Key Insights

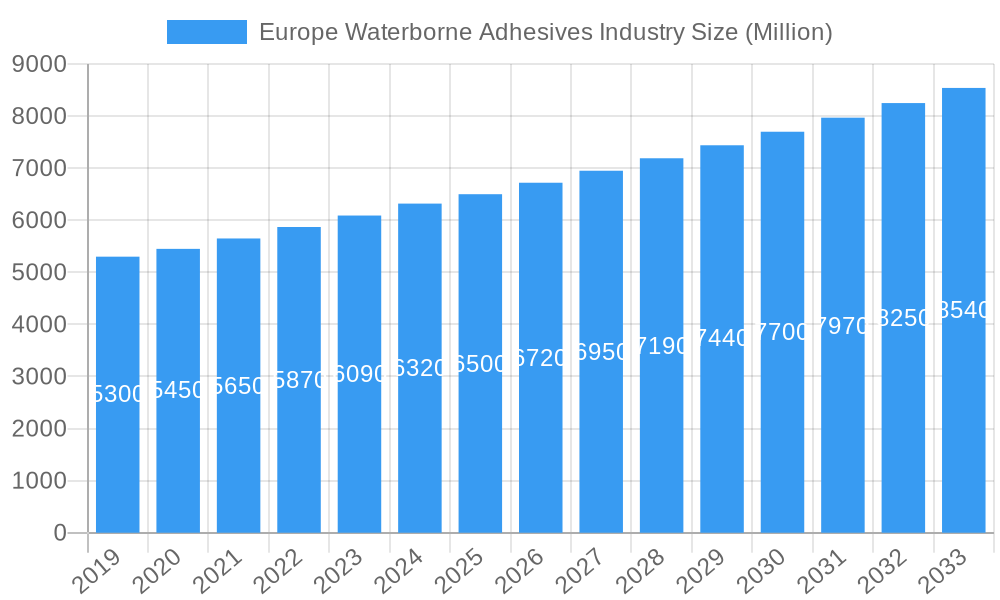

The European waterborne adhesives market is projected to achieve a market size of USD 19.29 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of 5.7% through 2033. This expansion is driven by the increasing demand for eco-friendly, low-VOC adhesive solutions in response to stringent European environmental regulations and a growing consumer preference for sustainable products. The building and construction sector is a primary beneficiary, utilizing waterborne adhesives for flooring, wall coverings, and structural bonding. The paper, board, and packaging industry also remains a significant consumer, benefiting from the cost-effectiveness and recyclability of these adhesives in applications such as carton sealing, labeling, and flexible packaging.

Europe Waterborne Adhesives Industry Market Size (In Billion)

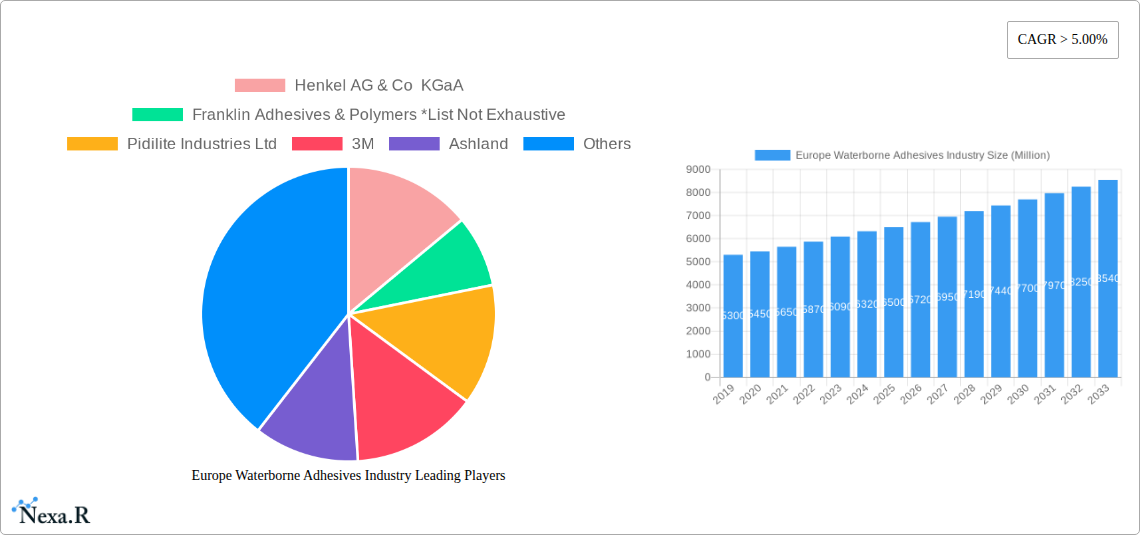

Technological advancements in resin formulations, enhancing adhesion strength, durability, and curing times, are key market drivers. While acrylics and PVA emulsions currently dominate due to their versatility and cost-effectiveness, innovations in EVA emulsions and polyurethane dispersions are emerging for specialized applications. Fluctuating raw material prices and the initial investment in advanced waterborne adhesive technologies are market restraints, offset by long-term cost savings and environmental compliance benefits. Leading companies such as Henkel AG & Co KGaA, Pidilite Industries Ltd, and 3M are actively investing in R&D to meet evolving market demands and expand their presence in key European markets, including Germany, the United Kingdom, and France.

Europe Waterborne Adhesives Industry Company Market Share

Europe Waterborne Adhesives Industry Report Description: Market Dynamics, Growth Trends, and Key Players (2019-2033)

This comprehensive report offers an in-depth analysis of the Europe waterborne adhesives market, a critical segment within the broader adhesives and sealants industry. Delving into market dynamics, growth trends, product landscape, and key players, this study provides actionable insights for stakeholders navigating the evolving European market. With a forecast period extending from 2025 to 2033, this report leverages historical data from 2019-2024 and a base year of 2025 to deliver precise market valuations in Million units. Discover critical information on parent and child market segments, driven by high-traffic keywords to maximize search engine visibility and engagement within the industry.

Europe Waterborne Adhesives Industry Market Dynamics & Structure

The Europe waterborne adhesives market exhibits a moderate to high concentration, with a few key global players holding significant market share. Technological innovation is a primary driver, fueled by increasing demand for eco-friendly and low-VOC (Volatile Organic Compound) adhesive solutions across various end-user industries. Regulatory frameworks, particularly those driven by the European Union's environmental directives, are instrumental in shaping product development and adoption. Competitive product substitutes, such as solvent-based or hot-melt adhesives, pose a consistent challenge, though the performance and environmental benefits of waterborne alternatives are gaining traction. End-user demographics are shifting, with a growing emphasis on sustainability and performance in sectors like Building & Construction and Paper, Board, and Packaging. Mergers and acquisitions (M&A) activity remains a notable trend, as companies seek to expand their product portfolios, geographical reach, and technological capabilities. For instance, the past few years have seen approximately 15-20 significant M&A deals valued at over €500 Million in the broader European adhesives sector, with waterborne technologies being a key focus. Innovation barriers include the high cost of research and development for novel formulations and the need for significant investment in manufacturing infrastructure to meet increasing demand.

- Market Concentration: Moderate to High.

- Key Drivers: Eco-friendliness, low-VOC regulations, demand for sustainable solutions.

- Regulatory Influence: Strong impact from EU environmental policies.

- Competitive Landscape: Waterborne vs. solvent-based and hot-melt adhesives.

- End-User Trends: Growing demand for performance and sustainability.

- M&A Activity: Consistent consolidation and strategic acquisitions.

- Innovation Barriers: R&D costs, infrastructure investment.

Europe Waterborne Adhesives Industry Growth Trends & Insights

The Europe waterborne adhesives market is poised for robust growth, driven by a confluence of evolving industry trends and increasing environmental consciousness. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period 2025-2033. Adoption rates for waterborne adhesives are steadily increasing across diverse end-user industries, notably in Building & Construction and Paper, Board, and Packaging, where demand for safer and more sustainable bonding solutions is paramount. Technological disruptions are continuously reshaping the market, with advancements in polymer science leading to the development of high-performance waterborne adhesives that rival traditional solvent-based formulations. These innovations include improved tack, faster curing times, enhanced water resistance, and greater adhesion to challenging substrates. Consumer behavior shifts are playing a significant role, with a growing preference for products manufactured using environmentally responsible processes. This is leading to increased pressure on manufacturers to adopt sustainable material solutions, including waterborne adhesives. Market penetration of waterborne adhesives in the Woodworking & Joinery sector, for example, is estimated to reach 45% by 2028, up from approximately 35% in 2024, reflecting this trend. The health and safety benefits associated with lower VOC emissions from waterborne adhesives are also a key factor influencing their adoption in sectors like Healthcare and Electrical & Electronics. Furthermore, the circular economy principles are gaining momentum, encouraging the use of waterborne adhesives that are often more compatible with recycling processes. The development of bio-based waterborne adhesives is another emerging trend that is expected to accelerate market growth, offering a sustainable alternative for a wide range of applications. The overall market evolution is characterized by a continuous push towards performance enhancements that do not compromise on environmental sustainability, making waterborne adhesives a preferred choice for a growing segment of the European market.

Dominant Regions, Countries, or Segments in Europe Waterborne Adhesives Industry

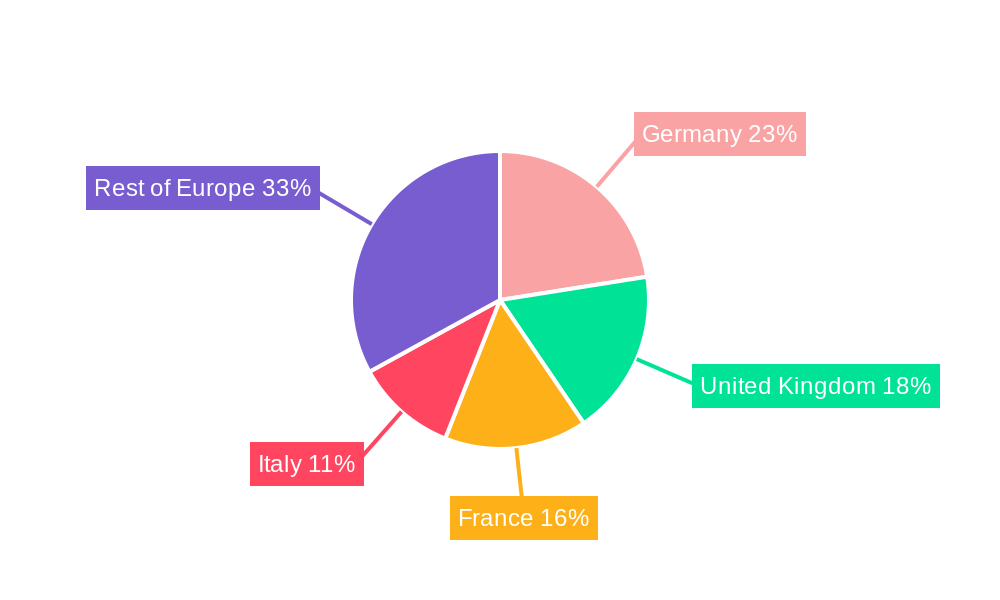

The Europe waterborne adhesives industry is experiencing significant growth, with particular dominance observed in specific regions and segments. Germany stands out as the leading country, driven by its robust industrial manufacturing base, stringent environmental regulations, and a strong emphasis on innovation in the Building & Construction and Automotive sectors. The country’s advanced infrastructure and high per capita income further contribute to the demand for premium, sustainable adhesive solutions.

Among the resin types, Acrylics are a dominant segment, accounting for an estimated 35% of the total market share in 2025. Their versatility, excellent adhesion properties, and adaptability to various formulations make them indispensable across numerous applications. Polyvinyl Acetate (PVA) Emulsion and Ethylene Vinyl Acetate (EVA) Emulsion are also significant contributors, particularly in the Paper, Board, and Packaging and Woodworking & Joinery segments, respectively.

The Building & Construction end-user industry is a major growth engine, contributing approximately 30% of the total market revenue in 2025. This is propelled by ongoing infrastructure development, renovation activities, and a growing preference for low-VOC building materials. The Paper, Board, and Packaging segment follows closely, driven by the surge in e-commerce and the demand for sustainable packaging solutions. The Woodworking & Joinery sector also plays a crucial role, with increasing demand for high-performance, environmentally friendly adhesives for furniture manufacturing and construction.

Key drivers of dominance in these segments include:

- Economic Policies: Government initiatives promoting green building and sustainable manufacturing.

- Infrastructure Development: Continuous investment in construction projects across Europe.

- Technological Advancements: Development of specialized waterborne adhesives for niche applications.

- Consumer Demand: Growing awareness and preference for eco-friendly and safe products.

- Regulatory Compliance: Strict adherence to environmental standards favoring low-VOC solutions.

For instance, the German government's "Green Building" initiatives and incentives for energy-efficient construction directly fuel the demand for waterborne adhesives in this sector. Similarly, the growing emphasis on recyclable packaging in the EU countries boosts the consumption of waterborne adhesives in the Paper, Board, and Packaging industry. The market share for Acrylic-based waterborne adhesives is projected to grow by 6% from 2025 to 2033, indicating its sustained dominance.

Europe Waterborne Adhesives Industry Product Landscape

The Europe waterborne adhesives industry is characterized by continuous product innovation focused on enhancing performance, sustainability, and application versatility. Manufacturers are developing advanced acrylic, PVA, and EVA emulsions with improved tack, faster drying times, and superior adhesion to a wider range of substrates, including challenging plastics and composites. Innovations in polyurethane dispersions (PUDs) are yielding high-performance adhesives with excellent durability and water resistance, suitable for demanding applications in Transportation and Building & Construction. Unique selling propositions often revolve around achieving "green" certifications, low-VOC content, and compliance with stringent environmental regulations like REACH. Technological advancements are enabling the creation of specialized formulations for specific end-user needs, such as UV-curable waterborne adhesives for rapid assembly in electronics or bio-based waterborne adhesives derived from renewable resources.

Key Drivers, Barriers & Challenges in Europe Waterborne Adhesives Industry

Key Drivers:

- Environmental Regulations: Stringent EU directives on VOC emissions are a primary catalyst for the adoption of waterborne adhesives.

- Sustainability Demand: Growing consumer and industrial preference for eco-friendly products and manufacturing processes.

- Technological Advancements: Development of high-performance, low-VOC waterborne formulations with improved adhesion and durability.

- Growth in Key End-User Industries: Expansion of sectors like Building & Construction and Paper, Board, and Packaging fuels demand.

Barriers & Challenges:

- Performance Limitations: In certain high-stress applications, some waterborne adhesives may still struggle to match the performance of solvent-based counterparts, particularly in terms of initial tack and water resistance.

- Cost Competitiveness: Historically, some waterborne formulations have been more expensive than traditional alternatives, impacting adoption rates in price-sensitive markets.

- Drying Times: While improving, drying times for waterborne adhesives can sometimes be longer than for solvent-based or hot-melt systems, affecting production line speeds.

- Supply Chain Volatility: Disruptions in the supply of raw materials, such as key monomers and polymers, can impact production and pricing. For example, recent global supply chain issues have led to an estimated 10-15% increase in raw material costs for certain adhesive components.

- Competition from Substitutes: Continued competition from established solvent-based and hot-melt adhesive technologies.

Emerging Opportunities in Europe Waterborne Adhesives Industry

Emerging opportunities in the Europe waterborne adhesives industry lie in the development of bio-based and biodegradable waterborne adhesives derived from renewable resources, catering to the growing circular economy focus. The expansion of smart packaging solutions presents a niche but growing market for specialized waterborne adhesives with unique functionalities. Furthermore, the increasing demand for lightweighting in the Transportation sector is driving innovation in waterborne adhesives for bonding advanced composite materials. Untapped markets within the Eastern European countries, driven by increasing industrialization and infrastructure projects, also represent significant growth potential. The rise of additive manufacturing (3D printing) is creating new opportunities for waterborne adhesive formulations specifically designed for these advanced fabrication techniques.

Growth Accelerators in the Europe Waterborne Adhesives Industry Industry

The long-term growth of the Europe waterborne adhesives industry is significantly accelerated by ongoing technological breakthroughs, particularly in polymer science and formulation chemistry, leading to enhanced adhesive properties and broader application ranges. Strategic partnerships between raw material suppliers, adhesive manufacturers, and end-users are crucial for co-developing tailored solutions and accelerating market adoption. Market expansion strategies, including entering emerging European economies and targeting niche application segments like medical device assembly or electronics, are also key growth accelerators. The continuous push for stricter environmental regulations across EU member states acts as a sustained catalyst, compelling industries to transition towards more sustainable adhesive solutions. The development of advanced application technologies and equipment that optimize the use and curing of waterborne adhesives further supports market expansion.

Key Players Shaping the Europe Waterborne Adhesives Industry Market

- Henkel AG & Co KGaA

- Franklin Adhesives & Polymers

- Pidilite Industries Ltd

- 3M

- Ashland

- Arkema Group

- Dow

- Sika AG

Notable Milestones in Europe Waterborne Adhesives Industry Sector

- 2023: Launch of a new generation of high-performance acrylic waterborne adhesives offering superior adhesion to recycled plastics.

- 2022: Significant investment in R&D by leading companies focused on developing bio-based waterborne adhesives.

- 2021: Increased M&A activity as larger players acquire smaller, innovative companies specializing in waterborne adhesive technologies.

- 2020: Heightened focus on low-VOC waterborne adhesives driven by reinforced environmental regulations across the EU.

- 2019: Introduction of novel polyurethane dispersion (PUD) based waterborne adhesives with enhanced durability for automotive applications.

In-Depth Europe Waterborne Adhesives Industry Market Outlook

The Europe waterborne adhesives industry is set for sustained growth, driven by a potent combination of regulatory mandates, increasing environmental consciousness, and continuous technological innovation. The outlook is characterized by the ongoing development of advanced, high-performance waterborne formulations that address specific end-user needs, from improved adhesion to faster curing times. Strategic partnerships and market expansion into promising Eastern European regions will further fuel demand. The industry's ability to adapt to circular economy principles and develop sustainable, bio-based alternatives will be critical for long-term success. Overall, the market presents substantial opportunities for companies investing in R&D and focusing on eco-friendly solutions.

Europe Waterborne Adhesives Industry Segmentation

-

1. Resin Type

- 1.1. Acrylics

- 1.2. Polyvinyl Acetate (PVA) Emulsion

- 1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 1.4. Polyuret

- 1.5. Other Resin Types

-

2. End-user Industry

- 2.1. Building & Construction

- 2.2. Paper, Board, and Packaging

- 2.3. Woodworking & Joinery

- 2.4. Transportation

- 2.5. Healthcare

- 2.6. Electrical & Electronics

- 2.7. Other End-user Industries

Europe Waterborne Adhesives Industry Segmentation By Geography

- 1. Geramany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Rest of Europe

Europe Waterborne Adhesives Industry Regional Market Share

Geographic Coverage of Europe Waterborne Adhesives Industry

Europe Waterborne Adhesives Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 5.1.1. Acrylics

- 5.1.2. Polyvinyl Acetate (PVA) Emulsion

- 5.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 5.1.4. Polyuret

- 5.1.5. Other Resin Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Building & Construction

- 5.2.2. Paper, Board, and Packaging

- 5.2.3. Woodworking & Joinery

- 5.2.4. Transportation

- 5.2.5. Healthcare

- 5.2.6. Electrical & Electronics

- 5.2.7. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Geramany

- 5.3.2. United Kingdom

- 5.3.3. France

- 5.3.4. Italy

- 5.3.5. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 6. Europe Waterborne Adhesives Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 6.1.1. Acrylics

- 6.1.2. Polyvinyl Acetate (PVA) Emulsion

- 6.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 6.1.4. Polyuret

- 6.1.5. Other Resin Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Building & Construction

- 6.2.2. Paper, Board, and Packaging

- 6.2.3. Woodworking & Joinery

- 6.2.4. Transportation

- 6.2.5. Healthcare

- 6.2.6. Electrical & Electronics

- 6.2.7. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 7. Geramany Europe Waterborne Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 7.1.1. Acrylics

- 7.1.2. Polyvinyl Acetate (PVA) Emulsion

- 7.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 7.1.4. Polyuret

- 7.1.5. Other Resin Types

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Building & Construction

- 7.2.2. Paper, Board, and Packaging

- 7.2.3. Woodworking & Joinery

- 7.2.4. Transportation

- 7.2.5. Healthcare

- 7.2.6. Electrical & Electronics

- 7.2.7. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 8. United Kingdom Europe Waterborne Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 8.1.1. Acrylics

- 8.1.2. Polyvinyl Acetate (PVA) Emulsion

- 8.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 8.1.4. Polyuret

- 8.1.5. Other Resin Types

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Building & Construction

- 8.2.2. Paper, Board, and Packaging

- 8.2.3. Woodworking & Joinery

- 8.2.4. Transportation

- 8.2.5. Healthcare

- 8.2.6. Electrical & Electronics

- 8.2.7. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 9. France Europe Waterborne Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Resin Type

- 9.1.1. Acrylics

- 9.1.2. Polyvinyl Acetate (PVA) Emulsion

- 9.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 9.1.4. Polyuret

- 9.1.5. Other Resin Types

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Building & Construction

- 9.2.2. Paper, Board, and Packaging

- 9.2.3. Woodworking & Joinery

- 9.2.4. Transportation

- 9.2.5. Healthcare

- 9.2.6. Electrical & Electronics

- 9.2.7. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Resin Type

- 10. Italy Europe Waterborne Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Resin Type

- 10.1.1. Acrylics

- 10.1.2. Polyvinyl Acetate (PVA) Emulsion

- 10.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 10.1.4. Polyuret

- 10.1.5. Other Resin Types

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Building & Construction

- 10.2.2. Paper, Board, and Packaging

- 10.2.3. Woodworking & Joinery

- 10.2.4. Transportation

- 10.2.5. Healthcare

- 10.2.6. Electrical & Electronics

- 10.2.7. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Resin Type

- 11. Rest of Europe Europe Waterborne Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Resin Type

- 11.1.1. Acrylics

- 11.1.2. Polyvinyl Acetate (PVA) Emulsion

- 11.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 11.1.4. Polyuret

- 11.1.5. Other Resin Types

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Building & Construction

- 11.2.2. Paper, Board, and Packaging

- 11.2.3. Woodworking & Joinery

- 11.2.4. Transportation

- 11.2.5. Healthcare

- 11.2.6. Electrical & Electronics

- 11.2.7. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Resin Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Henkel AG & Co KGaA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Franklin Adhesives & Polymers *List Not Exhaustive

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Pidilite Industries Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 3M

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ashland

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Arkema Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Dow

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Sika AG

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 Henkel AG & Co KGaA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Europe Waterborne Adhesives Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Waterborne Adhesives Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 2: Europe Waterborne Adhesives Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 5: Europe Waterborne Adhesives Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 8: Europe Waterborne Adhesives Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 9: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 11: Europe Waterborne Adhesives Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 12: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 14: Europe Waterborne Adhesives Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 17: Europe Waterborne Adhesives Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 18: Europe Waterborne Adhesives Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Waterborne Adhesives Industry?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the Europe Waterborne Adhesives Industry?

Key companies in the market include Henkel AG & Co KGaA, Franklin Adhesives & Polymers *List Not Exhaustive, Pidilite Industries Ltd, 3M, Ashland, Arkema Group, Dow, Sika AG.

3. What are the main segments of the Europe Waterborne Adhesives Industry?

The market segments include Resin Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.29 billion as of 2022.

5. What are some drivers contributing to market growth?

; Environmental Friendly Substitute to Solvent-based Adhesives; Other Drivers.

6. What are the notable trends driving market growth?

Polyvinyl Acetate (PVA) Emulsion to Dominate the Market.

7. Are there any restraints impacting market growth?

; Poor Setting Speed of the Waterborne Adhesives; Other Restraints.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Waterborne Adhesives Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Waterborne Adhesives Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Waterborne Adhesives Industry?

To stay informed about further developments, trends, and reports in the Europe Waterborne Adhesives Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence