are prominent players in the Soy-based Artificial Meat Products?

Key companies in the market include Beyond Meat, Impossible Foods, Turtle Island Foods, Maple Leaf, Yves Veggie Cuisine, Nestle, Kellogg's, Omnipork, PFI, Qishan Foods, Hongchang Food, Sulian Food, Fuzhou Sutianxia, Zhen Meat, Vesta food lab, Starfield.

3. What are the main segments of the Soy-based Artificial Meat Products?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Soy-based Artificial Meat Products," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Soy-based Artificial Meat Products report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Soy-based Artificial Meat Products?

To stay informed about further developments, trends, and reports in the Soy-based Artificial Meat Products, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence