Key Insights

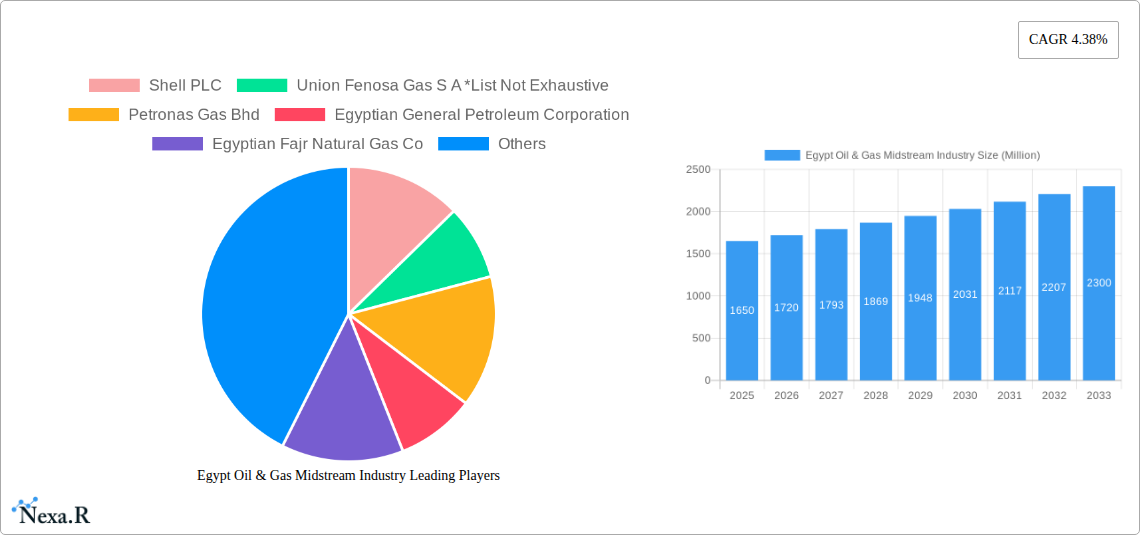

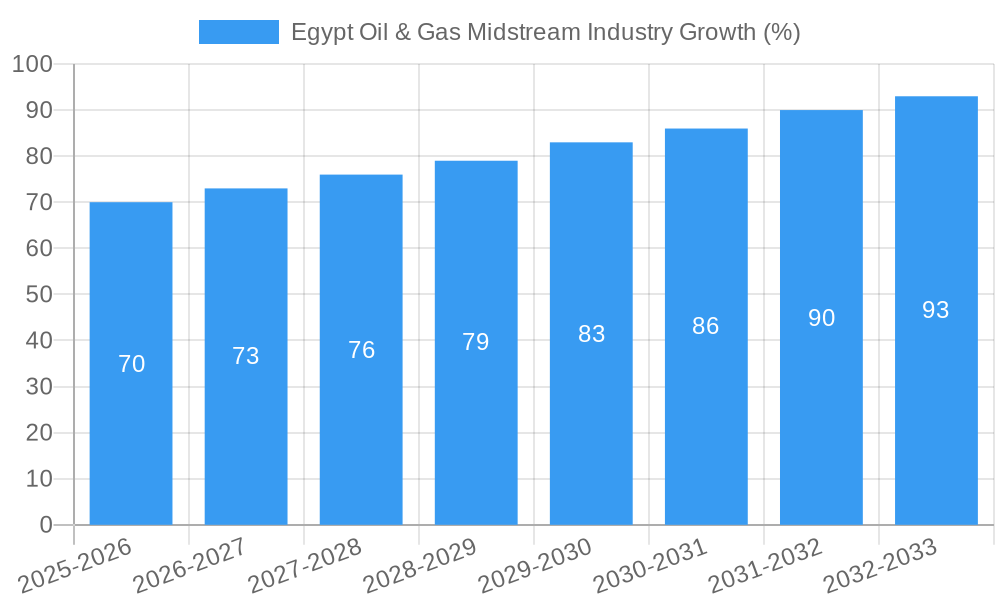

The Egypt Oil & Gas Midstream market, valued at $1.65 billion in 2025, is projected to experience steady growth, driven by increasing domestic energy demand and strategic investments in infrastructure development. A Compound Annual Growth Rate (CAGR) of 4.38% is anticipated from 2025 to 2033, indicating a robust expansion trajectory. Key growth drivers include the nation's ongoing efforts to enhance its gas processing and transportation capabilities, coupled with exploration and production activities aimed at boosting domestic gas reserves. This expansion is further fueled by Egypt's strategic geographical location, facilitating natural gas exports to neighboring countries and Europe. The market is segmented into LNG terminals, transportation, and storage, each contributing significantly to the overall market value. Major players like Shell PLC, BP plc, and Eni S.p.A., alongside national companies such as Egyptian General Petroleum Corporation, actively participate in this dynamic landscape. While challenges such as regulatory hurdles and geopolitical uncertainties exist, the overall positive outlook for Egypt's energy sector points towards continued growth in the midstream segment.

The significant investment in new LNG terminals and pipeline infrastructure is a key catalyst for growth. This expansion enhances Egypt's ability to process and transport natural gas efficiently, both domestically and internationally. Furthermore, the growing emphasis on renewable energy sources alongside natural gas represents a nuanced trend; while natural gas remains a vital energy source in the foreseeable future, the transition towards cleaner energy sources could potentially influence the long-term growth rate. The market's robust growth also reflects Egypt's commitment to strengthening its energy security and reducing reliance on imported energy. However, potential restraints include global price volatility of oil and gas and competition from other energy sources. Despite these challenges, the overall positive outlook is supported by the government's sustained investment in infrastructure and exploration, securing the future of the Egypt Oil & Gas Midstream sector.

Egypt Oil & Gas Midstream Industry: Market Report 2019-2033

This comprehensive report provides a detailed analysis of the Egypt oil & gas midstream industry, encompassing market dynamics, growth trends, key players, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry professionals, investors, and policymakers. The report delves into the parent market (Oil & Gas) and child markets (LNG Terminals, Transportation, Storage) to offer a holistic view.

Egypt Oil & Gas Midstream Industry Market Dynamics & Structure

This section analyzes the market concentration, technological innovation, regulatory landscape, competitive dynamics, and M&A activity within Egypt's oil & gas midstream sector. The Egyptian midstream market is characterized by a mix of state-owned enterprises and international players, leading to a moderately concentrated market structure. Market share is estimated at xx% for state-owned entities and xx% for private entities in 2025.

- Market Concentration: Moderate, with a mix of SOEs and international players. xx% market share held by top 5 players in 2025.

- Technological Innovation: Driven by the need for efficient transportation, storage, and regasification of LNG, with a focus on automation and digitalization. However, innovation is hampered by xx.

- Regulatory Framework: The Egyptian government plays a significant role in regulating the sector, focusing on infrastructure development and energy security. Recent policy changes have xx.

- Competitive Landscape: Intense competition among both domestic and international players exists, primarily focused on securing infrastructure access and contracts.

- M&A Activity: Moderate levels of M&A activity observed during 2019-2024, with xx deals finalized, primarily focused on infrastructure expansion. The total deal value was approximately xx million.

- End-User Demographics: Primarily focused on domestic consumption with increasing exports anticipated in the forecast period.

Egypt Oil & Gas Midstream Industry Growth Trends & Insights

The Egyptian oil & gas midstream market has experienced steady growth during the historical period (2019-2024), driven by increasing domestic demand and strategic investments in infrastructure. The market size is projected to reach xx million in 2025, growing at a CAGR of xx% from 2025 to 2033. This growth is fueled by increased LNG imports, investments in pipeline infrastructure and storage facilities, and government initiatives to enhance energy security. Technological disruptions such as the adoption of smart pipelines and digitalization of operations are driving efficiency gains. Shifting consumer behavior towards cleaner energy sources presents both challenges and opportunities.

Dominant Regions, Countries, or Segments in Egypt Oil & Gas Midstream Industry

The Ain Sokhna region is currently the dominant area for oil and gas midstream activities, driven by its strategic location on the Red Sea and access to major pipelines. Other key regions include Alexandria and Damietta, while the LNG terminal segment displays significant growth potential.

- LNG Terminals: The Ain Sokhna region is currently the most significant LNG terminal location in Egypt. The recent agreement with Jordan for use of the FSRU in Aqaba highlights the strategic importance of this segment.

- Transportation: Pipeline networks are the dominant mode of transportation, with significant investments being made to expand capacity and efficiency.

- Storage: The Ain Sokhna region dominates oil storage, with planned expansion in El-Tebbin further strengthening this segment's position.

Key growth drivers include government investments in infrastructure, increased LNG imports, and growing domestic energy consumption. The potential for regional energy trade further enhances the growth prospects of this segment.

Egypt Oil & Gas Midstream Industry Product Landscape

The Egyptian oil & gas midstream industry product landscape includes LNG terminals, pipelines, storage facilities, and related services. Recent innovations include the adoption of smart technologies for pipeline monitoring and the utilization of advanced storage systems to enhance efficiency and safety. The focus is on enhancing capacity, improving efficiency, and minimizing environmental impact.

Key Drivers, Barriers & Challenges in Egypt Oil & Gas Midstream Industry

Key Drivers: Increased domestic energy demand, government investments in infrastructure, strategic partnerships with international companies, and regional energy trade opportunities.

Key Challenges: High capital expenditure requirements for infrastructure development, regulatory complexities, and potential supply chain disruptions due to geopolitical instability. The estimated investment needed for infrastructure expansion between 2025 and 2033 is xx million.

Emerging Opportunities in Egypt Oil & Gas Midstream Industry

The growing demand for natural gas, investments in renewable energy infrastructure, and regional energy trade partnerships present significant opportunities. Further developments in LNG infrastructure and exploration in new gas fields are set to propel market growth.

Growth Accelerators in the Egypt Oil & Gas Midstream Industry Industry

Strategic government initiatives such as infrastructure development programs, increased private sector participation, and the adoption of advanced technologies will accelerate market expansion. The integration of renewable energy sources into the midstream infrastructure is also a significant growth catalyst.

Key Players Shaping the Egypt Oil & Gas Midstream Industry Market

- Shell PLC

- Union Fenosa Gas S A

- Petronas Gas Bhd

- Egyptian General Petroleum Corporation

- Egyptian Fajr Natural Gas Co

- Eni S p A

- Egyptian Natural Gas Holding Company

- BP p l c

- Spanish Egyptian Gas Company

Notable Milestones in Egypt Oil & Gas Midstream Industry Sector

- June 2023: Egypt and Jordan collaborate on using the FSRU at the Sheikh Sabah port in Aqaba.

- July 2022: Egyptian petroleum ministry announces plans for a new crude oil storage area in El-Tebbin (USD 96.21 million investment).

In-Depth Egypt Oil & Gas Midstream Industry Market Outlook

The Egyptian oil & gas midstream industry is poised for robust growth over the forecast period, driven by sustained domestic demand, strategic investments, and regional energy trade opportunities. Further investments in LNG infrastructure and exploration will unlock considerable market potential. Strategic partnerships and technological advancements will play crucial roles in shaping the sector’s future trajectory.

Egypt Oil & Gas Midstream Industry Segmentation

-

1. Transportation

-

1.1. Overview

- 1.1.1. Existing Infrastructure

- 1.1.2. Projects in pipeline

- 1.1.3. Upcoming projects

-

1.1. Overview

-

2. Storage

-

2.1. Overview

- 2.1.1. Existing Infrastructure

- 2.1.2. Projects in pipeline

- 2.1.3. Upcoming projects

-

2.1. Overview

-

3. LNG Terminals

-

3.1. Overview

- 3.1.1. Existing Infrastructure

- 3.1.2. Projects in pipeline

- 3.1.3. Upcoming projects

-

3.1. Overview

Egypt Oil & Gas Midstream Industry Segmentation By Geography

- 1. Egypt

Egypt Oil & Gas Midstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.38% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing investment in the Midstream Sector4.; Increasing Production of Oil and Natural Gas

- 3.3. Market Restrains

- 3.3.1. 4.; Inadequate Infrastructure in the Country

- 3.4. Market Trends

- 3.4.1. Transportation Sector to Witness Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Egypt Oil & Gas Midstream Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Transportation

- 5.1.1. Overview

- 5.1.1.1. Existing Infrastructure

- 5.1.1.2. Projects in pipeline

- 5.1.1.3. Upcoming projects

- 5.1.1. Overview

- 5.2. Market Analysis, Insights and Forecast - by Storage

- 5.2.1. Overview

- 5.2.1.1. Existing Infrastructure

- 5.2.1.2. Projects in pipeline

- 5.2.1.3. Upcoming projects

- 5.2.1. Overview

- 5.3. Market Analysis, Insights and Forecast - by LNG Terminals

- 5.3.1. Overview

- 5.3.1.1. Existing Infrastructure

- 5.3.1.2. Projects in pipeline

- 5.3.1.3. Upcoming projects

- 5.3.1. Overview

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Egypt

- 5.1. Market Analysis, Insights and Forecast - by Transportation

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Shell PLC

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Union Fenosa Gas S A *List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Petronas Gas Bhd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Egyptian General Petroleum Corporation

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Egyptian Fajr Natural Gas Co

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Eni S p A

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Egyptian Natural Gas Holding Company

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 BP p l c

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Spanish Egyptian Gas Company

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.1 Shell PLC

List of Figures

- Figure 1: Egypt Oil & Gas Midstream Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Egypt Oil & Gas Midstream Industry Share (%) by Company 2024

List of Tables

- Table 1: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Transportation 2019 & 2032

- Table 3: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Storage 2019 & 2032

- Table 4: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by LNG Terminals 2019 & 2032

- Table 5: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Transportation 2019 & 2032

- Table 8: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Storage 2019 & 2032

- Table 9: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by LNG Terminals 2019 & 2032

- Table 10: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Egypt Oil & Gas Midstream Industry?

The projected CAGR is approximately 4.38%.

2. Which companies are prominent players in the Egypt Oil & Gas Midstream Industry?

Key companies in the market include Shell PLC, Union Fenosa Gas S A *List Not Exhaustive, Petronas Gas Bhd, Egyptian General Petroleum Corporation, Egyptian Fajr Natural Gas Co, Eni S p A, Egyptian Natural Gas Holding Company, BP p l c, Spanish Egyptian Gas Company.

3. What are the main segments of the Egypt Oil & Gas Midstream Industry?

The market segments include Transportation, Storage, LNG Terminals.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.65 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing investment in the Midstream Sector4.; Increasing Production of Oil and Natural Gas.

6. What are the notable trends driving market growth?

Transportation Sector to Witness Growth.

7. Are there any restraints impacting market growth?

4.; Inadequate Infrastructure in the Country.

8. Can you provide examples of recent developments in the market?

In June 2023, Egypt and Jordan entered into a collaboration agreement that allows the North African nation to use the floating storage regasification unit (FSRU) at the Sheikh Sabah port in Aqaba. FSRU terminals are crucial in the liquefied natural gas value chain, forming the interface between LNG carriers and the local gas supply infrastructure. As part of the agreement, the Jordanian side will receive LNG from Egypt and pump back some of the gas through transborder pipelines to the country if needed.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Egypt Oil & Gas Midstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Egypt Oil & Gas Midstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Egypt Oil & Gas Midstream Industry?

To stay informed about further developments, trends, and reports in the Egypt Oil & Gas Midstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence