Key Insights

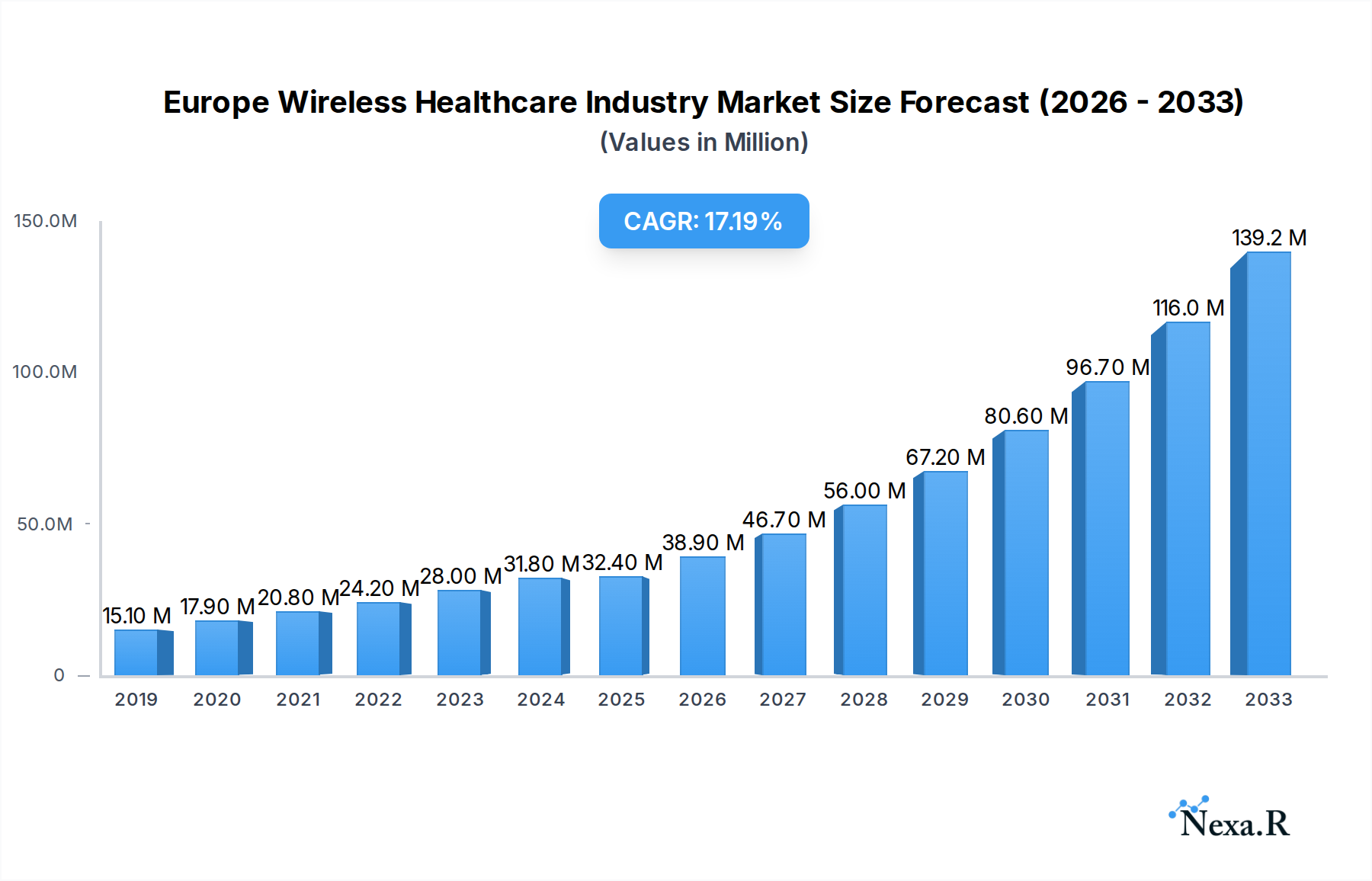

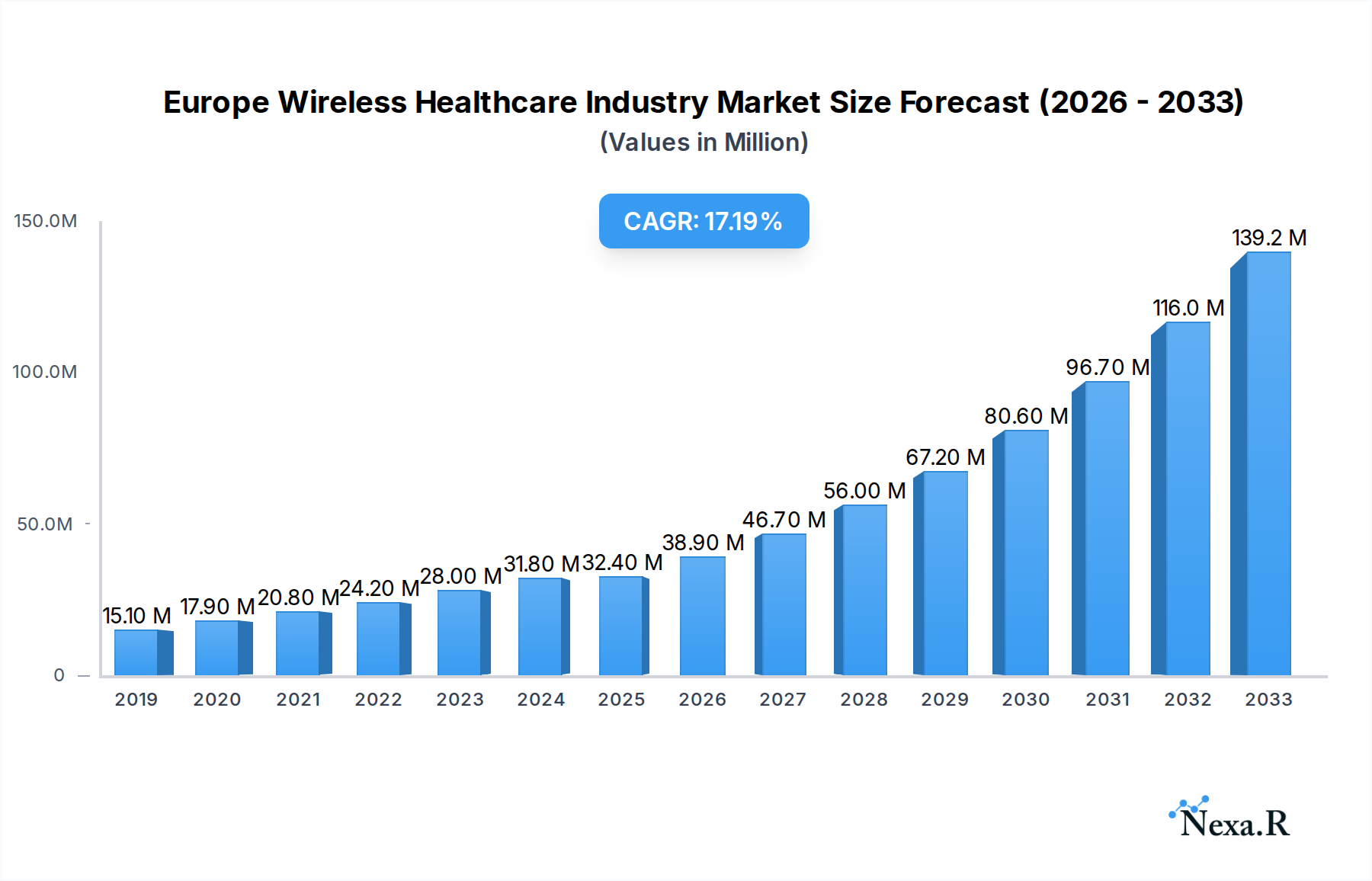

The Europe Wireless Healthcare Industry is poised for significant expansion, projected to reach a market size of $32.40 million by 2025, with a remarkable Compound Annual Growth Rate (CAGR) of 20.82% anticipated through 2033. This robust growth trajectory is fueled by an increasing demand for remote patient monitoring, enhanced hospital efficiency through interconnected devices, and the burgeoning adoption of digital health solutions across the continent. Key drivers include the escalating prevalence of chronic diseases, necessitating continuous care and monitoring capabilities, coupled with favorable regulatory environments promoting telehealth and digital health innovation. Furthermore, advancements in wireless technologies, such as 5G deployment, are enabling seamless data transmission and real-time analytics, paving the way for more sophisticated and accessible healthcare services. The industry is witnessing a strong focus on integrated solutions encompassing hardware, software, and services, with applications spanning hospitals, nursing homes, home care settings, and the pharmaceutical sector.

Europe Wireless Healthcare Industry Market Size (In Million)

The competitive landscape is characterized by the presence of major technology and healthcare giants, all vying to capture a significant share of this rapidly evolving market. Strategic collaborations, mergers, and acquisitions are expected to shape the industry dynamics as companies seek to expand their product portfolios and geographical reach. The trend towards personalized medicine and preventative healthcare, empowered by wireless connectivity, will continue to drive innovation in areas like wearable health trackers, smart medical devices, and secure patient data management systems. While the growth outlook is overwhelmingly positive, potential restraints could include data security and privacy concerns, the need for robust IT infrastructure upgrades in some healthcare facilities, and the complexities of interoperability between different systems. However, the overwhelming benefits of improved patient outcomes, reduced healthcare costs, and increased accessibility to medical expertise are expected to outweigh these challenges, solidifying the European wireless healthcare market's upward trend.

Europe Wireless Healthcare Industry Company Market Share

Europe Wireless Healthcare Industry Market Report: Unlocking Next-Generation Patient Care

This comprehensive report delivers a definitive analysis of the Europe Wireless Healthcare Industry, a rapidly evolving sector poised for significant growth. With the increasing demand for remote patient monitoring, enhanced data connectivity, and efficient healthcare delivery, wireless technologies are revolutionizing patient care across the continent. Our research provides in-depth insights into market dynamics, growth trends, regional dominance, product landscapes, key drivers, challenges, emerging opportunities, and strategic collaborations. We analyze parent and child market segments to offer a granular understanding of this dynamic industry, projecting a market size of $XXX Million Units by 2033.

Europe Wireless Healthcare Industry Market Dynamics & Structure

The Europe Wireless Healthcare Industry is characterized by a moderately concentrated market, driven by substantial technological innovation and evolving regulatory frameworks. Key drivers include the escalating adoption of Internet of Medical Things (IoMT) devices, advancements in 5G connectivity, and the growing need for remote patient monitoring solutions. Regulatory bodies are actively shaping the landscape, focusing on data security, privacy (GDPR compliance), and interoperability standards to ensure patient safety and effective technology integration. Competitive product substitutes are emerging, ranging from wired monitoring systems to alternative telehealth platforms, intensifying the need for differentiated value propositions. End-user demographics, particularly the aging European population and the rise of chronic diseases, are fueling the demand for accessible and continuous healthcare solutions. Mergers and acquisitions (M&A) are a significant trend, with companies consolidating to expand their product portfolios, geographical reach, and technological capabilities. For instance, the market has witnessed XX M&A deals in the historical period (2019-2024), indicating a strong consolidation drive. Innovation barriers primarily stem from the high cost of initial technology deployment, the need for extensive clinical validation, and challenges in achieving seamless integration with existing healthcare IT infrastructure.

- Market Concentration: Moderately concentrated with a few key players holding significant market share.

- Technological Innovation Drivers: IoMT, 5G, AI in healthcare, wearable sensors, cloud computing.

- Regulatory Frameworks: GDPR, MDR (Medical Device Regulation), national health authority guidelines.

- Competitive Product Substitutes: Wired monitoring systems, traditional in-person consultations, basic telemedicine platforms.

- End-User Demographics: Aging population, increasing prevalence of chronic diseases, demand for personalized medicine.

- M&A Trends: Strategic acquisitions to gain market share, expand product offerings, and acquire new technologies.

Europe Wireless Healthcare Industry Growth Trends & Insights

The Europe Wireless Healthcare Industry is projected to experience robust growth, driven by a confluence of technological advancements and shifting healthcare paradigms. The market size is anticipated to grow from an estimated $XXX Million Units in the Base Year 2025 to $XXX Million Units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period (2025-2033). This impressive trajectory is underpinned by increasing adoption rates of wireless health technologies across various applications, from hospitals and nursing homes to home care settings. Technological disruptions, such as the proliferation of AI-powered diagnostics and the development of miniaturized, energy-efficient sensors, are further accelerating market penetration. Consumer behavior shifts are also playing a pivotal role, with patients demonstrating a growing preference for proactive health management and convenient remote care options. This trend is amplified by the increasing digital literacy of the population and a greater willingness to engage with connected health devices. The COVID-19 pandemic acted as a significant catalyst, accelerating the adoption of telehealth and remote monitoring solutions, creating a lasting behavioral change in how healthcare is accessed and delivered.

The market penetration of wireless healthcare solutions is expected to rise steadily, fueled by supportive government initiatives and increasing healthcare expenditure across European nations. Investments in digital health infrastructure and the drive towards value-based healthcare models are creating a fertile ground for wireless technologies. For example, the ongoing digital transformation of healthcare systems in countries like Germany, France, and the UK is a key indicator of this growth. The development of more sophisticated wearable devices capable of continuous, real-time physiological monitoring, coupled with advanced data analytics platforms, will enable early detection of diseases and personalized treatment plans, thereby reducing hospital readmissions and improving patient outcomes. Furthermore, the integration of wireless technologies into emergency response systems and chronic disease management programs will unlock significant market potential. The growing demand for home healthcare services, driven by an aging population and a desire for comfort and convenience, will necessitate the widespread deployment of reliable and secure wireless monitoring solutions.

Dominant Regions, Countries, or Segments in Europe Wireless Healthcare Industry

The Hospitals and Nursing Homes application segment is emerging as the dominant force within the Europe Wireless Healthcare Industry, exhibiting exceptional growth potential and market penetration. This segment is driven by the imperative for hospitals to enhance patient care efficiency, reduce operational costs, and improve patient safety through continuous monitoring and real-time data access. The integration of wireless patient monitoring systems, such as GE Healthcare's Portrait Mobile, allows for uninterrupted patient oversight, facilitating early detection of critical changes and enabling timely interventions, thereby reducing adverse events and improving patient outcomes. Furthermore, hospitals are leveraging wireless technologies for asset tracking, staff communication, and medication management, streamlining workflows and optimizing resource allocation.

Key Drivers for Dominance in Hospitals and Nursing Homes:

- Improved Patient Monitoring & Safety: Continuous, real-time data from wireless sensors aids in proactive patient care and early detection of deterioration.

- Enhanced Operational Efficiency: Streamlined communication, asset tracking, and workflow optimization reduce administrative burdens and improve resource utilization.

- Reduced Hospital Readmissions: Effective remote monitoring and timely interventions contribute to better patient recovery and fewer readmissions.

- Supportive Regulatory Environment: Initiatives promoting digital health adoption within healthcare institutions.

- Technological Advancements: Availability of sophisticated wireless patient monitoring systems and integrated healthcare IT solutions.

The Hardware component segment, encompassing wireless sensors, medical devices, and connectivity modules, plays a crucial role in enabling the functionality of wireless healthcare solutions. This segment is experiencing substantial demand, driven by the continuous innovation in miniaturization, power efficiency, and data transmission capabilities of these devices. Companies like Qualcomm Inc. are at the forefront of developing advanced chipsets that power these sophisticated medical devices, ensuring reliable connectivity and high-performance data processing. The Software segment, including electronic health record (EHR) integration platforms, telehealth software, and data analytics tools, is also a critical growth area, facilitating the management, analysis, and secure transmission of patient data. The Services segment, encompassing installation, maintenance, technical support, and consulting, is essential for the seamless deployment and ongoing operation of wireless healthcare systems.

Dominant Countries Driving Growth:

- Germany: With a strong healthcare infrastructure and a proactive approach to digital health adoption, Germany leads in the implementation of wireless healthcare solutions in hospitals and for home care.

- United Kingdom: Government initiatives and a robust private healthcare sector are accelerating the adoption of wireless technologies, particularly in remote patient monitoring and telehealth services.

- France: Significant investments in healthcare modernization and the increasing demand for advanced medical devices are propelling the growth of the wireless healthcare market in France.

Europe Wireless Healthcare Industry Product Landscape

The Europe Wireless Healthcare Industry is characterized by a rapidly evolving product landscape, marked by continuous innovation in connected medical devices and intelligent software solutions. Key product categories include wireless patient monitoring systems, wearable health trackers, remote diagnostic tools, and telehealth platforms. For instance, GE Healthcare's Portrait Mobile exemplifies the trend towards sophisticated, patient-worn wireless sensors that facilitate continuous monitoring and early detection of patient deterioration. Tunstall Healthcare's expansion into the German market highlights the growing demand for integrated telehealth and telecare solutions that combine software, services, and advanced technology. Unique selling propositions revolve around enhanced data accuracy, real-time connectivity, improved patient comfort, and seamless integration with existing healthcare ecosystems. Technological advancements are focusing on miniaturization, increased battery life, enhanced data security, and the application of artificial intelligence for predictive analytics.

Key Drivers, Barriers & Challenges in Europe Wireless Healthcare Industry

The Europe Wireless Healthcare Industry is propelled by several key drivers, including the increasing demand for remote patient monitoring to manage chronic diseases and an aging population, alongside the growing adoption of IoMT devices for enhanced data collection and analysis. The development of 5G infrastructure promises faster and more reliable connectivity, crucial for real-time healthcare applications. Government initiatives promoting digital health adoption and favorable reimbursement policies for telehealth services further accelerate market growth.

- Technological Advancement: Miniaturization of sensors, AI integration, improved connectivity (5G).

- Demographic Shifts: Aging population, rise in chronic diseases.

- Healthcare System Reforms: Focus on efficiency, cost reduction, and value-based care.

- Patient Demand: Preference for convenience, personalized care, and proactive health management.

However, the industry faces significant barriers and challenges. High initial investment costs for implementing wireless healthcare infrastructure, concerns regarding data security and patient privacy (GDPR compliance), and the lack of interoperability between different systems remain critical hurdles. Stringent regulatory approval processes for medical devices and the need for extensive clinical validation also contribute to slower adoption rates. Supply chain disruptions and the availability of skilled personnel to manage and maintain these advanced systems further complicate market expansion.

- High Implementation Costs: Significant upfront investment required for technology and infrastructure.

- Data Security & Privacy Concerns: Ensuring compliance with stringent regulations like GDPR.

- Interoperability Issues: Challenges in integrating diverse wireless devices and platforms with existing EHRs.

- Regulatory Hurdles: Lengthy approval processes for new medical devices.

- Workforce Shortages: Lack of skilled professionals for implementation and maintenance.

Emerging Opportunities in Europe Wireless Healthcare Industry

Emerging opportunities in the Europe Wireless Healthcare Industry lie in the untapped potential of personalized and preventative healthcare through advanced wearable biosensors and AI-driven predictive analytics. The expansion of home care services, driven by an aging population and a preference for in-home treatment, presents a significant avenue for remote patient monitoring solutions. Furthermore, the integration of wireless technologies in mental health services, offering remote therapy sessions and monitoring of patient well-being, represents a nascent but growing market. The development of specialized wireless solutions for niche applications, such as remote rehabilitation and post-operative care, also offers substantial growth prospects.

Growth Accelerators in the Europe Wireless Healthcare Industry Industry

Several factors are acting as significant growth accelerators for the Europe Wireless Healthcare Industry. The rapid advancements in wireless communication technologies, particularly the rollout of 5G networks, are enabling faster data transmission and more reliable connectivity for critical healthcare applications. Strategic partnerships between technology providers, healthcare institutions, and pharmaceutical companies are fostering innovation and accelerating the development of integrated wireless healthcare solutions. For instance, collaborations between companies like Verizon Communication Inc. and healthcare providers are enhancing connectivity for remote patient monitoring. Market expansion strategies, including a focus on underserved regions and the development of cost-effective solutions, are also driving widespread adoption.

Key Players Shaping the Europe Wireless Healthcare Industry Market

- Motorola Solutions Inc

- Allscripts Healthcare Solutions Inc

- Verizon Communication Inc

- Samsung Electronics Co Ltd

- Cisco Systems Inc

- Philips Healthcare

- Extreme Networks Inc

- Apple Inc

- AT&T Inc

- Qualcomm Inc

Notable Milestones in Europe Wireless Healthcare Industry Sector

- June 2022: GE Healthcare introduced Portrait Mobile, a wireless patient monitoring system featuring continuously monitoring, patient-worn wireless sensors that communicate with a mobile monitor, assisting clinicians in detecting patient deterioration.

- March 2022: Tunstall Healthcare expanded its presence in the German market and service offering through the acquisition of BeWo Unternehmensgruppe (BeWo), a United Kingdom-based provider of software solutions, services, and technology for telehealth and telecare.

In-Depth Europe Wireless Healthcare Industry Market Outlook

The future outlook for the Europe Wireless Healthcare Industry is exceptionally promising, driven by a sustained focus on patient-centric care and operational efficiency. Growth accelerators include the ongoing development of more sophisticated and accessible IoMT devices, coupled with advancements in AI for personalized health insights and predictive diagnostics. The increasing adoption of telehealth platforms and remote monitoring solutions, further supported by favorable regulatory landscapes and evolving reimbursement models, will continue to shape market expansion. Strategic collaborations among technology developers, healthcare providers, and insurance companies are expected to foster innovation and accelerate the integration of wireless healthcare into mainstream patient care, unlocking substantial future market potential and creating new avenues for strategic investments.

Europe Wireless Healthcare Industry Segmentation

-

1. Component

- 1.1. Hardware

- 1.2. Software

- 1.3. Services

-

2. Application

- 2.1. Hospitals and Nursing Homes

- 2.2. Home Care

- 2.3. Pharmaceuticals

- 2.4. Other Applications

Europe Wireless Healthcare Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

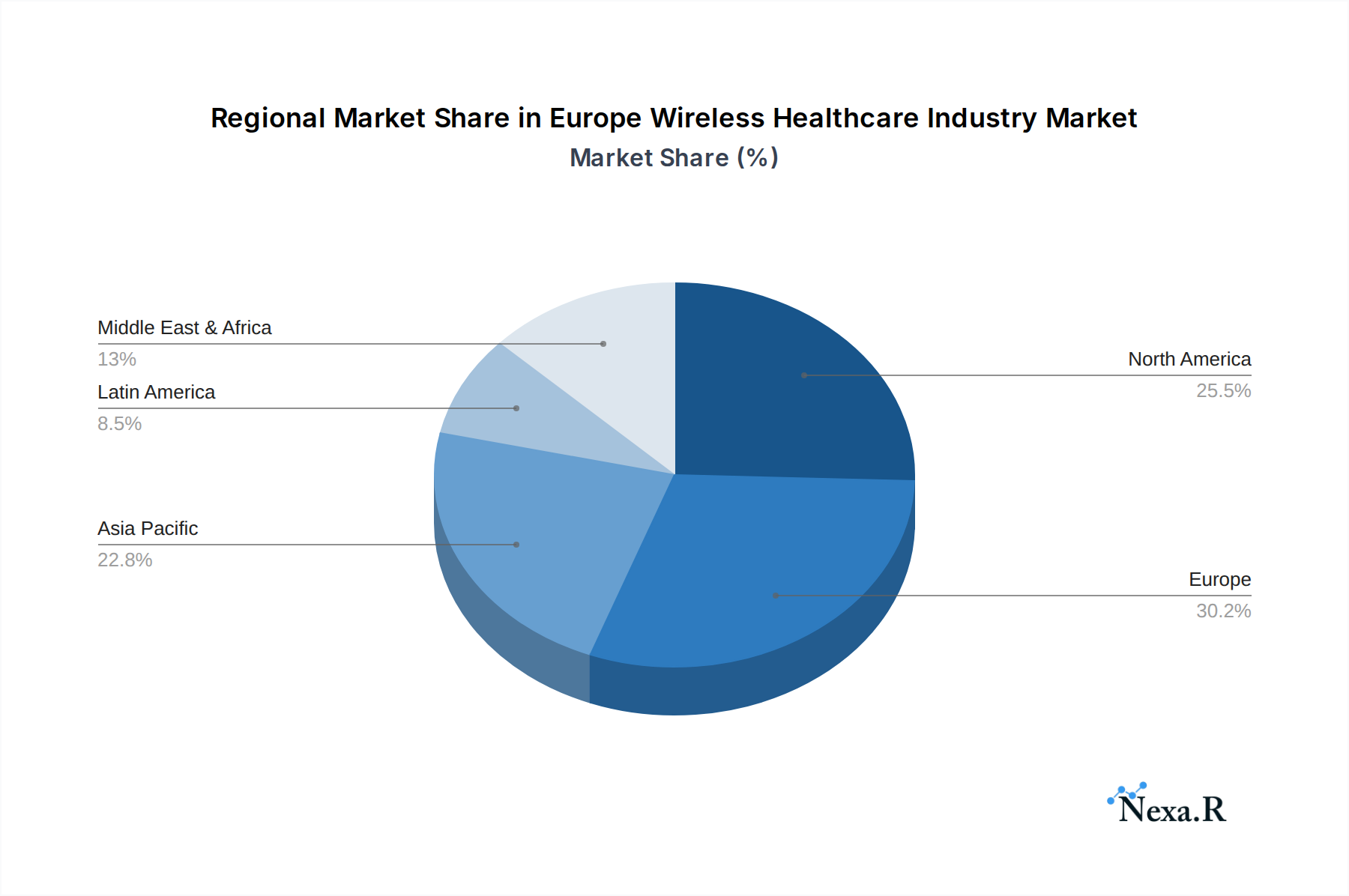

Europe Wireless Healthcare Industry Regional Market Share

Geographic Coverage of Europe Wireless Healthcare Industry

Europe Wireless Healthcare Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.82% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.2. Software

- 5.1.3. Services

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Hospitals and Nursing Homes

- 5.2.2. Home Care

- 5.2.3. Pharmaceuticals

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Europe Wireless Healthcare Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.2. Software

- 6.1.3. Services

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Hospitals and Nursing Homes

- 6.2.2. Home Care

- 6.2.3. Pharmaceuticals

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Motorola Solutions Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Allscripts Healthcare Solutions Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Verizon Communication Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Samsung Electronics Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Cisco Systems Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Philips Healthcare

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Extreme Networks Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Apple Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AT&T Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Qualcomm Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Motorola Solutions Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Wireless Healthcare Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Wireless Healthcare Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Wireless Healthcare Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 2: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 3: Europe Wireless Healthcare Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Europe Wireless Healthcare Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Europe Wireless Healthcare Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 8: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 9: Europe Wireless Healthcare Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: Europe Wireless Healthcare Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Europe Wireless Healthcare Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Germany Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: France Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Italy Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Italy Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Spain Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Spain Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Netherlands Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Netherlands Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Belgium Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Belgium Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Sweden Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Sweden Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Norway Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Norway Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Poland Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Poland Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Denmark Europe Wireless Healthcare Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Denmark Europe Wireless Healthcare Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Wireless Healthcare Industry?

The projected CAGR is approximately 20.82%.

2. Which companies are prominent players in the Europe Wireless Healthcare Industry?

Key companies in the market include Motorola Solutions Inc, Allscripts Healthcare Solutions Inc , Verizon Communication Inc, Samsung Electronics Co Ltd, Cisco Systems Inc, Philips Healthcare, Extreme Networks Inc, Apple Inc, AT&T Inc, Qualcomm Inc.

3. What are the main segments of the Europe Wireless Healthcare Industry?

The market segments include Component, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 32.40 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Connected Devices in Healthcare; Increasing Adoption of Internet of Things (IoT) and Wearable Devices in Healthcare to Drive the Wireless Healthcare Market.

6. What are the notable trends driving market growth?

Home Care is Expected to Gain Significant Share.

7. Are there any restraints impacting market growth?

Lack of Networking Infrastructure; Data Security and Device Certification Challenges; Impact of COVID-19 on the Industry.

8. Can you provide examples of recent developments in the market?

June 2022: GE Healthcare introduced Portrait Mobile, a wireless patient monitoring system that is continuously monitoring a patient’s stay. The wireless patient monitoring system assists clinicians in detecting patient deterioration. Portrait Mobile comprises patient-worn wireless sensors that communicate with a mobile monitor.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Wireless Healthcare Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Wireless Healthcare Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Wireless Healthcare Industry?

To stay informed about further developments, trends, and reports in the Europe Wireless Healthcare Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence