Key Insights

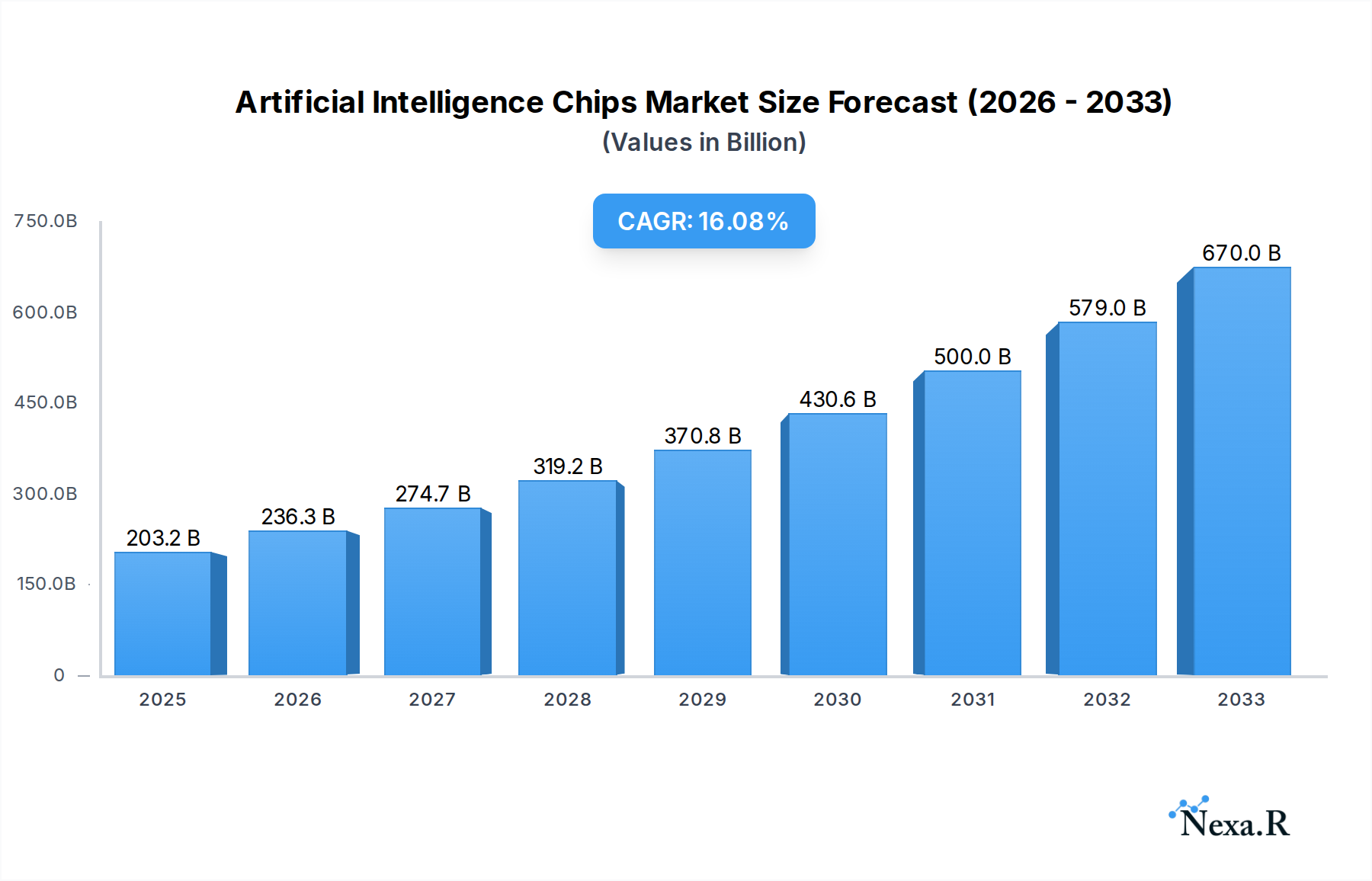

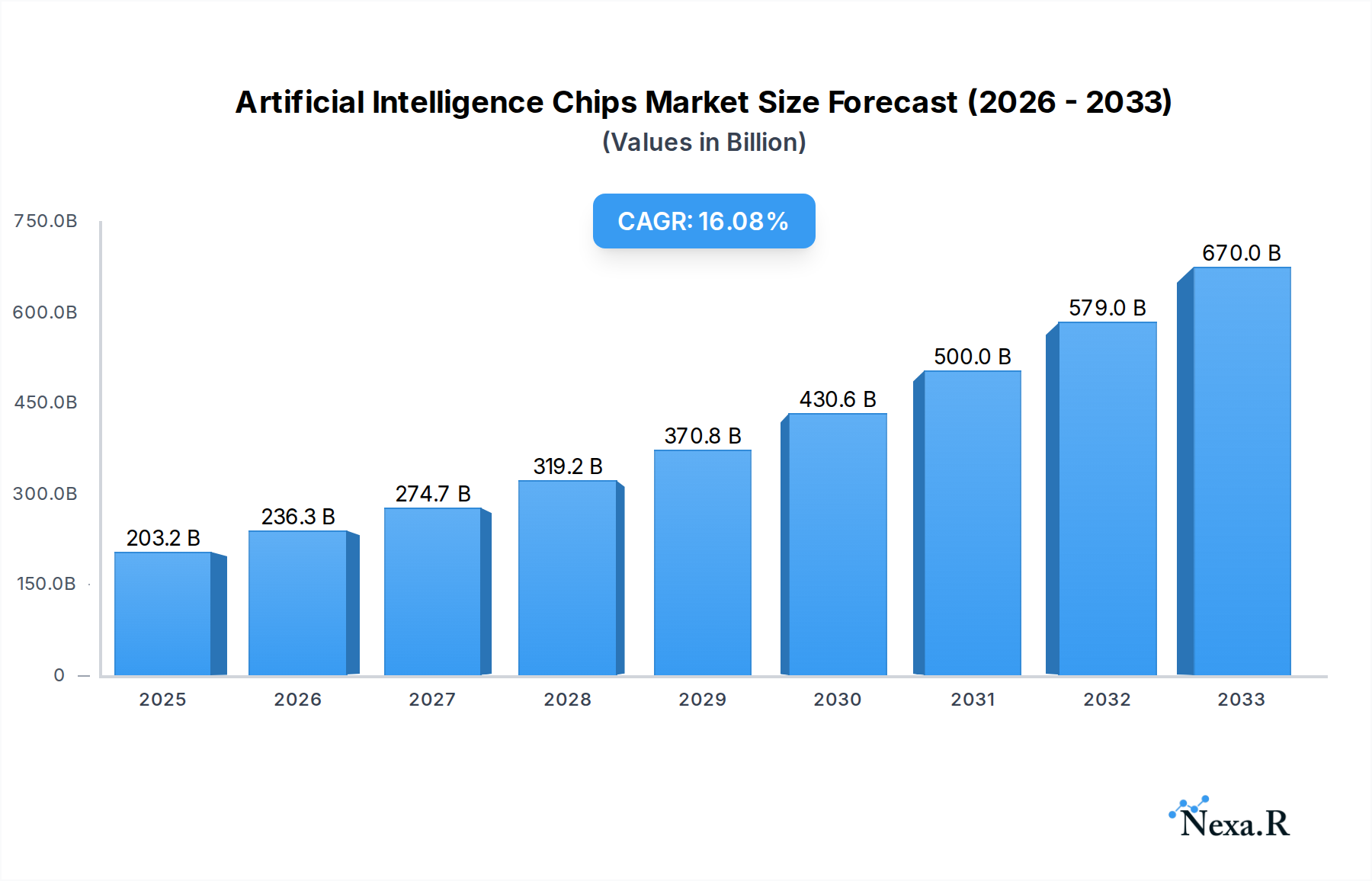

The Artificial Intelligence (AI) chip market is poised for exceptional growth, projected to reach $203.24 billion in 2025. This robust expansion is fueled by a 15.7% CAGR over the forecast period, indicating a significant surge in demand and technological advancement within the sector. The primary drivers for this growth are the escalating adoption of AI across diverse industries, the continuous innovation in AI algorithms demanding more powerful and specialized hardware, and the increasing investment in AI research and development by both established tech giants and emerging startups. Key applications like consumer electronics, automotive (specifically autonomous driving and advanced driver-assistance systems), industrial automation for enhanced efficiency, and sophisticated security systems are all heavily reliant on AI chips for their core functionalities. The market is characterized by intense competition and rapid technological evolution, with a strong emphasis on developing chips with higher processing power, lower energy consumption, and specialized architectures for machine learning and deep learning workloads.

Artificial Intelligence Chips Market Size (In Billion)

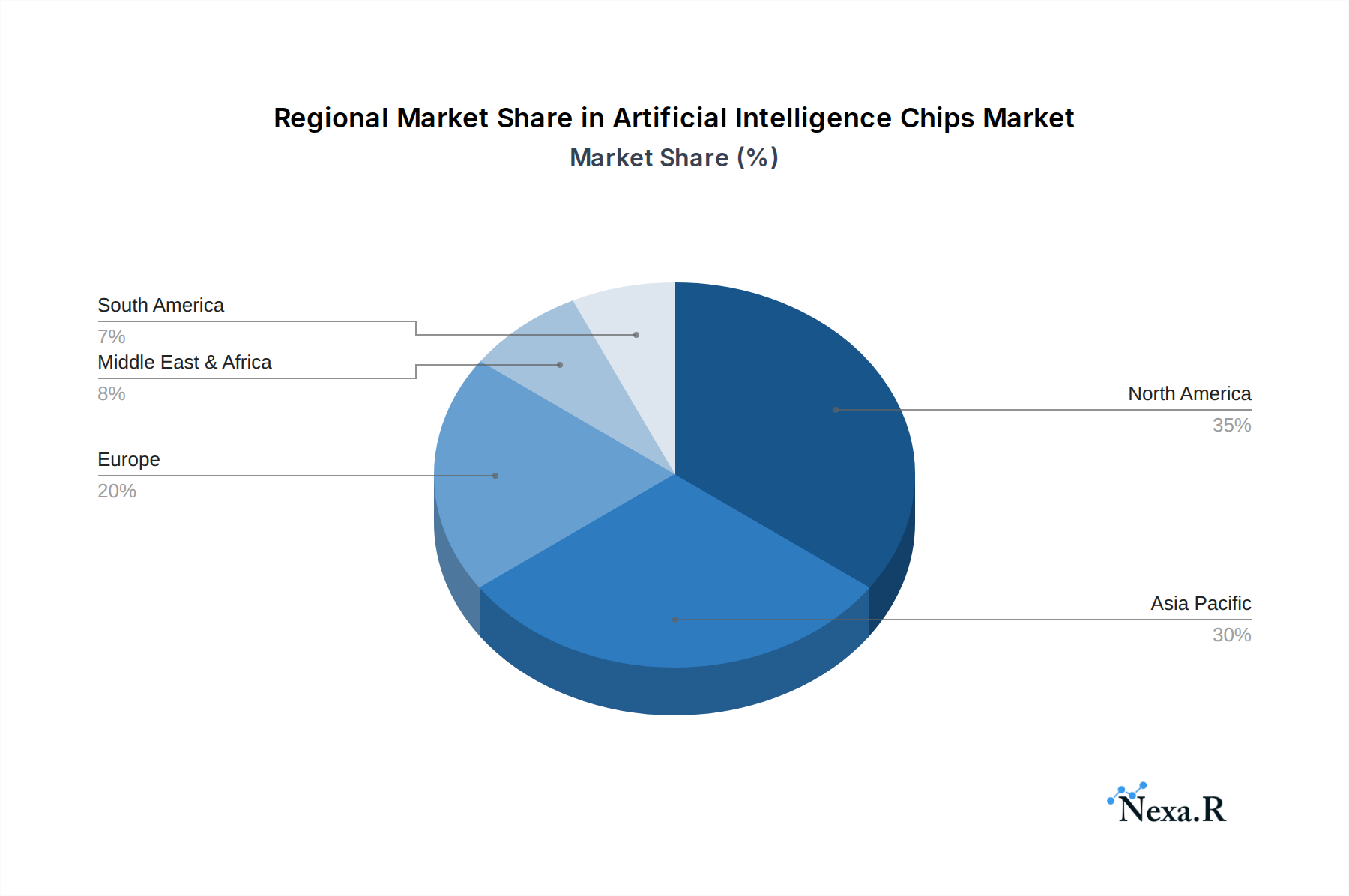

The market segmentation reveals a dynamic landscape. In terms of types, AI chips encompass a range of architectures, including the increasingly prevalent Graphics Processing Units (GPUs), Tensor Processing Units (TPUs) that are increasingly optimized for AI tasks, and Application-Specific Integrated Circuits (ASICs) designed for particular AI workloads, alongside more general-purpose Central Processing Units (CPUs) and other emerging architectures. Geographically, North America, particularly the United States, currently leads in AI chip development and adoption due to its strong R&D infrastructure and significant investment from major technology companies. However, the Asia Pacific region, driven by China and advancements in manufacturing capabilities, is expected to witness the fastest growth. Restraints, while present, are largely being overcome by innovation; these include the high cost of development and manufacturing, the need for specialized talent, and the ongoing challenge of energy efficiency in complex AI computations. Companies like NVIDIA, Intel, Qualcomm, and AMD are at the forefront, but an increasing number of specialized players are emerging, indicating a vibrant and competitive ecosystem.

Artificial Intelligence Chips Company Market Share

Artificial Intelligence Chips Market Dynamics & Structure

The artificial intelligence (AI) chips market is characterized by intense competition and rapid technological evolution, with key players like NVIDIA Corporation, Intel Corporation, and Qualcomm holding significant market share. The market concentration is moderately high, driven by the substantial R&D investments required and the proprietary nature of many AI architectures. Technological innovation is the primary driver, with continuous advancements in AI algorithms fueling the demand for specialized hardware. Key innovations include the development of more efficient AI accelerators, neuromorphic computing, and specialized processing units (PUs) tailored for deep learning inference and training. Regulatory frameworks, while nascent in some regions, are beginning to address data privacy, AI ethics, and semiconductor manufacturing capacity, potentially influencing market access and competition. Competitive product substitutes are emerging, particularly in specialized application domains, but high-performance GPUs and ASICs remain dominant for complex AI workloads. End-user demographics are broadening, encompassing not just technology giants but also enterprises across automotive, healthcare, and manufacturing sectors seeking to leverage AI for enhanced efficiency and new product development. Mergers and acquisitions (M&A) activity is a significant trend, with larger companies acquiring smaller, innovative startups to bolster their AI capabilities and secure intellectual property. For instance, the acquisition of ARM by NVIDIA (though ultimately blocked) highlights the strategic importance of IP in this sector. The market is projected to see a CAGR of 22.5% from 2025 to 2033, reaching an estimated market size of $135.8 billion in 2025 and expanding to $612.6 billion by 2033.

- Market Concentration: Moderate to High, driven by R&D intensity and IP ownership.

- Technological Innovation Drivers: Advancements in deep learning, neural networks, and specialized AI algorithms.

- Regulatory Frameworks: Emerging focus on AI ethics, data privacy, and semiconductor supply chain resilience.

- Competitive Product Substitutes: Growing emergence of specialized AI accelerators for specific applications.

- End-User Demographics: Expanding beyond tech giants to diverse enterprise sectors.

- M&A Trends: Strategic acquisitions of AI startups by established players to enhance capabilities.

Artificial Intelligence Chips Growth Trends & Insights

The artificial intelligence chips market is on an unprecedented growth trajectory, fueled by the ubiquitous integration of AI across virtually every industry. The market size for AI chips, which was valued at an estimated $78.4 billion in 2024, is projected to experience a robust compound annual growth rate (CAGR) of 22.5% during the forecast period of 2025–2033. This expansion is driven by an insatiable demand for processing power to handle increasingly complex AI models and workloads. Adoption rates are accelerating as businesses across consumer electronics, automotive, industrial automation, and security systems recognize the transformative potential of AI. From smart assistants and autonomous vehicles to predictive maintenance and sophisticated threat detection, AI chips are becoming the indispensable engine powering these innovations. Technological disruptions are a constant feature, with ongoing advancements in chip architectures such as GPUs, ASICs, and specialized PUs constantly pushing the boundaries of performance and efficiency. The development of dedicated AI accelerators, designed from the ground up for neural network computations, is a key trend. This has led to significant improvements in training times for deep learning models and faster inference speeds for real-time AI applications. Consumer behavior shifts are also playing a crucial role. As consumers become accustomed to AI-powered features in their daily lives, their expectations for intelligent products and services continue to rise, further stimulating demand for advanced AI hardware. The proliferation of smart devices, the increasing sophistication of gaming, and the growing adoption of virtual and augmented reality applications are all contributing factors. Furthermore, the push for edge AI, where AI processing is performed directly on devices rather than in the cloud, is creating new market opportunities for power-efficient and compact AI chips. This trend is particularly prominent in the automotive and industrial automation sectors, where low latency and robust data security are paramount. The market is also witnessing a surge in demand for AI chips capable of handling large language models (LLMs) and generative AI, which require immense computational resources. Companies are investing heavily in developing specialized hardware to cater to these computationally intensive tasks, leading to a dynamic and competitive landscape. The global market is anticipated to grow from an estimated $135.8 billion in 2025 to a staggering $612.6 billion by 2033. The parent market for AI chips is experiencing rapid expansion, with sub-segments like AI processors for data centers and AI chips for edge devices showing particularly strong growth. For instance, the demand for AI processors for data centers is driven by the increasing need for cloud-based AI services, while the market for edge AI chips is spurred by the proliferation of IoT devices and the need for on-device intelligence. The overall market growth is a testament to the foundational role AI chips play in enabling the next wave of technological innovation and digital transformation across all facets of the global economy.

Dominant Regions, Countries, or Segments in Artificial Intelligence Chips

The global artificial intelligence chips market is experiencing robust growth across multiple regions and segments, with certain areas exhibiting exceptional dominance. Currently, North America stands out as a leading region, driven by a confluence of factors including a strong presence of leading AI research institutions, a thriving venture capital ecosystem supporting AI startups, and a high concentration of technology giants investing heavily in AI R&D. The United States, in particular, benefits from companies like NVIDIA Corporation, Intel Corporation, and Google Inc., which are at the forefront of AI chip innovation and deployment. Economic policies that encourage technological advancement and significant government investment in AI research further bolster its position.

Within the Application segment, Consumer Electronics is a dominant force, representing approximately 35% of the total market share. This dominance is fueled by the widespread adoption of AI-powered features in smartphones, smart home devices, wearables, and gaming consoles. The ever-increasing demand for personalized experiences, enhanced functionality, and seamless user interfaces in consumer products necessitates powerful and efficient AI chips. The Automotive segment is rapidly emerging as a significant growth driver, with an estimated market share of 25%, driven by the development of autonomous driving systems, advanced driver-assistance systems (ADAS), and in-car infotainment powered by AI. The need for real-time data processing, object recognition, and decision-making in vehicles makes AI chips indispensable.

In terms of Types, GPUs (Graphics Processing Units) continue to hold a substantial market share, estimated at around 40%, owing to their inherent parallel processing capabilities, which are highly effective for AI training and deep learning workloads. However, ASICs (Application-Specific Integrated Circuits) designed specifically for AI tasks are gaining significant traction, capturing an estimated 30% of the market, due to their superior power efficiency and performance optimization for specific AI algorithms. PUs (Processing Units), including NPUs (Neural Processing Units), are also seeing rapid growth, with an estimated 25% market share, as they offer specialized acceleration for AI inference tasks in a more power-efficient manner, especially for edge computing applications.

- Dominant Region: North America, led by the United States, due to strong R&D, venture capital, and tech giant presence.

- Key Drivers: Technological innovation, supportive economic policies, government investment in AI.

- Dominant Application Segment: Consumer Electronics (approx. 35% market share).

- Key Drivers: Demand for AI-powered features in smart devices, personalized experiences, gaming.

- Emerging Application Segment: Automotive (approx. 25% market share).

- Key Drivers: Autonomous driving technology, ADAS, in-car AI.

- Dominant Chip Type: GPUs (approx. 40% market share).

- Key Drivers: Parallel processing for AI training and deep learning.

- Fastest Growing Chip Type: ASICs and PUs (approx. 30% and 25% market share respectively).

- Key Drivers: Power efficiency, specialized AI acceleration, edge computing.

Artificial Intelligence Chips Product Landscape

The artificial intelligence (AI) chips market is characterized by a dynamic product landscape focused on delivering increasingly sophisticated processing capabilities for AI workloads. Key product innovations include specialized AI accelerators designed for deep learning training and inference, such as NVIDIA's Tensor Cores, Intel's Gaudi accelerators, and Google's TPUs. These chips offer significant performance improvements over general-purpose CPUs. GPUs continue to be a popular choice for their parallel processing power, making them suitable for complex AI tasks. ASICs are emerging as a critical segment, with companies like Cerebras Systems developing wafer-scale engines for unparalleled AI computational power. The product landscape also features a growing array of PUs, including NPUs, which are optimized for energy-efficient AI inference at the edge, enabling AI functionalities in devices like smartphones and smart cameras. Performance metrics are constantly being pushed, with advancements in teraflops (TFLOPS) for AI computations, power efficiency (TOPS/watt), and memory bandwidth. Unique selling propositions revolve around raw performance, energy efficiency, cost-effectiveness for specific applications, and specialized architectures catering to evolving AI models.

Key Drivers, Barriers & Challenges in Artificial Intelligence Chips

The artificial intelligence (AI) chips market is propelled by several key drivers. The exponential growth of data generated globally, coupled with the increasing sophistication of AI algorithms and machine learning models, creates an insatiable demand for high-performance processing. The pervasive integration of AI across industries like automotive, healthcare, consumer electronics, and industrial automation, to enhance efficiency, unlock new insights, and drive innovation, is a primary growth catalyst. Furthermore, government initiatives and increasing R&D investments from leading technology companies are accelerating technological advancements in AI chip design.

However, significant barriers and challenges impede market growth. The high cost of developing and manufacturing advanced AI chips, coupled with the complexity of semiconductor fabrication, presents a substantial hurdle. Supply chain disruptions, particularly concerning the availability of advanced manufacturing equipment and raw materials, pose a constant threat. Regulatory hurdles related to data privacy, AI ethics, and international trade restrictions can also impact market access and adoption. Moreover, the intense competition among established players and emerging startups necessitates continuous innovation, making it challenging for smaller companies to compete on price and performance.

Emerging Opportunities in Artificial Intelligence Chips

Emerging opportunities in the artificial intelligence chips sector are abundant and multifaceted. The rapid expansion of the Internet of Things (IoT) ecosystem presents a significant opportunity for AI chips designed for edge computing, enabling intelligent processing directly on devices for applications ranging from smart homes and wearables to industrial sensors. The burgeoning field of generative AI, encompassing large language models and AI-driven content creation, is creating a demand for specialized, high-performance AI chips capable of handling immense computational loads for training and inference. Furthermore, the healthcare sector is increasingly adopting AI for drug discovery, personalized medicine, and medical imaging analysis, opening new avenues for AI chip development tailored to these specialized applications. The increasing focus on AI for sustainability, such as optimizing energy consumption and resource management, also presents untapped market potential.

Growth Accelerators in the Artificial Intelligence Chips Industry

Several critical factors are accelerating growth within the artificial intelligence chips industry. Continued breakthroughs in semiconductor manufacturing processes, enabling smaller transistor sizes and increased chip density, are fundamental. The relentless advancement of AI algorithms, particularly in deep learning and reinforcement learning, consistently drives the need for more powerful and specialized hardware. Strategic partnerships between chip manufacturers, AI software developers, and end-user industries are crucial for co-developing tailored solutions and accelerating market adoption. Market expansion into emerging economies and the development of more accessible AI chip solutions for smaller businesses and research institutions are also key growth catalysts.

Key Players Shaping the Artificial Intelligence Chips Market

- Huawei Technologies

- Qualcomm

- IBM Corporation

- NVIDIA Corporation

- Intel Corporation

- MediaTek Inc

- Cerebras Systems

- Samsung Electronics

- Advanced Micro Devices

- Apple Inc

- Google Inc

- ARM

- Intel

- Graphcore

- LG

- Imagination Technologies

- Anari

Notable Milestones in Artificial Intelligence Chips Sector

- 2023: NVIDIA announces its Blackwell GPU architecture, designed for advanced AI and metaverse workloads.

- 2023: Cerebras Systems unveils its Wafer-Scale Engine 3, delivering massive improvements in AI training performance.

- 2022: Intel releases its 4th Gen Xeon Scalable processors with integrated AI acceleration capabilities.

- 2022: Apple introduces its M2 Ultra chip, featuring enhanced Neural Engine performance for AI tasks.

- 2021: AMD launches its Instinct MI200 series accelerators, targeting high-performance AI and HPC workloads.

- 2020: Google announces its 5th generation of Tensor Processing Units (TPUs), further optimizing AI inference.

- 2019: Qualcomm introduces its Snapdragon 8 Gen 1 mobile platform with an advanced AI Engine.

- 2019: ARM announces its new Neoverse V-series cores, designed for AI and HPC applications in the cloud.

In-Depth Artificial Intelligence Chips Market Outlook

The outlook for the artificial intelligence (AI) chips market remains exceptionally strong, poised for sustained high-growth driven by foundational technological advancements and widespread industry adoption. Key growth accelerators include the continued evolution of AI algorithms, particularly in areas like generative AI and reinforcement learning, which will necessitate increasingly powerful and specialized processing capabilities. The expansion of edge AI, enabling intelligence at the device level, will fuel demand for energy-efficient and compact AI chips across diverse IoT applications. Strategic collaborations between chip manufacturers, software developers, and end-users will continue to foster innovation and accelerate product development cycles. Furthermore, increasing governmental support for domestic semiconductor manufacturing and AI research in various regions will create a more robust and resilient global supply chain, supporting market expansion and technological progress. The market is expected to witness significant investments in R&D for novel architectures, such as neuromorphic computing, further pushing the boundaries of AI processing.

Artificial Intelligence Chips Segmentation

-

1. Application

- 1.1. Consumer Electronics

- 1.2. Automotive

- 1.3. Industrial Automation

- 1.4. Security Systems

- 1.5. Others

-

2. Types

- 2.1. PU

- 2.2. GPU

- 2.3. ASIC

- 2.4. Others

Artificial Intelligence Chips Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Artificial Intelligence Chips Regional Market Share

Geographic Coverage of Artificial Intelligence Chips

Artificial Intelligence Chips REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Consumer Electronics

- 5.1.2. Automotive

- 5.1.3. Industrial Automation

- 5.1.4. Security Systems

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. PU

- 5.2.2. GPU

- 5.2.3. ASIC

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Artificial Intelligence Chips Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Consumer Electronics

- 6.1.2. Automotive

- 6.1.3. Industrial Automation

- 6.1.4. Security Systems

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. PU

- 6.2.2. GPU

- 6.2.3. ASIC

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Artificial Intelligence Chips Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Consumer Electronics

- 7.1.2. Automotive

- 7.1.3. Industrial Automation

- 7.1.4. Security Systems

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. PU

- 7.2.2. GPU

- 7.2.3. ASIC

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Artificial Intelligence Chips Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Consumer Electronics

- 8.1.2. Automotive

- 8.1.3. Industrial Automation

- 8.1.4. Security Systems

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. PU

- 8.2.2. GPU

- 8.2.3. ASIC

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Artificial Intelligence Chips Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Consumer Electronics

- 9.1.2. Automotive

- 9.1.3. Industrial Automation

- 9.1.4. Security Systems

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. PU

- 9.2.2. GPU

- 9.2.3. ASIC

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Artificial Intelligence Chips Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Consumer Electronics

- 10.1.2. Automotive

- 10.1.3. Industrial Automation

- 10.1.4. Security Systems

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. PU

- 10.2.2. GPU

- 10.2.3. ASIC

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Artificial Intelligence Chips Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Consumer Electronics

- 11.1.2. Automotive

- 11.1.3. Industrial Automation

- 11.1.4. Security Systems

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. PU

- 11.2.2. GPU

- 11.2.3. ASIC

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Huawei Technologies

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Qualcomm

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 IBM Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 NVIDIA Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Intel Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 MediaTek Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Cerebras Systems

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Samsung Electronics

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Advanced Micro Devices

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Apple Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Google Inc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 ARM

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Intel

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Graphcore

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 LG

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Imagination Technologies

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Anari

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 Huawei Technologies

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Artificial Intelligence Chips Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Artificial Intelligence Chips Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Artificial Intelligence Chips Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Artificial Intelligence Chips Volume (K), by Application 2025 & 2033

- Figure 5: North America Artificial Intelligence Chips Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Artificial Intelligence Chips Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Artificial Intelligence Chips Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Artificial Intelligence Chips Volume (K), by Types 2025 & 2033

- Figure 9: North America Artificial Intelligence Chips Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Artificial Intelligence Chips Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Artificial Intelligence Chips Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Artificial Intelligence Chips Volume (K), by Country 2025 & 2033

- Figure 13: North America Artificial Intelligence Chips Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Artificial Intelligence Chips Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Artificial Intelligence Chips Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Artificial Intelligence Chips Volume (K), by Application 2025 & 2033

- Figure 17: South America Artificial Intelligence Chips Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Artificial Intelligence Chips Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Artificial Intelligence Chips Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Artificial Intelligence Chips Volume (K), by Types 2025 & 2033

- Figure 21: South America Artificial Intelligence Chips Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Artificial Intelligence Chips Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Artificial Intelligence Chips Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Artificial Intelligence Chips Volume (K), by Country 2025 & 2033

- Figure 25: South America Artificial Intelligence Chips Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Artificial Intelligence Chips Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Artificial Intelligence Chips Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Artificial Intelligence Chips Volume (K), by Application 2025 & 2033

- Figure 29: Europe Artificial Intelligence Chips Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Artificial Intelligence Chips Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Artificial Intelligence Chips Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Artificial Intelligence Chips Volume (K), by Types 2025 & 2033

- Figure 33: Europe Artificial Intelligence Chips Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Artificial Intelligence Chips Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Artificial Intelligence Chips Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Artificial Intelligence Chips Volume (K), by Country 2025 & 2033

- Figure 37: Europe Artificial Intelligence Chips Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Artificial Intelligence Chips Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Artificial Intelligence Chips Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Artificial Intelligence Chips Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Artificial Intelligence Chips Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Artificial Intelligence Chips Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Artificial Intelligence Chips Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Artificial Intelligence Chips Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Artificial Intelligence Chips Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Artificial Intelligence Chips Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Artificial Intelligence Chips Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Artificial Intelligence Chips Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Artificial Intelligence Chips Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Artificial Intelligence Chips Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Artificial Intelligence Chips Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Artificial Intelligence Chips Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Artificial Intelligence Chips Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Artificial Intelligence Chips Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Artificial Intelligence Chips Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Artificial Intelligence Chips Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Artificial Intelligence Chips Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Artificial Intelligence Chips Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Artificial Intelligence Chips Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Artificial Intelligence Chips Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Artificial Intelligence Chips Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Artificial Intelligence Chips Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Artificial Intelligence Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Artificial Intelligence Chips Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Artificial Intelligence Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Artificial Intelligence Chips Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Artificial Intelligence Chips Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Artificial Intelligence Chips Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Artificial Intelligence Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Artificial Intelligence Chips Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Artificial Intelligence Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Artificial Intelligence Chips Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Artificial Intelligence Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Artificial Intelligence Chips Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Artificial Intelligence Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Artificial Intelligence Chips Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Artificial Intelligence Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Artificial Intelligence Chips Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Artificial Intelligence Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Artificial Intelligence Chips Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Artificial Intelligence Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Artificial Intelligence Chips Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Artificial Intelligence Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Artificial Intelligence Chips Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Artificial Intelligence Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Artificial Intelligence Chips Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Artificial Intelligence Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Artificial Intelligence Chips Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Artificial Intelligence Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Artificial Intelligence Chips Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Artificial Intelligence Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Artificial Intelligence Chips Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Artificial Intelligence Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Artificial Intelligence Chips Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Artificial Intelligence Chips Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Artificial Intelligence Chips Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Artificial Intelligence Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Artificial Intelligence Chips Volume K Forecast, by Country 2020 & 2033

- Table 79: China Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Artificial Intelligence Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Artificial Intelligence Chips Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Artificial Intelligence Chips?

The projected CAGR is approximately 15.7%.

2. Which companies are prominent players in the Artificial Intelligence Chips?

Key companies in the market include Huawei Technologies, Qualcomm, IBM Corporation, NVIDIA Corporation, Intel Corporation, MediaTek Inc, Cerebras Systems, Samsung Electronics, Advanced Micro Devices, Apple Inc, Google Inc, ARM, Intel, Graphcore, LG, Imagination Technologies, Anari.

3. What are the main segments of the Artificial Intelligence Chips?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Artificial Intelligence Chips," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Artificial Intelligence Chips report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Artificial Intelligence Chips?

To stay informed about further developments, trends, and reports in the Artificial Intelligence Chips, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence