Key Insights

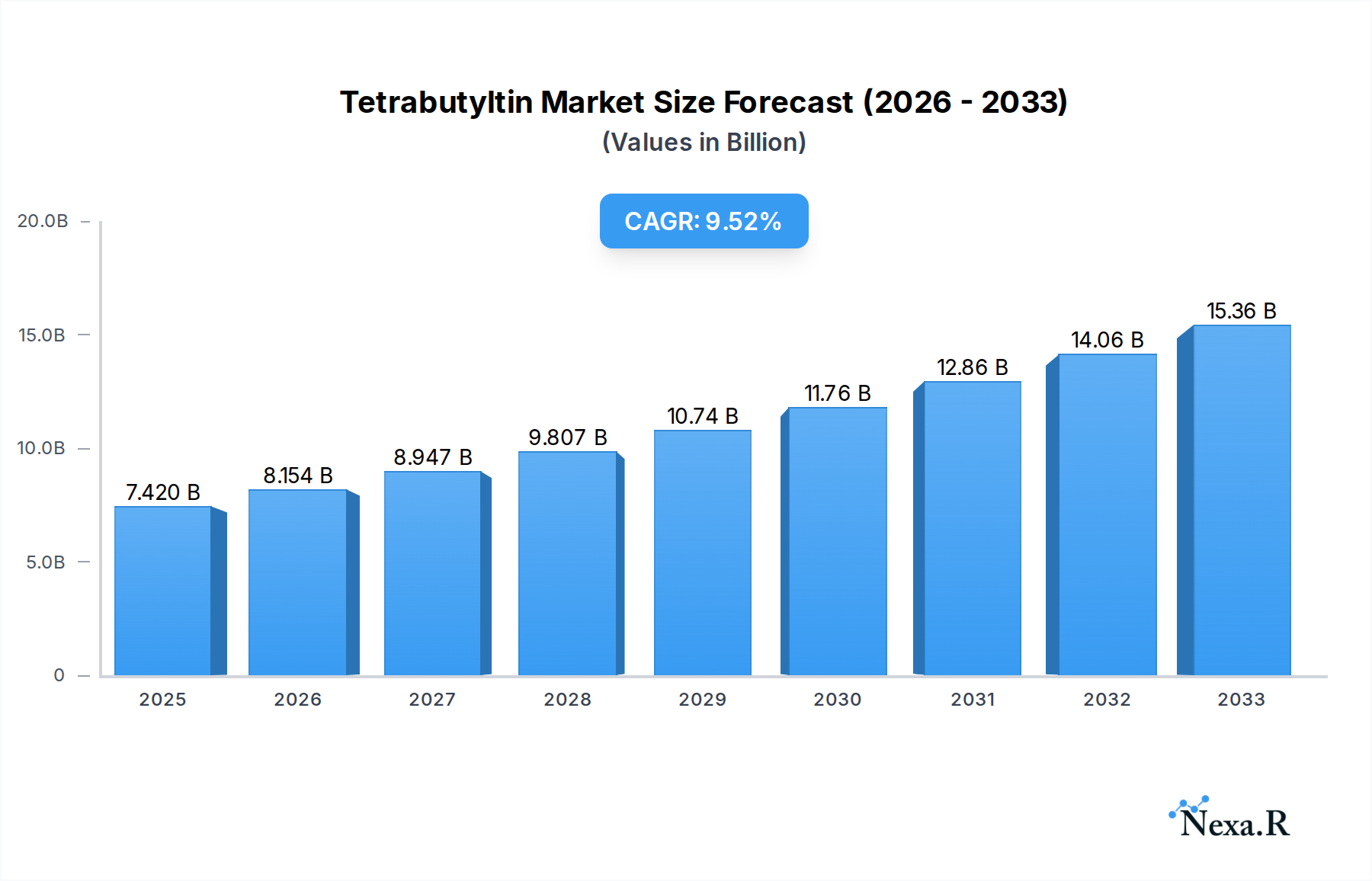

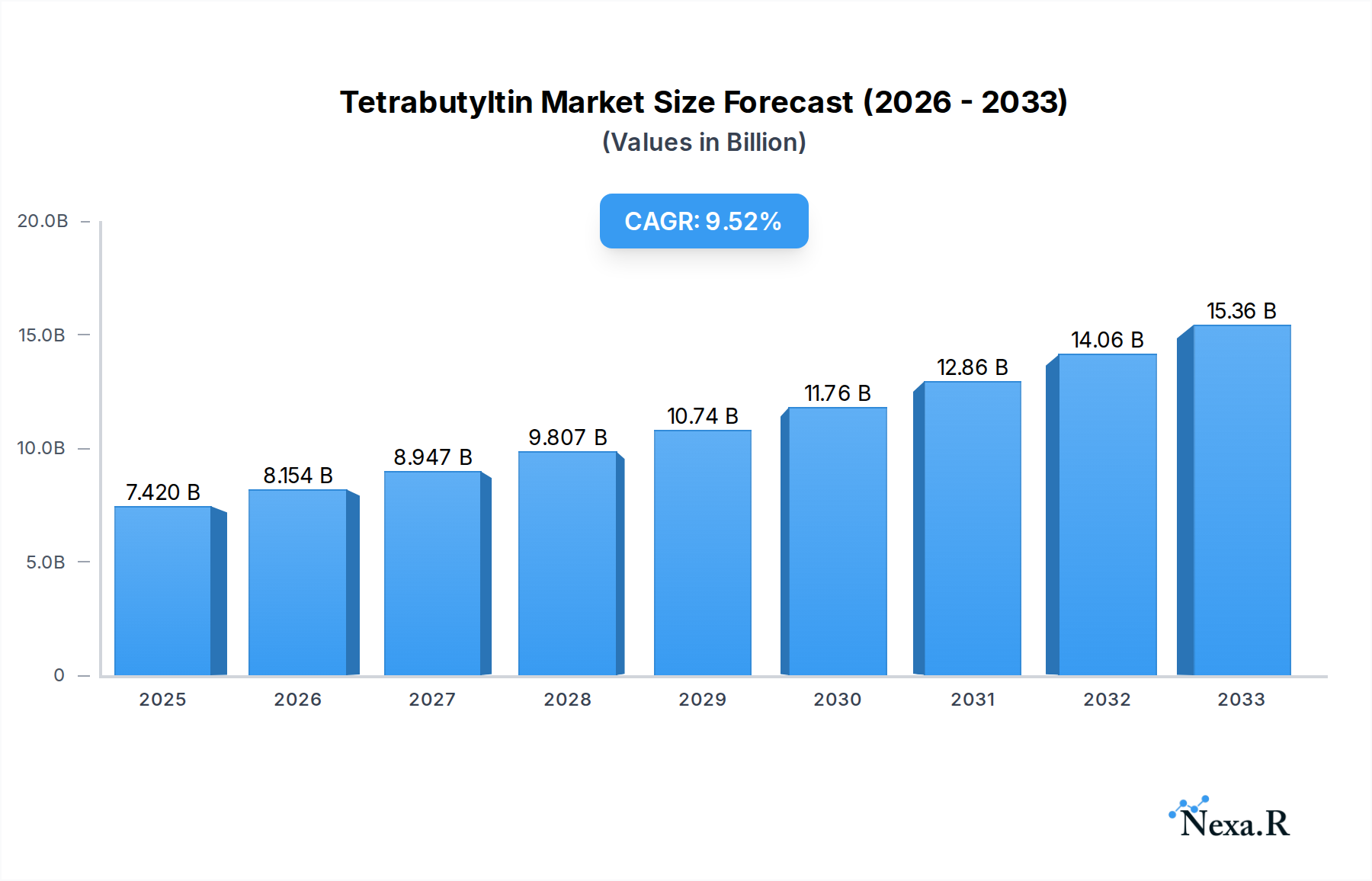

The Tetrabutyltin market is poised for robust expansion, driven by its critical applications across diverse industrial sectors. With a projected **market size of *$7.42 billion* in 2025**, the sector is expected to witness a significant Compound Annual Growth Rate (CAGR) of *9.76%* over the forecast period. This growth is primarily fueled by the increasing demand for Tetrabutyltin in the chemical industry as a catalyst and intermediate in various synthesis processes. Furthermore, its indispensable role in the petroleum sector for enhancing fuel additives and in the coatings industry for anti-fouling paints is a major growth stimulant. The rising global industrialization, particularly in emerging economies, is also contributing to the upward trajectory of this market. Technological advancements leading to improved production efficiencies and higher purity grades (Purity ≥95%) are further bolstering market confidence and adoption.

Tetrabutyltin Market Size (In Billion)

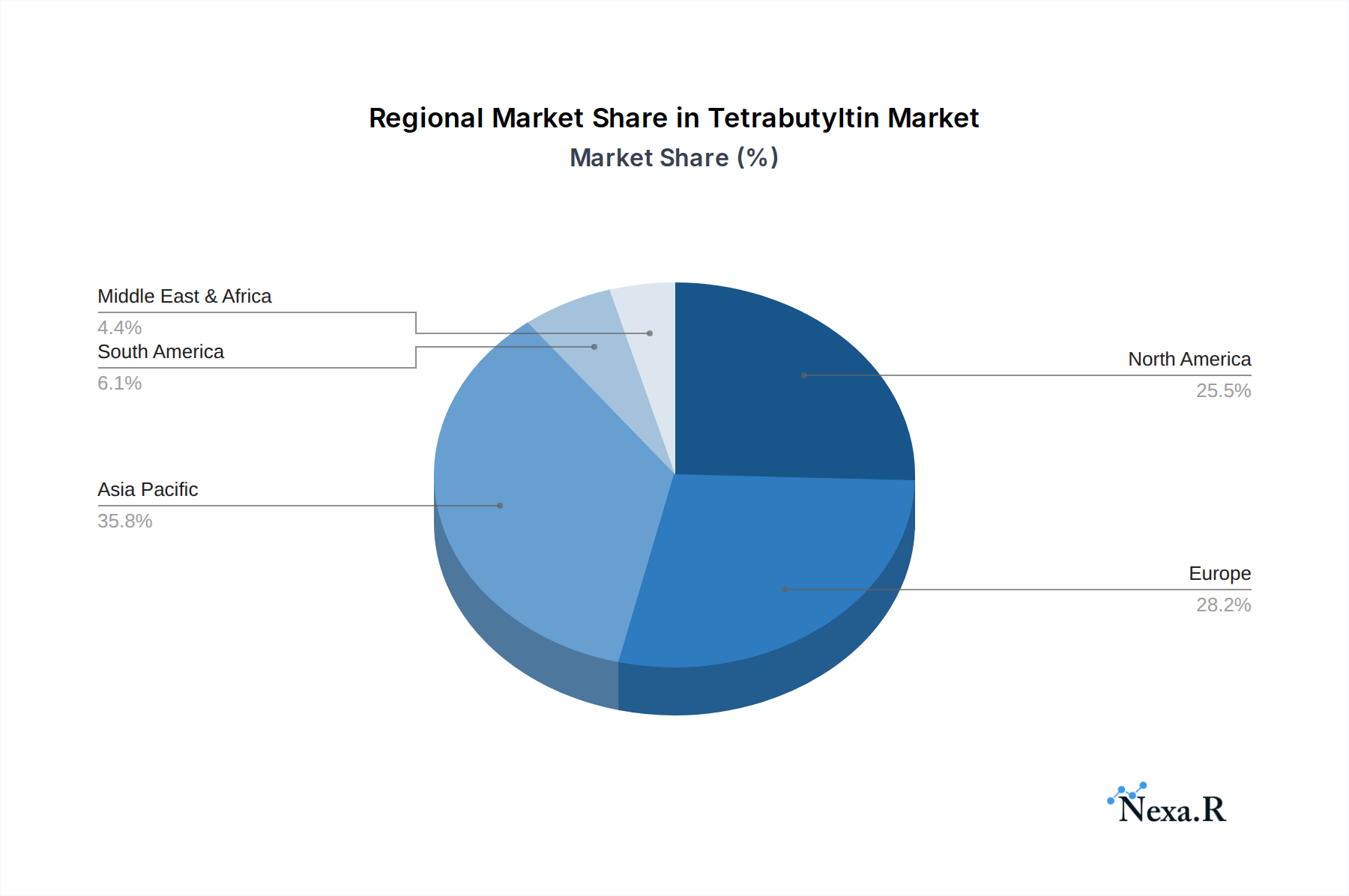

Despite the promising outlook, the Tetrabutyltin market faces certain constraints. Stringent environmental regulations concerning the handling and disposal of organotin compounds can pose a challenge, necessitating significant investment in compliance and sustainable practices. Moreover, the development of alternative, more environmentally benign compounds in certain applications could temper growth in specific segments. However, the inherent performance advantages and established utility of Tetrabutyltin in many core applications are expected to outweigh these restraints. The market is segmented by purity, with a notable shift towards higher purity grades (Purity ≥95%) due to enhanced performance requirements in advanced applications. Geographically, Asia Pacific, led by China and India, is anticipated to be a key growth engine, supported by its burgeoning manufacturing base and increasing R&D investments.

Tetrabutyltin Company Market Share

Tetrabutyltin Market Dynamics & Structure

The global Tetrabutyltin market is characterized by a moderate level of concentration, with key players like Gelest, Ereztech, BNT Chemicals, Azeocryst Organic, Yunnan Tin Chemical, Hangzhou Right Chemical, and Nantong Advance Chemicals holding significant sway. Technological innovation is primarily driven by the demand for higher purity grades and novel applications in specialized chemical synthesis. Regulatory frameworks, particularly concerning environmental impact and handling of organotin compounds, play a crucial role in shaping market entry and product development. Competitive product substitutes, though limited for highly specialized applications, exist in areas where less toxic alternatives are being explored, prompting continuous innovation from incumbent manufacturers. End-user demographics are predominantly B2B, encompassing research institutions, chemical manufacturers, and end-product formulators. Mergers and acquisitions (M&A) activity has been moderate, with strategic acquisitions aimed at expanding product portfolios and geographical reach. For instance, in the historical period (2019-2024), there were an estimated 3-5 significant M&A deals valued at approximately \$50-75 million in total. Barriers to innovation include the high cost of R&D for novel organotin compounds and stringent safety protocols required for their production.

- Market Concentration: Moderate, with a few key players dominating.

- Technological Drivers: Demand for high-purity grades and novel synthesis pathways.

- Regulatory Impact: Significant influence on production, handling, and environmental compliance.

- Competitive Landscape: Limited direct substitutes for niche applications, but evolving with safer alternatives.

- End-User Base: Primarily industrial and research-focused B2B clients.

- M&A Trends: Strategic acquisitions for portfolio expansion and market access.

Tetrabutyltin Growth Trends & Insights

The global Tetrabutyltin market is projected to witness robust growth driven by its indispensable role as a precursor and catalyst in various chemical processes. The market size, which was approximately \$1.2 billion in the base year 2025, is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 6.5% during the forecast period of 2025–2033. This expansion is underpinned by increasing adoption rates in the chemical and petroleum industries, where Tetrabutyltin is crucial for the synthesis of advanced materials and efficient refining processes. Technological disruptions, while not revolutionary, are focused on improving synthesis efficiency and reducing byproducts, leading to more cost-effective and environmentally conscious production methods. Consumer behavior shifts are indirectly influencing the market, with a growing demand for end-products that rely on Tetrabutyltin's unique chemical properties, such as specialized polymers and catalysts for pharmaceuticals. The market penetration of high-purity Tetrabutyltin (≥95%) is expected to rise as sophisticated applications become more prevalent.

The market evolution is also shaped by global economic policies and industrial expansion in emerging economies. For example, increased investment in petrochemical infrastructure in the Asia-Pacific region is directly correlating with a higher demand for chemical intermediates like Tetrabutyltin. Furthermore, the ongoing quest for enhanced performance in coatings and the development of more effective, yet environmentally sound, pesticide formulations are creating new avenues for Tetrabutyltin utilization. The historical data from 2019–2024 indicates a steady upward trajectory, with a CAGR of approximately 5.8% during that period, setting a strong foundation for future growth. The forecast period is expected to see this growth accelerate due to advancements in application research and increased industrialization globally.

Adoption rates are also influenced by the cost-effectiveness of Tetrabutyltin compared to potential alternatives, especially in large-scale industrial applications. Research into greener synthetic routes and improved recycling of organotin compounds will further bolster market adoption and sustainability. The intrinsic chemical versatility of Tetrabutyltin ensures its continued relevance in a dynamic industrial landscape, where specialized chemicals are paramount for innovation and competitive advantage. The estimated market size in 2033 is projected to reach approximately \$2.0 billion.

Dominant Regions, Countries, or Segments in Tetrabutyltin

The Chemical application segment, particularly within the Purity ≥95% sub-segment, stands as the dominant force driving growth in the global Tetrabutyltin market. This dominance is primarily concentrated in the Asia-Pacific region, with China emerging as a leading country. The robust growth in this segment is propelled by several key drivers, including substantial government investments in chemical manufacturing infrastructure, favorable economic policies promoting industrial output, and a rapidly expanding downstream chemical industry. China's extensive chemical production capabilities, coupled with its position as a global manufacturing hub for a wide array of products requiring specialized chemical intermediates, directly translates into a high demand for Tetrabutyltin.

The market share within the chemical application segment is estimated to be around 45-50% of the overall Tetrabutyltin market. The purity ≥95% sub-segment accounts for a significant portion of this, driven by its use in high-value synthesis, catalysis, and the production of advanced materials where precise chemical reactions are critical. Countries in Asia-Pacific benefit from established supply chains and a large pool of skilled labor, further enhancing their competitive edge in the production and consumption of Tetrabutyltin.

- Dominant Application Segment: Chemical (Market Share: ~45-50%)

- Key Drivers: Extensive use in organic synthesis, catalyst production, and polymer manufacturing.

- Growth Potential: Continued expansion of the global chemical industry, particularly in Asia.

- Dominant Type Segment: Purity ≥95%

- Key Drivers: Demand for high-purity reagents in pharmaceuticals, electronics, and advanced materials.

- Growth Potential: Increasing sophistication of chemical synthesis processes and stricter quality requirements.

- Dominant Region: Asia-Pacific

- Key Drivers: Strong manufacturing base, government support for chemical industries, and growing domestic demand.

- Market Share Contribution: Approximately 50-55% of global consumption.

- Leading Country: China

- Key Drivers: Massive chemical production capacity, robust R&D investments, and extensive export market.

- Infrastructure: Advanced chemical parks and logistics networks supporting large-scale operations.

The Petroleum segment, while important, represents a smaller but growing share, driven by its use in certain fuel additives and refining catalysts. The Coatings and Pesticides segments are emerging markets, showing steady growth as new formulations and applications are developed. However, their current market contribution is considerably less than the chemical sector. The competitive advantage of the Asia-Pacific region, especially China, in terms of production scale, cost-effectiveness, and access to raw materials, solidifies its leadership position for the foreseeable future.

Tetrabutyltin Product Landscape

Tetrabutyltin is distinguished by its organometallic structure, featuring a tin atom bonded to four butyl groups. This unique composition imparts excellent solubility in organic solvents and acts as a versatile precursor and catalyst in numerous chemical transformations. Product innovations focus on enhancing its reactivity, selectivity, and stability for specific applications, such as in the Stille coupling reaction for carbon-carbon bond formation, or as a key component in the synthesis of organotin stabilizers for PVC. Manufacturers are increasingly offering ultra-high purity grades (e.g., >99%) to meet the stringent demands of pharmaceutical intermediates and electronic materials manufacturing. Performance metrics are evaluated based on catalytic efficiency, product yield, and minimized byproduct formation. The development of safer handling protocols and more environmentally benign production methods are also key areas of product advancement.

Key Drivers, Barriers & Challenges in Tetrabutyltin

Key Drivers:

- Expanding Chemical Synthesis: The fundamental role of Tetrabutyltin as a catalyst and reagent in organic synthesis, particularly for complex molecule construction in pharmaceuticals and fine chemicals, is a primary growth driver.

- Advancements in Material Science: Its utility in creating specialized polymers, tin-based catalysts, and precursors for advanced materials fuels demand across various industrial sectors.

- Growing Demand from Emerging Economies: Rapid industrialization and increasing investment in chemical manufacturing in regions like Asia-Pacific directly translate to higher consumption of Tetrabutyltin.

- Technological Innovations: Development of more efficient synthetic routes and higher purity grades makes Tetrabutyltin more attractive for demanding applications.

Barriers & Challenges:

- Environmental Regulations: Strict regulations concerning the production, use, and disposal of organotin compounds due to their potential environmental impact pose a significant challenge, necessitating higher compliance costs.

- Toxicity Concerns: The inherent toxicity of organotin compounds requires stringent safety measures during handling, storage, and transportation, increasing operational expenses.

- Availability of Substitutes: While direct substitutes are limited for highly specialized applications, research into less toxic or bio-based alternatives could impact future market share in certain segments.

- Supply Chain Volatility: Dependence on raw material availability and price fluctuations, coupled with geopolitical factors, can lead to supply chain disruptions and cost instability.

Emerging Opportunities in Tetrabutyltin

Emerging opportunities for Tetrabutyltin lie in the development of novel, greener synthetic pathways for its production, which could mitigate environmental concerns and potentially lower costs. Furthermore, its application in emerging fields like advanced electronics, particularly in the development of specialized semiconductors and conductive materials, presents a significant growth avenue. The increasing focus on sustainable chemistry is also creating opportunities for research into bio-degradable organotin compounds or closed-loop recycling processes for existing Tetrabutyltin applications. Untapped markets in niche chemical applications and a growing demand for high-performance catalysts in specialized industrial processes also represent fertile ground for market expansion.

Growth Accelerators in the Tetrabutyltin Industry

Technological breakthroughs in catalyst design and synthesis methodologies are significant growth accelerators. The ongoing refinement of the Stille coupling reaction and its expanding applications in drug discovery and complex organic molecule synthesis are key drivers. Strategic partnerships between chemical manufacturers and end-users, focusing on co-development of tailored Tetrabutyltin formulations for specific industrial needs, will further boost market penetration. Market expansion strategies, particularly targeting the growing chemical industries in developing nations and capitalizing on the increasing demand for high-purity reagents, are crucial for sustained growth. Investment in R&D for environmentally friendlier production processes will also be a critical accelerator.

Key Players Shaping the Tetrabutyltin Market

- Gelest

- Ereztech

- BNT Chemicals

- Azeocryst Organic

- Yunnan Tin Chemical

- Hangzhou Right Chemical

- Nantong Advance Chemicals

Notable Milestones in Tetrabutyltin Sector

- 2019: Increased focus on stricter environmental regulations for organotin compounds globally, leading to investments in compliance technologies by manufacturers.

- 2020: Enhanced research into greener synthesis methods for Tetrabutyltin, aiming to reduce hazardous byproducts.

- 2021: Rise in demand for high-purity Tetrabutyltin for pharmaceutical intermediate synthesis and advanced electronic materials.

- 2022: Several M&A activities noted, focused on consolidating market share and expanding product portfolios in niche organometallic chemicals.

- 2023: Advancements in catalytic applications of Tetrabutyltin, leading to improved efficiency in various chemical processes.

- 2024: Growing exploration of Tetrabutyltin in new material science applications, including specialized polymers and coatings.

In-Depth Tetrabutyltin Market Outlook

The future outlook for the Tetrabutyltin market is highly optimistic, projected to reach approximately \$2.0 billion by 2033. This growth is underpinned by the compound's indispensable role in advanced chemical synthesis and the increasing global demand for specialized chemicals. Strategic opportunities lie in capitalizing on the expanding pharmaceutical and electronics sectors, where high-purity Tetrabutyltin is essential. Continued investment in R&D for sustainable production methods and the development of novel applications will be critical for sustained market expansion. The Asia-Pacific region, particularly China, is expected to remain the dominant market due to its robust manufacturing capabilities and growing industrial base, presenting significant opportunities for market players focused on this region.

Tetrabutyltin Segmentation

-

1. Application

- 1.1. Chemical

- 1.2. Petroleum

- 1.3. Coatings

- 1.4. Pesticides

- 1.5. Others

-

2. Type

- 2.1. Purity <95%

- 2.2. Purity≥95%

Tetrabutyltin Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Tetrabutyltin Regional Market Share

Geographic Coverage of Tetrabutyltin

Tetrabutyltin REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.76% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Tetrabutyltin Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Chemical

- 5.1.2. Petroleum

- 5.1.3. Coatings

- 5.1.4. Pesticides

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Purity <95%

- 5.2.2. Purity≥95%

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Tetrabutyltin Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Chemical

- 6.1.2. Petroleum

- 6.1.3. Coatings

- 6.1.4. Pesticides

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Purity <95%

- 6.2.2. Purity≥95%

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Tetrabutyltin Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Chemical

- 7.1.2. Petroleum

- 7.1.3. Coatings

- 7.1.4. Pesticides

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Purity <95%

- 7.2.2. Purity≥95%

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Tetrabutyltin Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Chemical

- 8.1.2. Petroleum

- 8.1.3. Coatings

- 8.1.4. Pesticides

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Purity <95%

- 8.2.2. Purity≥95%

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Tetrabutyltin Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Chemical

- 9.1.2. Petroleum

- 9.1.3. Coatings

- 9.1.4. Pesticides

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Purity <95%

- 9.2.2. Purity≥95%

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Tetrabutyltin Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Chemical

- 10.1.2. Petroleum

- 10.1.3. Coatings

- 10.1.4. Pesticides

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Purity <95%

- 10.2.2. Purity≥95%

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Gelest

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Ereztech

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BNT Chemicals

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Azeocryst Organic

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Yunnan Tin Chemical

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hangzhou Right Chemical

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Nantong Advance Chemicals

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.1 Gelest

List of Figures

- Figure 1: Global Tetrabutyltin Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Tetrabutyltin Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Tetrabutyltin Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Tetrabutyltin Volume (K), by Application 2025 & 2033

- Figure 5: North America Tetrabutyltin Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Tetrabutyltin Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Tetrabutyltin Revenue (undefined), by Type 2025 & 2033

- Figure 8: North America Tetrabutyltin Volume (K), by Type 2025 & 2033

- Figure 9: North America Tetrabutyltin Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Tetrabutyltin Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Tetrabutyltin Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Tetrabutyltin Volume (K), by Country 2025 & 2033

- Figure 13: North America Tetrabutyltin Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Tetrabutyltin Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Tetrabutyltin Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Tetrabutyltin Volume (K), by Application 2025 & 2033

- Figure 17: South America Tetrabutyltin Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Tetrabutyltin Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Tetrabutyltin Revenue (undefined), by Type 2025 & 2033

- Figure 20: South America Tetrabutyltin Volume (K), by Type 2025 & 2033

- Figure 21: South America Tetrabutyltin Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Tetrabutyltin Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Tetrabutyltin Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Tetrabutyltin Volume (K), by Country 2025 & 2033

- Figure 25: South America Tetrabutyltin Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Tetrabutyltin Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Tetrabutyltin Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Tetrabutyltin Volume (K), by Application 2025 & 2033

- Figure 29: Europe Tetrabutyltin Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Tetrabutyltin Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Tetrabutyltin Revenue (undefined), by Type 2025 & 2033

- Figure 32: Europe Tetrabutyltin Volume (K), by Type 2025 & 2033

- Figure 33: Europe Tetrabutyltin Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Tetrabutyltin Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Tetrabutyltin Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Tetrabutyltin Volume (K), by Country 2025 & 2033

- Figure 37: Europe Tetrabutyltin Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Tetrabutyltin Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Tetrabutyltin Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Tetrabutyltin Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Tetrabutyltin Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Tetrabutyltin Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Tetrabutyltin Revenue (undefined), by Type 2025 & 2033

- Figure 44: Middle East & Africa Tetrabutyltin Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Tetrabutyltin Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Tetrabutyltin Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Tetrabutyltin Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Tetrabutyltin Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Tetrabutyltin Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Tetrabutyltin Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Tetrabutyltin Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Tetrabutyltin Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Tetrabutyltin Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Tetrabutyltin Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Tetrabutyltin Revenue (undefined), by Type 2025 & 2033

- Figure 56: Asia Pacific Tetrabutyltin Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Tetrabutyltin Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Tetrabutyltin Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Tetrabutyltin Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Tetrabutyltin Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Tetrabutyltin Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Tetrabutyltin Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Tetrabutyltin Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Tetrabutyltin Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Tetrabutyltin Revenue undefined Forecast, by Type 2020 & 2033

- Table 4: Global Tetrabutyltin Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Tetrabutyltin Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Tetrabutyltin Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Tetrabutyltin Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Tetrabutyltin Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Tetrabutyltin Revenue undefined Forecast, by Type 2020 & 2033

- Table 10: Global Tetrabutyltin Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Tetrabutyltin Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Tetrabutyltin Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Tetrabutyltin Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Tetrabutyltin Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Tetrabutyltin Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Global Tetrabutyltin Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Tetrabutyltin Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Tetrabutyltin Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Tetrabutyltin Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Tetrabutyltin Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Tetrabutyltin Revenue undefined Forecast, by Type 2020 & 2033

- Table 34: Global Tetrabutyltin Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Tetrabutyltin Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Tetrabutyltin Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Tetrabutyltin Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Tetrabutyltin Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Tetrabutyltin Revenue undefined Forecast, by Type 2020 & 2033

- Table 58: Global Tetrabutyltin Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Tetrabutyltin Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Tetrabutyltin Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Tetrabutyltin Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Tetrabutyltin Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Tetrabutyltin Revenue undefined Forecast, by Type 2020 & 2033

- Table 76: Global Tetrabutyltin Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Tetrabutyltin Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Tetrabutyltin Volume K Forecast, by Country 2020 & 2033

- Table 79: China Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Tetrabutyltin Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Tetrabutyltin Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Tetrabutyltin?

The projected CAGR is approximately 9.76%.

2. Which companies are prominent players in the Tetrabutyltin?

Key companies in the market include Gelest, Ereztech, BNT Chemicals, Azeocryst Organic, Yunnan Tin Chemical, Hangzhou Right Chemical, Nantong Advance Chemicals.

3. What are the main segments of the Tetrabutyltin?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Tetrabutyltin," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Tetrabutyltin report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Tetrabutyltin?

To stay informed about further developments, trends, and reports in the Tetrabutyltin, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence